The Federal Deposit Insurance Corporation recently issued the Uninsured Deposit Reporting Guidance Letter to ensure financial institutions accurately report deposit insurance coverage. This guidance clarifies data expectations and reporting standards to improve transparency and risk management across the banking sector. Understanding these regulatory updates is essential for compliance officers and financial reporting teams. Below are some ready to use template.

Image cover: Professional Templates and Regulatory Guidance for Uninsured Deposit Reporting

Letter Samples List

- Uninsured Deposit Reporting Guidance Letter

- Regulatory Compliance Letter for Uninsured Deposits

- Quarterly Uninsured Deposit Call Report Submission Letter

- Depositor Notification Letter for Uninsured Funds

- Internal Audit Findings Letter on Uninsured Deposit Reporting

- Uninsured Deposit Threshold Exceedance Warning Letter

- Bank Executive Certification Letter for Uninsured Deposits

- Uninsured Deposit Policy Revision Transmittal Letter

- Commercial Account Uninsured Deposit Acknowledgment Letter

- Uninsured Deposit Stress Testing Methodology Letter

- Supervisory Guidance Letter on Uninsured Deposit Volatility

- Year-End Uninsured Deposit Reconciliation Letter

- Liquidity Risk Management Letter for Uninsured Deposits

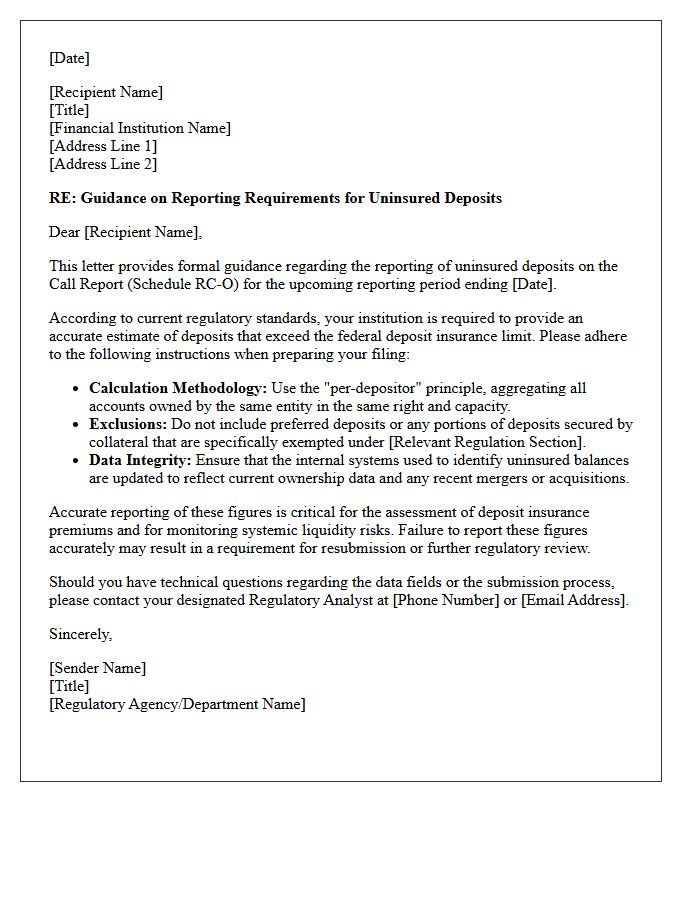

Uninsured Deposit Reporting Guidance Letter

The Uninsured Deposit Reporting Guidance Letter provides critical instructions for financial institutions to accurately calculate and report unprotected funds. It ensures transparency regarding deposits exceeding FDIC insurance limits, focusing on custodial accounts and complex ownership structures. Compliance is essential for regulatory oversight and assessing bank liquidity risks. Financial institutions must strictly follow these standardized reporting protocols to maintain systemic stability and ensure accurate data collection for federal insurance assessments.

