The Interagency Supervisory Guidance Letter provides critical regulatory expectations for financial institutions managing third-party risks and operational resilience. This document outlines standardized safety and soundness practices coordinated across multiple governing bodies to ensure systemic stability. Understanding these compliance mandates is essential for maintaining robust governance frameworks and avoiding enforcement actions. To simplify your compliance journey, below are some ready to use template.

Image cover: Official Templates and Professional Samples for Interagency Supervisory Guidance Letters

Letter Samples List

- Interagency Supervisory Guidance Letter on Commercial Real Estate Risk Management

- Interagency Supervisory Guidance Letter on Third-Party Relationship Risk

- Interagency Supervisory Guidance Letter Regarding Anti-Money Laundering Compliance

- Interagency Supervisory Guidance Letter on Climate-Related Financial Risk Management

- Interagency Supervisory Guidance Letter Addressing Cybersecurity Incident Notification

- Interagency Supervisory Guidance Letter on Liquidity Risk Management Practices

- Interagency Supervisory Guidance Letter Concerning Model Risk Management

- Interagency Supervisory Guidance Letter on Fair Lending Compliance and Enforcement

- Interagency Supervisory Guidance Letter Regarding Crypto-Asset Related Activities

- Interagency Supervisory Guidance Letter on Capital Adequacy and Stress Testing

- Interagency Supervisory Guidance Letter Addressing Consumer Protection Practices

- Interagency Supervisory Guidance Letter on Leveraged Lending Activities

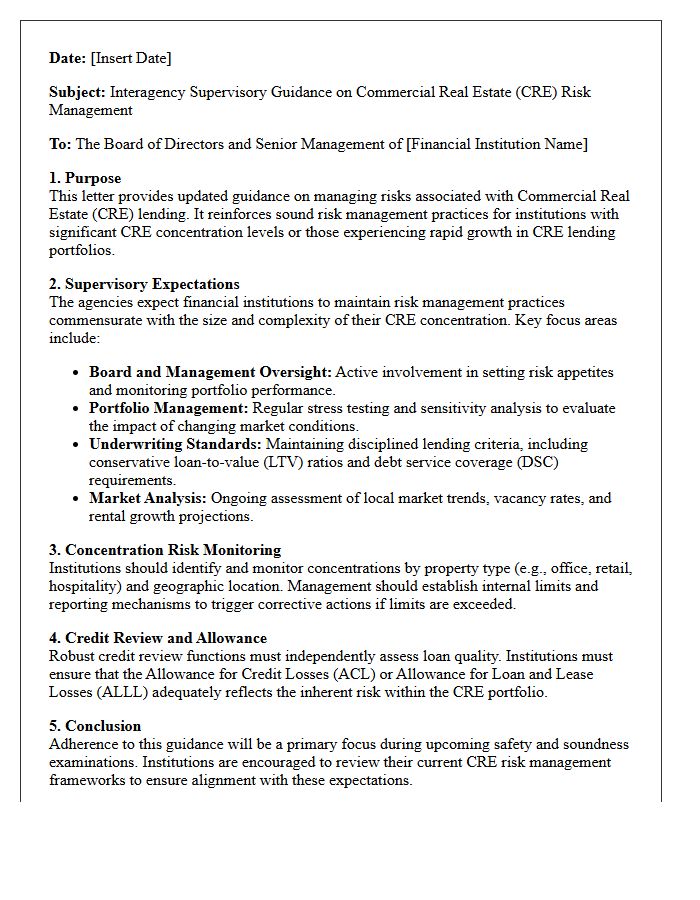

Interagency Supervisory Guidance Letter on Commercial Real Estate Risk Management

The Interagency Supervisory Guidance emphasizes the importance of Risk Management Practices for financial institutions with significant exposure to commercial real estate. It highlights that lenders must maintain robust Internal Controls, including stress testing and portfolio monitoring, especially when CRE concentrations exceed specific thresholds. Banks are expected to implement disciplined underwriting standards and adequate Capital Levels to mitigate potential losses. This guidance ensures that credit risk remains manageable during economic fluctuations, urging boards of directors to oversee strategic Risk Appetite and ensure long-term financial stability within the evolving real estate market.

