Stay informed with our latest Consumer Protection Regulatory Update Letter, designed to help businesses navigate evolving compliance standards and legal requirements. This essential guide simplifies complex legislative changes to ensure your operations remain transparent and consumer-friendly. Review the critical insights to protect your brand reputation and mitigate risks. To streamline your communication process, below are some ready to use template.

Image cover: Latest Consumer Protection Regulatory Update: Official Letter Templates and Compliance Samples

Letter Samples List

- Truth In Lending Act Regulatory Update Letter

- Electronic Fund Transfer Act Compliance Letter

- Fair Credit Reporting Act Policy Update Letter

- Equal Credit Opportunity Act Notification Letter

- Consumer Financial Protection Bureau Guidance Letter

- Gramm-Leach-Bliley Act Privacy Standard Letter

- Overdraft Protection Fee Schedule Update Letter

- Mortgage Servicing Rights And Disclosure Letter

- Fair Debt Collection Practices Act Update Letter

- Unfair Deceptive Or Abusive Acts Prevention Letter

- Customer Dispute And Complaint Resolution Update Letter

- Consumer Fraud Protection Regulatory Update Letter

- Real Estate Settlement Procedures Act Notice Letter

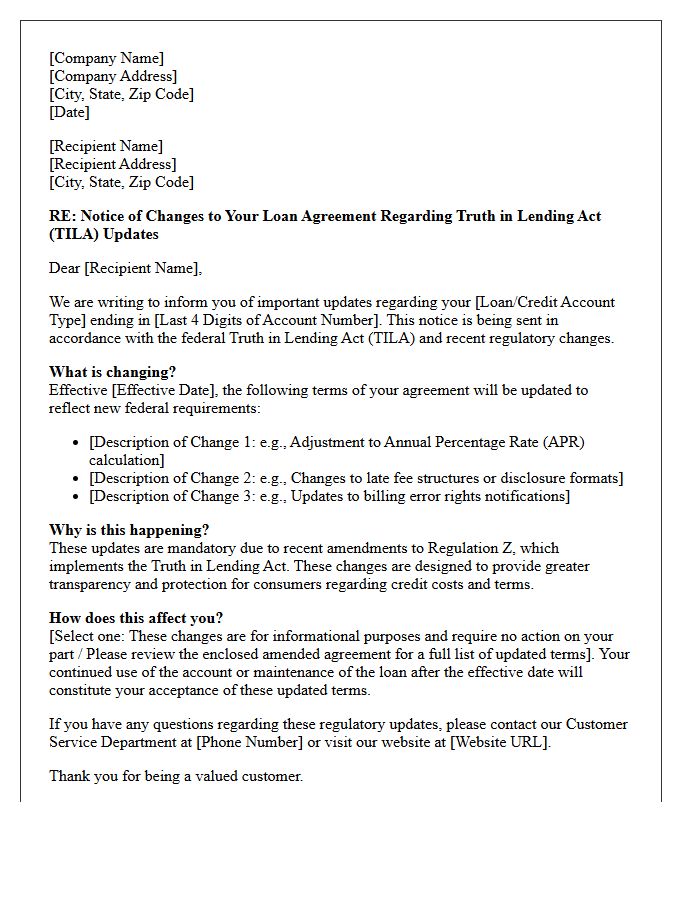

Truth In Lending Act Regulatory Update Letter

The Truth In Lending Act Regulatory Update Letter serves as a critical compliance notification regarding mandatory changes to Regulation Z. Financial institutions must review these updates to ensure accurate disclosure of annual percentage rates, finance charges, and loan terms. Staying current with these amendments helps lenders mitigate legal risks and maintain transparency with consumers. Failure to implement these regulatory adjustments can lead to significant penalties and compliance violations. This document is essential for mapping institutional policy to evolving federal credit standards and consumer protection requirements.

