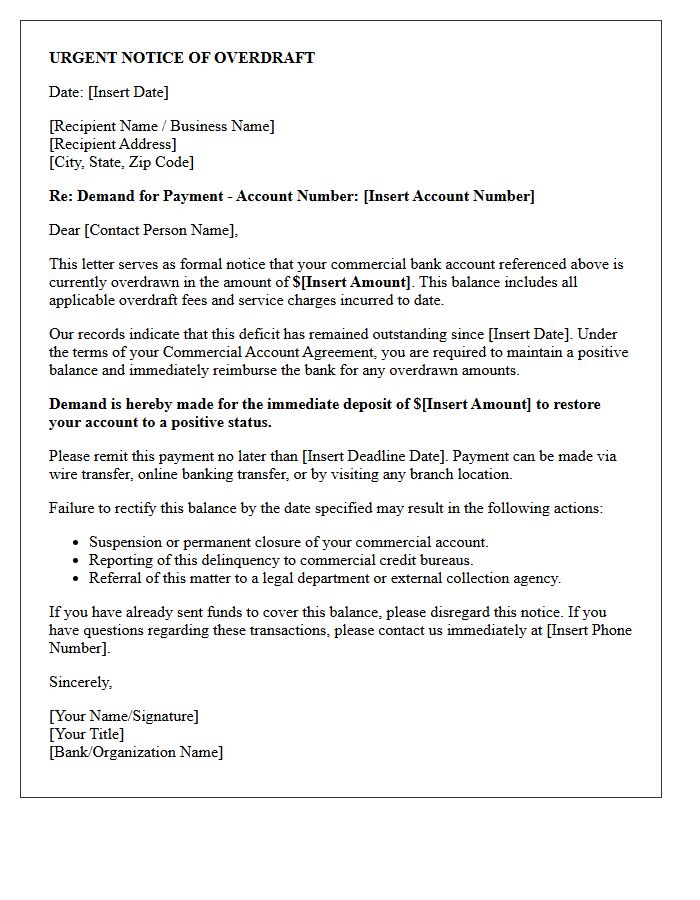

Ignoring an Urgent Notice of Unfunded Overdraft Balance can lead to high penalties and account suspension. It is essential to settle negative balances immediately to maintain your credit standing and avoid legal action from financial institutions. Clear communication with your bank is the first step toward resolving these urgent debt issues. To assist your response, below are some ready to use template.

Image cover: Immediate Action Required: Notice of Unfunded Overdraft Balance and Payment Templates

