Receiving a notice regarding potential adverse credit bureau reporting is a serious matter that can damage your financial reputation and credit score. Understanding how to address delinquent accounts promptly is essential to preventing long-term fiscal consequences. This guide explores your rights, effective resolution strategies, and communication methods to protect your creditworthiness. To help you respond effectively, below are some ready to use template.

Image cover: Final Notice: Pending Credit Bureau Reporting and Delinquent Account Templates

Letter Samples List

- Initial Delinquent Account Credit Bureau Reporting Warning Letter

- Second Notice of Adverse Credit Reporting Letter

- Final Warning Letter for Adverse Credit Bureau Reporting

- Pre-Charge-Off Credit Bureau Reporting Warning Letter

- Delinquent Mortgage Account Credit Bureau Reporting Warning Letter

- Auto Loan Default Adverse Credit Reporting Warning Letter

- Credit Card Arrears Credit Bureau Reporting Warning Letter

- Notice of Intent to Report Adverse Credit History Letter

- Payment Demand and Credit Bureau Reporting Warning Letter

- Notice to Cure Default to Prevent Adverse Credit Reporting Letter

- Commercial Delinquency Adverse Credit Bureau Reporting Letter

- Grace Period Expiration and Credit Bureau Warning Letter

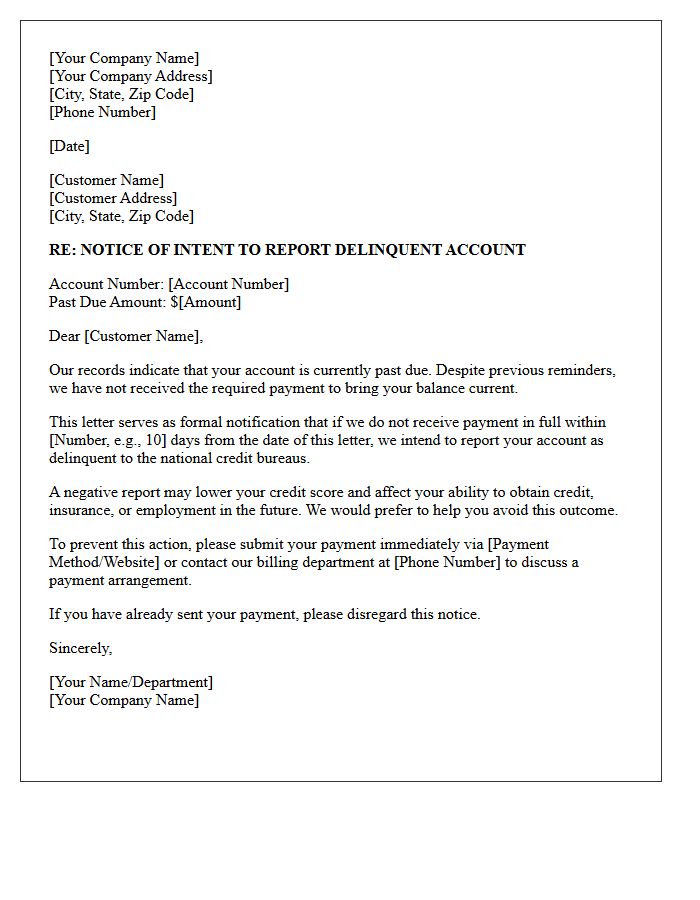

Initial Delinquent Account Credit Bureau Reporting Warning Letter

An Initial Delinquent Account Credit Bureau Reporting Warning Letter serves as a formal notice that your overdue debt is approaching a critical deadline. This mandatory communication informs you that failure to resolve the balance will result in a negative report to major credit bureaus. Receiving this letter provides a final opportunity to settle the payment or dispute inaccuracies before your credit score is impacted. Timely action is essential to prevent long-term financial consequences, such as increased interest rates or difficulty securing future loans due to a derogatory mark on your record.