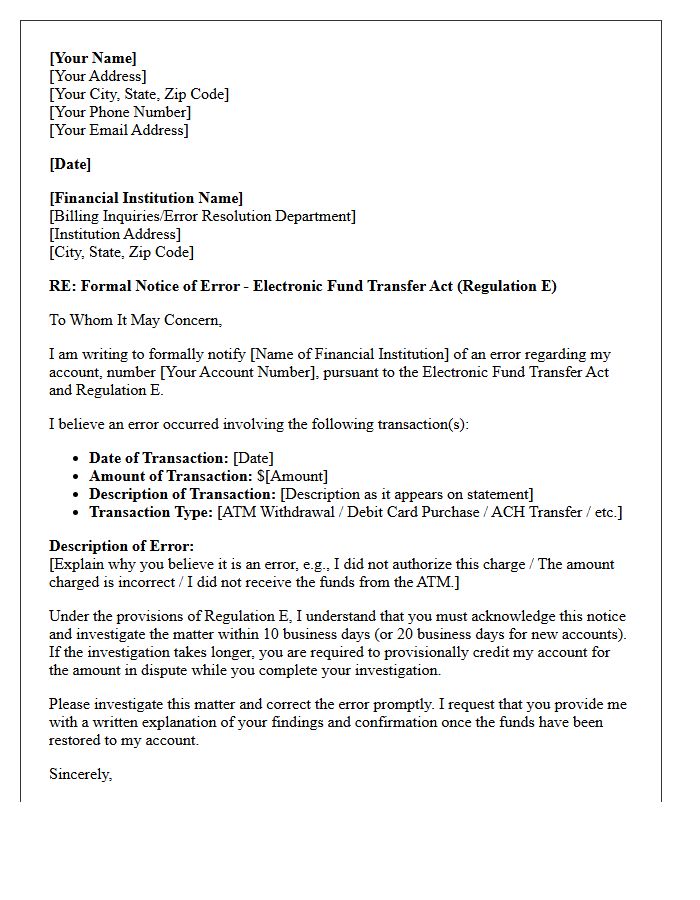

Electronic Fund Transfer Act Compliance Letter

An Electronic Fund Transfer Act Compliance Letter is a formal notice used to report unauthorized transactions or billing errors. Under Regulation E, consumers must notify their financial institution within sixty days of a statement date to protect their legal rights. The letter must detail the specific error, the date, and the disputed amount. Providing this written documentation ensures the bank investigates the claim and initiates provisional credit if the process exceeds ten business days. Timely submission is critical to limit personal liability for fraudulent electronic transfers and maintain account security.