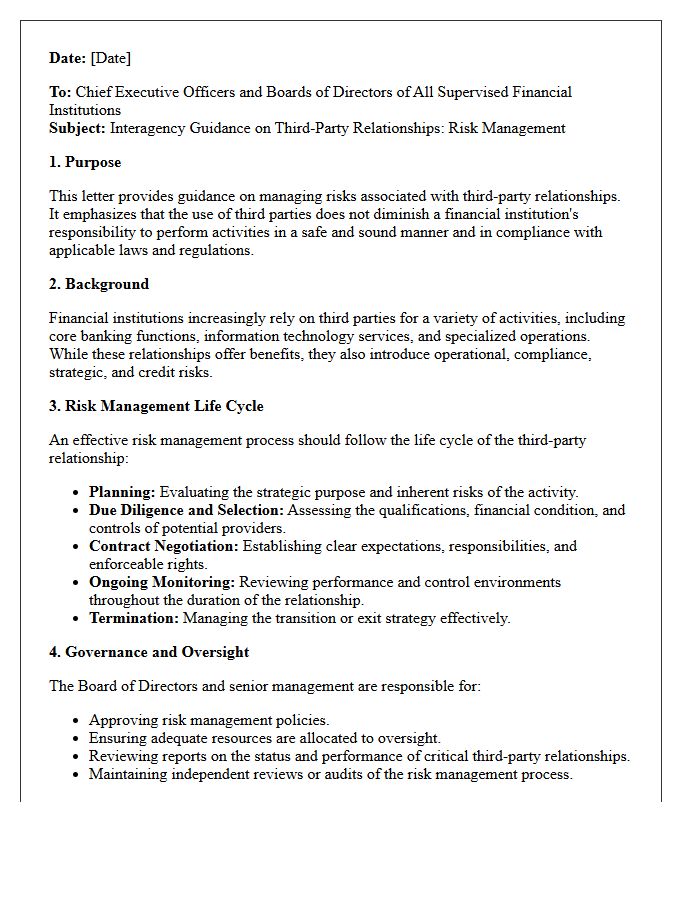

Interagency Supervisory Guidance Letter on Third-Party Relationship Risk

The Interagency Guidance on Third-Party Relationships establishes a unified framework for banking organizations to manage risks associated with external partnerships. It emphasizes that using vendors does not remove a bank's responsibility to operate safely and soundly. Financial institutions must implement a tailored risk management life cycle, including rigorous due diligence, continuous monitoring, and clear contract negotiations. This guidance ensures that activities performed by third parties, such as fintech collaborations or traditional outsourcing, comply with applicable laws and maintain operational resilience throughout the entire business relationship.

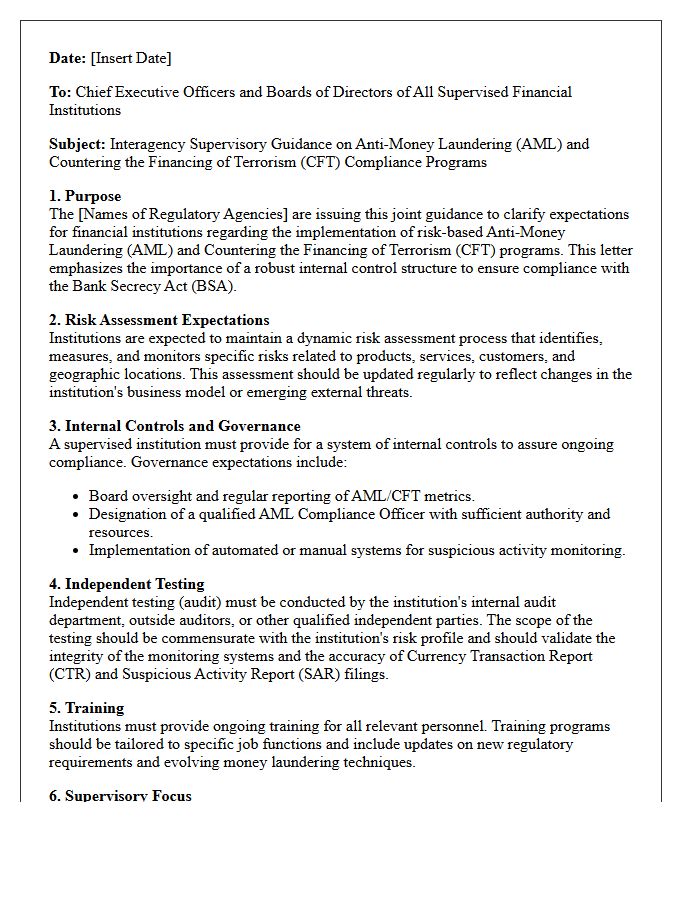

Interagency Supervisory Guidance Letter Regarding Anti-Money Laundering Compliance

