A Second Notice of Loan Payment Delinquency serves as a critical follow-up to remind borrowers of their overdue debt. This formal communication outlines the outstanding balance, late fees, and potential legal or credit consequences if the default persists. It is essential for maintaining professional debt recovery standards. To help you draft a clear and compliant message, below are some ready to use template.

Image cover: Second Notice of Past Due Loan Payment: Templates and Professional Samples

Letter Samples List

- Second Notice of Loan Delinquency Letter

- Urgent Second Warning Letter for Overdue Loan Account

- Outstanding Loan Balance Second Reminder Letter

- Second Delinquency Notification Letter for Commercial Loan

- Retail Banking Second Overdue Payment Letter

- Second Notice of Arrears Letter for Mortgage Loan

- Auto Loan Second Delinquency Warning Letter

- Second Past Due Loan Installment Letter

- Unpaid Personal Loan Second Request Letter

- Second Notice Letter Regarding Delinquent Loan Account

- Escalated Loan Payment Delinquency Second Letter

- Second Reminder Letter for Non-Performing Loan

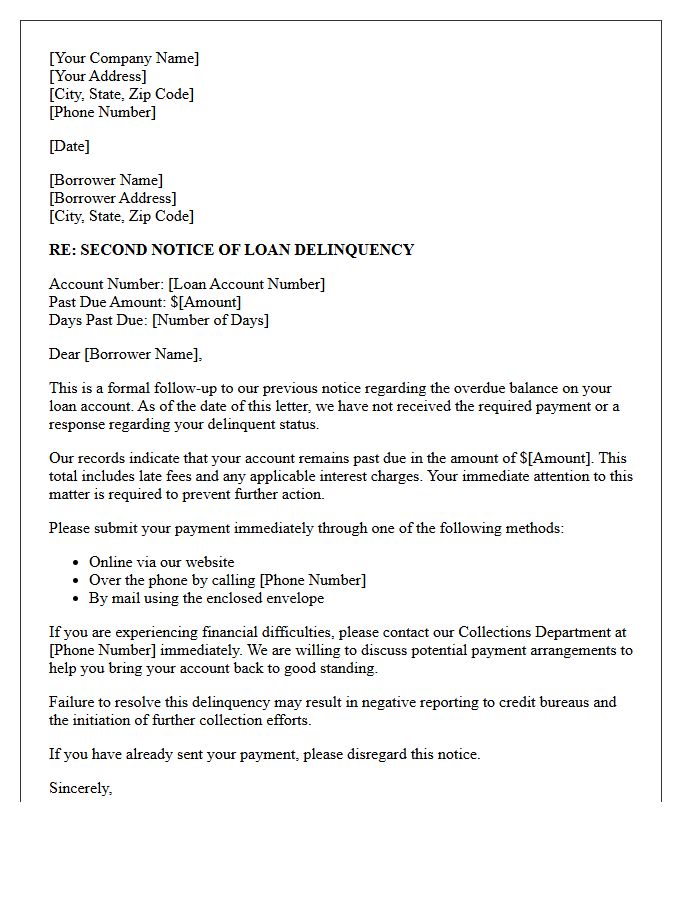

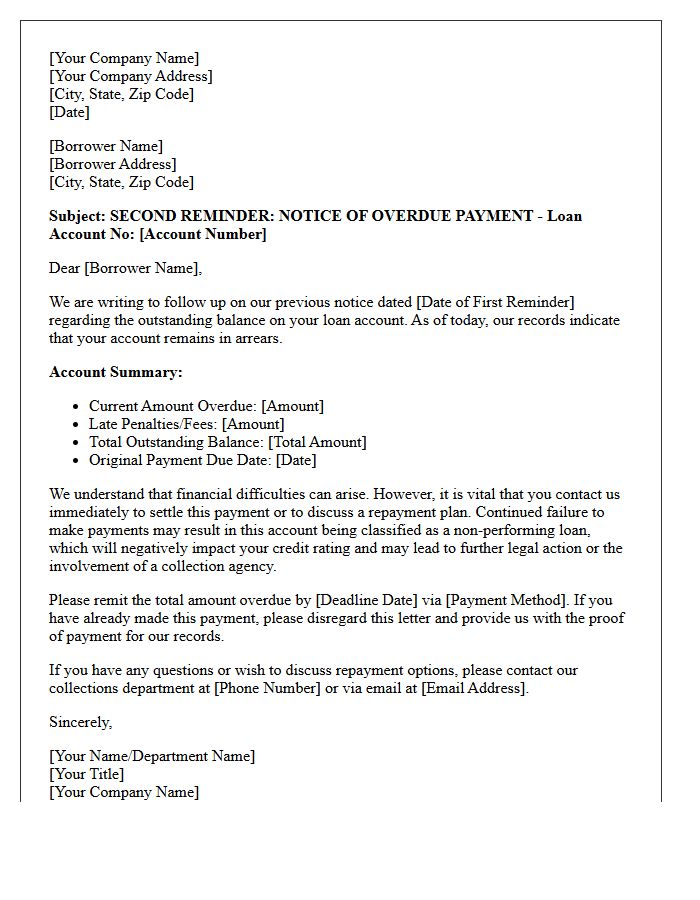

Second Notice of Loan Delinquency Letter

