A Mortgage Servicing Standards Compliance Letter is a formal document used to verify that loan administration adheres to legal and regulatory requirements. It ensures transparency between lenders and borrowers while meeting CFPB guidelines. Proper documentation mitigates legal risks and confirms operational integrity during audits. To assist your professional outreach, below are some ready to use templates.

Image cover: Essential Guide to Mortgage Servicing Compliance: Letter Templates and Standards Compliance Tools

Letter Samples List

- Notice of Servicing Transfer Compliance Letter

- Annual Escrow Account Disclosure Letter

- Force-Placed Insurance Notification Letter

- Loss Mitigation Application Acknowledgment Letter

- Notice of Error Resolution Compliance Letter

- Qualified Written Request Response Letter

- Early Intervention Delinquency Notice Letter

- Loan Modification Approval Compliance Letter

- Fair Debt Collection Practices Act Compliance Letter

- Servicemembers Civil Relief Act Eligibility Letter

- Mortgage Payoff Statement Compliance Letter

- Successor in Interest Verification Letter

- Pre-Foreclosure Review Compliance Letter

- Internal Servicing Standards Audit Letter

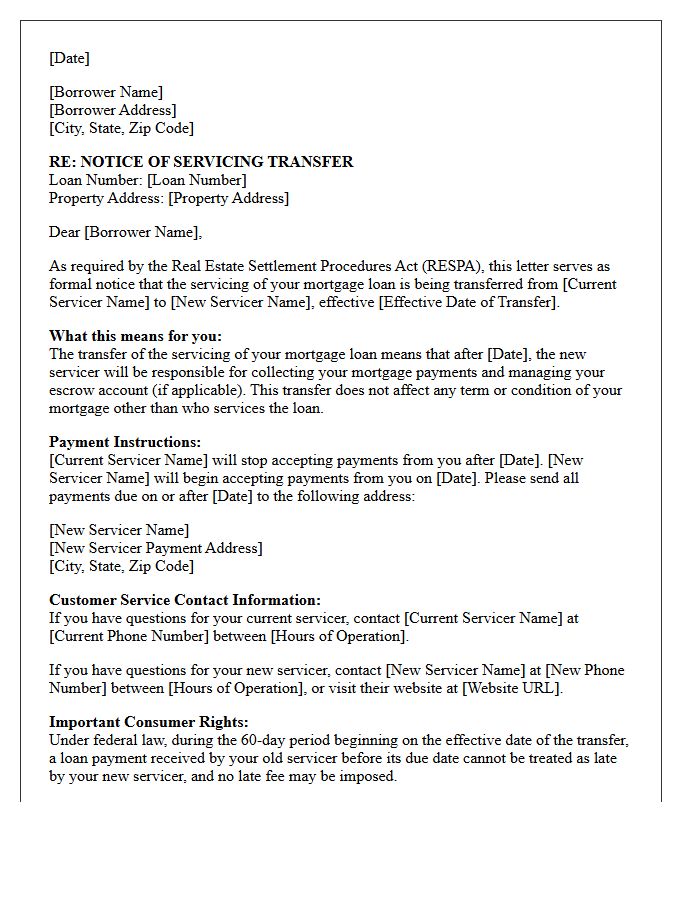

Notice of Servicing Transfer Compliance Letter

A Notice of Servicing Transfer is a mandatory legal document informing homeowners that their mortgage loan management is moving to a new provider. To ensure RESPA compliance, your current servicer must send this letter at least 15 days before the change. It contains the effective transfer date, contact details for the new entity, and payment instructions. Importantly, there is a 60-day grace period during which you cannot be penalized for sending payments to the previous servicer, protecting you from late fees while you update your records.