The Interagency Statement clarifies how regulators evaluate bank compliance with BSA/AML requirements. It emphasizes that minor, isolated technical failures do not automatically trigger formal enforcement actions. Instead, examiners focus on whether an institution maintains a functional compliance program with adequate board oversight and internal controls. This guidance helps financial institutions distinguish between corrective action recommendations and cease and desist orders, ensuring that regulatory responses are proportional to the severity of the deficiency while prioritizing the detection of illicit financial activities and money laundering risks.

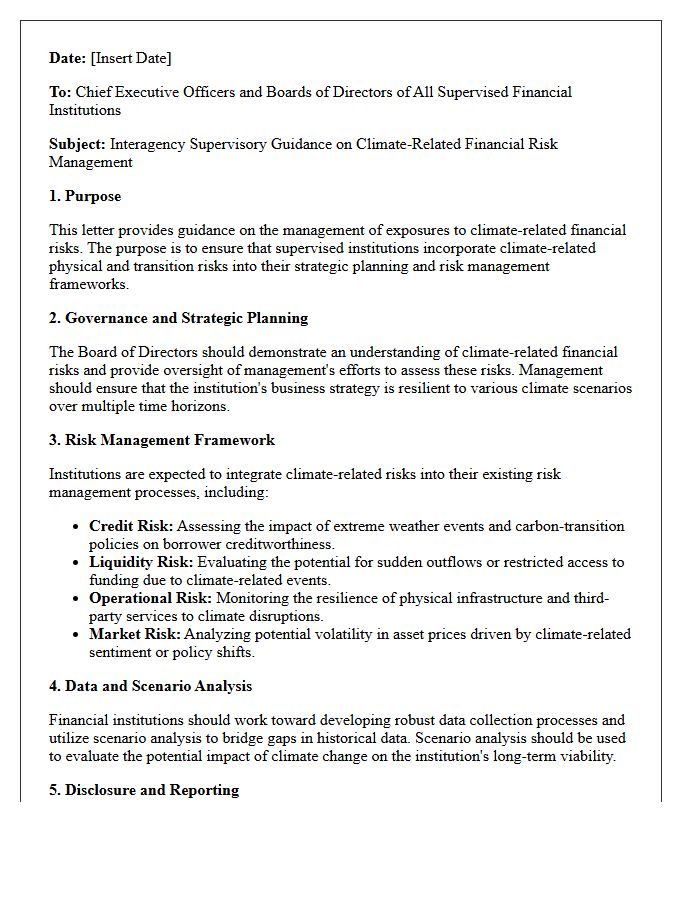

Interagency Supervisory Guidance Letter on Climate-Related Financial Risk Management

The Interagency Supervisory Guidance establishes a framework for large financial institutions to manage climate-related financial risks. It emphasizes that physical and transition risks can impact safety and soundness through credit, market, and operational channels. Boards of directors must ensure risk management practices integrate climate considerations into strategic planning and internal controls. By promoting consistent data collection and scenario analysis, the guidance helps banks identify vulnerabilities while ensuring financial stability. This regulatory oversight ensures institutions remain resilient as climate-driven economic shifts evolve, maintaining the integrity of the broader financial system through proactive governance.