Letter Samples List

- Initial Overdraft Balance Notification Letter

- Urgent Unfunded Account Deficit Demand Letter

- Second Warning Overdraft Repayment Letter

- Final Notice of Unfunded Balance Letter

- Account Suspension and Overdraft Notice Letter

- Pre-Collections Overdraft Warning Letter

- Overdraft Fee Assessment and Balance Letter

- Unfunded Disbursement Recovery Letter

- Commercial Account Overdraft Demand Letter

- Retail Banking Overdraft Resolution Letter

- Legal Action Pending for Unfunded Overdraft Letter

- Overdraft Settlement Negotiation Letter

- Immediate Overdraft Restitution Request Letter

- Account Closure Due to Unfunded Overdraft Letter

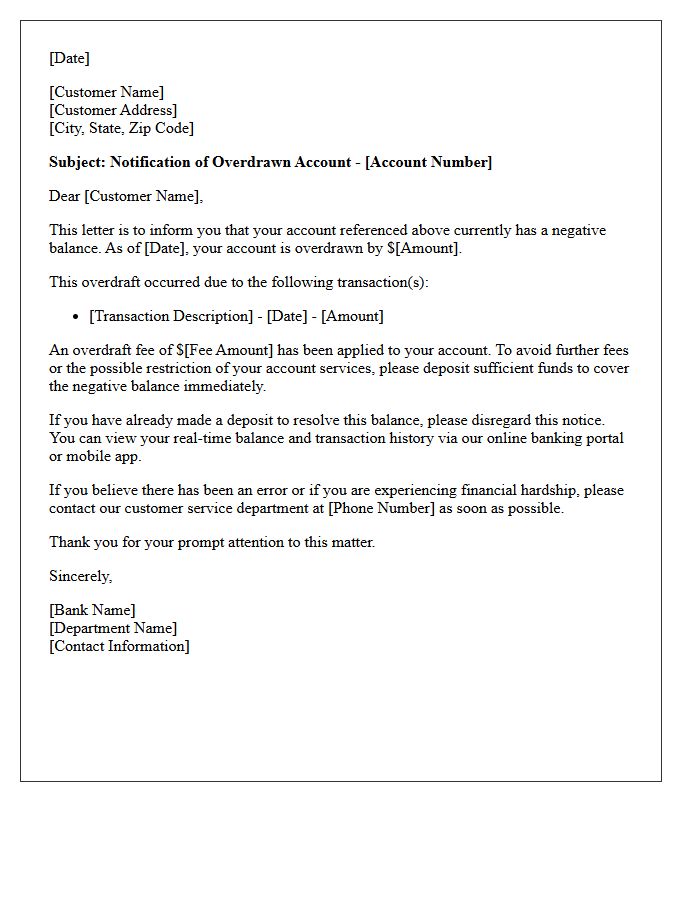

Initial Overdraft Balance Notification Letter

An Initial Overdraft Balance Notification Letter is a formal notice sent by a bank when your account balance falls below zero. This document is essential because it informs you of the outstanding debt and any associated penalties or daily fees. To avoid negative impacts on your credit score or account closure, you must deposit funds immediately to cover the deficit. Understanding this letter helps you manage your liquidity and prevents further financial charges resulting from a prolonged overdrawn status.

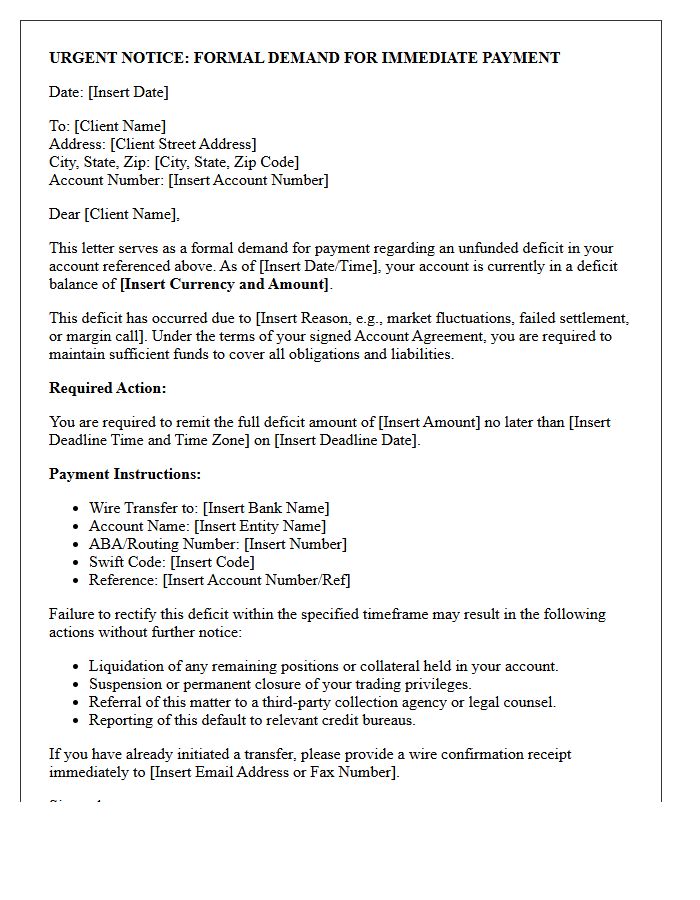

Urgent Unfunded Account Deficit Demand Letter

An Urgent Unfunded Account Deficit Demand Letter is a formal notice from a financial institution requiring immediate payment to cover a negative balance. This legal demand typically triggers a strict deadline, often 24 to 48 hours, to deposit cleared funds. Failure to rectify the margin call or overdraft can result in the forced liquidation of assets, account closure, and potential legal action. Receiving this document signifies a critical financial shortfall that must be addressed instantly to prevent significant credit damage and further institutional penalties.