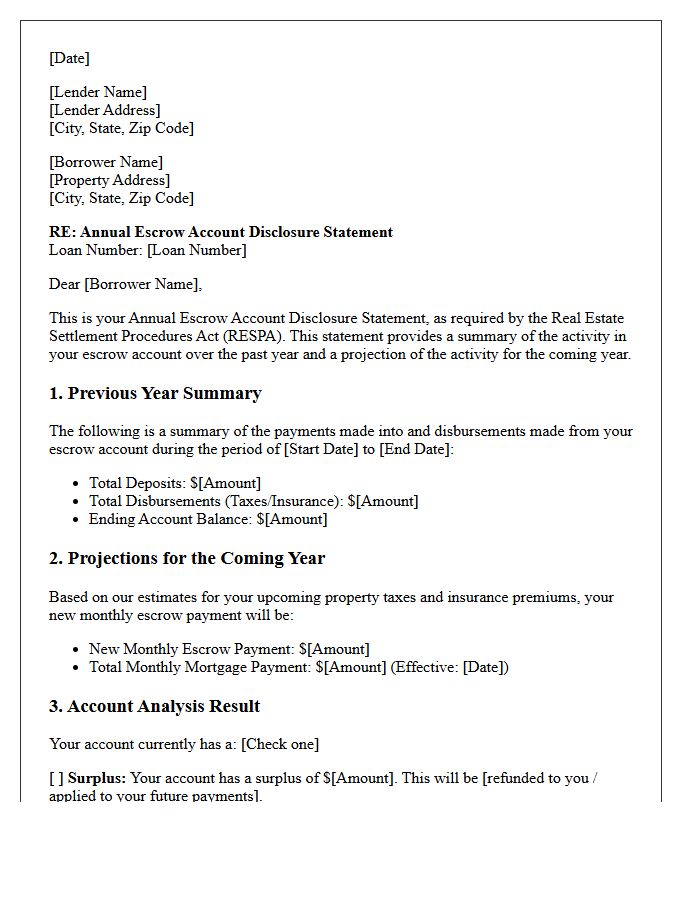

Annual Escrow Account Disclosure Letter

An Annual Escrow Account Disclosure Statement is a mandatory financial summary provided by your mortgage servicer. It tracks your escrow account activity over the past year and forecasts future payments for property taxes and homeowners insurance. This document is essential because it determines if you have a surplus, which may be refunded, or a shortage, which typically increases your monthly mortgage payment. Reviewing this letter helps you understand fluctuations in your total housing costs and ensures your lender is maintaining an adequate cushion to cover essential obligations.

