Regulators issued the Credit Allowance Methodology Advisory Letter to provide essential guidance on calculating expected loan losses. This document outlines best practices for financial institutions to maintain robust risk management and ensure accounting compliance. Understanding these standards is critical for accurate financial reporting and regulatory alignment. To assist your implementation, below are some ready to use template.

Image cover: Effective Templates and Advisory Letter Samples for Credit Allowance Methodology

Letter Samples List

- Current Expected Credit Loss Methodology Advisory Letter

- Allowance For Loan And Lease Losses Assessment Letter

- Credit Impairment Model Validation Advisory Letter

- Historical Loss Rate Methodology Review Letter

- Macroeconomic Factor Integration Advisory Letter

- Probability Of Default Modeling Advisory Letter

- Loss Given Default Calculation Advisory Letter

- Qualitative Framework Adjustment Advisory Letter

- Credit Risk Provisioning Strategy Advisory Letter

- Portfolio Segmentation Methodology Advisory Letter

- Forward Looking Information Assessment Letter

- Credit Allowance Scenario Analysis Advisory Letter

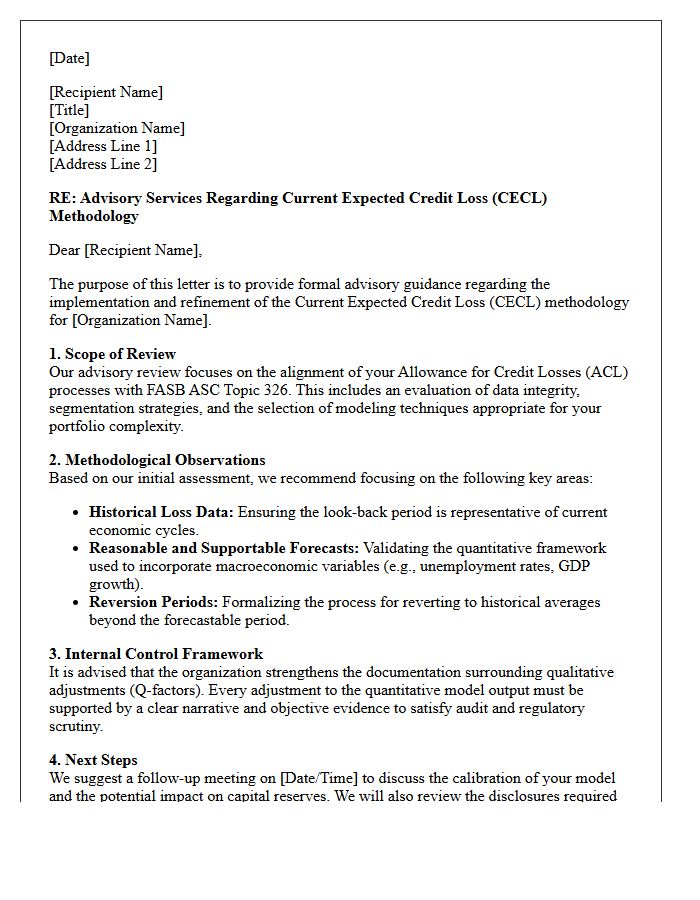

Current Expected Credit Loss Methodology Advisory Letter

The Current Expected Credit Loss (CECL) methodology shifts financial institutions from an incurred loss model to an expected loss framework. This advisory letter emphasizes that banks must estimate lifetime credit losses at the time of asset origination. Key considerations include utilizing historical data, current economic conditions, and reasonable forecasts to determine allowance levels. Compliance requires robust internal controls and granular data collection to ensure accurate financial reporting. This forward-looking approach ensures capital adequacy against potential future defaults, maintaining overall banking stability through proactive risk management and transparent valuation standards.