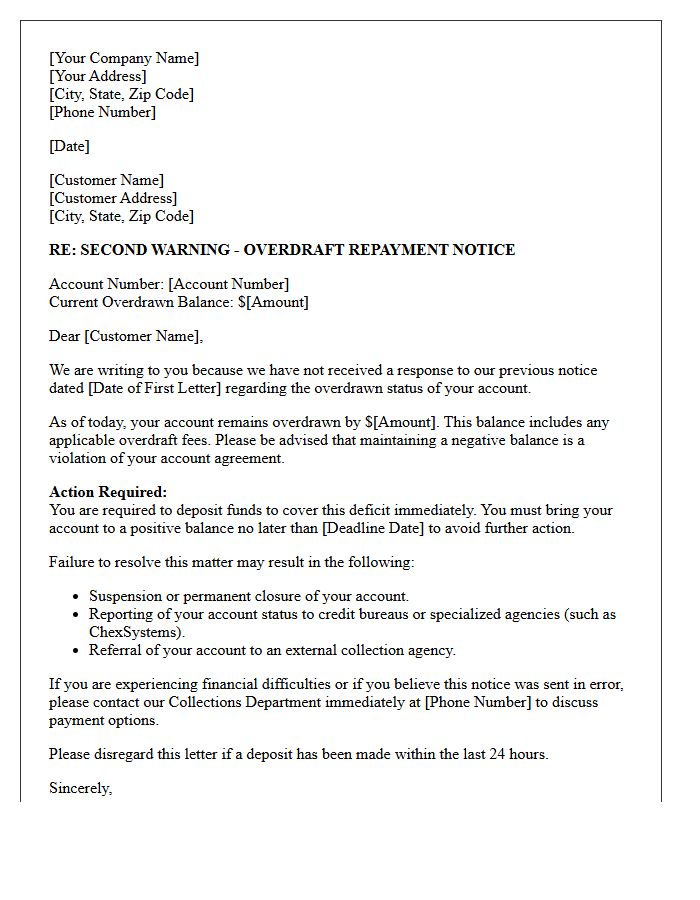

Second Warning Overdraft Repayment Letter

A Second Warning Overdraft Repayment Letter is a formal notice issued by a bank when a customer fails to resolve a negative balance after the initial request. It serves as a final opportunity to settle the debt or establish a repayment plan before the account faces serious consequences. Receiving this letter indicates that the bank may soon terminate your banking relationship, report the default to credit bureaus, or involve external debt collection agencies. Prompt communication is essential to prevent long-term damage to your credit score and future financial accessibility.

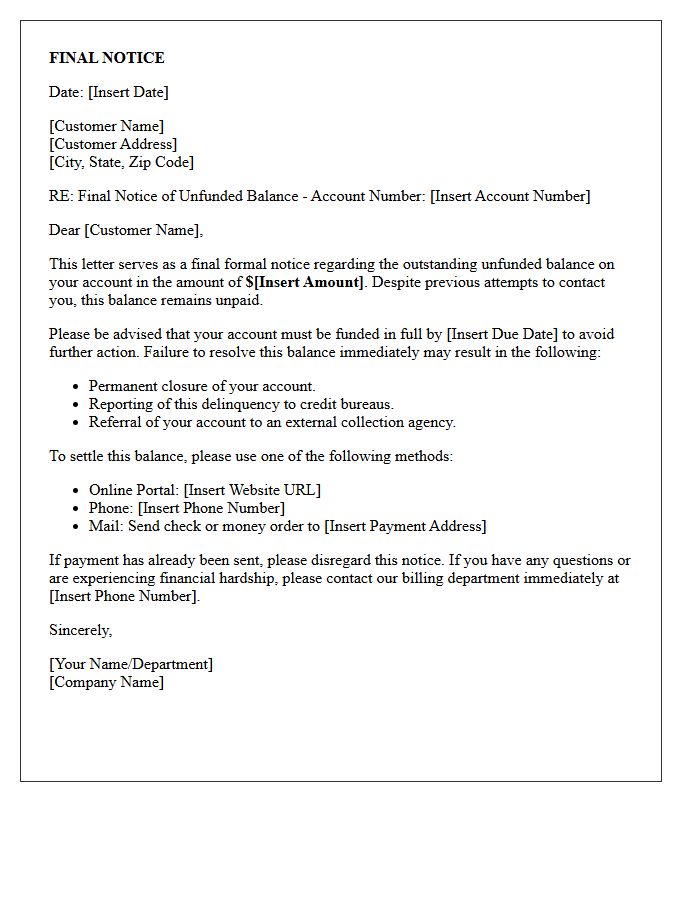

Final Notice of Unfunded Balance Letter

A Final Notice of Unfunded Balance Letter is a critical legal notification issued by a financial institution or service provider. It serves as a formal demand for immediate payment when an account remains in arrears. Receiving this document indicates that previous attempts to collect the debt were unsuccessful. Failure to settle the outstanding amount or establish a payment plan may lead to account suspension, negative credit reporting, or legal action. It is essential to verify the balance accuracy and respond promptly to avoid further penalties or the involvement of collection agencies.

