If your bank has charged fees or demanded immediate payment for an unauthorized account overdraft, it is essential to understand your consumer rights. Banks must follow specific legal procedures before reclaiming funds or applying penalties. This guide explains how to dispute wrongful charges and formalize your request for a correction. Below are some ready to use templates to help you take action.

Image cover: Formal Demand Letter Templates for Unauthorized Account Overdrafts

Letter Samples List

- Initial Demand Letter For Repayment Of Unauthorized Account Overdraft

- Second Notice Letter For Unauthorized Overdraft Balance Repayment

- Final Warning Letter For Repayment Of Unauthorized Account Overdraft

- Corporate Banking Letter Demanding Repayment Of Unauthorized Overdraft

- Retail Banking Notice Letter For Unauthorized Overdraft Repayment

- Legal Escalation Letter For Unpaid Unauthorized Account Overdraft

- Overdraft Facility Breach Letter Demanding Immediate Repayment

- Joint Account Letter For Repayment Of Unauthorized Overdraft

- Business Account Overdraft Repayment Demand Letter

- Account Suspension And Overdraft Repayment Demand Letter

- Pre-Litigation Demand Letter For Unauthorized Overdraft Recovery

- Debt Collection Agency Referral Letter For Unauthorized Overdraft

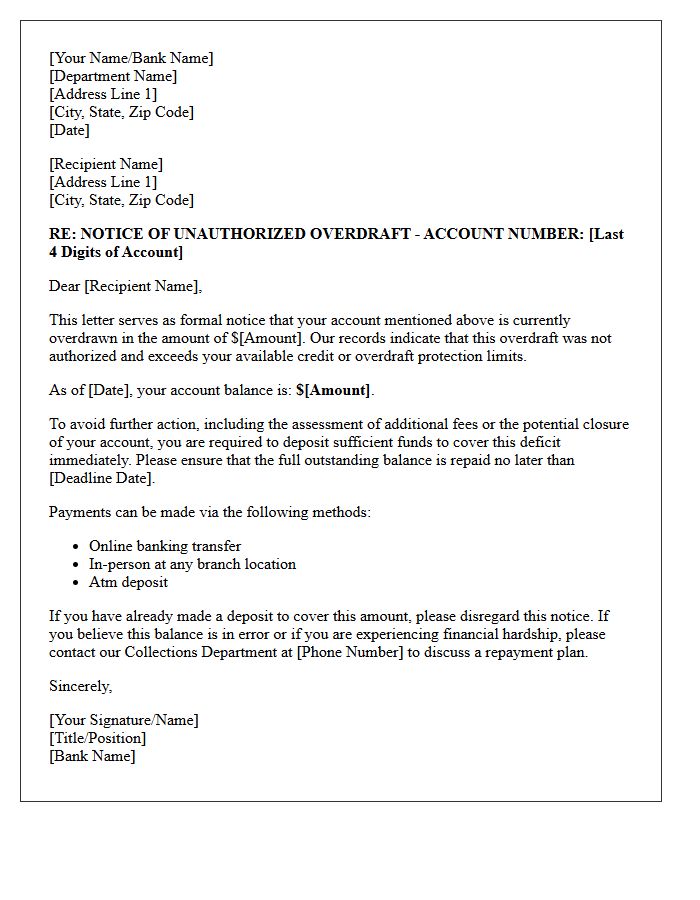

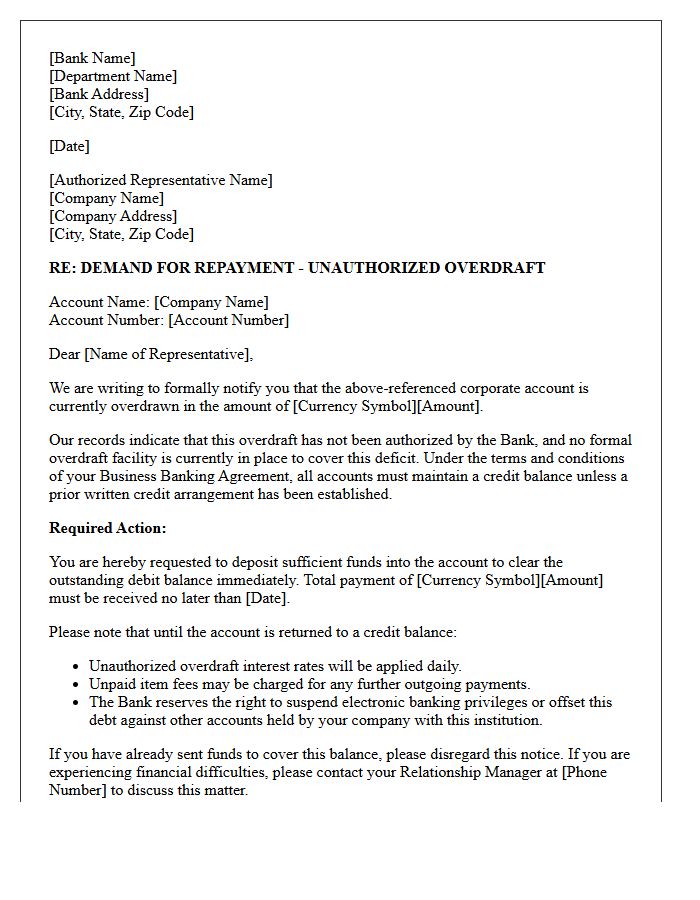

Initial Demand Letter For Repayment Of Unauthorized Account Overdraft

An Initial Demand Letter For Repayment Of Unauthorized Account Overdraft is a formal legal notice issued by a financial institution or creditor. It serves as an official request for the immediate restoration of funds following a negative balance. This document outlines the total debt owed, including accrued interest and administrative penalties. It establishes a strict deadline for repayment to avoid further escalations. Timely action is essential, as ignoring this notification can lead to the permanent closure of the account, credit score damage, and potential litigation or third-party collection efforts.