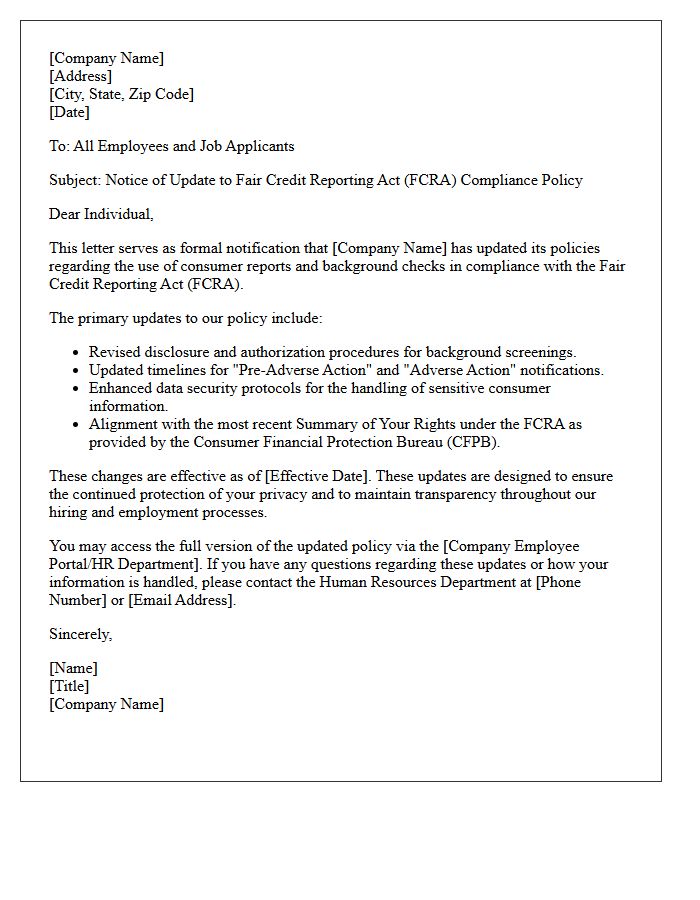

Fair Credit Reporting Act Policy Update Letter

A Fair Credit Reporting Act Policy Update Letter notifies consumers and employees about regulatory changes regarding their financial data privacy. This document explains how an organization collects, stores, and shares consumer report information to ensure legal compliance. It is critical to understand your rights, including the ability to dispute inaccuracies and restrict access to your credit history. Recipients must review these updates to verify that data protection standards meet federal requirements, safeguarding against identity theft and ensuring transparency in all reporting procedures mandated by the FCRA.

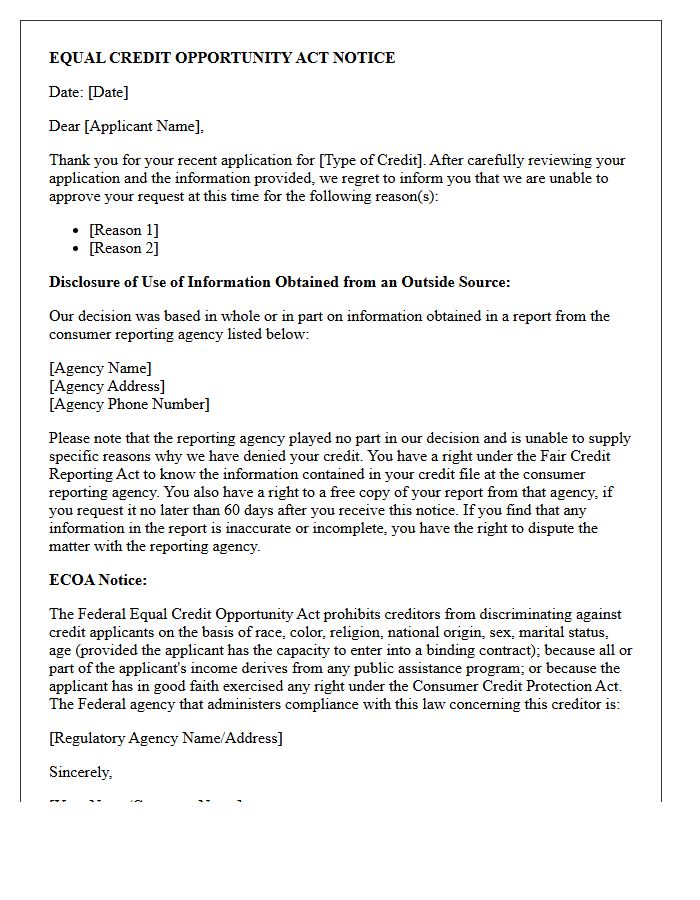

Equal Credit Opportunity Act Notification Letter

An Equal Credit Opportunity Act Notification Letter is a mandatory document issued when a lender denies credit or offers less favorable terms. It ensures transparency by requiring creditors to provide specific reasons for an adverse action within thirty days. This protection prevents discrimination based on race, religion, gender, or age. Understanding this notice is essential for consumers to identify potential errors in their credit profile, exercise their right to fair lending practices, and take necessary steps to improve their financial standing for future applications.

