The Market Risk Capital Rule Letter serves as a critical communication tool for financial institutions to demonstrate regulatory compliance. This formal document outlines how banks calculate and manage risk exposure under current Basel standards to ensure financial stability. Navigating these complex reporting requirements is essential for maintaining capital adequacy. To assist your firm's compliance efforts, below are some ready to use template.

Image cover: Streamline Your Compliance: Market Risk Capital Rule Notification Templates

Letter Samples List

- Market Risk Capital Rule Compliance Certification Letter

- Internal Models Approach Approval Request Letter

- Trading Book Boundary Policy Implementation Letter

- Standardized Approach Capital Calculation Submission Letter

- Regulatory Market Risk Reporting Variance Letter

- Model Validation and Backtesting Results Letter

- Market Risk Capital Rule Audit Remediation Letter

- Value at Risk Model Exception Notification Letter

- Market Risk Capital Adequacy Assessment Letter

- Fundamental Review of the Trading Book Transition Letter

- Stress Testing and Capital Surcharge Acknowledgment Letter

- Market Risk Capital Rule Supervisory Response Letter

- Covered Position Portfolio Designation Letter

- Market Risk Capital Framework Board Approval Letter

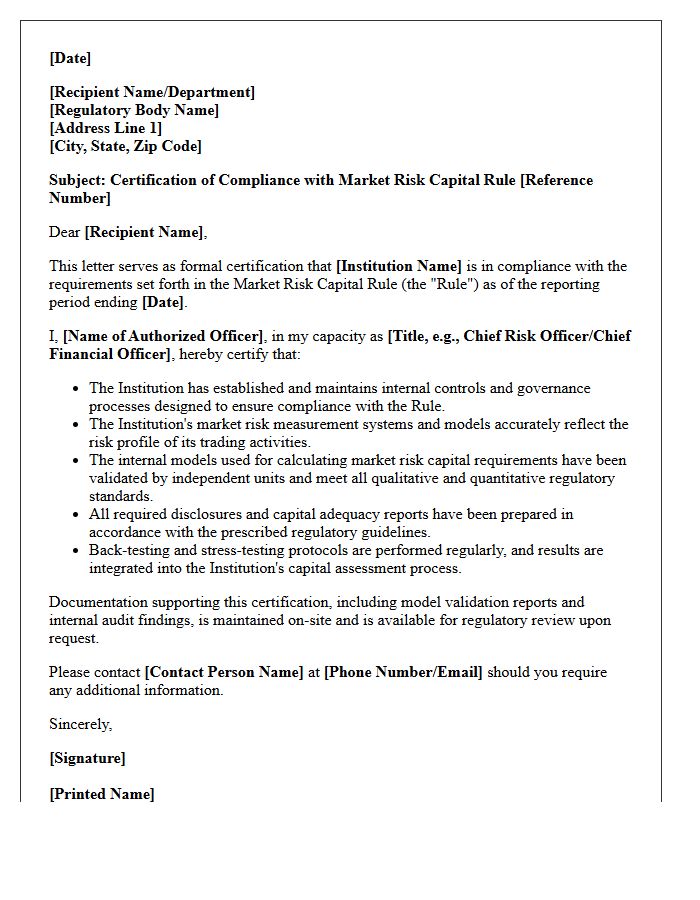

Market Risk Capital Rule Compliance Certification Letter

A Market Risk Capital Rule Compliance Certification Letter is a formal document submitted by financial institutions to regulators. It verifies that the firm's internal models and risk management frameworks strictly adhere to regulatory capital requirements. This letter confirms that the bank has conducted thorough backtesting and validation of its market risk processes. Ensuring accuracy in this certification is vital, as it determines the amount of risk-weighted assets a bank must hold to buffer against potential trading losses and maintain overall financial stability within the global banking system.