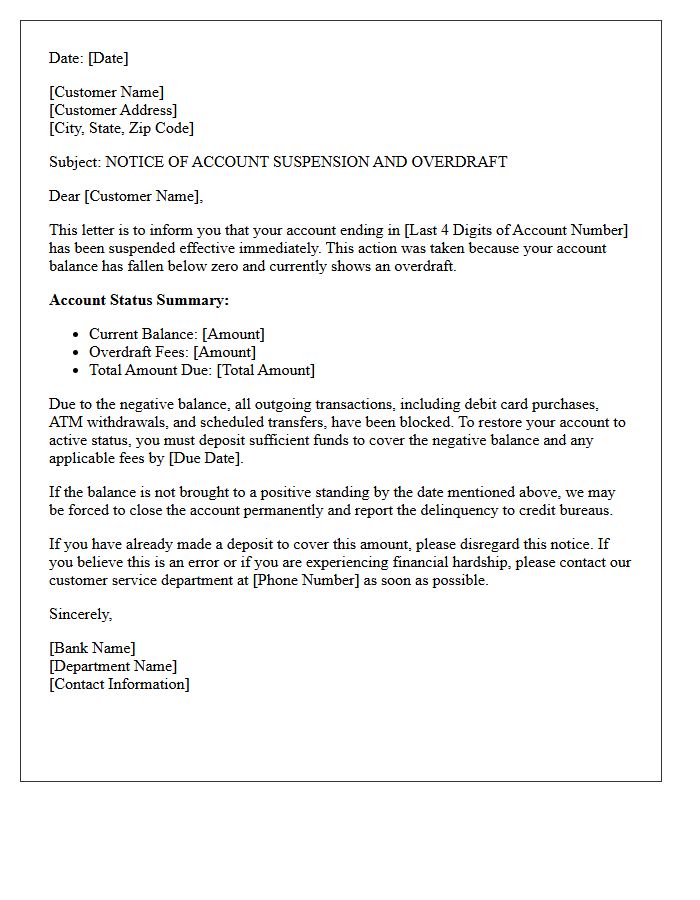

Account Suspension and Overdraft Notice Letter

An Account Suspension and Overdraft Notice is a critical formal communication indicating that your banking privileges are restricted due to a negative balance. This letter serves as a legal warning that you must immediately deposit funds to cover the deficit and associated penalties. Ignoring this notice can lead to permanent account closure, damaged credit scores, and reporting to agencies like ChexSystems. It is essential to contact your financial institution promptly to resolve the debt, negotiate fees, and restore your financial standing before the matter escalates to professional collection agencies.

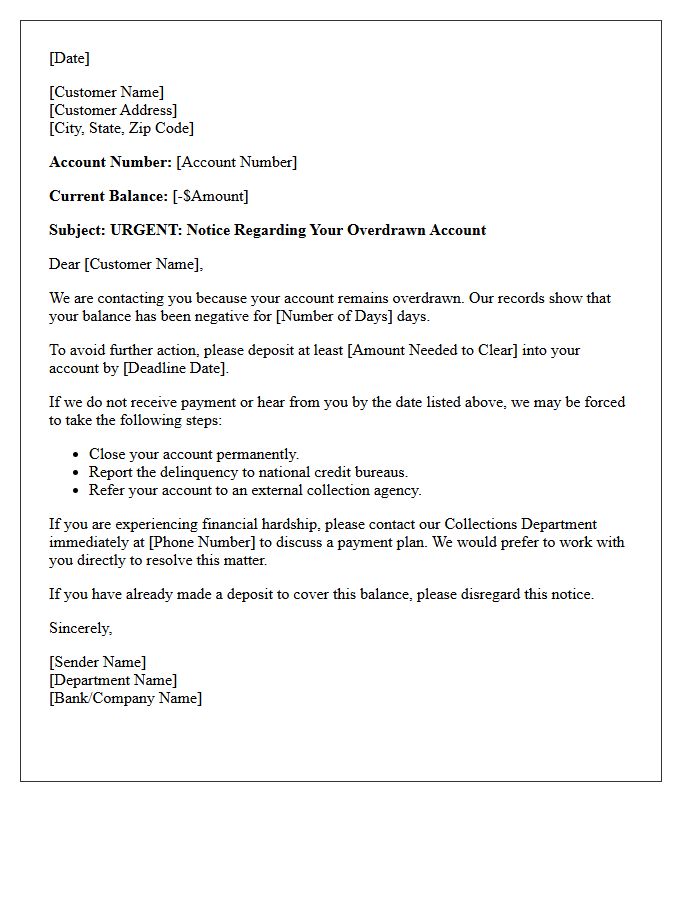

Pre-Collections Overdraft Warning Letter

A Pre-Collections Overdraft Warning Letter is a formal notice from your bank indicating that your account has a negative balance. This final notice serves as a grace period, urging you to deposit funds immediately to avoid further penalties. If ignored, the debt will be transferred to a third-party collection agency, which can severely damage your credit score and limit your ability to open future bank accounts. Promptly settling the balance or contacting the bank for a repayment plan is essential to protect your financial standing and prevent legal action.