Regulatory Compliance Letter for Uninsured Deposits

A Regulatory Compliance Letter for Uninsured Deposits serves as formal verification that a financial institution manages non-guaranteed funds according to strict legal mandates. This document outlines the collateralization strategies used to protect balances exceeding standard insurance limits, such as those provided by the FDIC. It ensures transparency regarding risk mitigation, reporting requirements, and liquidity standards. For institutional investors and corporate entities, obtaining this letter is essential to demonstrate fiduciary responsibility and verify that the bank maintains adequate security measures to safeguard large-scale capital against potential insolvency.

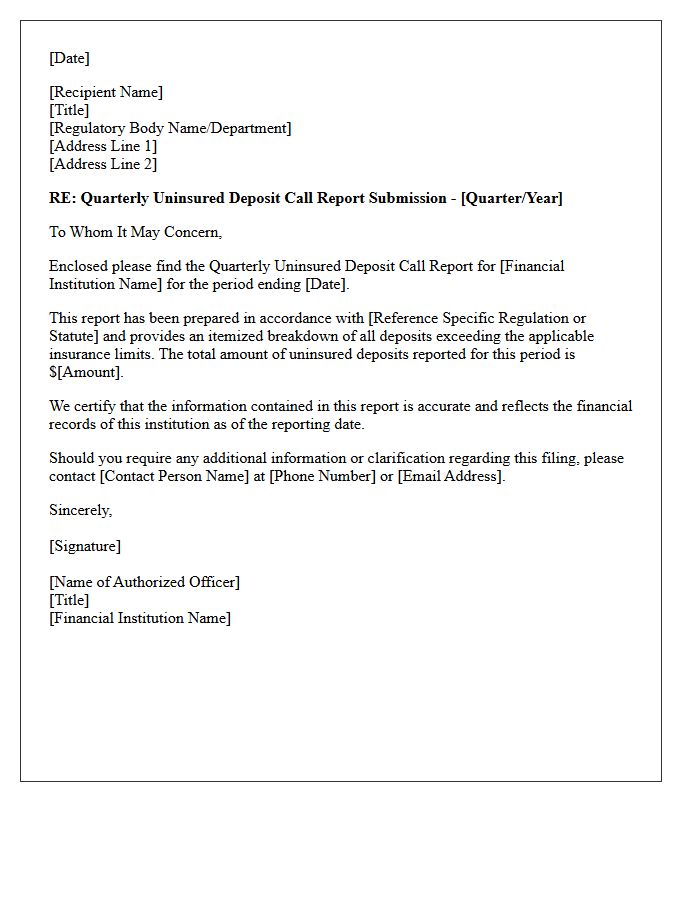

Quarterly Uninsured Deposit Call Report Submission Letter

The Quarterly Uninsured Deposit Call Report Submission Letter is a mandatory regulatory filing for FDIC-insured institutions. It requires banks to report the total value of uninsured deposits held at the end of each fiscal quarter. This data is critical for determining assessment rates and ensuring financial stability within the banking system. Institutions must ensure accurate reporting and timely electronic submission via the Central Data Repository (CDR). Failure to comply can lead to regulatory penalties and affects the calculation of the Deposit Insurance Fund (DIF) requirements.