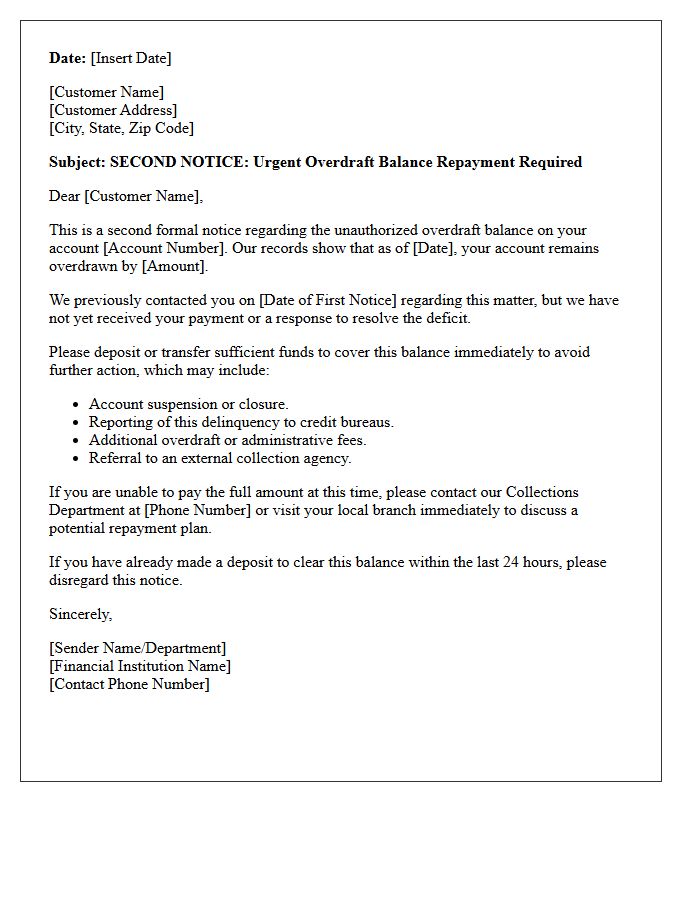

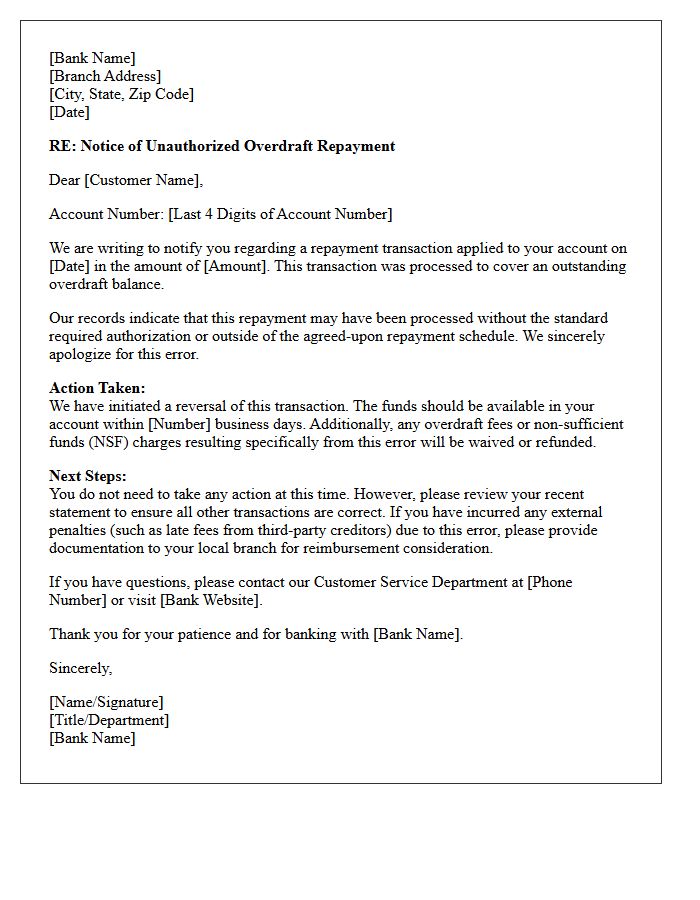

Second Notice Letter For Unauthorized Overdraft Balance Repayment

A Second Notice Letter is a critical formal warning regarding an unauthorized overdraft balance. It signifies that previous requests for repayment have been ignored, and the account remains in default. Receiving this document indicates that the financial institution may soon initiate legal action, report the delinquency to credit bureaus, or transfer the debt to a collection agency. To avoid severe damage to your credit score and potential loss of banking privileges, you must prioritize immediate repayment or contact the bank to establish a formal debt settlement plan.