A Second Notice of Loan Delinquency is a critical formal warning issued when a borrower fails to resolve missed payments after the initial reminder. This letter serves as a final opportunity to restate repayment obligations before the lender initiates aggressive collection actions. Receiving this notice indicates that your account is nearing default, which can severely damage your credit score. It is essential to contact your lender immediately to discuss hardship options or loan modification programs to prevent legal proceedings or potential asset foreclosure.

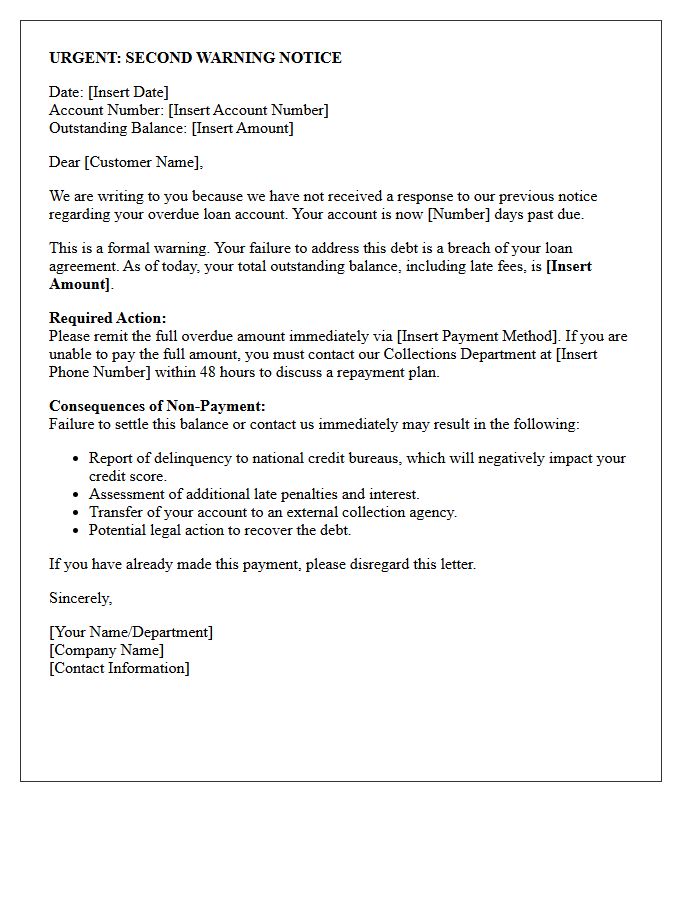

Urgent Second Warning Letter for Overdue Loan Account

Receiving an Urgent Second Warning Letter for an overdue loan account indicates a critical escalation in the collection process. This formal notice signifies that your previous missed payments remain unresolved, placing your credit score at significant risk of severe damage. Failure to settle the balance or arrange a repayment plan immediately may lead to legal action or the involvement of a debt collection agency. It is essential to contact your lender now to discuss hardship options and prevent further penalties, additional interest charges, or potential asset repossession.