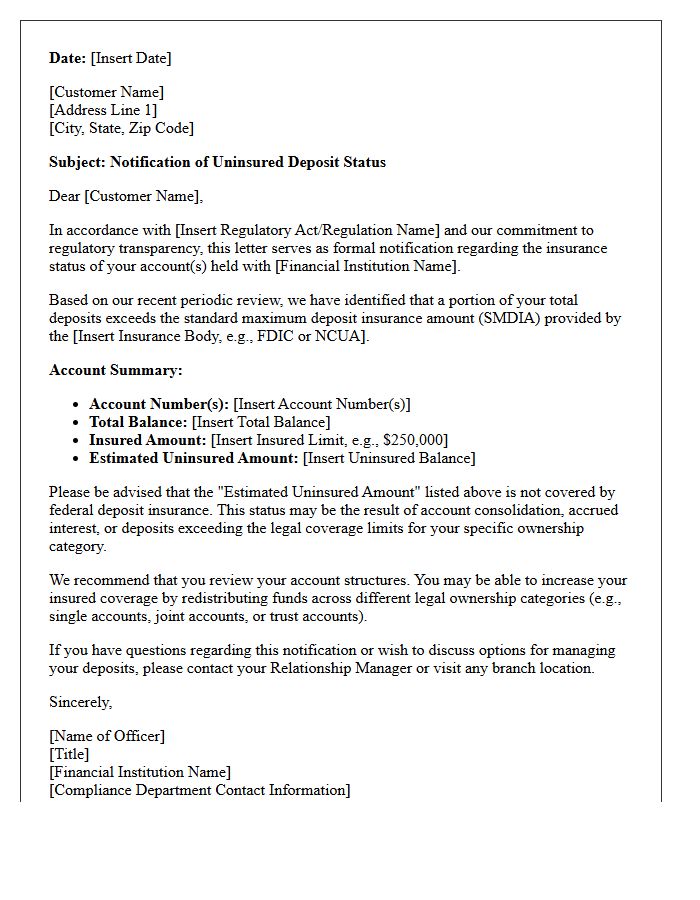

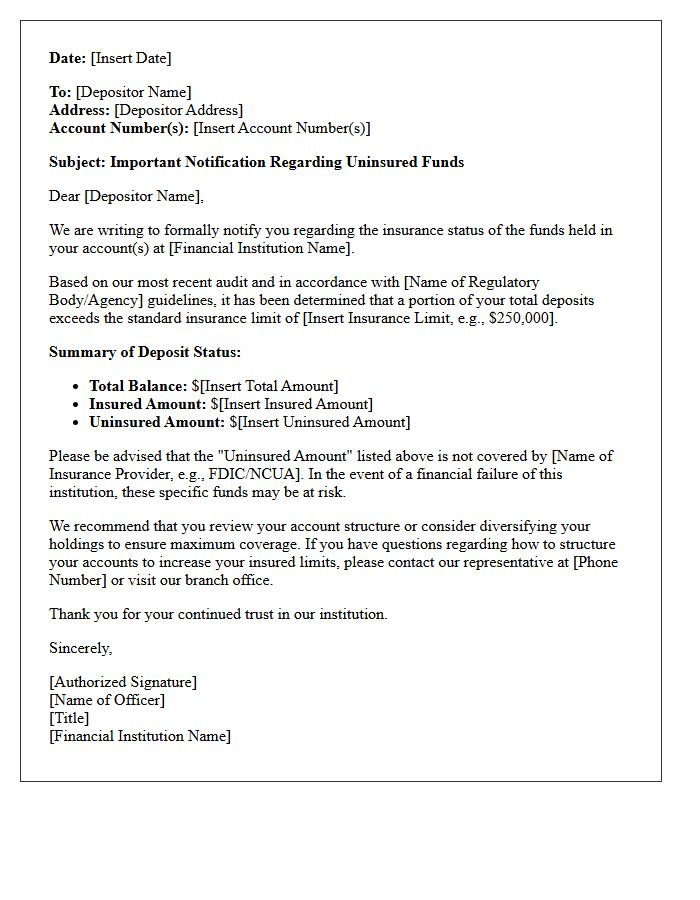

Depositor Notification Letter for Uninsured Funds

A Depositor Notification Letter is a formal notice issued by a financial institution to inform clients when their account balances exceed government insurance limits. It is a critical risk disclosure highlighting that uninsured funds are not protected by the FDIC or equivalent regulatory bodies in the event of a bank failure. Depositors must review these letters to assess their financial exposure and consider diversification strategies or specialized excess coverage products to safeguard their capital against potential loss. Maintaining awareness of insurance thresholds ensures proactive asset protection.