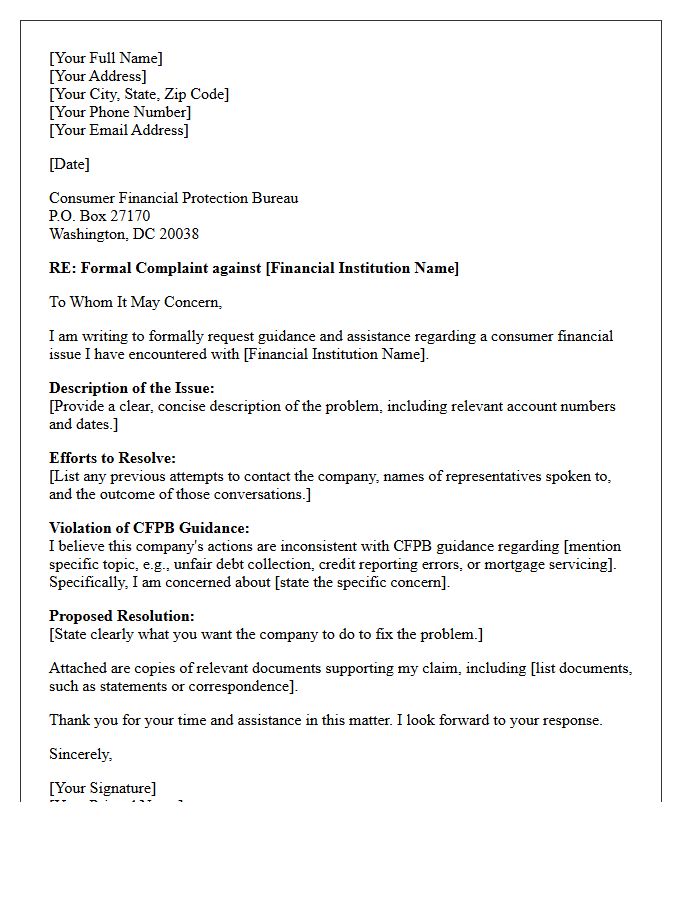

Consumer Financial Protection Bureau Guidance Letter

The Consumer Financial Protection Bureau (CFPB) Guidance Letter serves as an official advisory to financial institutions regarding regulatory expectations. It clarifies how federal laws apply to modern products like junk fees, algorithmic lending, and banking automation. These letters highlight compliance standards to prevent unfair, deceptive, or abusive acts. For consumers and businesses, understanding these documents is essential for ensuring legal protection and maintaining transparency in financial markets. They signal upcoming enforcement priorities, helping organizations mitigate risks while protecting the financial well-being of the public from systemic industry malpractices.