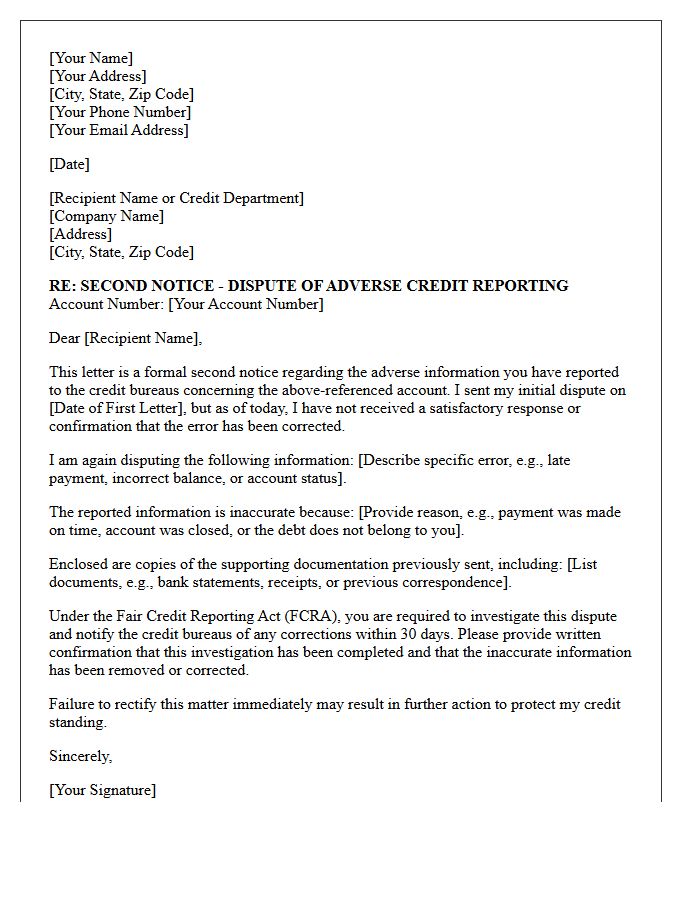

Second Notice of Adverse Credit Reporting Letter

A Second Notice of Adverse Credit Reporting Letter is a final warning sent by creditors before reporting delinquent debt to credit bureaus. This document provides a final opportunity to resolve outstanding balances to avoid severe credit score damage. It must include the specific amount owed and details regarding your legal rights. Promptly addressing this notice is essential, as negative entries can remain on your credit report for seven years, hindering your ability to secure future loans, housing, or favorable interest rates.