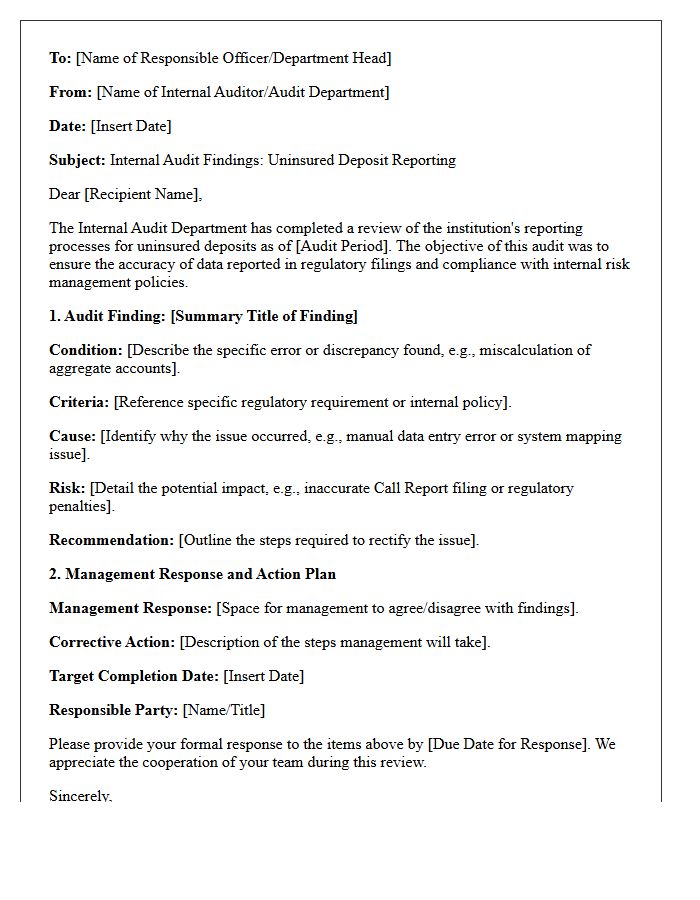

Internal Audit Findings Letter on Uninsured Deposit Reporting

An Internal Audit Findings Letter regarding uninsured deposit reporting identifies critical discrepancies in how financial institutions classify and report non-insured funds to regulators. It highlights remediation requirements for data accuracy, system calculation errors, and internal control weaknesses. Ensuring precise Part 360 compliance is vital to avoid regulatory penalties and maintain public trust. Management must address these audit deficiencies promptly to ensure that Call Reports and liquidity risk assessments reflect the institution's true risk profile, protecting both the bank and its stakeholders from unforeseen operational or financial liabilities.