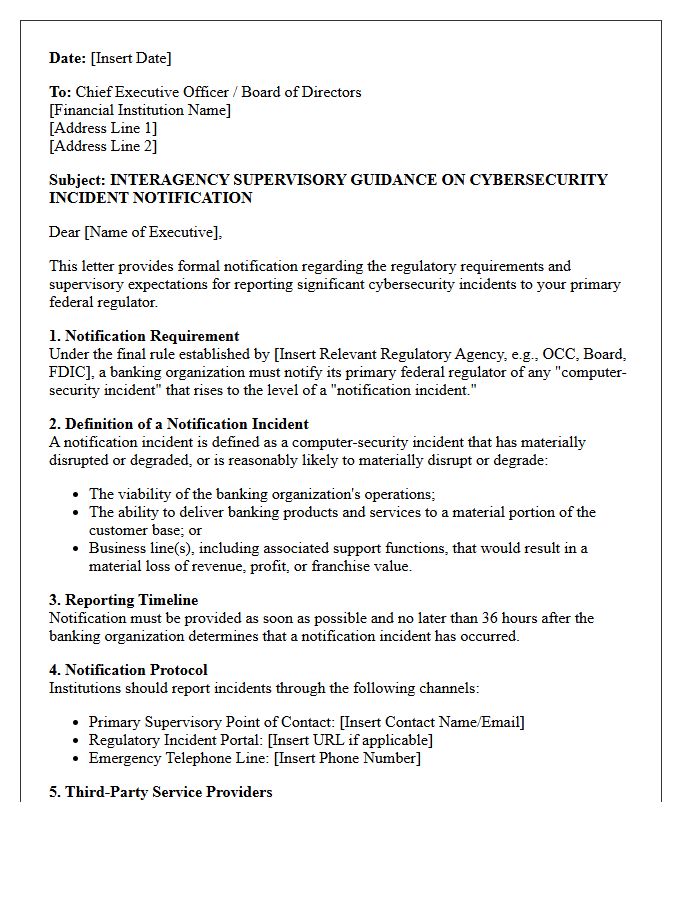

Interagency Supervisory Guidance Letter Addressing Cybersecurity Incident Notification

The Interagency Supervisory Guidance Letter mandates that banking organizations provide a cybersecurity incident notification within 36 hours of determining a significant disruption occurred. This rule aims to enhance early awareness of threats, allowing federal agencies to assess systemic risks across the financial sector. Regulated entities must report incidents that materially affect their viability, operations, or customer base. Compliance ensures regulatory transparency and helps coordinate rapid responses to large-scale cyberattacks, ultimately safeguarding the stability of the global financial infrastructure against evolving digital threats and vulnerabilities.

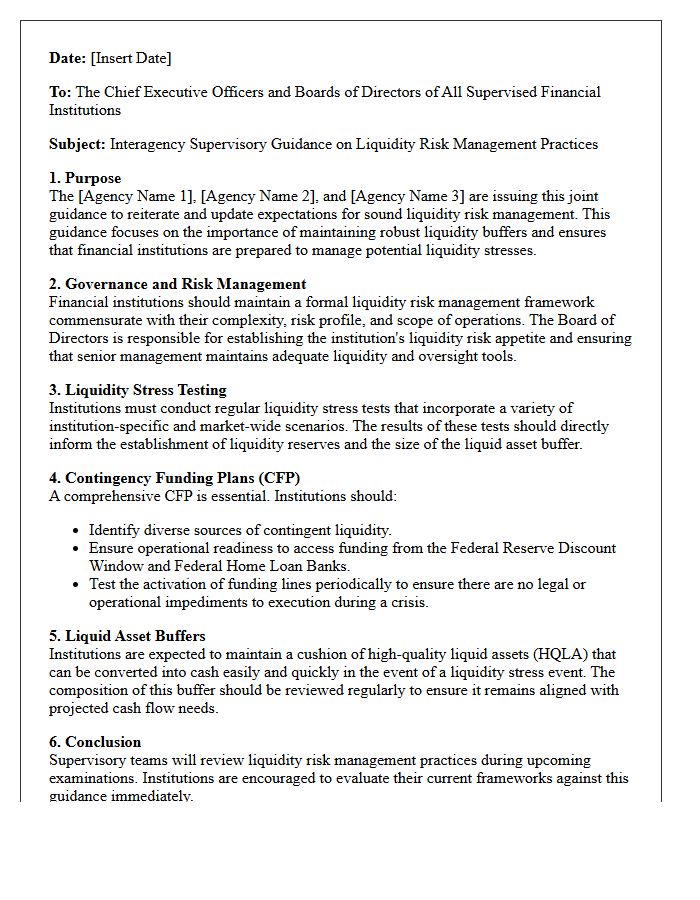

Interagency Supervisory Guidance Letter on Liquidity Risk Management Practices

The Interagency Supervisory Guidance Letter outlines critical expectations for robust liquidity risk management within financial institutions. It emphasizes that banks must maintain sufficient liquidity buffers and diverse funding sources to survive severe stress scenarios. Key requirements include implementing comprehensive cash flow forecasting, establishing formal contingency funding plans, and conducting regular liquidity stress tests. Supervisors use this framework to evaluate whether a firm's risk appetite aligns with its operational complexity, ensuring institutional stability and broader financial market resilience during periods of economic volatility or sudden market disruptions.

