A First Notice of Overdue Account Default serves as a formal communication to inform a debtor that their payment is past due. It is the initial step in debt recovery, clearly stating the balance owed and the required deadline to avoid further collection actions. Professionalism is key to maintaining business relationships. Below are some ready to use templates.

Image cover: Professional Templates for Your First Overdue Payment Notice

Letter Samples List

- First Notice of Overdue Account Default Letter

- Initial Overdue Banking Account Notice Letter

- First Warning of Account Default Letter

- Bank Account Overdue Balance First Notice Letter

- Notice of Initial Account Default Letter

- First Notification of Overdue Loan Account Letter

- Banking Institution Overdue Payment First Notice Letter

- Initial Default Warning for Overdue Account Letter

- First Notice of Past Due Account Balance Letter

- Preliminary Overdue Account Default Notification Letter

- First Demand for Overdue Account Payment Letter

- Bank Account Delinquency First Notice Letter

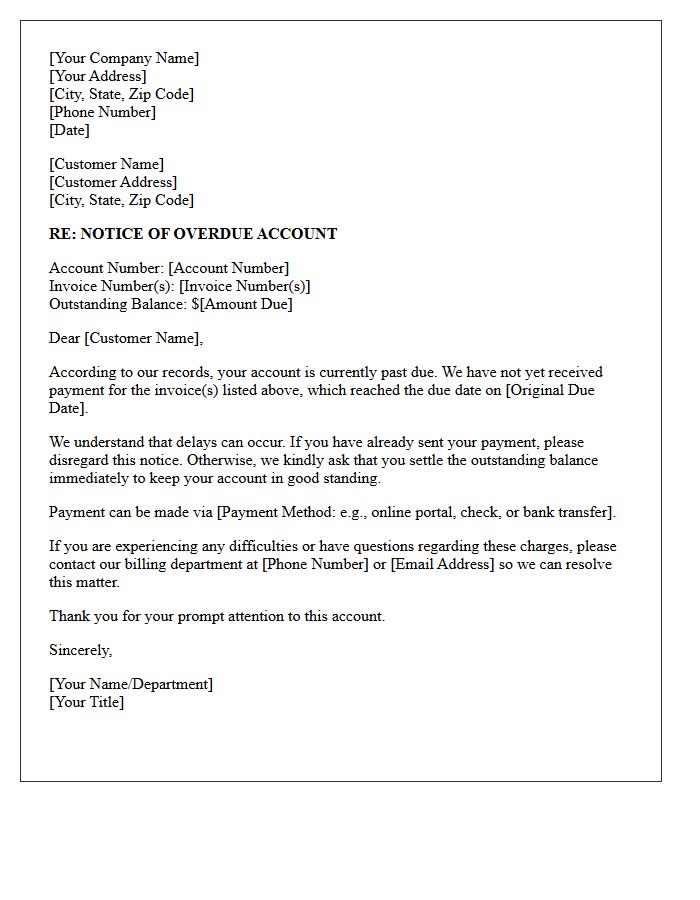

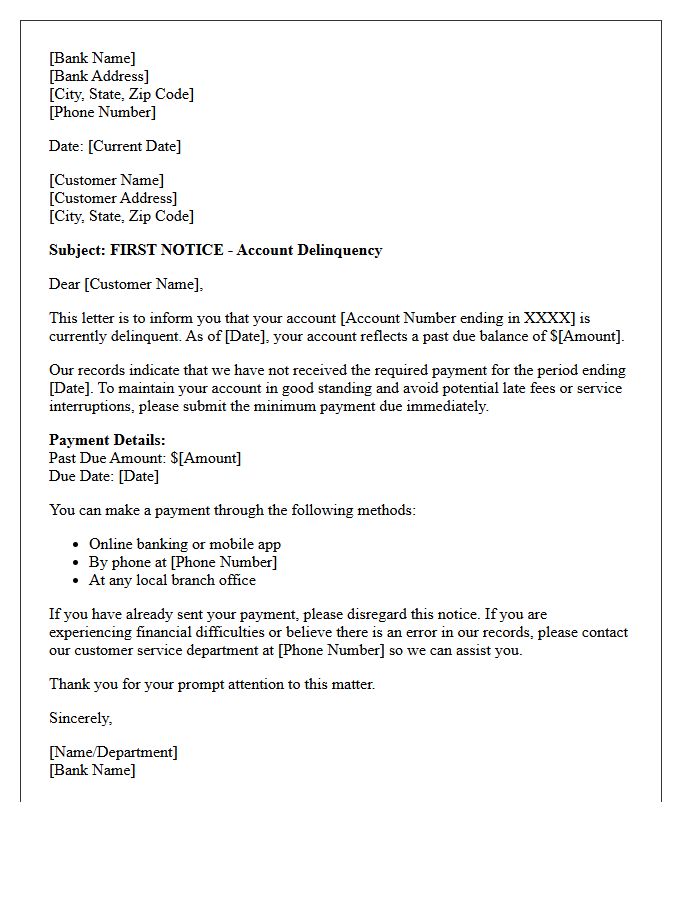

First Notice of Overdue Account Default Letter