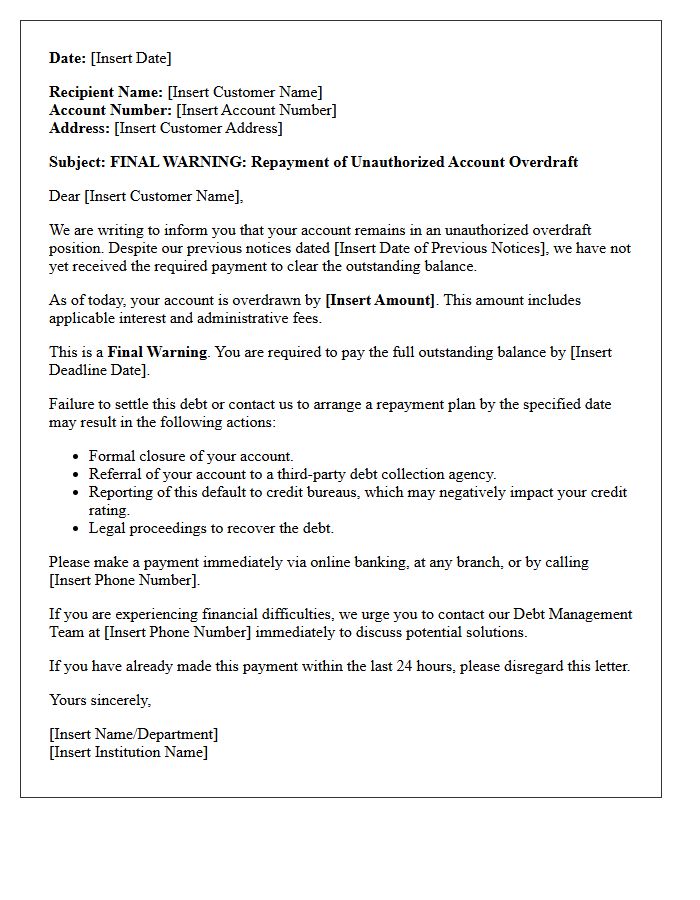

Final Warning Letter For Repayment Of Unauthorized Account Overdraft

A Final Warning Letter for an unauthorized overdraft is a critical legal notice demanding immediate repayment of a negative balance. It signifies the final stage of a bank's internal collection process before escalating the matter to debt collection agencies or initiating legal action. Receiving this letter means your credit score is at risk of severe damage. To prevent account closure and litigation, you must settle the outstanding debt or negotiate a repayment plan immediately. Ignoring this formal demand will lead to additional fees and potential court proceedings.

Corporate Banking Letter Demanding Repayment Of Unauthorized Overdraft

When a business receives a formal demand letter for an unauthorized overdraft, it signifies a breach of the facility agreement. This legal notice requires immediate repayment of the overdrawn balance plus accrued interest and penalty fees. Banks may freeze accounts or initiate recovery proceedings if the debt is not settled promptly. It is critical to review your bank statements and loan covenants to verify the claim. Businesses should prioritize urgent negotiation with their relationship manager to propose a repayment plan and avoid negative impacts on their corporate credit rating.

Retail Banking Notice Letter For Unauthorized Overdraft Repayment

A retail banking notice for unauthorized overdraft repayment is a legal notification informing you of a negative balance. It requires immediate repayment to avoid additional penalties. This letter outlines the specific amount owed, applicable fees, and a deadline for action. Understanding these terms is crucial to prevent account closure or negative impacts on your credit score. If you dispute the charges, contact your bank's customer service promptly to discuss a payment plan or investigate potential errors. Always maintain accurate records of your transactions to ensure financial transparency and avoid unauthorized debt collection activities.