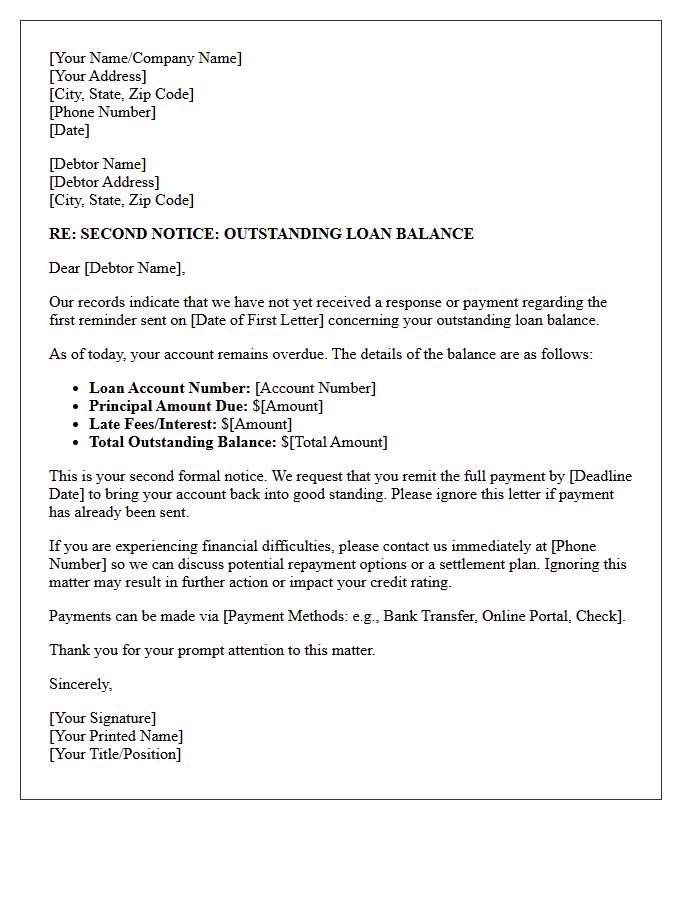

Outstanding Loan Balance Second Reminder Letter

An Outstanding Loan Balance Second Reminder Letter is a formal notification issued when a previous request for payment remains unaddressed. It serves as a critical final opportunity to settle arrears before the lender initiates formal recovery actions or imposes penalties. This document typically outlines the total debt, accrued interest, and a strict deadline for remittance. Reviewing this notice immediately is essential to protect your credit score and avoid potential legal proceedings or additional late fees. Timely communication with the creditor may still allow for restructured repayment terms or debt settlement options.