A First Notice of Overdue Account is a formal legal notification sent when a payment exceeds its due date. This letter serves as an essential warning to the debtor, providing a final opportunity to settle the balance before further debt collection actions or legal proceedings commence. It typically outlines the total amount owed, applicable late fees, and a specific deadline for payment. Receiving this notice is a critical signal to prioritize communication with the creditor to prevent negative impacts on your credit score and overall financial standing.

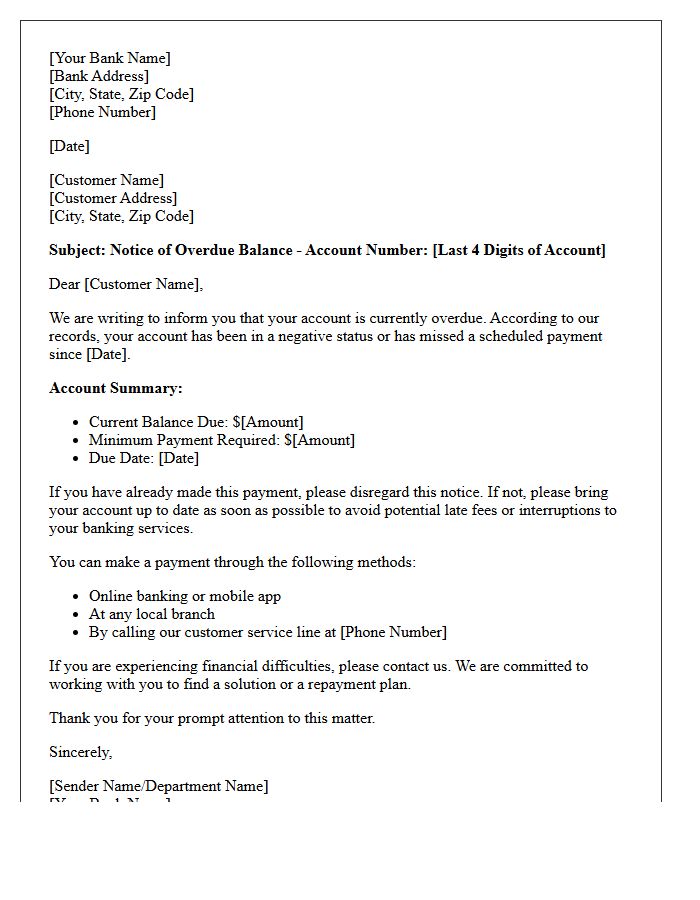

Initial Overdue Banking Account Notice Letter

Receiving an Initial Overdue Banking Account Notice Letter is a formal warning that your account has a negative balance or missed payment. It is crucial to act immediately to avoid costly overdraft fees, penalty interest, or negative impacts on your credit score. This document typically outlines the total amount owed and a specific deadline for repayment. Contacting your bank promptly can often resolve the issue through a repayment plan, preventing the debt from being transferred to a formal collection agency or resulting in account closure.