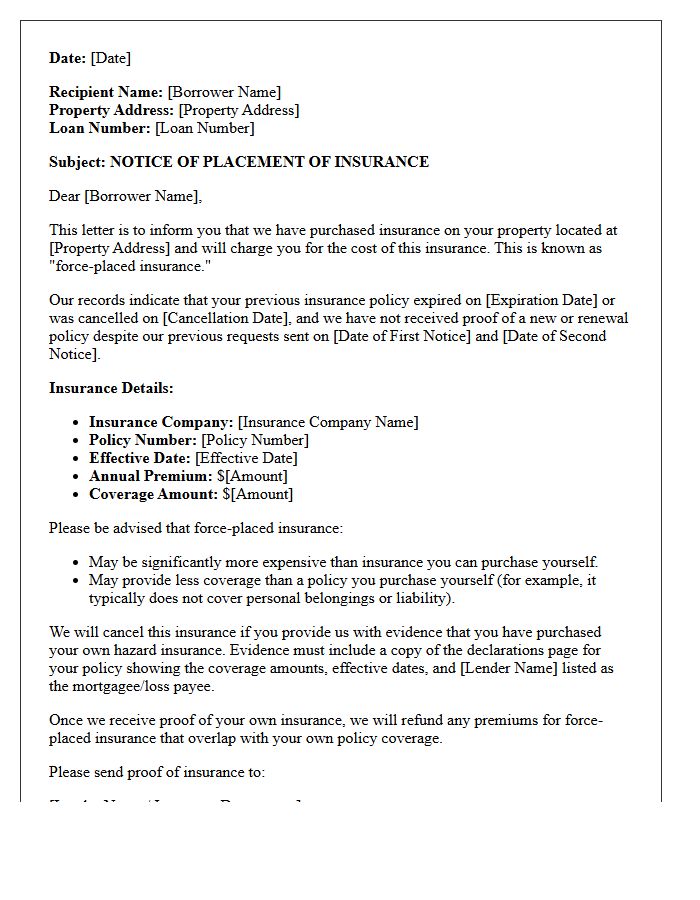

Force-Placed Insurance Notification Letter

A Force-Placed Insurance Notification Letter is a formal notice from your mortgage lender stating they intend to purchase coverage for your property because your own policy has lapsed or is insufficient. You must provide proof of insurance immediately to avoid this, as lender-placed policies are significantly more expensive and typically only protect the lender's financial interest, not your personal belongings. Federal law requires lenders to send two notices before charging you, giving you a 45-day window to reinstate your private coverage and prevent costly premium additions to your monthly mortgage payment.

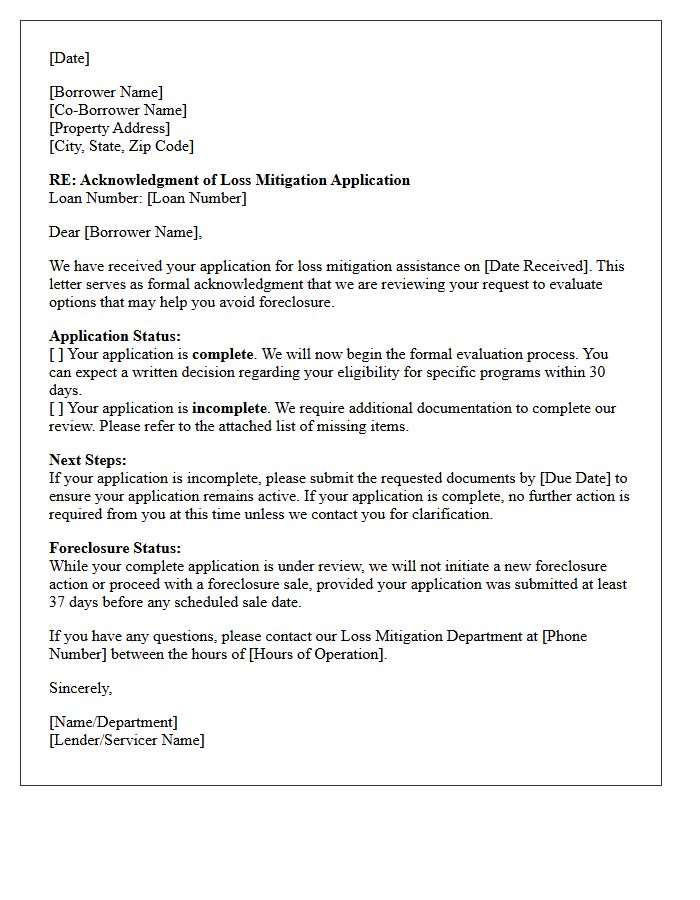

Loss Mitigation Application Acknowledgment Letter

A Loss Mitigation Application Acknowledgment Letter is a formal notice sent by mortgage servicers within five business days of receiving your request for foreclosure alternatives. This document confirms receipt and highlights whether your application is complete or requires additional documentation. Reviewing this letter promptly is critical because it outlines specific timelines and missing information needed to evaluate you for options like loan modifications. Providing a full package ensures your legal protections against dual tracking, effectively pausing the foreclosure process while your lender reviews your financial situation for a resolution.