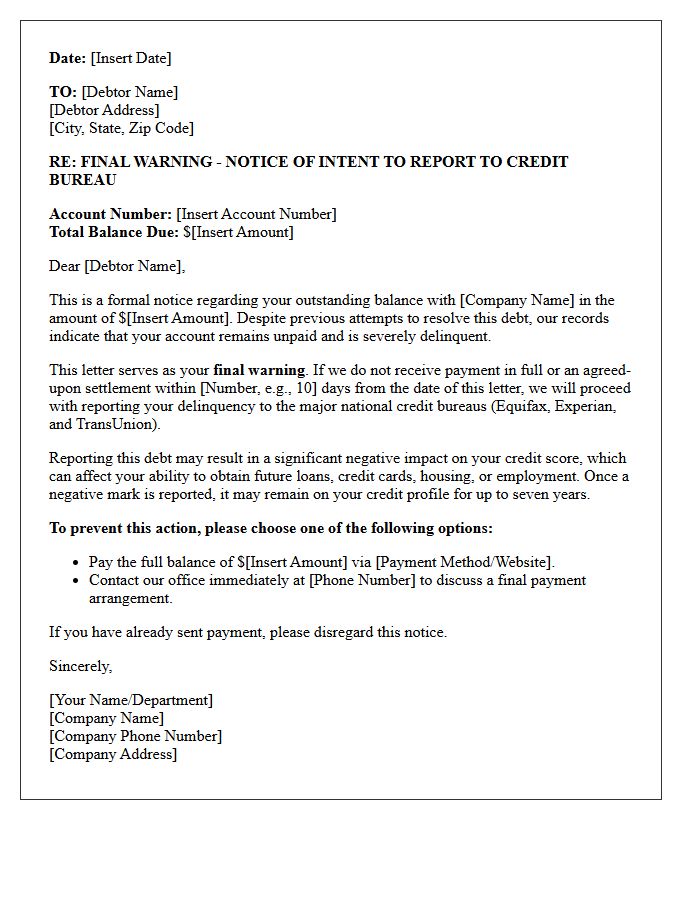

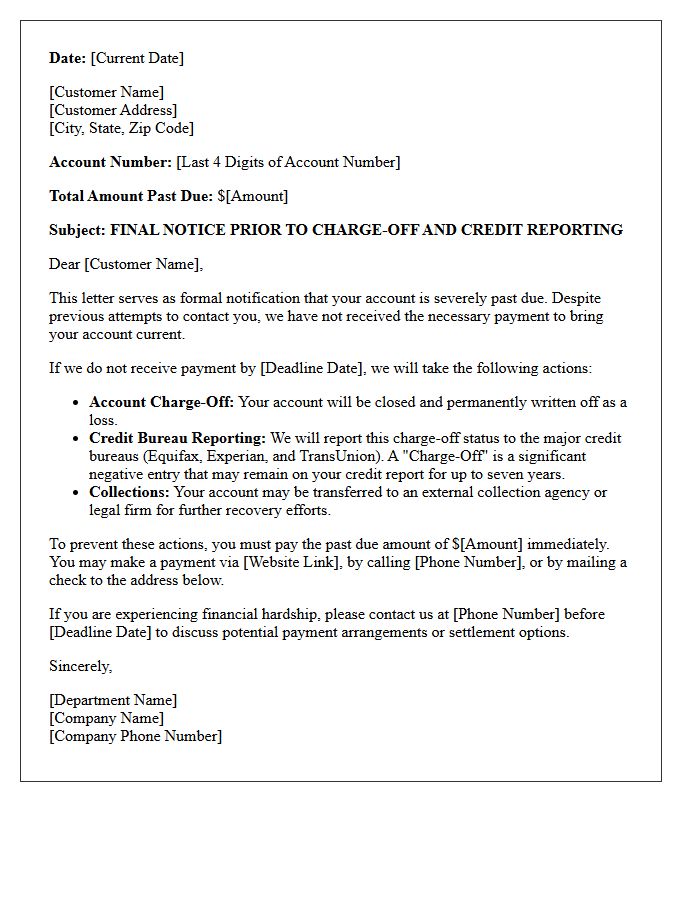

Final Warning Letter for Adverse Credit Bureau Reporting

A final warning letter serves as a formal notice before a creditor submits negative information to a credit agency. This document is a critical opportunity to resolve outstanding debts and prevent long-term damage to your credit score. Ignoring this notice typically leads to adverse reporting, which can restrict your ability to secure loans or favorable interest rates for years. To protect your financial standing, you should immediately verify the debt's accuracy and arrange a settlement or payment plan within the specified timeframe to stop the reporting process.

Pre-Charge-Off Credit Bureau Reporting Warning Letter

A Pre-Charge-Off Credit Bureau Reporting Warning Letter is a formal notice sent by lenders before declaring a debt uncollectible. It serves as a final opportunity to settle delinquent accounts before they are classified as a charge-off. Receiving this letter indicates that a severe negative entry is imminent on your credit report, which can drastically lower your credit score for seven years. To protect your financial standing, you must prioritize immediate payment or contact the creditor to negotiate a workout plan before the reporting deadline expires.