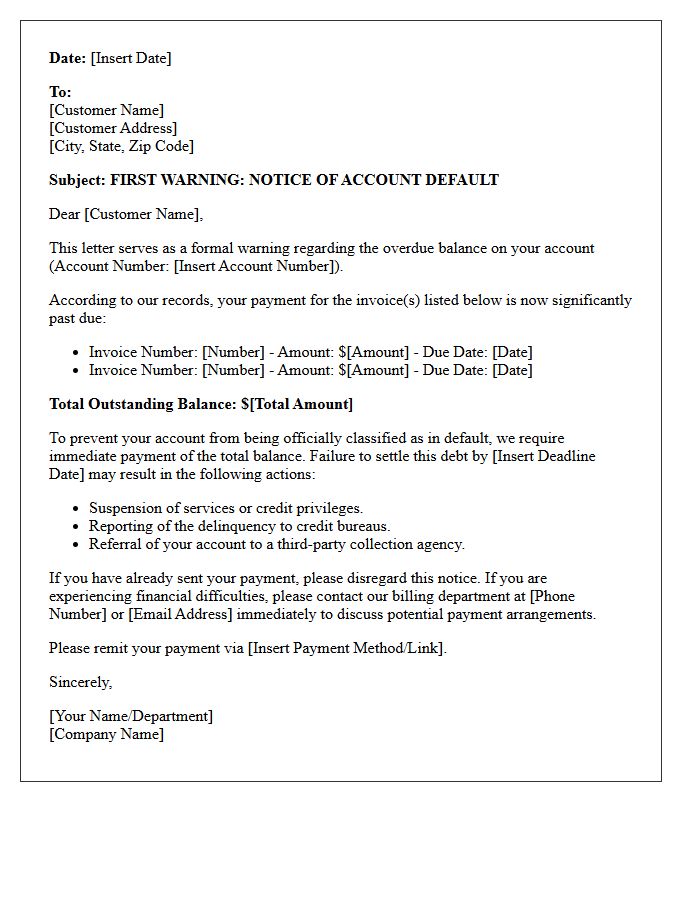

First Warning of Account Default Letter

A First Warning of Account Default Letter serves as a formal notification that your payments are overdue. This critical document warns that failure to settle the outstanding balance within a specific timeframe will result in a formal default registered on your credit file. Receiving this notice is a final opportunity to negotiate a repayment plan or seek financial advice before your credit score is severely impacted for six years. Acting immediately can prevent further legal action and preserve your future borrowing capacity.

Bank Account Overdue Balance First Notice Letter

A Bank Account Overdue Balance First Notice Letter is a formal notification informing you that your account has a negative balance. This initial warning serves as a reminder to deposit funds immediately to avoid additional overdraft fees or account suspension. It typically outlines the exact amount owed and provides a deadline for repayment. Ignoring this notice can negatively impact your credit score and lead to the permanent closure of your banking facilities. Prompt communication with your bank is essential to resolve discrepancies and maintain a positive financial standing.

Notice of Initial Account Default Letter

A Notice of Initial Account Default Letter is a formal warning indicating you have missed scheduled payments on a credit agreement. This legal document is a critical step before a formal default is recorded on your credit file. It outlines the total arrears owed and provides a specific timeframe to remedy the breach. Ignoring this notice can lead to account termination, legal action, and long-term damage to your credit score. To protect your financial standing, you must contact your creditor immediately to arrange a repayment plan or clear the outstanding balance.

First Notification of Overdue Loan Account Letter

A First Notification of Overdue Loan Account Letter is a formal notice sent by lenders when a scheduled payment is missed. This early intervention serves as a reminder to settle the outstanding balance and avoid potential penalties. It outlines the specific amount due, the original due date, and available repayment options. Receiving this letter is a critical opportunity to communicate with your creditor to prevent credit score damage or further legal action. Promptly addressing this notice helps maintain financial stability and restores your account to good standing before escalation occurs.