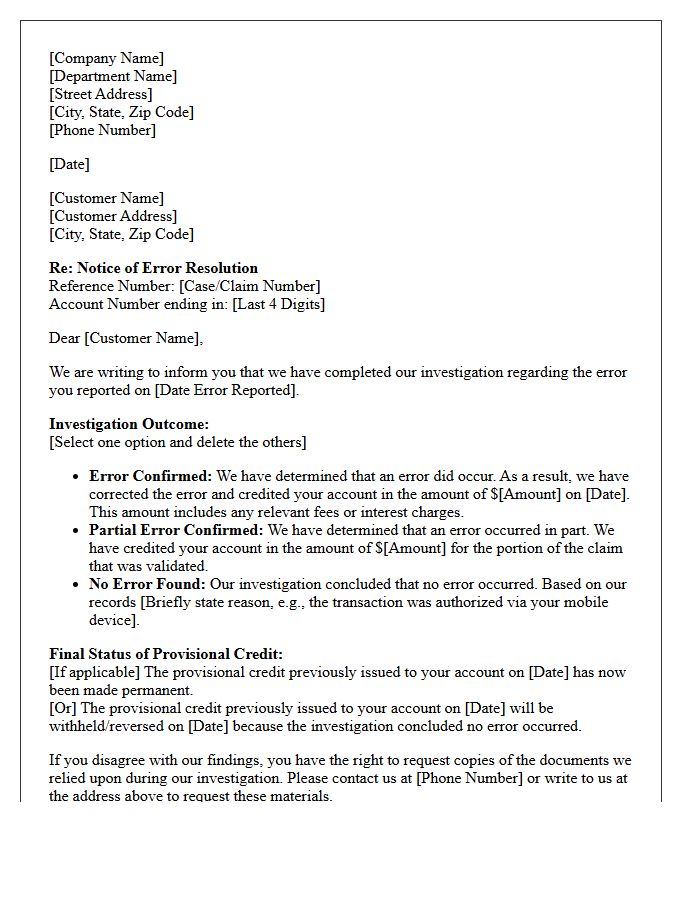

Notice of Error Resolution Compliance Letter

A Notice of Error Resolution Compliance Letter is a formal document issued by financial institutions to confirm the outcome of an investigation into reported billing or account discrepancies. Under the Electronic Fund Transfer Act and Regulation E, banks must notify consumers in writing whether a reported error was corrected or denied. This letter serves as legal proof that the entity adhered to federal timelines and consumer protection standards. Reviewing this document is essential for verifying account accuracy and understanding your rights regarding dispute resolution and final adjustments to your balance.