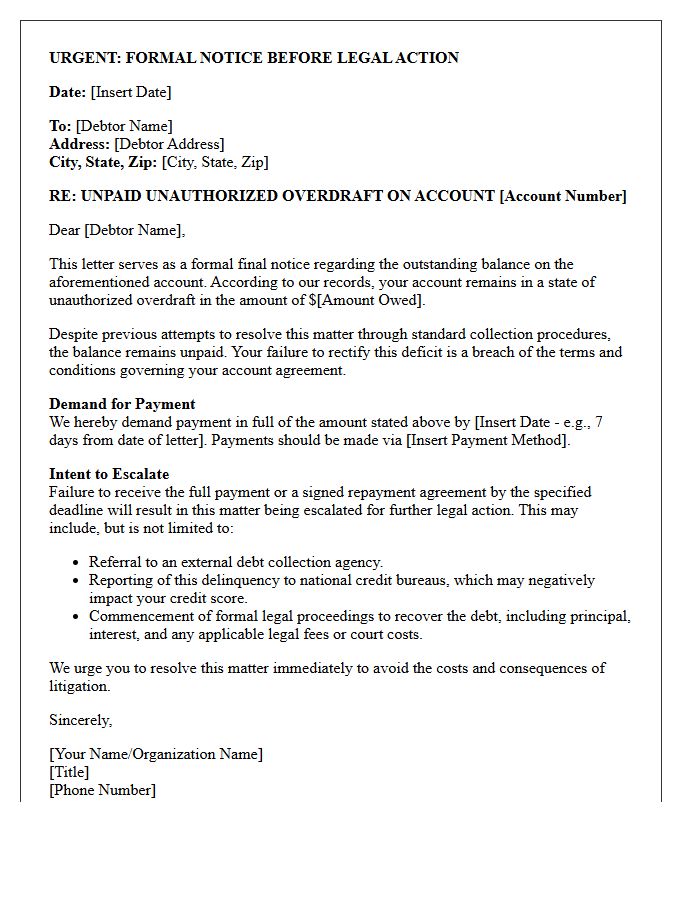

Legal Escalation Letter For Unpaid Unauthorized Account Overdraft

A legal escalation letter is a formal notice sent when a financial institution fails to resolve an unauthorized account overdraft. This document serves as a final demand before pursuing litigation or filing a regulatory complaint. It must detail the specific billing error, the timeline of previous disputes, and the consumer's rights under the Electronic Fund Transfer Act. Sending this letter creates a necessary paper trail, demonstrating that you attempted to settle the debt or error in good faith before seeking legal remedies or involving a consumer protection agency.

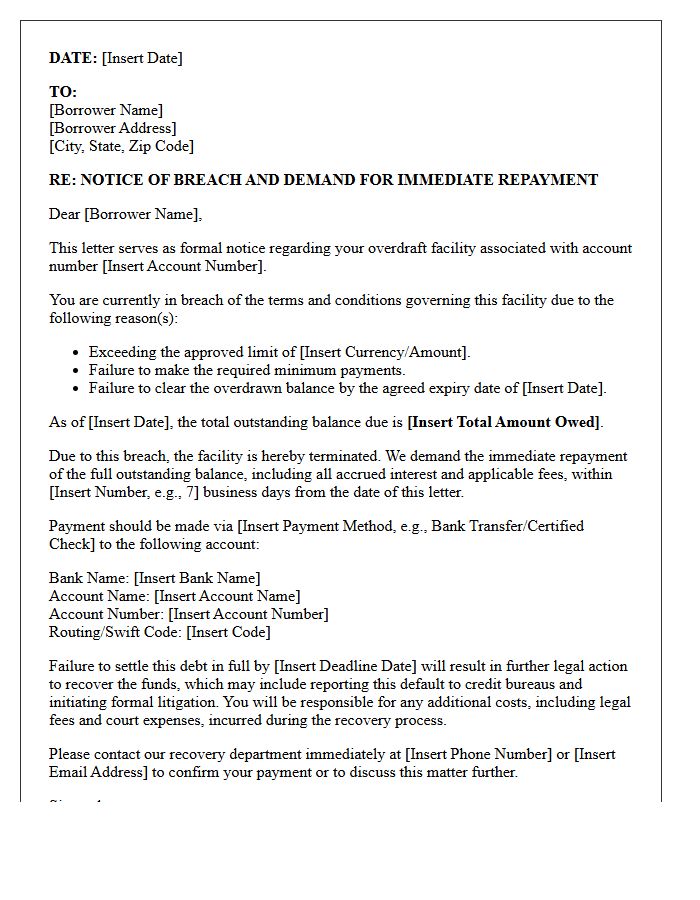

Overdraft Facility Breach Letter Demanding Immediate Repayment

Receiving an Overdraft Facility Breach Letter signifies that you have violated your banking agreement, typically by exceeding a credit limit or missing payments. This formal notice acts as a demand for immediate repayment of the outstanding balance. Failure to settle the debt or negotiate a repayment plan promptly can lead to severe consequences, including the withdrawal of banking facilities, legal action, and negative impacts on your credit rating. It is essential to contact your lender immediately to discuss options and avoid further financial penalties or formal debt collection processes.