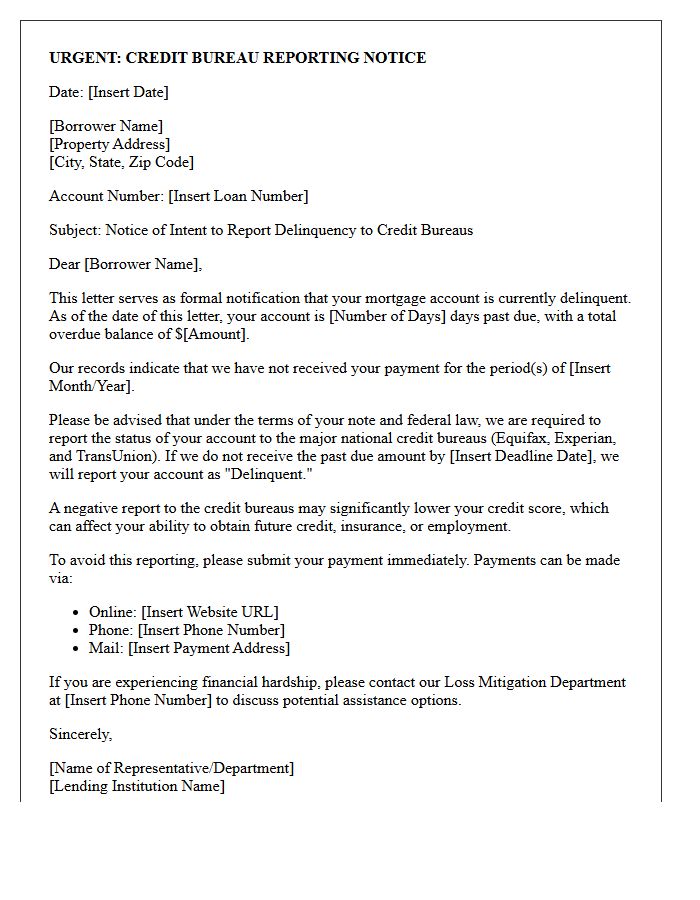

Delinquent Mortgage Account Credit Bureau Reporting Warning Letter

A Delinquent Mortgage Account Credit Bureau Reporting Warning Letter serves as a formal notice that your home loan payment is past due. Lenders send this document to alert you that failure to resolve the arrears within a specific timeframe will result in negative reporting to major credit agencies. This action can significantly lower your credit score, making future financing difficult. It is crucial to contact your servicer immediately upon receipt to discuss loss mitigation options or repayment plans to protect your financial standing and prevent potential foreclosure proceedings.

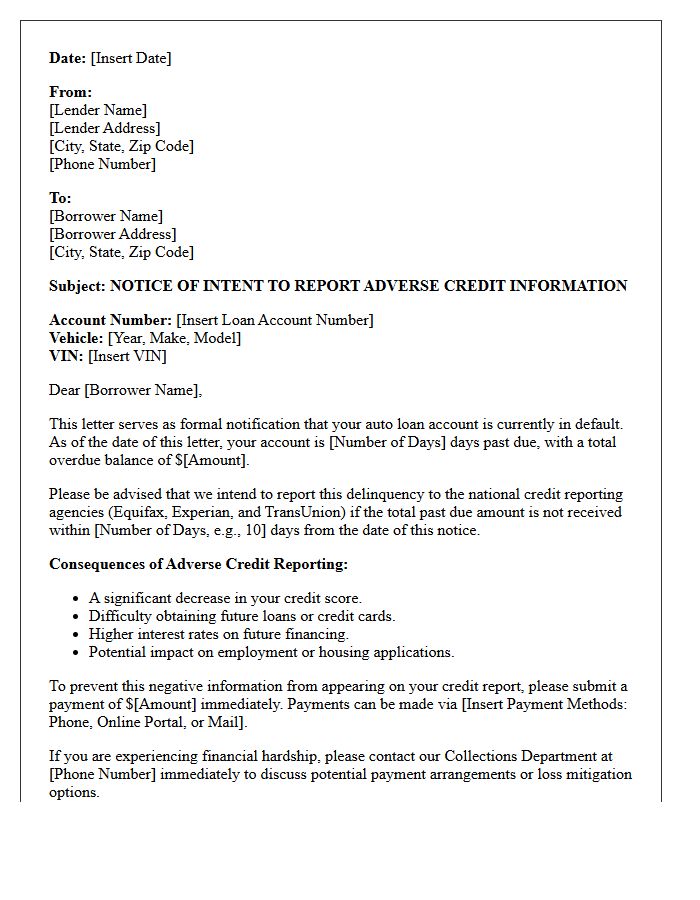

Auto Loan Default Adverse Credit Reporting Warning Letter

An Auto Loan Default Adverse Credit Reporting Warning Letter serves as a formal notice that your vehicle financing is in default. This critical document warns that failure to resolve arrears will result in negative credit reporting, severely damaging your credit score for up to seven years. It acts as a final opportunity to cure the default through payment or negotiation before the lender initiates repossession. Prompt communication with your lender after receiving this warning is essential to prevent long-term financial consequences and the loss of your transportation.