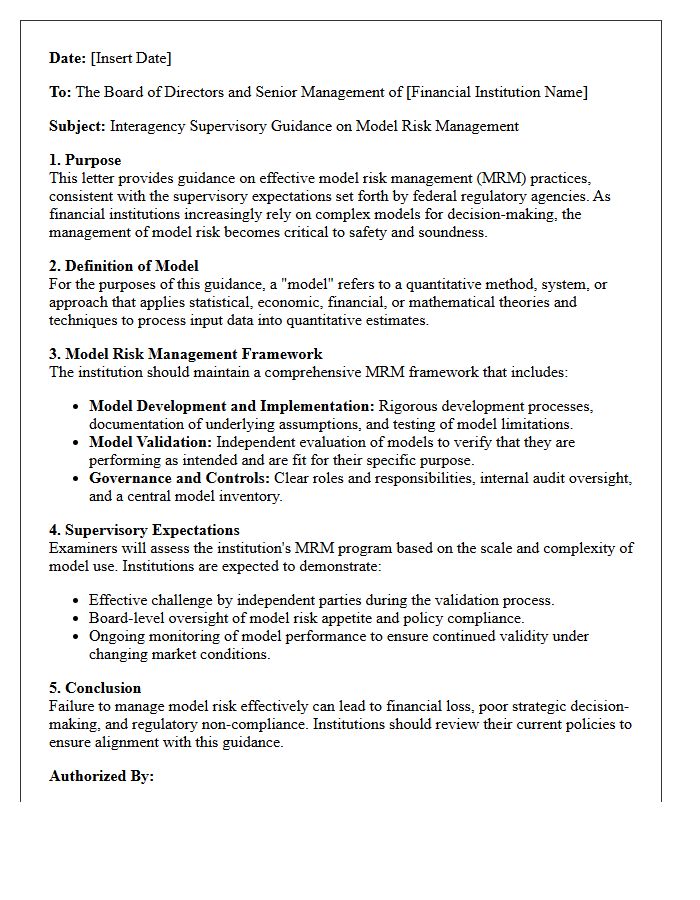

Interagency Supervisory Guidance Letter Concerning Model Risk Management

The Interagency Supervisory Guidance Letter Concerning Model Risk Management, often identified as SR 11-7, establishes critical standards for financial institutions. It emphasizes that models are essential tools but pose significant risks if misused or flawed. The guidance mandates a robust model risk management framework involving rigorous validation, sound development, and ongoing monitoring. Effective governance requires clear accountability and an independent review process to mitigate potential adverse consequences from decisions based on incorrect outputs. Adhering to these principles ensures financial stability and operational resilience across the banking sector.