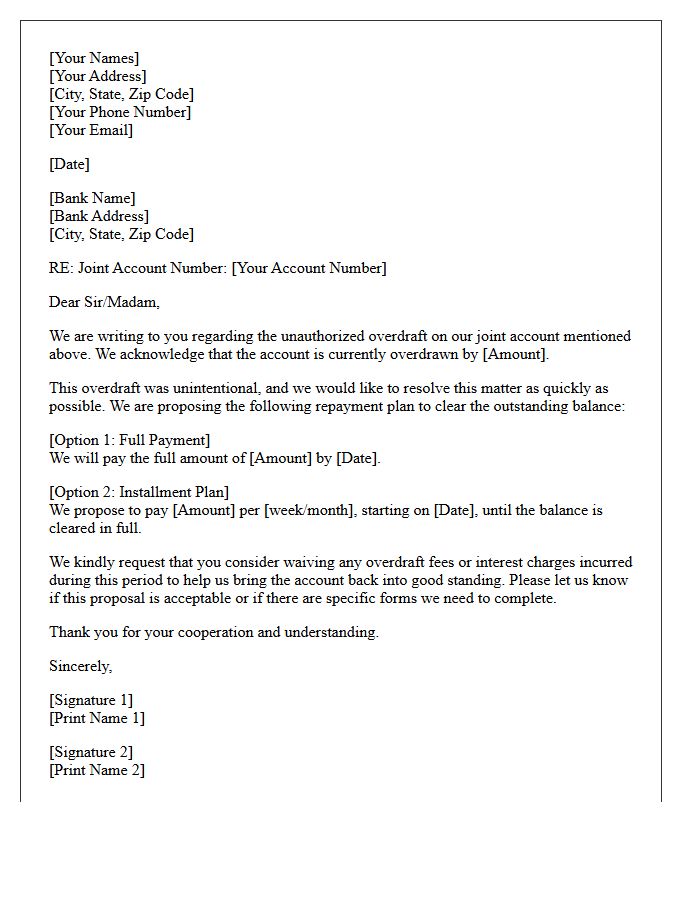

Joint Account Letter For Repayment Of Unauthorized Overdraft

A joint account letter for repayment of an unauthorized overdraft is a formal request to your bank to resolve an unarranged debt. Since all account holders share joint and several liability, each individual is legally responsible for the full balance. The letter should clearly outline a repayment plan or request a fee waiver if the overdraft occurred due to bank error or financial hardship. Submitting this written proposal helps prevent further interest accumulation and protects the credit scores of both parties involved in the agreement.