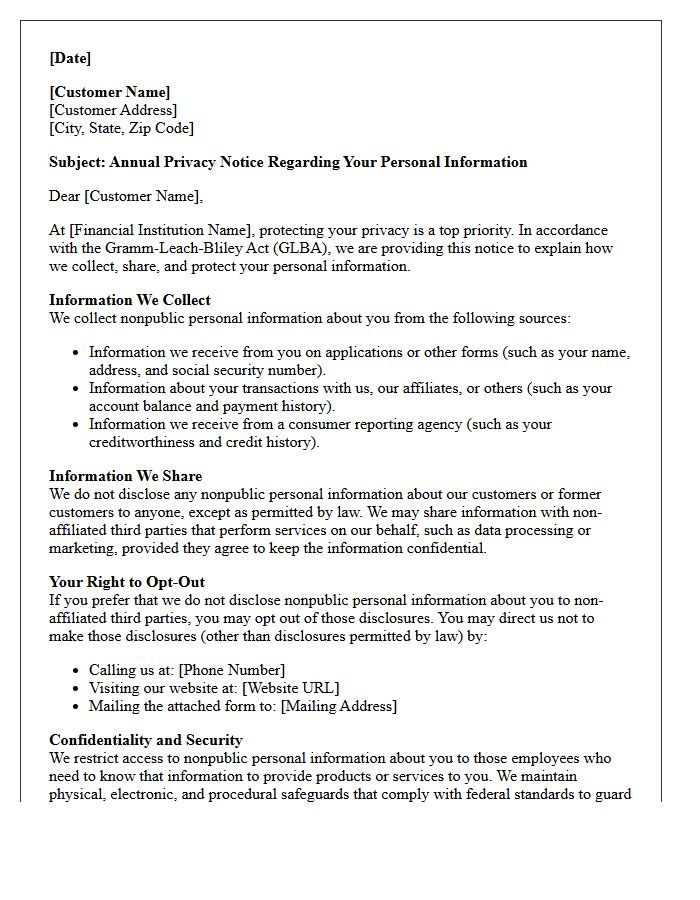

Gramm-Leach-Bliley Act Privacy Standard Letter

The Gramm-Leach-Bliley Act (GLBA) Privacy Standard Letter is a mandatory notice financial institutions must provide to consumers. It explains how your nonpublic personal information is collected, shared, and protected. A key requirement is the Opt-Out Right, which allows individuals to restrict the sharing of their data with non-affiliated third parties. This transparency ensures compliance with federal privacy regulations while safeguarding sensitive financial data against unauthorized access. Reviewing this document helps you understand your data privacy rights and the security measures used to defend your personal financial identity.

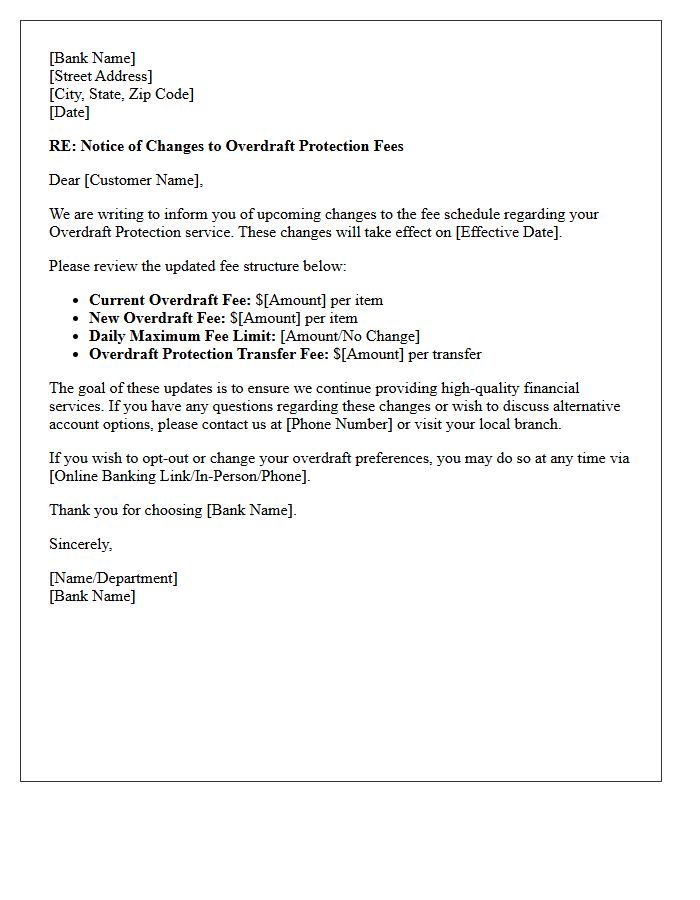

Overdraft Protection Fee Schedule Update Letter

An Overdraft Protection Fee Schedule Update Letter is a formal notification from your bank regarding changes to service charges. It is crucial to review this document to understand new transaction costs, daily limits, and penalty structures. These updates directly impact your account balance if you spend more than your available funds. Pay close attention to the effective date to avoid unexpected fees. Comparing the revised rates with your current spending habits helps you decide whether to maintain, adjust, or opt-out of your existing overdraft protection coverage to ensure financial stability.