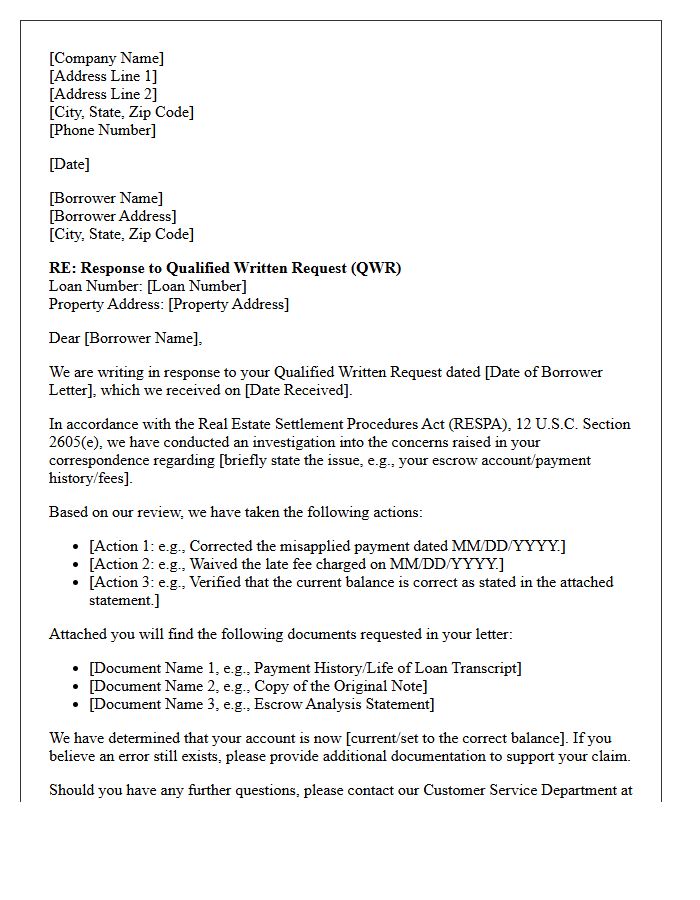

Qualified Written Request Response Letter

A Qualified Written Request (QWR) Response Letter is a formal communication sent by a mortgage servicer under RESPA guidelines. This document serves as an official reply to a homeowner's inquiry regarding account errors or information requests. It is essential to verify that the servicer has corrected billing discrepancies or provided necessary loan history documentation. Borrowers should review the response carefully to ensure all specific concerns were addressed within the legal 30-day timeframe, as this letter provides critical legal evidence for protecting consumer rights and resolving mortgage disputes effectively.

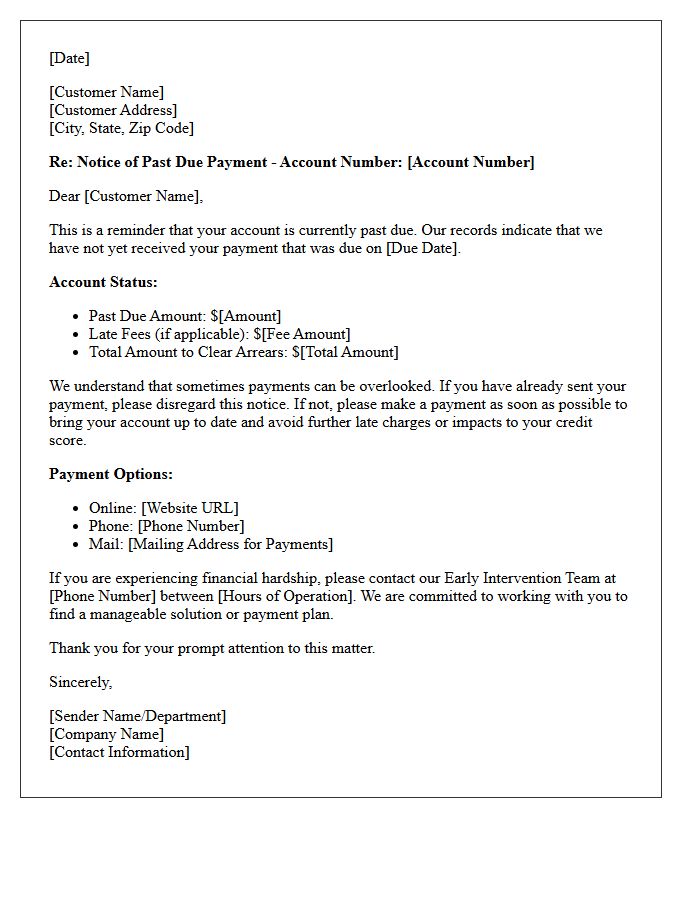

Early Intervention Delinquency Notice Letter

An Early Intervention Delinquency Notice Letter is a critical communication sent by mortgage servicers when a borrower misses a payment. Required by federal law, it typically arrives by the 45th day of delinquency. This document outlines loss mitigation options, such as loan modifications or forbearance, to help homeowners avoid foreclosure. It provides a designated contact person to assist with recovery. Timely response is vital to protecting your credit and maintaining homeownership stability through proactive repayment solutions and professional guidance.

Loan Modification Approval Compliance Letter

A Loan Modification Approval Compliance Letter is a legal document confirming that a mortgage adjustment adheres to federal and state lending regulations. This notice ensures the modified terms, such as interest rates and monthly payments, meet Consumer Financial Protection Bureau standards. Borrowers must review this letter to verify the legality of their new agreement and protect against predatory practices. It serves as official proof that the lender has fulfilled its regulatory obligations, providing transparency and security for homeowners seeking long-term financial stability through a restructured debt plan.