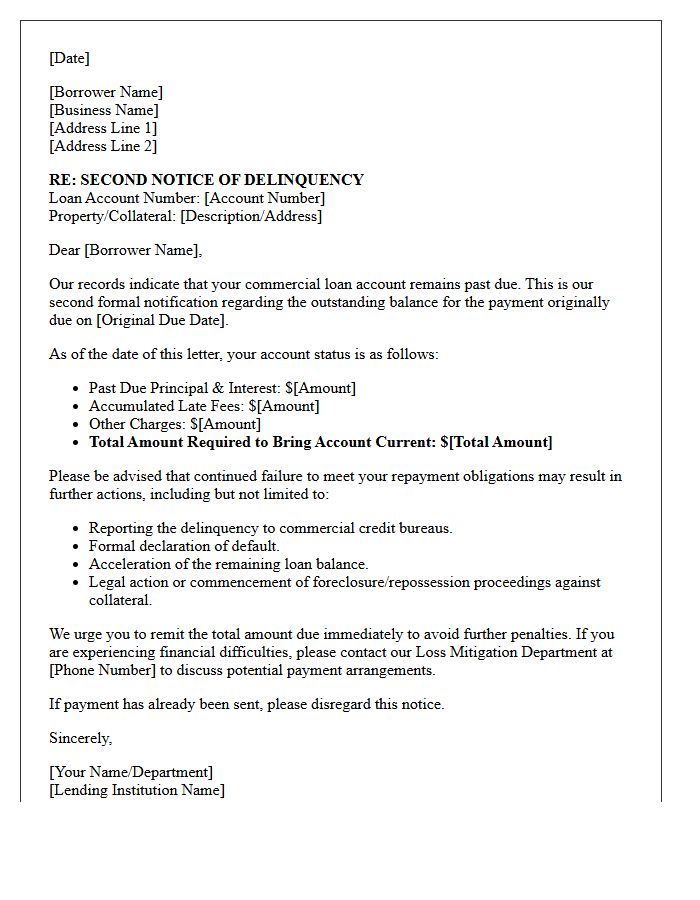

Second Delinquency Notification Letter for Commercial Loan

A Second Delinquency Notification Letter serves as a critical formal warning for commercial borrowers who failed to resolve missed payments after the initial notice. This document confirms the default status of the commercial loan and outlines potential legal consequences, including acceleration of the debt or foreclosure actions. It is essential for borrowers to communicate with lenders immediately to discuss workout agreements or restructuring options. Timely response is vital to prevent permanent damage to corporate credit scores and the possible seizure of business collateral or personal assets used as security.

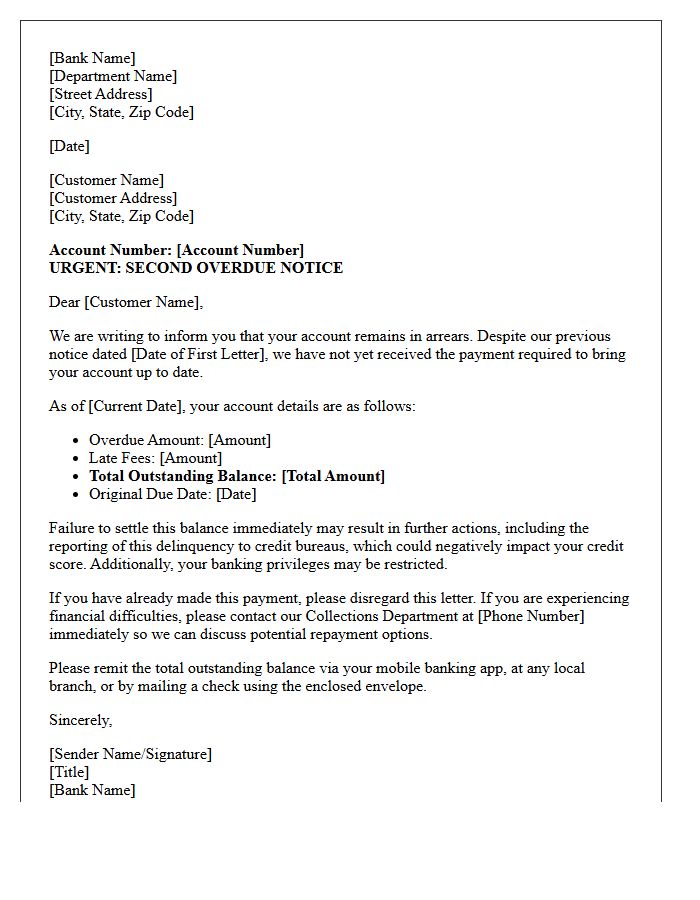

Retail Banking Second Overdue Payment Letter

A retail banking second overdue payment letter serves as a formal follow-up regarding a delinquent account. It warns customers that their credit score may be negatively impacted and additional late fees will apply. This notice emphasizes the urgency of settling the outstanding balance immediately to avoid further collection actions or legal measures. Banks often include repayment options or contact details for financial assistance to encourage resolution before the account is classified as a default, which severely limits future borrowing capacity and financial stability.