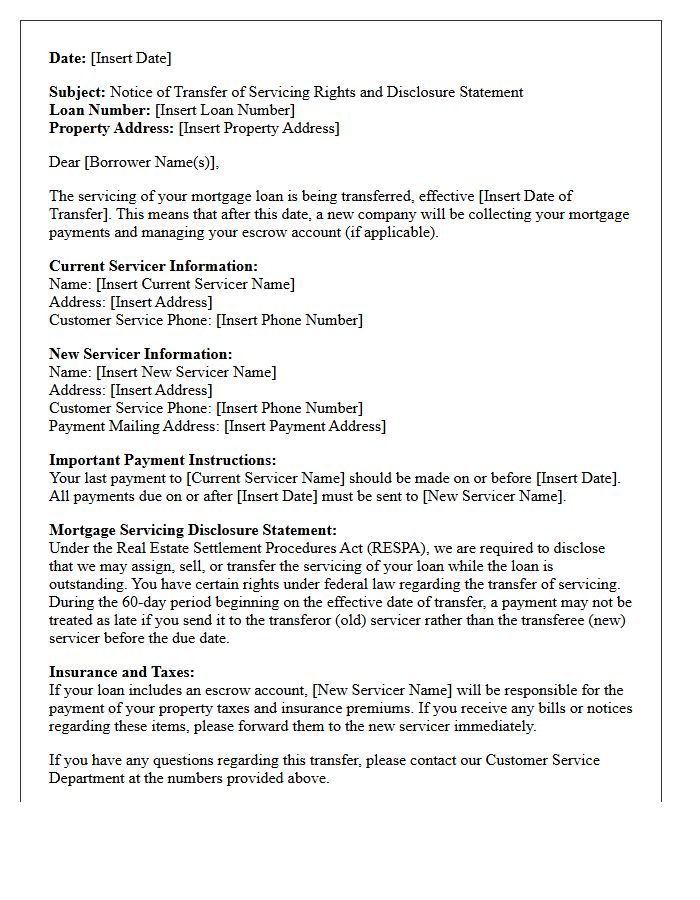

Mortgage Servicing Rights And Disclosure Letter

A Mortgage Servicing Rights (MSR) transfer occurs when the right to manage your loan is sold to a new company. This change does not alter your loan terms but affects where you send payments. Federal law requires a Disclosure Letter, often called a "goodbye" and "hello" notice, to be sent by both the current and new servicers. This document provides the effective transfer date and new contact information. Always verify these notices to prevent payment errors or fraud during the transition period.

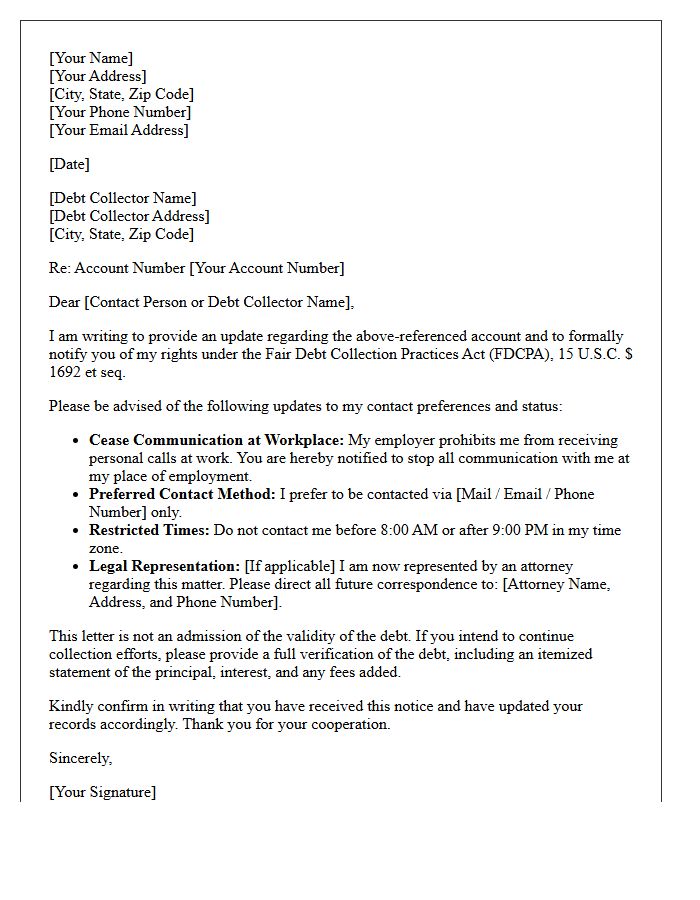

Fair Debt Collection Practices Act Update Letter

A Fair Debt Collection Practices Act (FDCPA) Update Letter is a critical formal notice used to inform consumers of their legal protections against abusive recovery tactics. This document ensures compliance with federal regulations by outlining your right to dispute a debt and request verification. It must clearly state the collector's identity and provide a validation period of thirty days. Receiving this letter is a vital step in maintaining consumer privacy and preventing harassment, as it establishes the official framework for all future communication regarding your financial obligations.