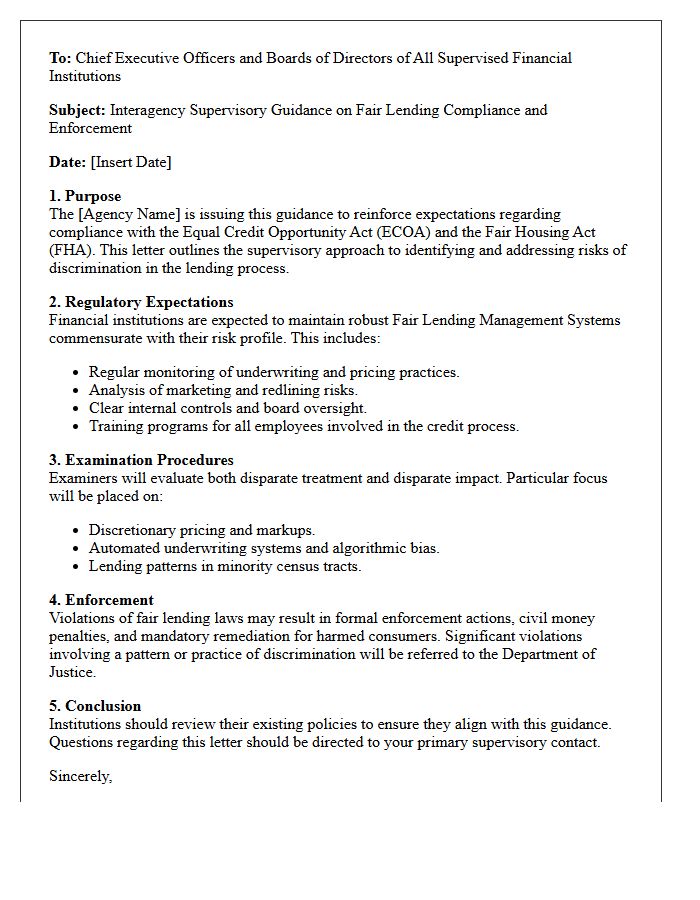

Interagency Supervisory Guidance Letter on Fair Lending Compliance and Enforcement

The Interagency Supervisory Guidance establishes a unified framework for federal agencies to monitor fair lending compliance. It outlines the examination procedures used to detect potential discrimination under the Equal Credit Opportunity Act and Fair Housing Act. Financial institutions must maintain robust compliance management systems to mitigate risk related to underwriting, pricing, and redlining. This guidance ensures that regulators apply consistent standards during enforcement actions, emphasizing that equitable access to credit is a fundamental requirement for all supervised lenders in the modern financial marketplace.

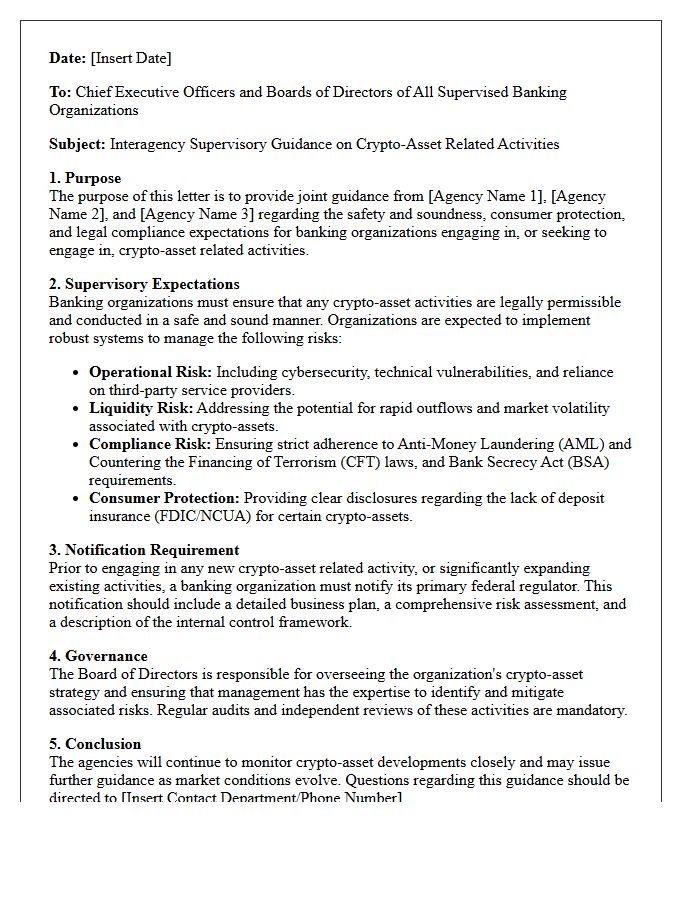

Interagency Supervisory Guidance Letter Regarding Crypto-Asset Related Activities

The Interagency Supervisory Guidance establishes rigorous expectations for banking organizations engaging in crypto-asset activities. It emphasizes that institutions must notify their primary federal regulator before commencing any crypto-related services. Banks are required to demonstrate safe and sound practices, ensuring adequate controls for liquidity, operational resilience, and consumer protection. This guidance ensures that digital asset integration does not compromise the stability of the broader financial system by mandating comprehensive risk assessments and legal compliance prior to participation in the evolving crypto marketplace.