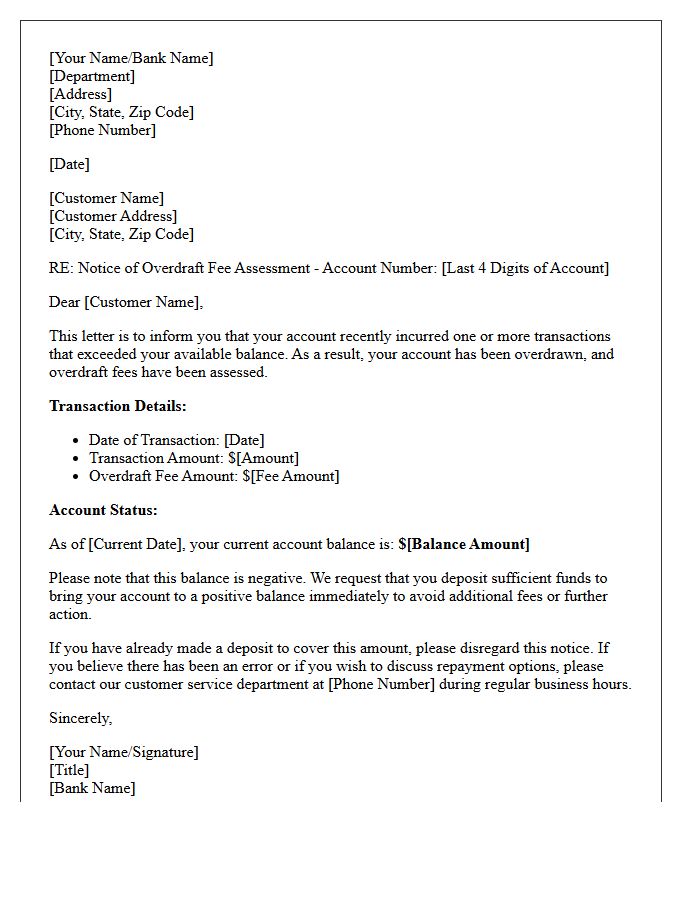

Overdraft Fee Assessment and Balance Letter

An Overdraft Fee Assessment and Balance Letter is a formal notice sent by a financial institution when an account balance falls below zero. This document details the specific transaction that triggered the deficit and the resulting penalty charges applied to the account. It serves as a legal record of the outstanding balance and any required corrective actions. Monitoring these letters is essential to avoid compounding fees, manage financial liability, and ensure your account status remains in good standing through prompt repayment of the overdrawn amount.

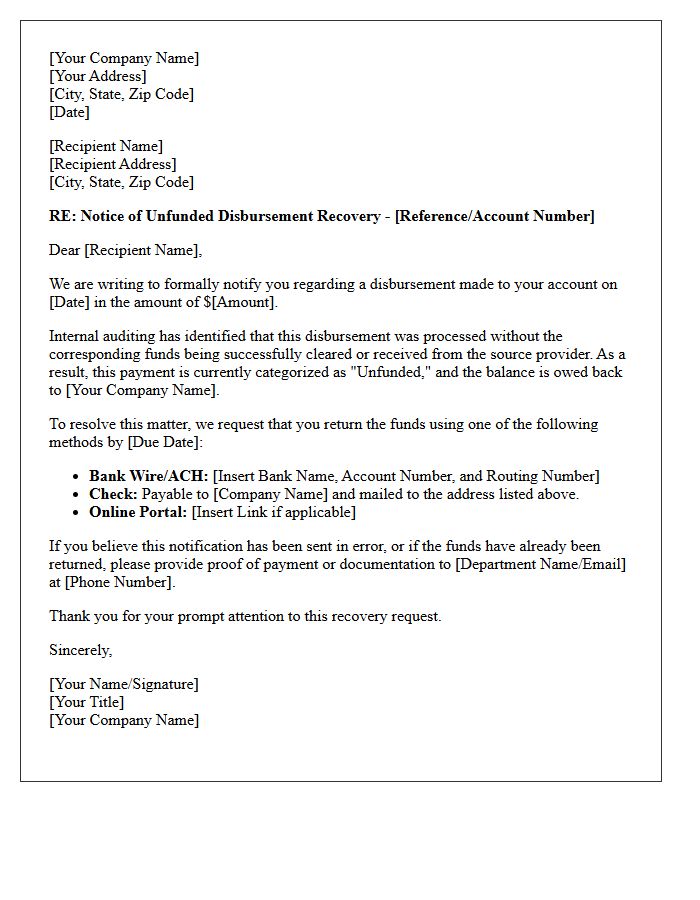

Unfunded Disbursement Recovery Letter

An Unfunded Disbursement Recovery Letter is a formal notice sent by a financial institution or lender to reclaim funds released in error. This typically occurs when a disbursement is made before the necessary loan conditions are met or if the underlying account lacks sufficient backing. Receiving this letter indicates a legal obligation to return the specific amount immediately to rectify the accounting discrepancy. Failure to comply can lead to legal action or negative impacts on your credit standing. It is essential to verify the claim and coordinate a repayment plan promptly.

Commercial Account Overdraft Demand Letter

A Commercial Account Overdraft Demand Letter is a formal legal notification sent by a financial institution to a business entity. It serves as an official request for the immediate repayment of a negative balance plus associated fees. Unlike consumer accounts, commercial overdrafts often lack the same statutory protections, making swift resolution critical to avoid litigation or account closure. Receiving this letter indicates that the bank may pursue legal action or report the delinquency to credit agencies if the debt remains outstanding within the specified deadline.