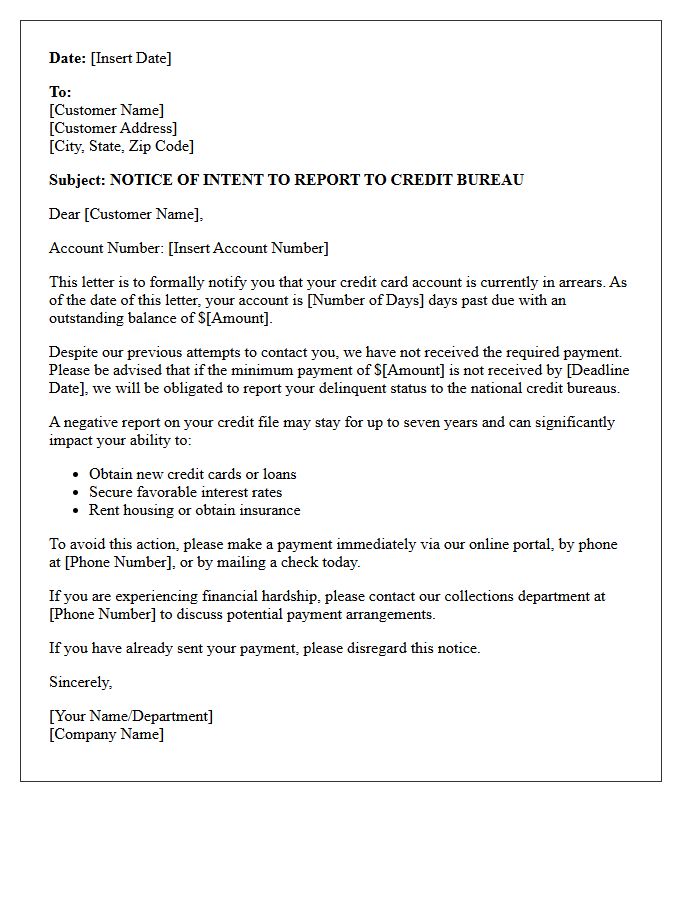

Credit Card Arrears Credit Bureau Reporting Warning Letter

A Credit Card Arrears Warning Letter is a formal notice sent by lenders before reporting missed payments to a credit bureau. This document serves as a final opportunity to settle outstanding debts and avoid severe damage to your credit score. Ignoring this warning can lead to a default record, making it difficult to secure future loans or competitive interest rates. To protect your financial profile, prioritize immediate repayment or contact your creditor to negotiate a formal payment arrangement before the specified reporting deadline expires.