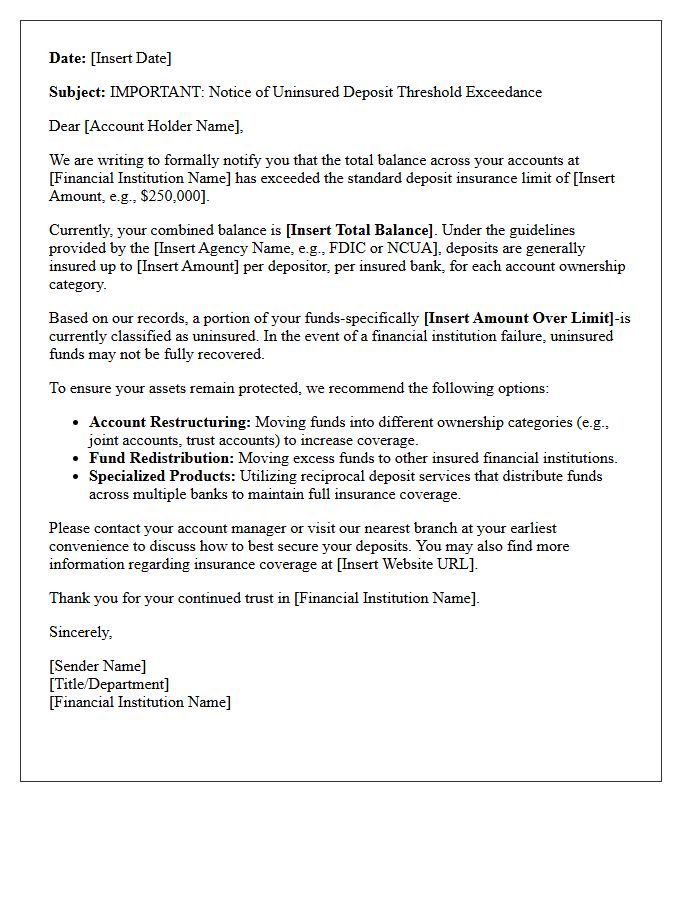

Uninsured Deposit Threshold Exceedance Warning Letter

An Uninsured Deposit Threshold Exceedance Warning Letter is a formal notification from a financial institution informing you that your account balance exceeds the standard FDIC or NCUA insurance limit, typically $250,000. This alert serves as a critical risk management tool, highlighting that funds above this ceiling are not government-guaranteed in the event of a bank failure. To protect your capital, consider diversifying assets across different institutions or utilizing specialized services like ICS to ensure full coverage and financial security for all your deposits.

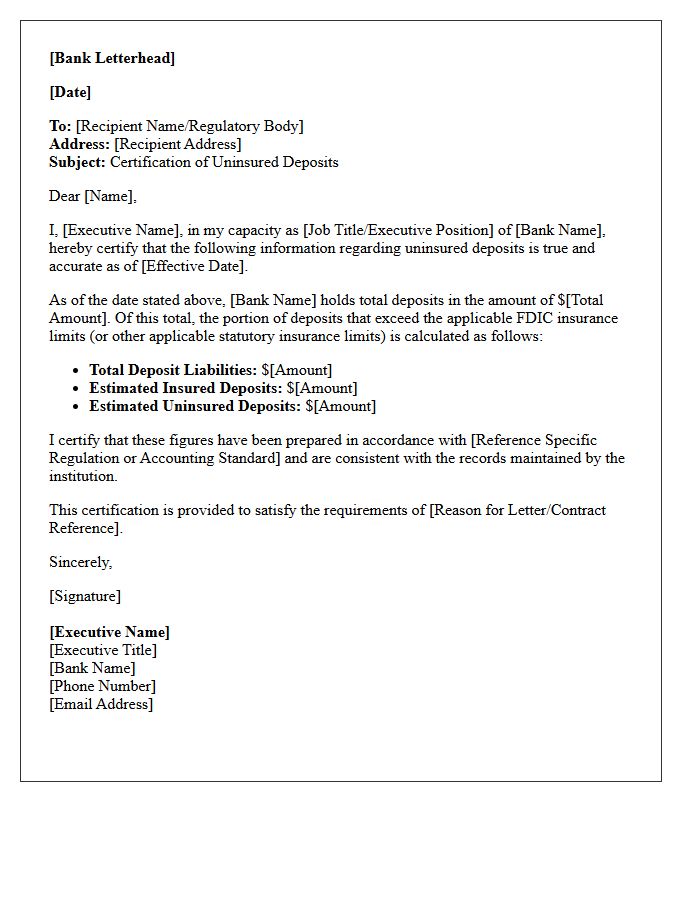

Bank Executive Certification Letter for Uninsured Deposits

A Bank Executive Certification Letter for uninsured deposits is a formal document verifying funds that exceed standard FDIC insurance limits. It serves as an official guarantee of account ownership and balance validity, often required during high-value corporate transactions or private placements. This letter confirms the institution's commitment to the depositor and provides necessary due diligence for third parties. It is essential for managing institutional risk and ensuring compliance in financial environments where traditional deposit insurance does not fully cover the total asset value held within the bank.

Uninsured Deposit Policy Revision Transmittal Letter

The Uninsured Deposit Policy Revision Transmittal Letter serves as an official communication detailing critical updates to how financial institutions manage non-guaranteed funds. It outlines regulatory adjustments regarding reporting requirements, risk mitigation strategies, and collateralization protocols for deposits exceeding statutory insurance limits. Understanding these revisions is essential for maintaining compliance and ensuring institutional liquidity. The letter clarifies the transition period for implementation, ensuring that banks align their internal controls with current oversight standards to protect the stability of the broader financial system and minimize potential exposure during periods of economic volatility.