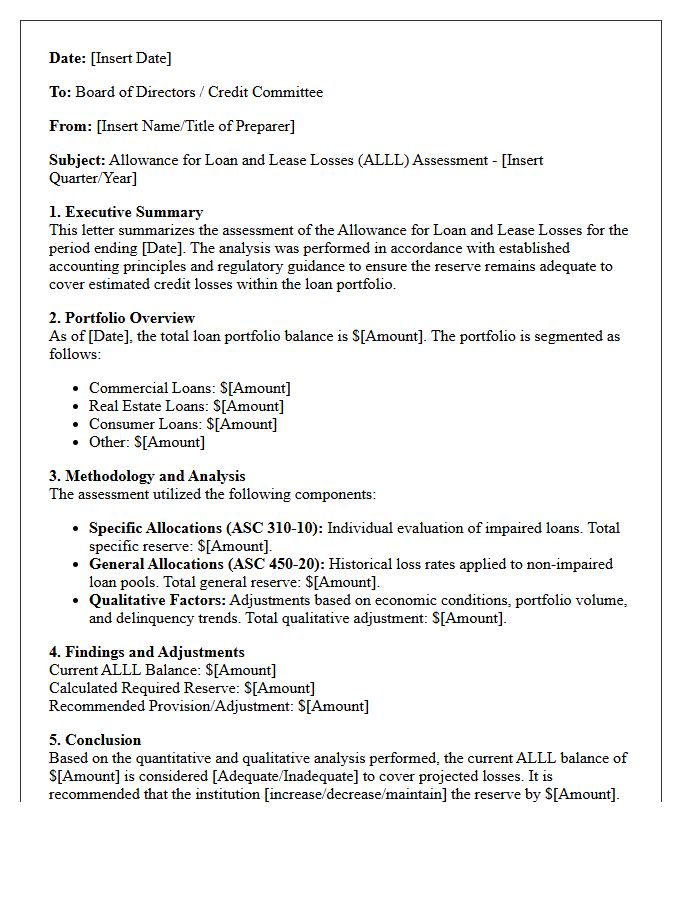

Allowance For Loan And Lease Losses Assessment Letter

The Allowance for Loan and Lease Losses Assessment Letter is a critical regulatory document used by financial institutions to justify their reserves against potential credit defaults. It outlines the methodology and qualitative factors used to estimate credit risk within a loan portfolio. Maintaining an accurate assessment ensures compliance with GAAP standards and provides transparency for bank examiners. This letter serves as formal evidence that management has rigorously evaluated economic conditions and historical loss data to maintain adequate capital buffers against unforeseen financial losses.

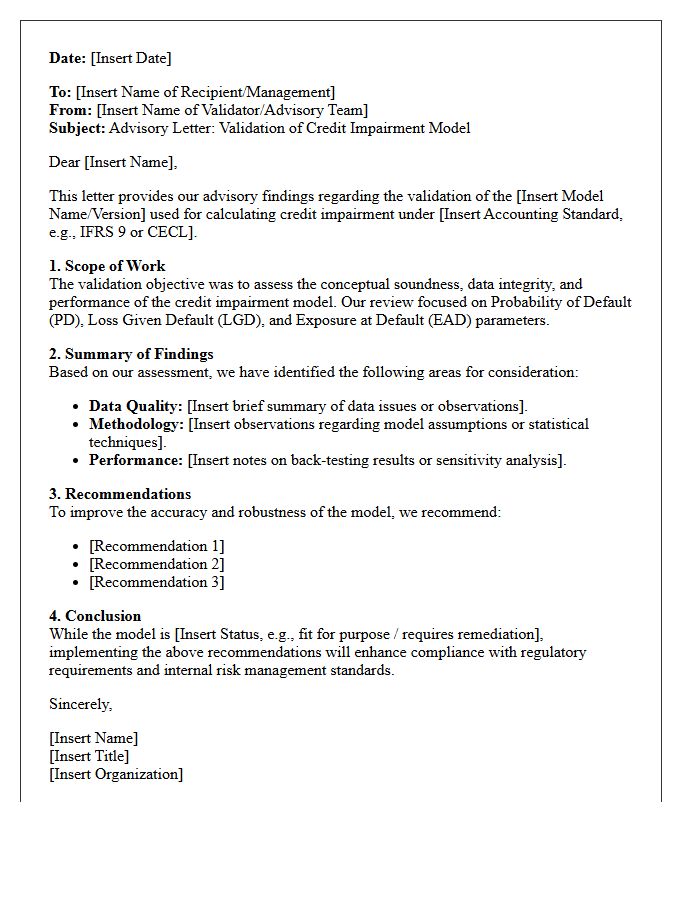

Credit Impairment Model Validation Advisory Letter

The Credit Impairment Model Validation Advisory Letter provides critical regulatory guidance on assessing the accuracy and robustness of financial loss estimation processes. It emphasizes that institutions must perform rigorous independent validation of their models to ensure compliance with accounting standards like CECL or IFRS 9. Key focuses include data integrity, conceptual soundness, and ongoing monitoring to mitigate model risk. Proper validation confirms that credit impairment calculations are reliable, transparent, and capable of reflecting changing economic conditions for sound risk management.

Historical Loss Rate Methodology Review Letter

A Historical Loss Rate Methodology Review Letter is a formal assessment evaluating the accuracy of a financial institution's credit loss estimations. This document confirms if the applied calculation methods align with current regulatory standards and economic conditions. It identifies potential weaknesses in data segmentation, look-back periods, and qualitative adjustments. Ensuring the methodology is statistically sound helps maintain adequate capital reserves. For auditors and stakeholders, this letter serves as essential evidence that the institution effectively quantifies credit risk exposure based on realized historical performance trends.

Macroeconomic Factor Integration Advisory Letter

A Macroeconomic Factor Integration Advisory Letter provides institutional investors with guidance on embedding systemic variables into portfolio construction. It emphasizes how inflation, interest rates, and GDP growth influence long-term asset valuations and risk exposure. By utilizing quantitative modeling, the letter helps fiduciaries align their strategies with shifting economic cycles. The primary objective is to enhance resilience against market volatility through top-down analysis. This formal communication ensures that investment decisions are informed by structural trends, ultimately optimizing risk-adjusted returns within a complex global financial landscape.