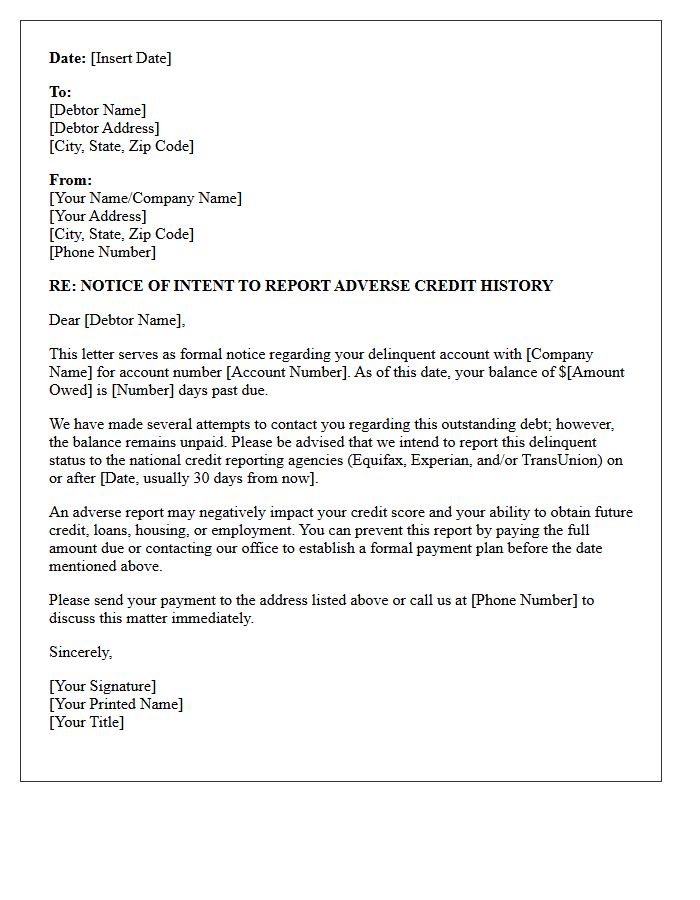

Notice of Intent to Report Adverse Credit History Letter

A Notice of Intent to Report Adverse Credit History is a formal warning from a creditor before they submit negative data to credit bureaus. This document is legally required in many jurisdictions to give consumers a final opportunity to resolve an outstanding debt. Receiving this highlighted notification means you typically have 30 days to pay the balance or dispute the claim to avoid a significant drop in your credit score. Promptly addressing this notice is the most effective way to protect your financial reputation and prevent long-term reporting penalties.

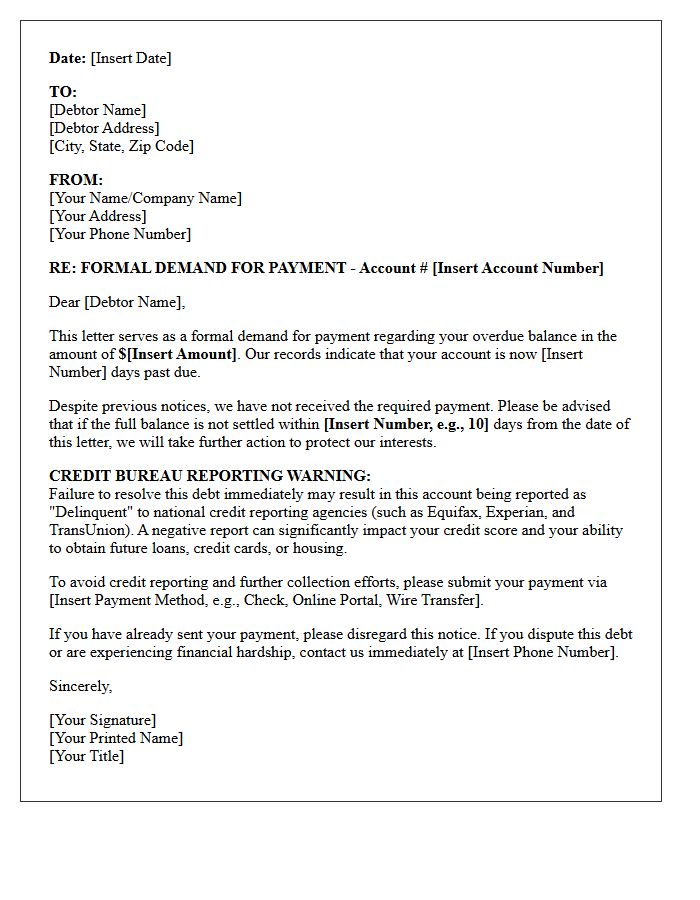

Payment Demand and Credit Bureau Reporting Warning Letter

A Payment Demand and Credit Bureau Reporting Warning Letter serves as a final formal notice before a creditor reports delinquency to credit agencies. This legal communication notifies the debtor of an outstanding balance and provides a deadline to prevent negative impacts on their credit score. Receiving this letter indicates that the account is at risk of being sent to collections. To protect your financial standing, it is essential to respond immediately by making a payment, arranging a settlement, or disputing the debt in writing to avoid long-term credit damage.