Fair Debt Collection Practices Act Compliance Letter

A Fair Debt Collection Practices Act (FDCPA) Compliance Letter is a formal document used to exercise your legal rights against third-party collectors. It serves as a debt validation request, forcing the agency to provide proof of the alleged balance. Sending this letter within thirty days of initial contact legally halts collection efforts until verification is provided. This consumer protection tool prevents harassment, ensures accurate reporting, and creates a paper trail to hold agencies accountable for potential violations under federal law.

Servicemembers Civil Relief Act Eligibility Letter

A Servicemembers Civil Relief Act (SCRA) Eligibility Letter serves as official verification of an individual's active duty status. This document is essential for service members to exercise their legal protections, such as interest rate caps, eviction stays, and contract terminations. Lenders and service providers require this letter to confirm military service dates before applying federal benefits. Typically obtained through the Defense Manpower Data Center (DMDC), it ensures that personnel can focus on their mission without facing undue financial or legal burdens while serving on active duty or qualifying reserve orders.

Mortgage Payoff Statement Compliance Letter

A Mortgage Payoff Statement Compliance Letter is a formal document confirming that a loan has been fully satisfied according to legal and regulatory standards. It serves as official proof that the borrower has met all financial obligations, ensuring the lien release is processed correctly with local authorities. This document protects homeowners by verifying the debt is legally cleared, preventing future title disputes. It is essential for verifying compliance with state lending laws and confirming the lender has received the final payment in full to close the account permanently.

Successor in Interest Verification Letter

A Successor in Interest Verification Letter is a formal document used to confirm legal ownership of a property following the death or transfer from the original borrower. To assume loan management, you must provide supporting documentation, such as a death certificate or legal deed. This process allows heirs or transferees to receive mortgage information and explore loss mitigation options. Once verified, the successor gains the same legal rights as the previous owner, ensuring a smooth transition of the mortgage obligations while preventing foreclosure during the review period.

Pre-Foreclosure Review Compliance Letter

A Pre-Foreclosure Review Compliance Letter is a mandatory legal notice sent by mortgage servicers to borrowers before initiating legal action. It serves as a final warning, confirming that the lender has fulfilled state and federal loss mitigation requirements. This document details the total amount past due and provides options for foreclosure prevention. Receiving this letter is critical because it marks the end of the initial grace period, signifying that the foreclosure process will officially begin if the default is not cured or a workout plan is not established immediately.

Internal Servicing Standards Audit Letter

An Internal Servicing Standards Audit Letter is a critical regulatory document used to evaluate a financial institution's compliance with operational benchmarks. It assesses whether internal workflows meet legal obligations and consumer protection mandates. This audit verifies the accuracy of account management, payment processing, and disclosure timelines. For stakeholders, receiving this letter signifies a formal review of risk management protocols. Ensuring these standards are met is vital for maintaining regulatory transparency, mitigating potential penalties, and upholding the integrity of loan servicing operations within the financial sector.

What is a Mortgage Servicing Standards Compliance Letter?

A Mortgage Servicing Standards Compliance Letter is a formal document certifying that a loan servicer is adhering to federal and state regulations, such as those mandated by the CFPB, regarding the management and administration of mortgage loans.

What information is typically included in a compliance certification letter?

The letter typically includes confirmation of adherence to escrow management rules, error resolution procedures, loss mitigation protocols, and verification that periodic statements are being issued in accordance with Truth in Lending Act (TILA) requirements.

Why do investors require a Mortgage Servicing Standards Compliance Letter?

Investors and regulatory bodies require this letter to mitigate risk, ensuring that the entity servicing the mortgage is following the Real Estate Settlement Procedures Act (RESPA) and avoiding legal liabilities associated with improper loan handling.

How often should a mortgage servicer issue a compliance audit letter?

While specific timelines vary by jurisdiction and investor agreement, most servicing standards require an annual independent compliance audit and a subsequent certification letter to maintain standing with GSEs like Fannie Mae or Freddie Mac.

What are the consequences of failing to meet mortgage servicing compliance standards?

Failure to comply with servicing standards can result in significant civil penalties from the CFPB, loss of servicing rights, legal action from borrowers, and mandatory corrective action plans to rectify systemic operational failures.

Comments