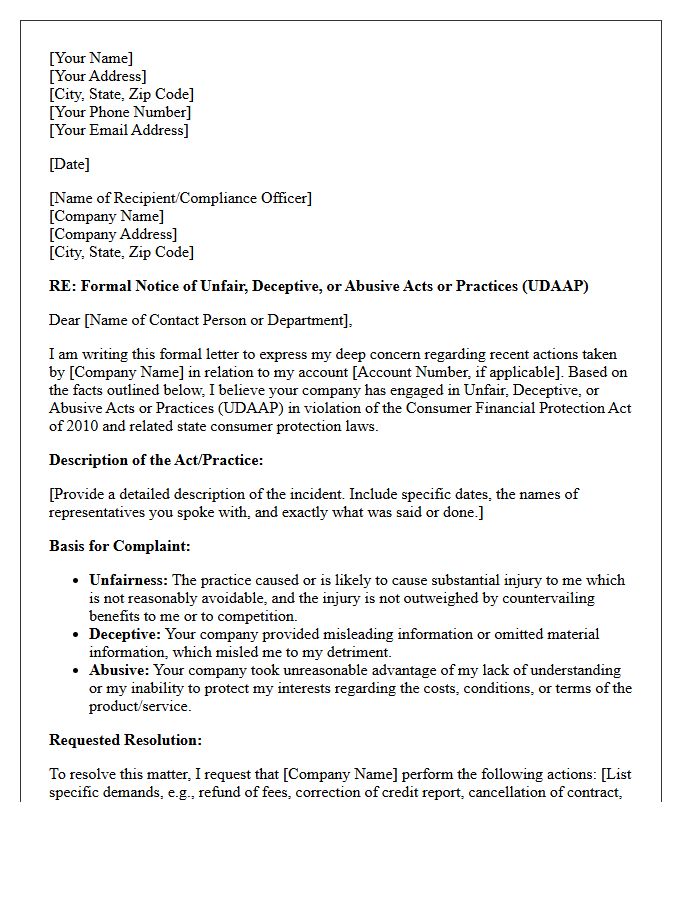

Unfair Deceptive Or Abusive Acts Prevention Letter

An Unfair, Deceptive, or Abusive Acts or Practices (UDAAP) prevention letter is a formal document used to ensure compliance with consumer protection laws. It outlines specific regulatory standards to prevent misleading representations, lack of transparency, or practices that cause substantial injury to consumers. Financial institutions use these letters to mandate corrective actions, ensuring all marketing and service activities are ethical and legal. Implementing these protocols is essential for mitigating legal risks, avoiding heavy regulatory fines, and maintaining institutional integrity within the marketplace.