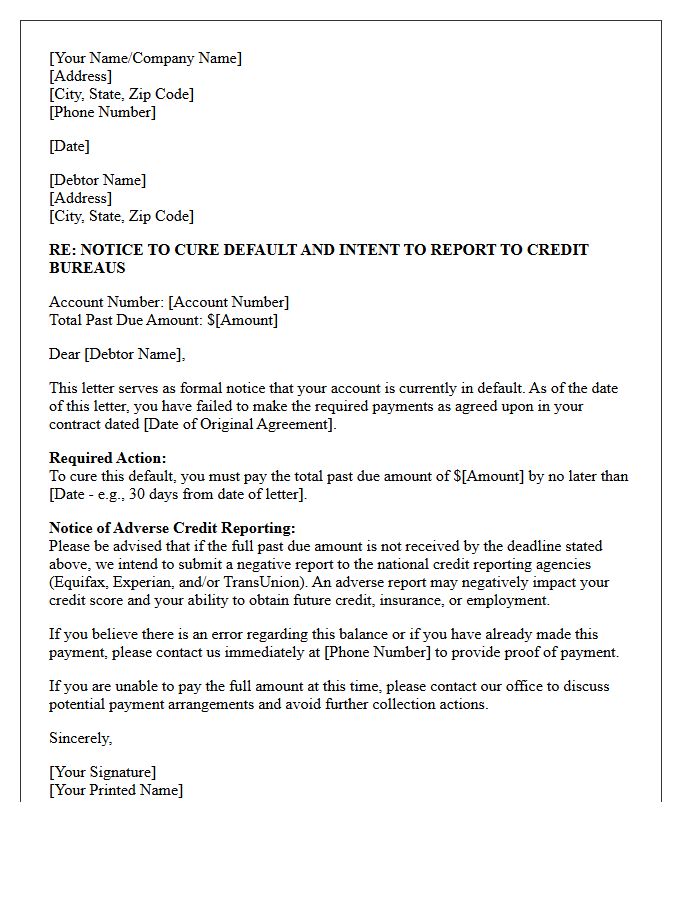

Notice to Cure Default to Prevent Adverse Credit Reporting Letter

A Notice to Cure Default is a critical legal warning sent by creditors before reporting negative payment history to bureaus. Receiving this letter provides a final opportunity to pay the past-due balance and avoid severe damage to your credit score. Under the Fair Credit Reporting Act, lenders must often notify consumers before submitting adverse information. To protect your financial reputation, you must resolve the delinquency within the specified cure period mentioned in the document. Ignoring this notice typically results in a formal default record that lasts seven years on your report.

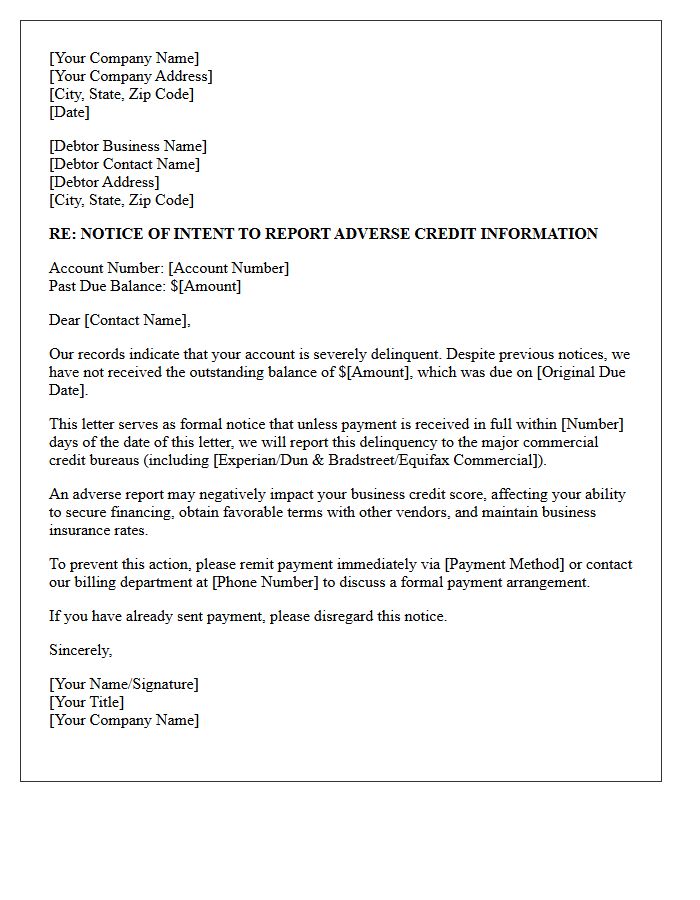

Commercial Delinquency Adverse Credit Bureau Reporting Letter

A Commercial Delinquency Adverse Credit Bureau Reporting Letter serves as a final formal notice before negative payment data is shared with business credit agencies like Dun & Bradstreet or Experian. This document warns the debtor that their non-payment will soon impact their business credit score, potentially hindering future financing and vendor terms. Receiving this letter is a critical opportunity to settle outstanding debts or negotiate a payment plan to prevent long-term reputational damage. Timely action is essential to maintain financial credibility and operational viability in the commercial marketplace.