Retail Banking Overdraft Resolution Letter

A Retail Banking Overdraft Resolution Letter is a formal document sent by a financial institution to notify a customer of a negative account balance. This notice outlines the specific outstanding debt, including any accrued service fees, and sets a strict deadline for repayment. It serves as a final opportunity to rectify the deficit before the bank initiates collection actions or closes the account. Promptly addressing this letter is essential to protect your credit score and maintain your standing with the bank while preventing further financial penalties or legal escalations.

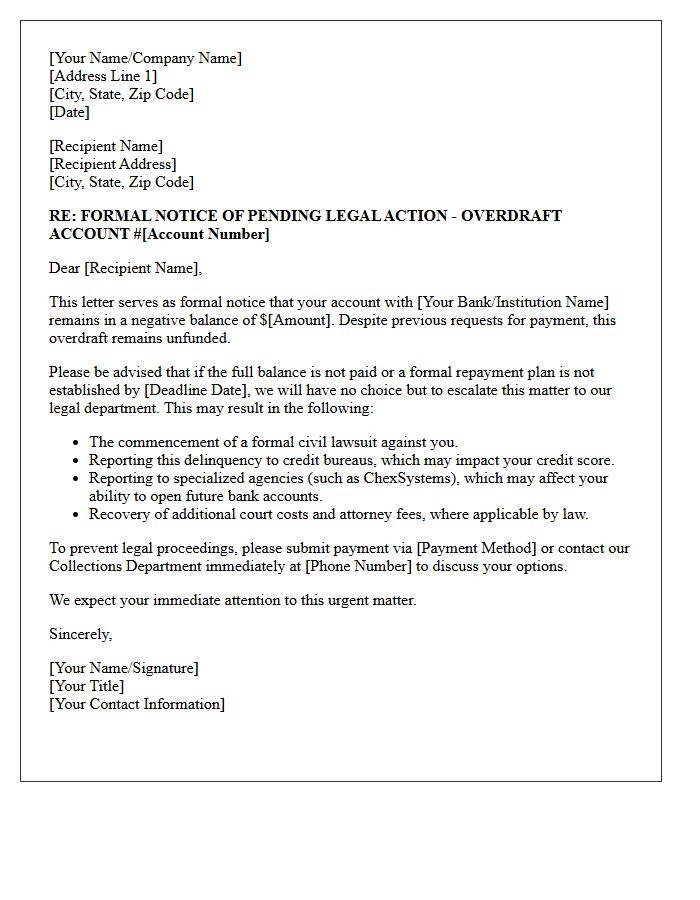

Legal Action Pending for Unfunded Overdraft Letter

Receiving a Legal Action Pending for Unfunded Overdraft Letter indicates that your financial institution is preparing to sue for an unresolved negative balance. This formal notice serves as a final warning to settle delinquent debts before litigation begins. Ignoring this correspondence can lead to court summons, wage garnishment, or asset seizure. To prevent severe damage to your credit score and ChexSystems record, you must contact the bank immediately to negotiate a repayment plan or verify the debt's validity. Timely communication is critical to avoiding a permanent legal judgment on your public record.