Probability Of Default Modeling Advisory Letter

The Probability of Default Modeling Advisory Letter provides critical regulatory guidance for financial institutions developing credit risk frameworks. It emphasizes the need for robust statistical validation, sound governance, and data integrity when estimating the likelihood of borrower insolvency. Banks must ensure their PD models are sensitive to economic cycles and internal risk ratings. Adhering to these supervisory expectations is essential for maintaining regulatory compliance, ensuring capital adequacy, and enhancing the accuracy of risk-weighted asset calculations within a bank's internal ratings-based approach.

Loss Given Default Calculation Advisory Letter

A Loss Given Default (LGD) Calculation Advisory Letter provides critical regulatory guidance on estimating the net loss a financial institution incurs when a borrower defaults. It outlines expectations for economic loss measurement, including recovery costs, timing, and discount rates. Banks must ensure their internal models align with supervisory standards to maintain accurate capital requirements. Adhering to these guidelines helps mitigate credit risk and ensures compliance with Basel framework policies, emphasizing the importance of robust data validation and transparent methodology in risk management reporting.

Qualitative Framework Adjustment Advisory Letter

A Qualitative Framework Adjustment Advisory Letter is a formal notification issued by financial regulators or auditors to address necessary changes in an organization's risk assessment models. It focuses on subjective enhancements and internal controls rather than purely quantitative data. This document outlines required methodological updates to improve governance, compliance, and decision-making processes. Recipient institutions must implement these adjustments to ensure their risk management frameworks remain robust, accurate, and aligned with evolving regulatory expectations and market conditions.

Credit Risk Provisioning Strategy Advisory Letter

A Credit Risk Provisioning Strategy Advisory Letter provides essential guidance on estimating Expected Credit Losses (ECL) to ensure regulatory compliance. This document outlines the methodology for calculating financial reserves against potential loan defaults. It highlights critical factors like forward-looking economic indicators, historical loss data, and risk mitigation techniques. By following this expert advice, financial institutions can maintain capital adequacy and transparency under frameworks like IFRS 9 or CECL. Ultimately, it serves as a strategic roadmap for proactive risk management and accurate balance sheet reporting.

Portfolio Segmentation Methodology Advisory Letter

A Portfolio Segmentation Methodology Advisory Letter provides a strategic framework for categorizing assets based on risk, liquidity, and performance objectives. This document outlines the governance standards required to ensure consistent classification across diverse investment holdings. By defining clear parameters for asset allocation and sub-asset classes, the letter helps institutions mitigate concentration risk and align their portfolios with specific regulatory mandates. Ultimately, it serves as a formal guide to optimizing capital efficiency and enhancing data transparency through systematic, methodology-driven reporting for stakeholders and internal investment committees.

Forward Looking Information Assessment Letter

A Forward Looking Information Assessment Letter is a critical document used by lenders to evaluate a borrower's future financial viability. It focuses on predictive data, such as projected cash flows and market trends, rather than historical performance alone. This assessment helps financial institutions determine credit risk and loan eligibility under evolving economic conditions. Providing accurate projections within this letter ensures transparency, allowing stakeholders to gauge the sustainability of a business model and its ability to meet future debt obligations in a volatile marketplace.

Credit Allowance Scenario Analysis Advisory Letter

A Credit Allowance Scenario Analysis Advisory Letter provides a strategic evaluation of potential loan losses under various economic conditions. It outlines how forward-looking assessments and hypothetical shifts impact financial reserves. This advisory tool helps institutions refine their Expected Credit Loss models and ensures regulatory compliance. By examining credit risk exposure through multiple stress tests, the letter offers actionable insights for maintaining capital adequacy and enhancing portfolio resilience. It serves as a critical document for stakeholders to understand the sensitivity of credit allowances to volatile market fluctuations and evolving economic trends.

What is the purpose of the Credit Allowance Methodology Advisory Letter?

The advisory letter provides formal guidance to financial institutions on establishing and maintaining a robust methodology for estimating credit losses, ensuring compliance with current accounting standards such as CECL (Current Expected Credit Losses).

What are the core components of an acceptable credit allowance methodology?

An acceptable methodology must include a systematic process for evaluating credit risk, documentation of historical loss data, adjustments for current conditions, and reasonable and supportable forecasts for future economic environments.

How does the advisory letter address qualitative factor adjustments?

The letter emphasizes that qualitative adjustments should be used to account for factors not captured in historical data, such as changes in underwriting standards, economic trends, and portfolio concentrations, provided they are supported by clear documentation.

What documentation is required for credit allowance validation?

Financial institutions must maintain comprehensive records that justify their estimation techniques, including the rationale for model selection, data integrity checks, and evidence of periodic independent validation of the methodology.

How often should a financial institution review its credit allowance methodology?

The advisory recommends a formal review at least annually or whenever significant changes occur in the institution's risk profile, economic conditions, or regulatory requirements to ensure the allowance remains adequate and accurate.

Comments