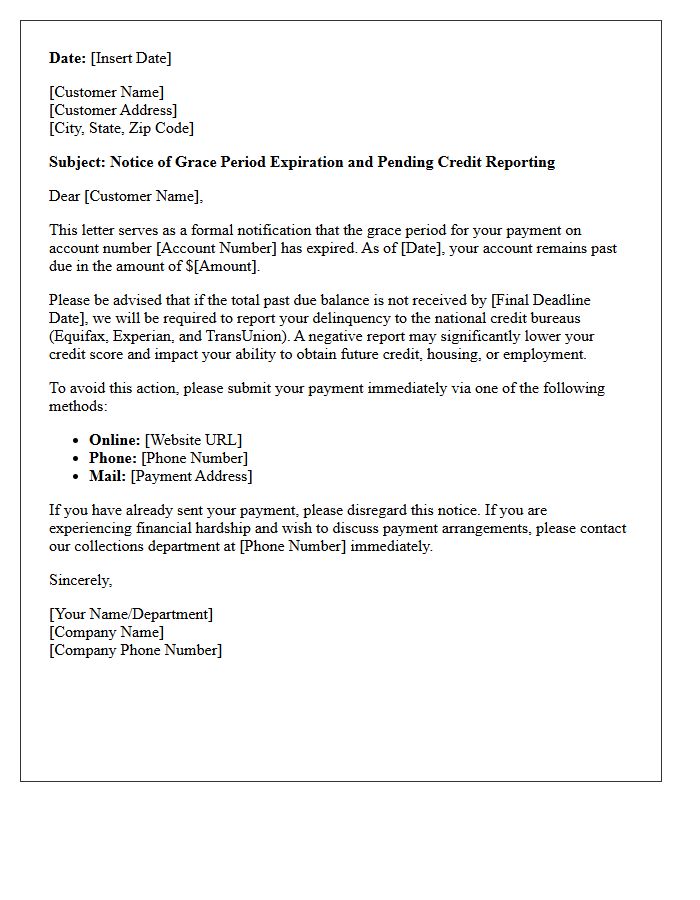

Grace Period Expiration and Credit Bureau Warning Letter

A Grace Period Expiration notice signifies that the additional time allowed to settle a debt without penalties has ended. If payment is not received immediately, creditors will issue a Credit Bureau Warning Letter. This formal notice alerts you that your delinquency is about to be reported to agencies like Equifax or Experian. To protect your credit score and avoid long-term financial damage, you must resolve the balance before the reporting deadline. Timely action prevents a derogatory mark from appearing on your credit history for up to seven years.

What does a warning of adverse credit bureau reporting mean?

A warning of adverse credit bureau reporting is a formal notification from a creditor stating that they intend to report your delinquent account to major credit bureaus (Equifax, Experian, or TransUnion) if the overdue balance is not paid within a specific timeframe.

How long can a delinquent account stay on my credit report?

Once an account is reported as delinquent, it can remain on your credit report for up to seven years from the date of the original missed payment, significantly lowering your credit score and affecting future loan eligibility.

Can I prevent a late payment from being reported to credit bureaus?

Yes, you can typically prevent adverse reporting by paying the past-due amount before the deadline stated in the warning notice, or by contacting the creditor to negotiate a payment plan or a "goodwill" extension before the reporting date.

How many days past due must an account be before it is reported?

By law, creditors cannot report a payment as late to the credit bureaus until it is at least 30 days past the official due date, though internal late fees and collection efforts may begin immediately after the deadline.

What are the consequences of having an adverse credit report entry?

Adverse reporting can lead to a substantial drop in your credit score, higher interest rates on future loans, denial of credit card applications, and potential difficulties in securing housing or employment during background checks.

Comments