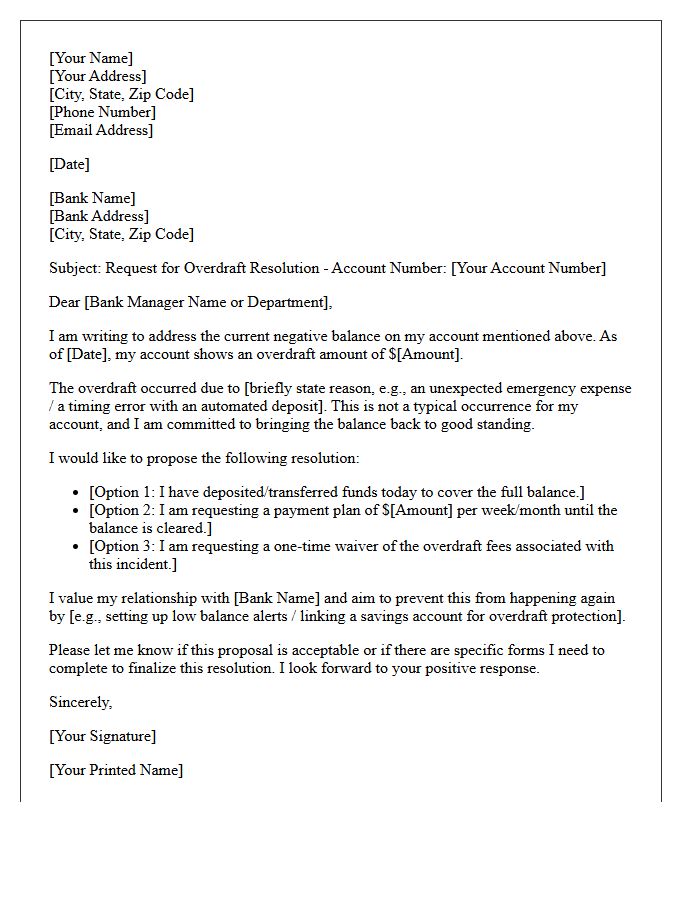

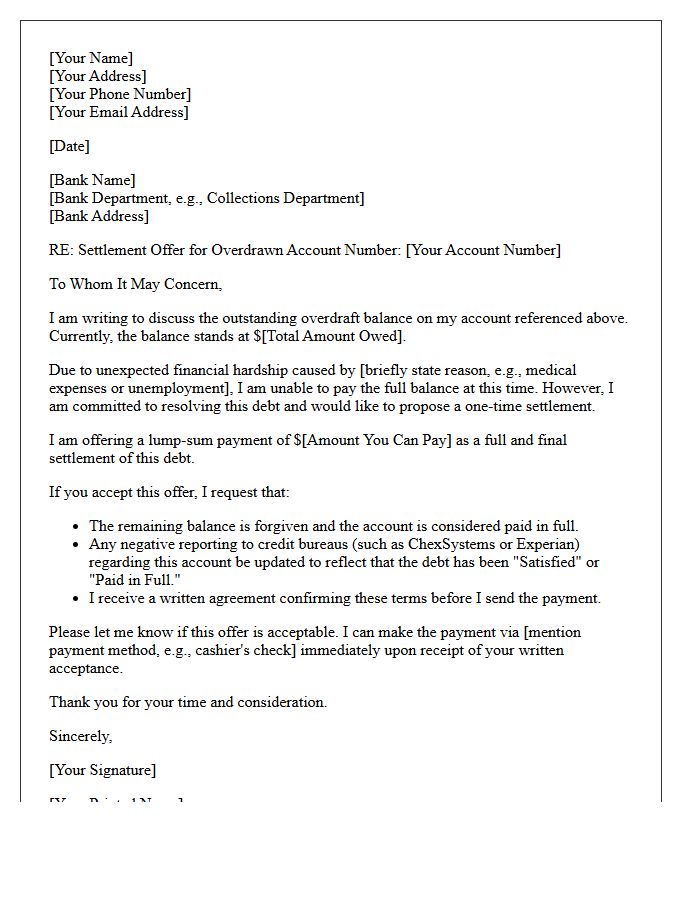

Overdraft Settlement Negotiation Letter

An Overdraft Settlement Negotiation Letter is a formal request sent to a bank to resolve unpaid debt for less than the total balance. To be effective, the letter should clearly explain financial hardships and offer a specific lump-sum payment or structured settlement. It is crucial to request that the bank reports the debt as "paid in full" to credit bureaus to protect your credit score. Always keep a copy for your records and ensure any final agreement is confirmed in writing before sending payment to avoid further legal action or fees.