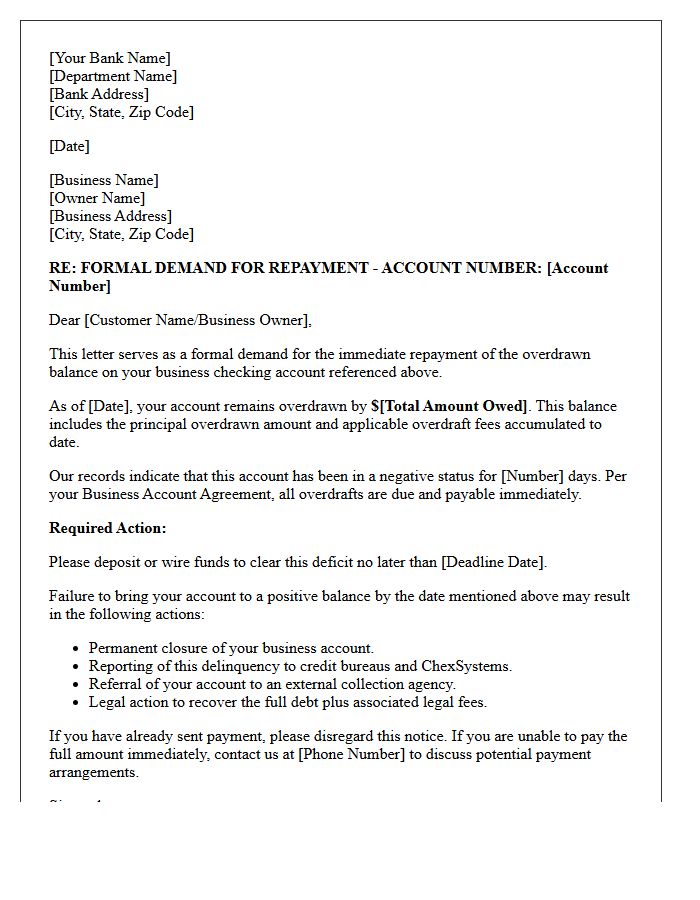

Business Account Overdraft Repayment Demand Letter

A Business Account Overdraft Repayment Demand Letter is a formal notification from a financial institution requiring the immediate settlement of a negative balance. It is legally binding and serves as a final warning before the bank initiates debt collection or legal action. It is imperative to respond promptly to avoid credit score damage or account closure. Business owners should review the outstanding amount for accuracy and contact the bank to negotiate a repayment plan or provide proof of payment to mitigate further financial penalties and protect their commercial reputation.

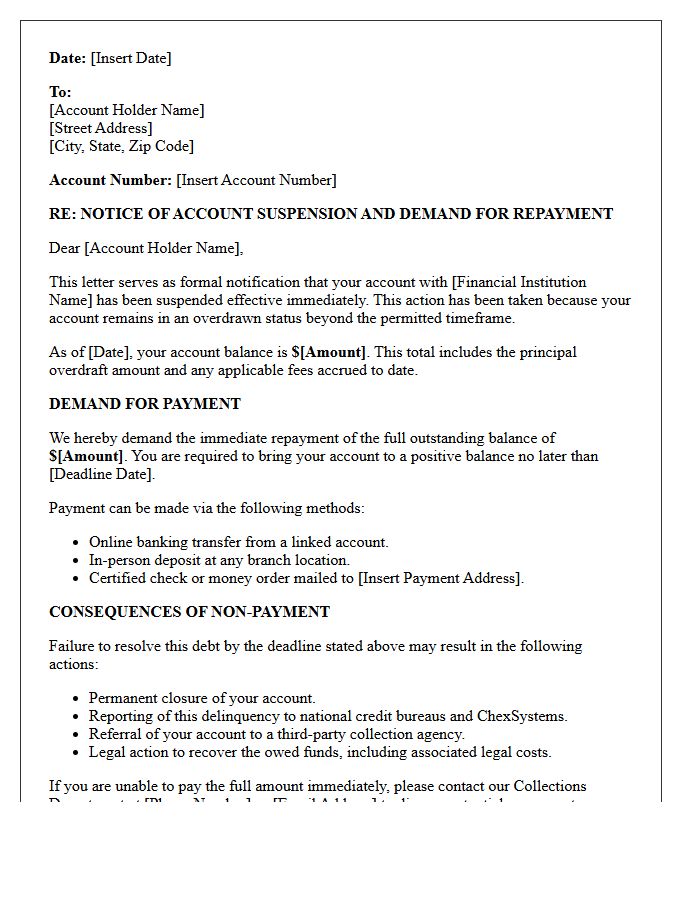

Account Suspension And Overdraft Repayment Demand Letter

Receiving an Account Suspension and Overdraft Repayment Demand Letter is a formal notice that your financial institution has frozen your banking privileges due to a negative balance. This document serves as a legal requirement for you to settle outstanding debts immediately. Failure to comply can lead to collection agency involvement, permanent closure of your account, and severe damage to your credit score. It is essential to communicate with your bank promptly to arrange a repayment plan and prevent further legal action or reporting to specialized consumer reporting agencies like ChexSystems.