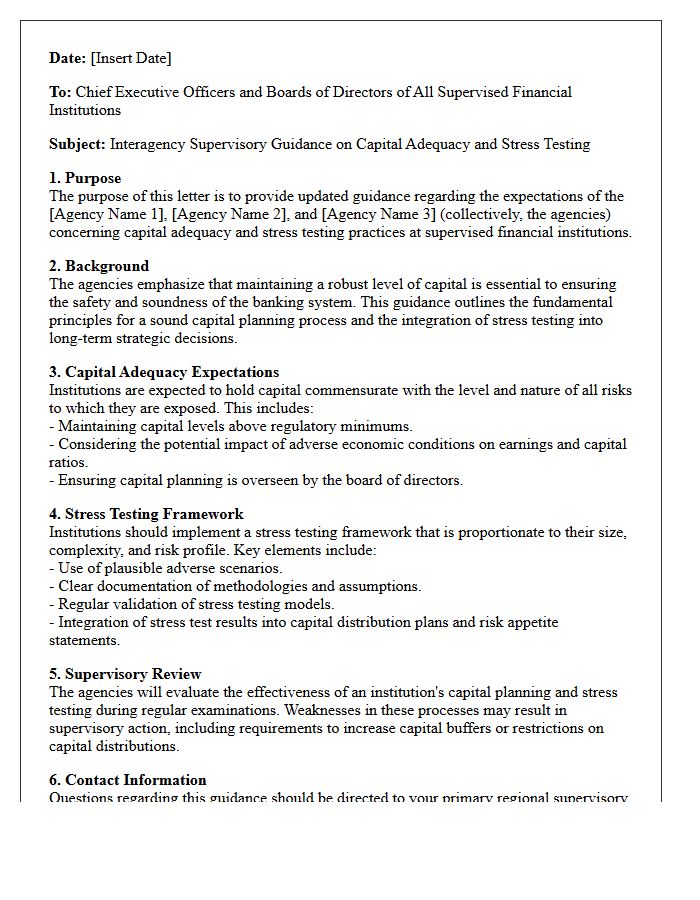

Interagency Supervisory Guidance Letter on Capital Adequacy and Stress Testing

The Interagency Supervisory Guidance Letter emphasizes that robust capital adequacy is fundamental to a bank's safety and soundness. It mandates that banking organizations integrate stress testing into their broader risk management frameworks to ensure they hold sufficient capital against potential economic downturns. This guidance directs boards of directors to maintain capital levels commensurate with their specific risk profiles, rather than relying solely on minimum regulatory ratios. Effective processes must include rigorous scenario analysis, internal controls, and forward-looking assessments to absorb losses and support continued lending during financial stress.

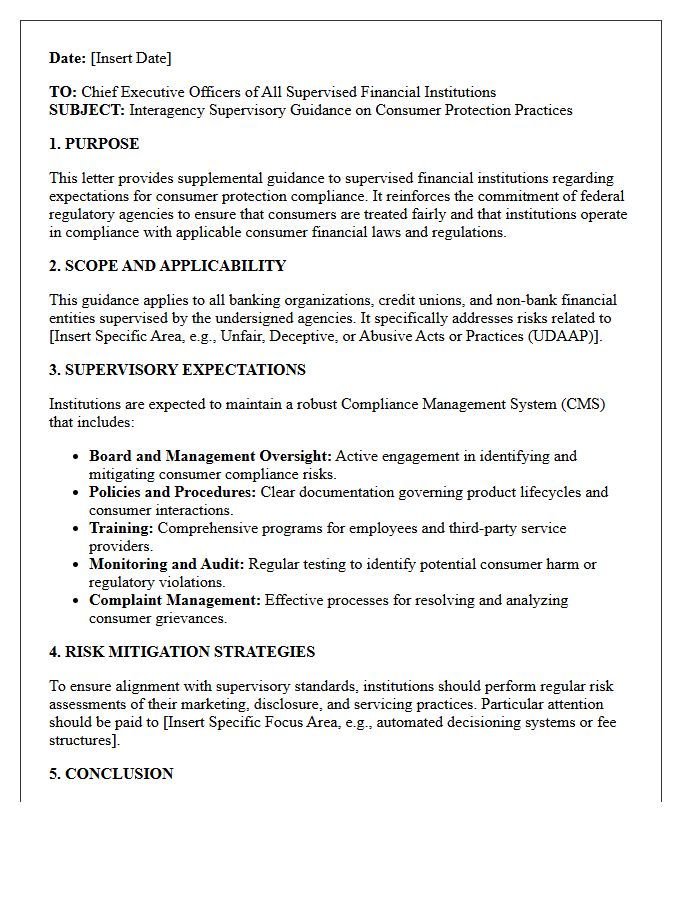

Interagency Supervisory Guidance Letter Addressing Consumer Protection Practices

The Interagency Supervisory Guidance Letter establishes crucial standards for consumer protection within financial institutions. It emphasizes that banks must maintain robust management systems to prevent unfair, deceptive, or abusive practices. This guidance ensures that compliance programs align with federal laws to mitigate reputational and legal risks. By prioritizing transparency and fair treatment, the letter mandates that institutions proactively monitor internal controls and third-party relationships. Understanding these expectations is vital for ensuring regulatory adherence and safeguarding the financial interests of all customers in a competitive marketplace.