Banking Institution Overdue Payment First Notice Letter

A Banking Institution Overdue Payment First Notice Letter serves as a formal reminder regarding a missed deadline. This initial communication aims to prompt immediate action to settle the outstanding balance before additional penalties apply. It typically includes the payment amount, due date, and available methods for resolution. Maintaining open communication with your bank after receiving this notice is essential to protect your credit score and avoid late fees or escalated collection efforts. Timely responses help preserve your financial standing and prevent long-term negative impacts on your credit history.

Initial Default Warning for Overdue Account Letter

An Initial Default Warning is a formal notice sent to a debtor when an account becomes overdue. Its primary purpose is to inform the recipient of the outstanding balance and provide a final opportunity to settle the debt before formal escalation. This letter serves as a crucial legal step, documenting the creditor's attempt to resolve the issue amicably. It must clearly state the payment deadline and potential consequences, such as credit score impacts or legal action, ensuring the process remains compliant with fair debt collection practices.

First Notice of Past Due Account Balance Letter

Receiving a First Notice of Past Due Account Balance Letter serves as an initial formal reminder that a specific payment deadline has been missed. This document outlines the outstanding balance, including any applicable late fees, and provides instructions for immediate settlement. It is a critical stage in credit management, designed to resolve delinquencies before the account faces more severe consequences like service suspension or negative credit reporting. Addressing this notice promptly allows for the negotiation of payment arrangements and helps maintain a positive relationship between the creditor and the debtor.

Preliminary Overdue Account Default Notification Letter

A Preliminary Overdue Account Default Notification Letter serves as a final formal warning before a creditor registers a default against your credit file. This document informs the debtor that their payment is seriously overdue and outlines the specific timeframe remaining to settle the balance. Receiving this notice is critical because an official default significantly damages your credit score for several years, hindering future borrowing. It is essential to contact the lender immediately to arrange a repayment plan or seek financial advice to prevent further legal action or collection escalations.

First Demand for Overdue Account Payment Letter

A First Demand for Overdue Account Payment Letter serves as a formal professional reminder to a debtor. Its primary purpose is to request immediate settlement of an outstanding invoice while maintaining a positive business relationship. The document must clearly state the exact balance due, the original due date, and acceptable payment methods. By acting as an official notice of delinquency, it creates a crucial paper trail for potential legal action or debt collection. Sending this notice promptly encourages account reconciliation and helps resolve billing oversights before escalated enforcement becomes necessary.

Bank Account Delinquency First Notice Letter

A Bank Account Delinquency First Notice Letter serves as a formal alert that your account has a negative balance or overdue payment. This initial correspondence is crucial for preventing further financial penalties, such as overdraft fees or credit score damage. It typically requests immediate repayment to restore the account to good standing. Addressing this notice promptly allows you to resolve errors or settle debts before the bank initiates collection actions or account closure. Proactive communication with your financial institution is essential to maintain long-term financial stability and banking access.

What is a First Notice of Overdue Account Default?

A First Notice of Overdue Account Default is a formal written communication sent by a creditor to a borrower when a payment is missed. It serves as an official alert that the account is in arrears and warns of potential legal or credit consequences if the balance is not rectified immediately.

How does receiving a default notice affect my credit score?

While the initial notice itself is a warning, failure to resolve the overdue amount can lead to a formal default being recorded on your credit report. A registered default can remain on your credit file for up to six years, significantly lowering your credit score and making it difficult to obtain future financing.

What steps should I take after receiving a first overdue account notice?

Upon receiving the notice, you should immediately verify the debt amount, check your payment records, and contact the creditor to settle the balance. If you are unable to pay in full, you should propose a repayment plan or discuss hardship options to prevent the account from escalating to a collection agency.

Can a creditor take legal action after the first notice of default?

The first notice is typically the start of a structured collections process; however, continued non-payment grants the creditor the right to pursue further action. This may include transferring the debt to a collection agency, filing a lawsuit to obtain a judgment, or initiating wage garnishment depending on local regulations.

Is it possible to dispute a First Notice of Overdue Account Default?

Yes, if you believe the notice was sent in error or the balance is incorrect, you have the right to dispute it. You should submit a formal written dispute to the creditor providing evidence of payment or documentation of the error, which stays further collection efforts while the account is under investigation.

Comments