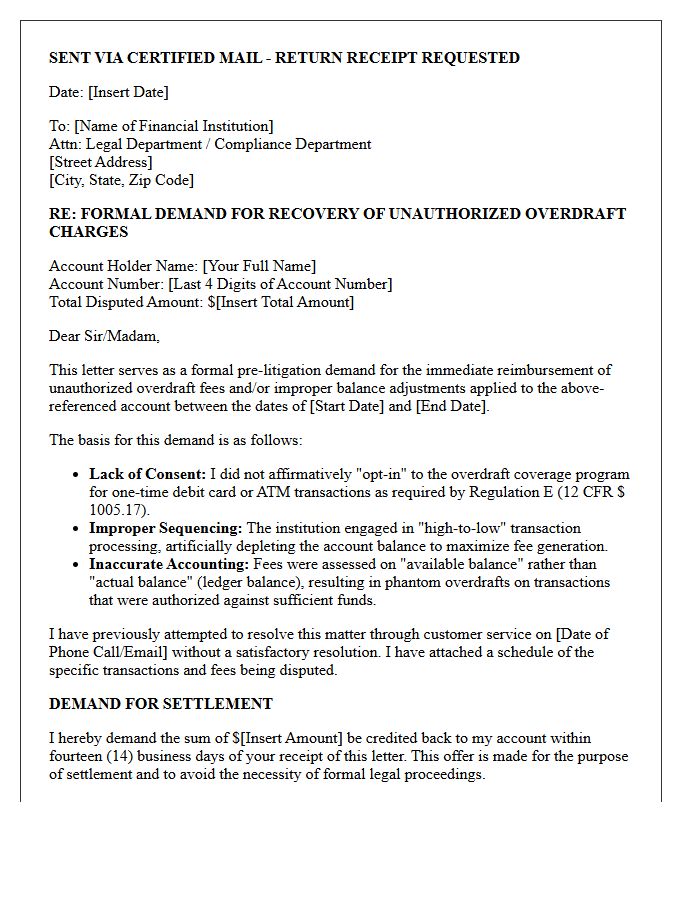

Pre-Litigation Demand Letter For Unauthorized Overdraft Recovery

A Pre-Litigation Demand Letter serves as a formal legal notice to a financial institution regarding unauthorized overdraft fees. This critical document outlines specific transaction errors, breach of contract claims, or regulatory violations. It provides the bank a final opportunity to refund disputed amounts and resolve the dispute through settlement before a lawsuit is filed. By clearly detailing the factual basis and demanding restitution within a set timeframe, the letter establishes a paper trail essential for proving the bank's non-compliance in potential court proceedings or arbitration.

Debt Collection Agency Referral Letter For Unauthorized Overdraft

A debt collection agency referral letter serves as formal notification that an unauthorized overdraft balance remains unpaid. Banks issue this document after multiple internal collection attempts fail. It signals that your account is being transferred to a third-party agency, which can negatively impact your credit score. Before referral, ensure you verify the debt's accuracy and explore repayment options. Promptly addressing this letter is crucial to prevent legal action or additional collection fees. Always request a debt validation notice to confirm the total amount owed and protect your financial rights under consumer laws.

What is a Demand for Repayment of an unauthorized account overdraft?

A Demand for Repayment is a formal notice sent by a financial institution requiring a customer to immediately deposit funds to cover a negative balance incurred without a prior credit agreement or overdraft protection plan.

What are the legal consequences of ignoring an overdraft repayment demand?

Failure to settle an unauthorized overdraft can lead to the closure of your account, reporting to credit bureaus such as ChexSystems or Early Warning Services (EWS), and potential legal action or referral to a third-party debt collection agency.

Can I dispute an unauthorized account overdraft charge?

Yes, if the overdraft was caused by bank error, identity theft, or unauthorized fraudulent transactions, you have the right to dispute the charges under the Electronic Fund Transfer Act (Regulation E) by notifying your bank within 60 days of the statement date.

How long do I have to pay back an unauthorized overdraft before it affects my credit?

Most banks provide a grace period of 30 to 60 days to bring the account balance to zero. After this period, the bank typically "charges off" the debt and reports the delinquency to specialty credit reporting agencies, which can prevent you from opening future bank accounts.

Are there options for a repayment plan if I cannot pay the full overdraft amount immediately?

Many financial institutions offer internal repayment schedules or hardship programs to recover the funds over time. Contacting the bank's collections department early to negotiate a structured payment plan can prevent the debt from being sold to a collection agency.

Comments