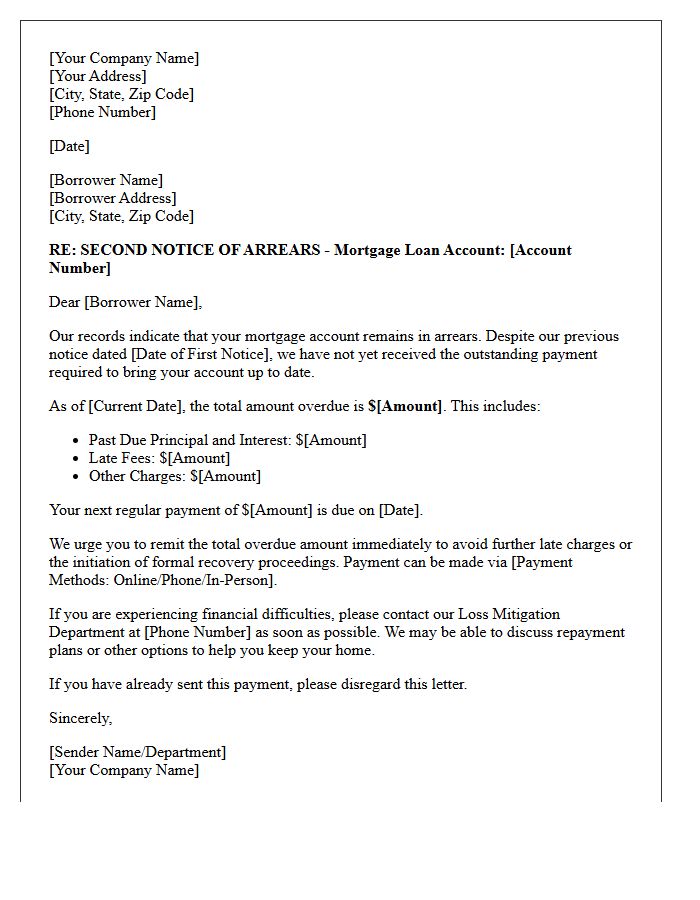

Second Notice of Arrears Letter for Mortgage Loan

A second notice of arrears serves as a formal warning that your mortgage delinquency remains unresolved. This document indicates that initial contact attempts failed and your account is now in a critical stage of default. It is essential to seek legal advice or contact your lender immediately to discuss repayment plans. Ignoring this letter significantly increases the risk of the lender initiating formal foreclosure proceedings. Take action now to explore loss mitigation options, such as loan modification or forbearance, to protect your property and stabilize your financial situation before further penalties accrue.

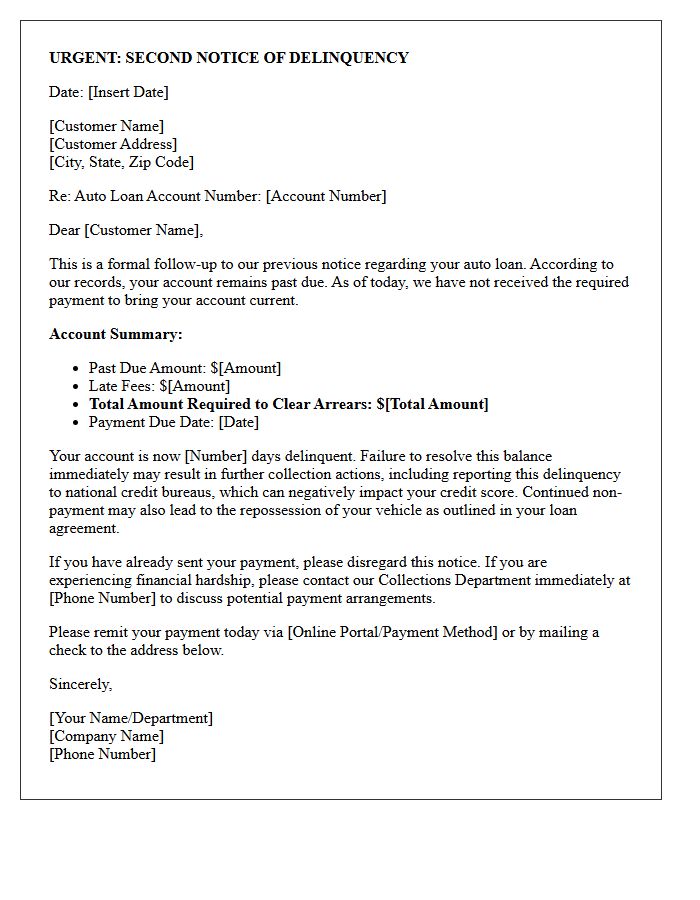

Auto Loan Second Delinquency Warning Letter

An Auto Loan Second Delinquency Warning Letter is a critical formal notice indicating that your vehicle financing is severely past due. This document serves as a final opportunity to resolve arrears before the lender initiates aggressive collection actions. Receiving this letter means your account is nearing repossession status, which will significantly damage your credit score. It is essential to contact your lienholder immediately to discuss repayment plans or loan modifications to prevent the loss of your transportation and maintain long-term financial stability.