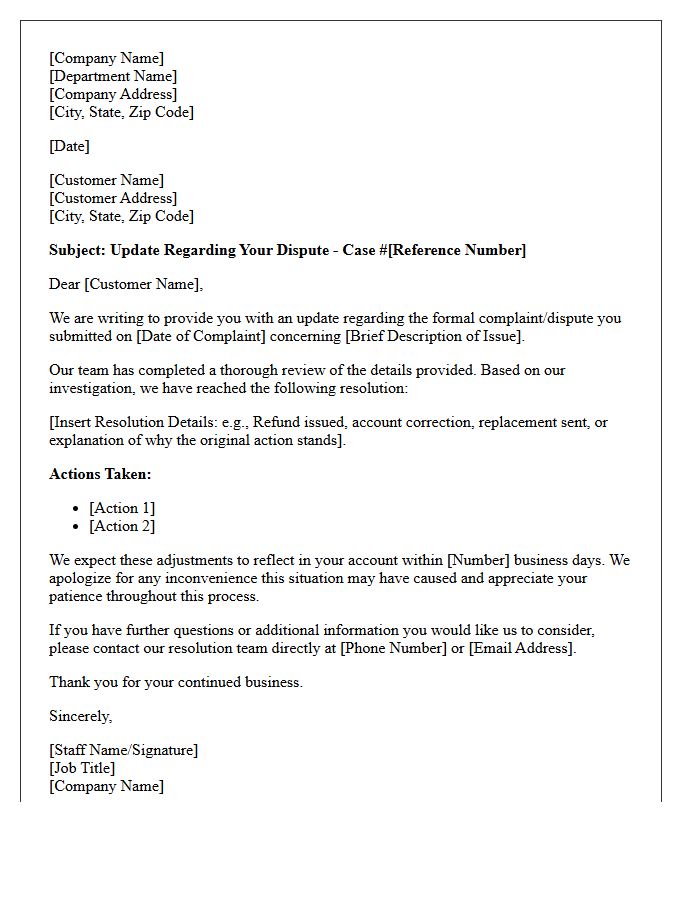

Customer Dispute And Complaint Resolution Update Letter

A Customer Dispute and Complaint Resolution Update Letter is an essential communication tool used to inform clients about the progress of their formal grievances. This document ensures transparency by detailing the investigation steps taken, any preliminary findings, and the anticipated timeline for a final decision. Providing regular updates helps maintain customer trust and demonstrates a commitment to fair treatment. Clearly outlining the resolution process reduces frustration and prevents further escalation, ensuring the professional management of sensitive service issues while maintaining a positive relationship with the consumer throughout the reconciliation period.

Consumer Fraud Protection Regulatory Update Letter

A Consumer Fraud Protection Regulatory Update Letter is a critical communication notifying financial institutions of new compliance mandates. These letters outline updated legal frameworks designed to combat evolving deceptive practices and identity theft. Staying informed is essential for maintaining regulatory adherence and ensuring robust consumer data security. Failure to implement these changes can lead to significant legal penalties and reputational damage. Organizations must prioritize reviewing these updates to enhance their fraud prevention strategies and protect customer assets within the current financial landscape.

Real Estate Settlement Procedures Act Notice Letter

The Real Estate Settlement Procedures Act (RESPA) notice letter is a mandatory disclosure sent to borrowers when their mortgage servicing rights are transferred. Under federal law, lenders must provide a Notice of Transfer of Servicing at least 15 days before the effective date. This document ensures transparency regarding where to send monthly payments and how to contact the new servicer. It protects homeowners by providing a 60-day grace period during which late fees cannot be charged if payments are mistakenly sent to the previous lender, maintaining financial stability during transitions.

What is a Consumer Protection Regulatory Update Letter?

A Consumer Protection Regulatory Update Letter is an official communication sent by regulatory bodies or legal departments to inform businesses and consumers about recent changes, amendments, or new enforcement priorities in consumer protection laws.

Why did I receive a notice regarding new consumer protection regulations?

Businesses receive these notices to ensure legal compliance with evolving standards, while consumers receive them to stay informed about their strengthened rights regarding data privacy, fair lending, and protection against deceptive marketing practices.

How do these regulatory updates affect existing consumer contracts?

New regulations may mandate updates to terms of service, privacy policies, or refund procedures; companies are typically required to implement these changes by a specific effective date to remain compliant with the latest consumer safeguards.

What are the penalties for non-compliance with the updated consumer laws?

Failure to adhere to the requirements outlined in the regulatory update can result in significant administrative fines, mandatory audits, consumer restitution orders, and potential litigation from state or federal oversight agencies.

Where can I find more details about specific consumer protection amendments?

Detailed information is usually available through official government portals such as the Federal Trade Commission (FTC) or the Consumer Financial Protection Bureau (CFPB), as well as within the specific legal citations provided in your update letter.

Comments