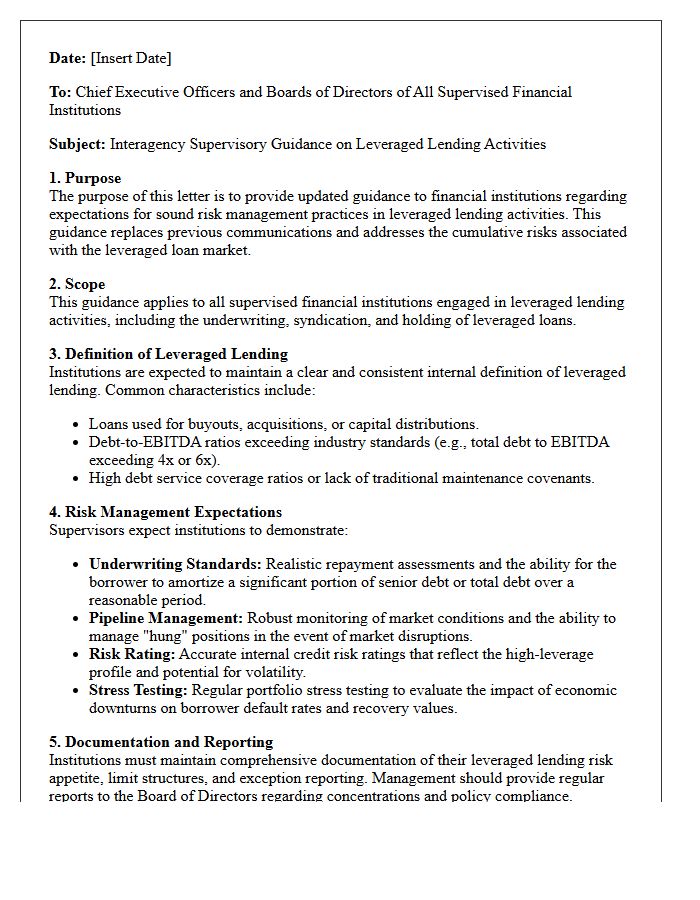

Interagency Supervisory Guidance Letter on Leveraged Lending Activities

The Interagency Supervisory Guidance on Leveraged Lending Activities establishes critical risk management expectations for financial institutions. It emphasizes that sound underwriting standards must prevent excessive leverage, typically defined as debt exceeding six times EBITDA. Regulators monitor enterprise value assessments and repayment capacity to ensure loans can be amortized within a reasonable timeframe. This guidance aims to mitigate systemic risk by ensuring banks maintain robust internal controls and stress testing frameworks when engaging with highly indebted borrowers, thereby promoting overall financial stability across the banking sector.

What is the purpose of the Interagency Supervisory Guidance Letter?

The Interagency Supervisory Guidance Letter is designed to provide financial institutions with unified instructions from multiple regulatory bodies, ensuring consistent application of laws and oversight standards across the banking industry.

Which regulatory bodies typically issue Interagency Supervisory Guidance?

These letters are commonly issued jointly by the Federal Reserve Board (FRB), the Federal Deposit Insurance Corporation (FDIC), and the Office of the Comptroller of the Currency (OCC).

Is the Interagency Supervisory Guidance Letter legally binding?

No, supervisory guidance does not have the force and effect of law. It is intended to outline expectations and provide clarity on how agencies intend to evaluate compliance with existing statutes and regulations.

How should financial institutions implement the recommendations in these letters?

Institutions should incorporate the guidance into their internal risk management frameworks, compliance programs, and audit processes to align their operations with regulatory expectations.

Where can I find the latest Interagency Supervisory Guidance Letters?

The latest letters are published on the official websites of the respective regulatory agencies, such as the OCC's newsroom, the FDIC's Financial Institution Letters (FILs) page, and the Federal Reserve's supervision and regulation section.

Comments