Commercial Account Uninsured Deposit Acknowledgment Letter

A Commercial Account Uninsured Deposit Acknowledgment Letter is a formal notice used by financial institutions when a business deposit exceeds FDIC or NCUA insurance limits. This document ensures the depositor understands that funds surpassing the standard $250,000 threshold are not government-guaranteed. Signing this acknowledgment protects the bank by confirming the client is aware of the potential risk associated with excess liquidity. It is a vital compliance step for managing large corporate balances and maintaining transparent risk management protocols within commercial banking relationships.

Uninsured Deposit Stress Testing Methodology Letter

The Uninsured Deposit Stress Testing Methodology Letter provides critical guidance for financial institutions to evaluate liquidity risks. It outlines quantitative frameworks for simulating extreme outflow scenarios among non-guaranteed accounts. Banks must assess their contingency funding plans to ensure stability during market volatility or loss of depositor confidence. This methodology emphasizes the importance of liquidity stress testing to identify potential vulnerabilities in funding structures, helping regulators monitor systemic risk and institutional resilience against sudden capital flight.

Supervisory Guidance Letter on Uninsured Deposit Volatility

The Supervisory Guidance Letter addresses risks associated with uninsured deposit volatility, highlighting how rapid outflows can threaten bank liquidity. Regulators emphasize that contingency funding plans must account for the speed of modern digital withdrawals. Banks are encouraged to diversify funding sources and enhance monitoring of large, uninsured accounts. This guidance ensures financial institutions maintain adequate liquidity buffers to withstand sudden market shifts. Understanding these expectations is vital for effective risk management and maintaining stability during periods of economic uncertainty or heightened depositor sensitivity.

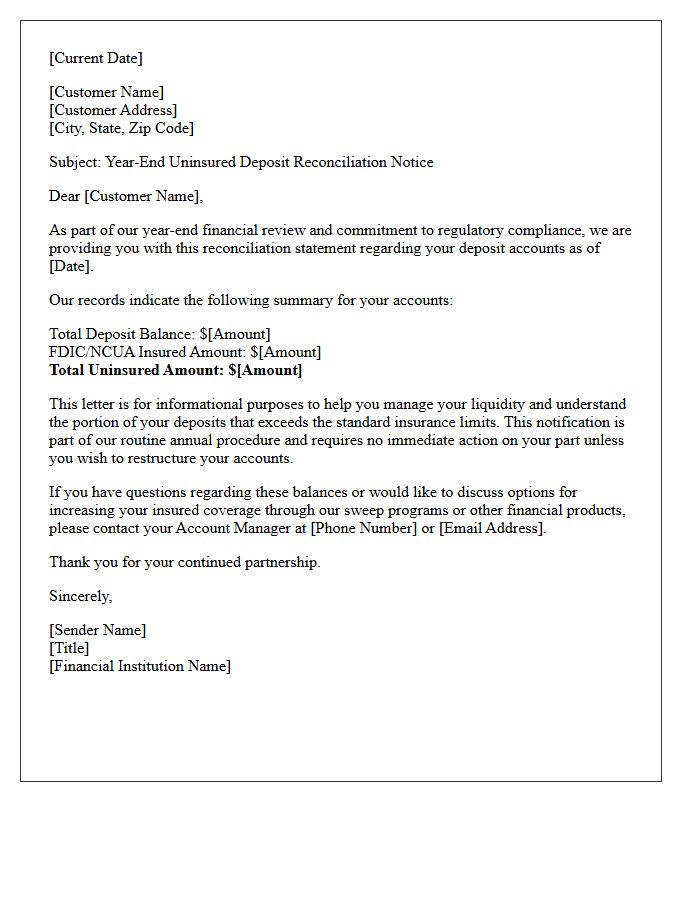

Year-End Uninsured Deposit Reconciliation Letter

The Year-End Uninsured Deposit Reconciliation Letter is a critical regulatory notification sent by financial institutions to clients holding deposits exceeding the standard FDIC insurance limit. This document confirms the specific amount of funds currently unprotected by federal coverage as of December 31st. It serves as an essential compliance tool for businesses and high-net-worth individuals to accurately assess liquidity risk, manage balance sheet transparency, and ensure proper fiduciary oversight for the upcoming fiscal year. Reviewing this statement helps depositors make informed decisions regarding fund diversification and asset security.