Second Past Due Loan Installment Letter

A second past due loan installment letter serves as a formal demand for payment after an initial reminder was ignored. It is a critical legal step before a lender initiates debt collection or reports the delinquency to credit bureaus. This document typically outlines the total outstanding balance, including late fees, and provides a final deadline to avoid account default. Receivers should prioritize immediate repayment negotiation or communication with the creditor to prevent severe damage to their credit score and potential legal action or asset repossession.

Unpaid Personal Loan Second Request Letter

An Unpaid Personal Loan Second Request Letter serves as a final formal notice before escalating debt recovery actions. This document reminds the borrower of their missed payment, includes the total outstanding balance, and specifies a strict deadline for resolution. It is a critical step in maintaining a paper trail for potential legal proceedings or credit reporting. Clear communication at this stage may offer a last chance for a repayment plan, helping both parties avoid the costs and complications of formal litigation or professional collection agencies.

Second Notice Letter Regarding Delinquent Loan Account

A Second Notice Letter serves as a critical final warning regarding a delinquent loan account. Receiving this document indicates that previous payment requests were ignored and the lender is preparing for further escalation. It typically outlines the total overdue balance, late fees, and a firm deadline for payment. Ignoring this notice can lead to severe credit score damage, loss of collateral, or legal action. To prevent default, borrowers should immediately contact their creditor to negotiate a repayment plan or settle the outstanding debt before the account moves to formal collections.

Escalated Loan Payment Delinquency Second Letter

An Escalated Loan Payment Delinquency Second Letter serves as a final formal warning before severe legal action or credit impairment occurs. This document indicates that previous attempts to resolve the overdue balance have failed. It typically outlines the total amount due, including accrued interest and late fees, while specifying a strict deadline for payment. Ignoring this notice often leads to loan default, asset repossession, or debt transfer to a third-party collection agency. Immediate communication with the lender is essential to discuss potential repayment plans and avoid long-term financial consequences.

Second Reminder Letter for Non-Performing Loan

A second reminder letter for a non-performing loan serves as a final formal notice before the creditor initiates legal action or debt recovery proceedings. It highlights the continued breach of contract and specifies the total outstanding balance, including accrued interest and late fees. Receiving this document indicates that your account status is critical. To avoid foreclosure or a severely damaged credit score, you must immediately contact the lender to negotiate a repayment plan or settlement. Ignoring this communication typically leads to the permanent loss of collateral or judicial intervention.

What is a Second Notice of Loan Payment Delinquency?

A Second Notice of Loan Payment Delinquency is a formal communication sent by a lender when a borrower has failed to remit payment for two consecutive billing cycles. It serves as a final warning before the account is escalated to more severe collection actions or legal proceedings.

How does receiving a second delinquency notice affect my credit score?

Receiving a second notice typically indicates that your account is 60 days past due. This status is reported to credit bureaus and can cause a significant drop in your credit score, making it harder to secure future financing or favorable interest rates.

What are the consequences of ignoring a second payment notice?

Ignoring a second notice can lead to the acceleration of the loan, where the full balance becomes due immediately. It may also result in the account being sent to a third-party collection agency, the initiation of foreclosure or repossession proceedings, and additional late fees or legal costs.

Can I still negotiate a payment plan after a second notice?

Yes, most lenders are willing to discuss loss mitigation options even after a second notice. You may be eligible for a loan modification, a temporary forbearance, or a structured repayment plan to bring the account current and avoid further escalation.

What steps should I take immediately after receiving this notice?

You should immediately contact your lender's loss mitigation department to explain your financial situation. Document all communications, review your budget to determine what you can afford to pay, and consider seeking advice from a certified credit counselor to explore your debt relief options.

Comments