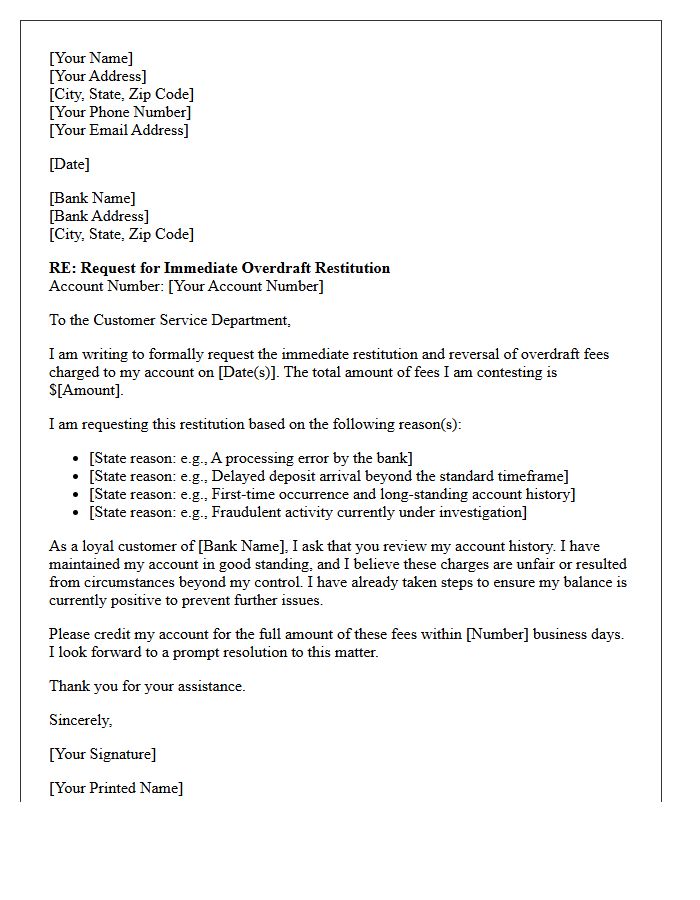

Immediate Overdraft Restitution Request Letter

An Immediate Overdraft Restitution Request Letter is a formal notice sent to a bank or financial institution. It serves as a written demand to rectify unauthorized charges or errors that caused an account deficit. To ensure effectiveness, the letter must include specific account details, transaction dates, and a clear timeline for the reversal of fees. Providing documented evidence of the discrepancy is essential to protect consumer rights and restore a positive balance promptly, preventing further penalties or negative impacts on your credit history.

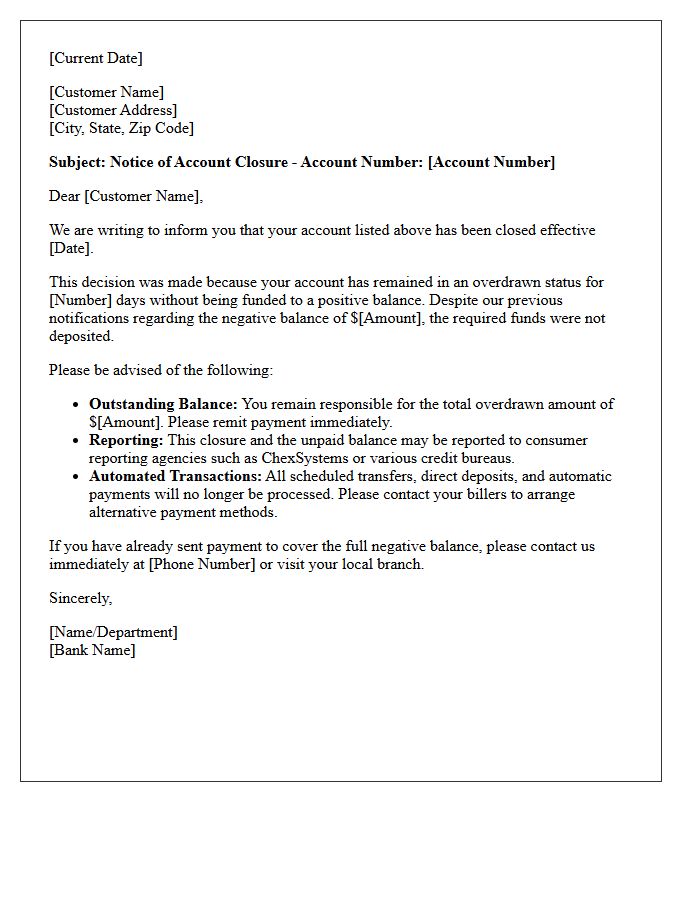

Account Closure Due to Unfunded Overdraft Letter

An Account Closure Due to Unfunded Overdraft Letter serves as a formal notification that a bank is terminating a contractual relationship because a negative balance remained unpaid for too long. Receiving this notice indicates that the institution has charged off the debt, which significantly damages your banking history. This action is typically reported to ChexSystems, potentially preventing you from opening new accounts elsewhere for several years. To mitigate long-term financial consequences, it is vital to repay the outstanding balance immediately and request a formal letter confirming the debt has been settled.

What does an "Urgent Notice of Unfunded Overdraft Balance" mean?

This notice indicates that your bank account has a negative balance that has not been covered by a deposit or a pre-arranged overdraft limit. It serves as a formal request to deposit funds immediately to bring your account balance back to zero or above.

How long do I have to resolve an unfunded overdraft balance?

Typically, banks require you to fund the deficit within 24 to 48 hours of receiving the notice. Failure to rectify the balance promptly may result in additional daily overdraft fees, account suspension, or reporting to credit bureaus.

What are the consequences of ignoring an urgent overdraft notice?

Ignoring this notice can lead to returned item fees (NSF), the closure of your bank account, and a negative report to ChexSystems or early-warning services. This can make it difficult to open new bank accounts or obtain credit in the future.

Can I dispute an overdraft fee associated with this notice?

Yes, if you believe the overdraft was caused by a bank error or an unauthorized transaction, you should contact your bank's customer service department immediately. In some cases, banks may offer a one-time fee waiver as a courtesy for long-standing customers.

How can I prevent receiving unfunded overdraft notices in the future?

To avoid future notices, you can set up low-balance mobile alerts, link a savings account for automatic overdraft protection transfers, or opt-out of overdraft coverage for point-of-sale transactions to ensure cards are declined instead of overdrawn.

Comments