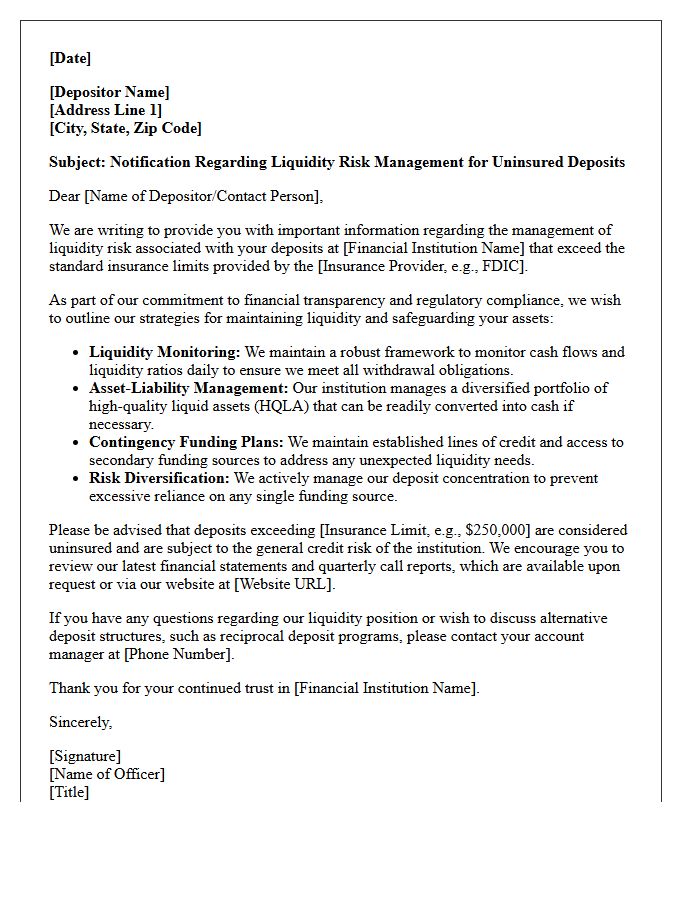

Liquidity Risk Management Letter for Uninsured Deposits

A Liquidity Risk Management Letter for uninsured deposits is a critical regulatory document ensuring financial stability. It outlines strategies to manage funding volatility associated with large, unprotected balances. Banks must maintain liquid assets sufficient to cover potential rapid outflows during market stress. Key components include stress testing, contingency funding plans, and detailed monitoring of concentration risks. Effective oversight prevents liquidity crunches, protecting the institution's solvency and maintaining depositor confidence. This proactive framework is essential for mitigating risks inherent in concentrated deposit bases that lack federal insurance coverage.

What is the purpose of the Uninsured Deposit Reporting Guidance Letter?

The guidance letter provides financial institutions with standardized instructions for identifying, calculating, and reporting the portion of deposits that exceed the federal deposit insurance limit to ensure accurate assessment of risk exposure.

Which financial institutions are required to comply with these reporting requirements?

This guidance applies to all insured depository institutions (IDIs) that are mandated to file quarterly Consolidated Reports of Condition and Income (Call Reports) and meet specific asset thresholds or risk profiles outlined by regulatory authorities.

How should institutions calculate the uninsured portion of a deposit account?

Institutions must calculate the uninsured amount by determining the total market value of the deposit balance and subtracting the maximum applicable insurance coverage-typically $250,000 per depositor, per ownership category-taking into account account aggregation rules.

What are the common exclusions when reporting uninsured deposits?

Common exclusions include preferred deposits, such as certain public fund deposits that are secured by pledged collateral, and specific interbank or intra-entity deposits as defined in the technical instructions of the guidance letter.

What are the consequences of inaccurate uninsured deposit reporting?

Inaccurate reporting can lead to incorrect risk-based premium assessments, regulatory enforcement actions, and a requirement to restate prior Call Report filings to reflect the corrected liability structure of the institution.

Comments