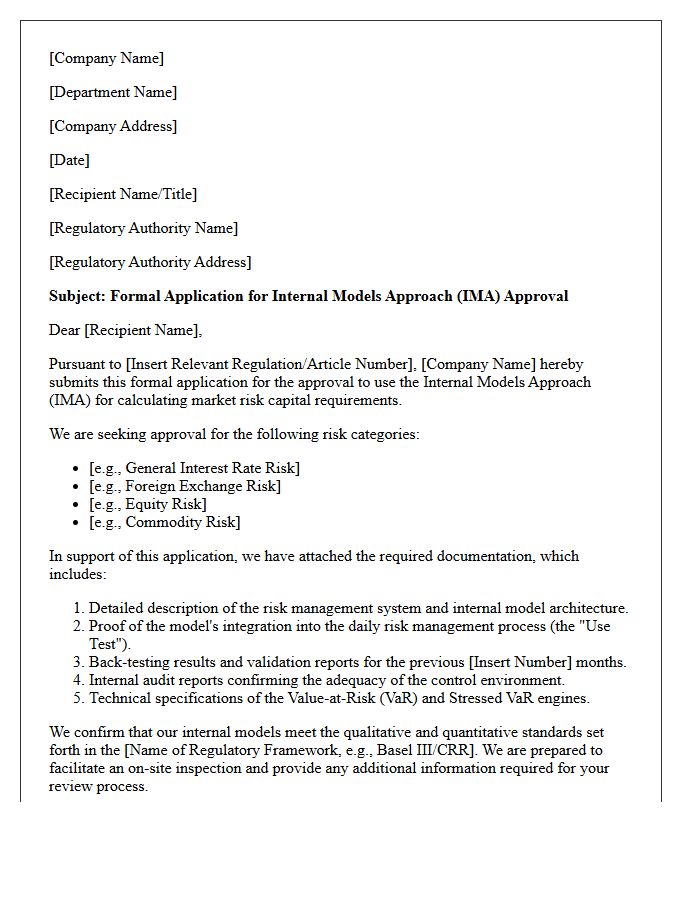

Internal Models Approach Approval Request Letter

An Internal Models Approach (IMA) Approval Request Letter is a formal submission to financial regulators seeking permission to use proprietary risk systems for calculating market risk capital requirements. Under Basel III standards, banks must demonstrate that their internal models are robust, validated, and compliant with qualitative and quantitative criteria. The letter outlines the scope of application, model methodology, and governance frameworks. Securing approval allows institutions to optimize capital allocation by replacing standardized formulas with more precise, risk-sensitive internal measurements tailored to their specific investment portfolios and trading activities.

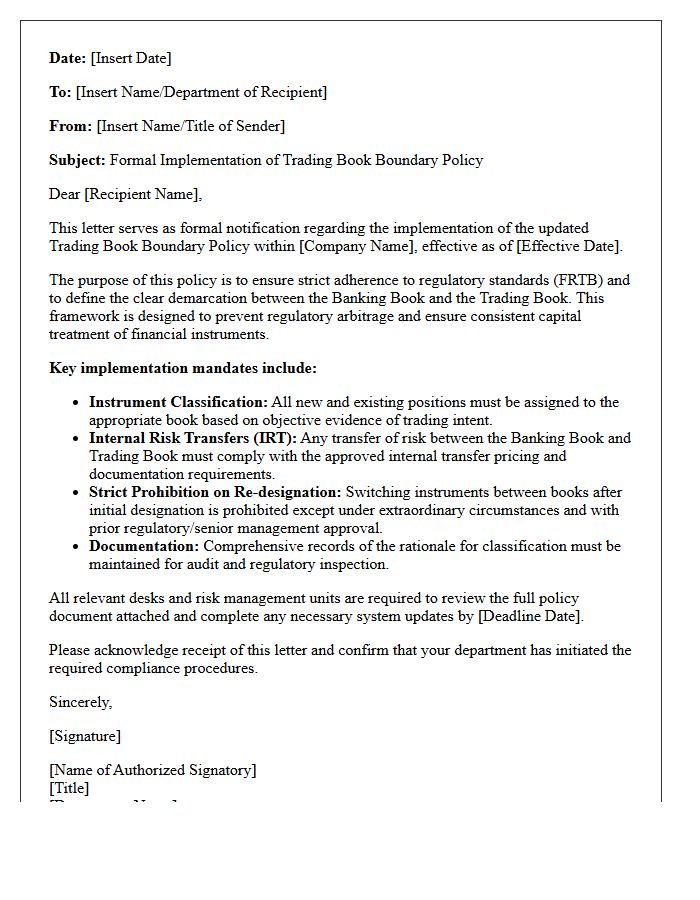

Trading Book Boundary Policy Implementation Letter

The Trading Book Boundary Policy Implementation Letter is a critical regulatory document used by financial institutions to define the classification of instruments. It ensures compliance with BCBS standards by strictly distinguishing between the trading book and the banking book. This letter outlines internal governance, risk management protocols, and the criteria for instrument allocation to prevent regulatory arbitrage. Proper implementation is essential for calculating market risk capital requirements accurately under the FRTB framework, ensuring that all financial assets are assigned to the correct regulatory regime for capital adequacy reporting.

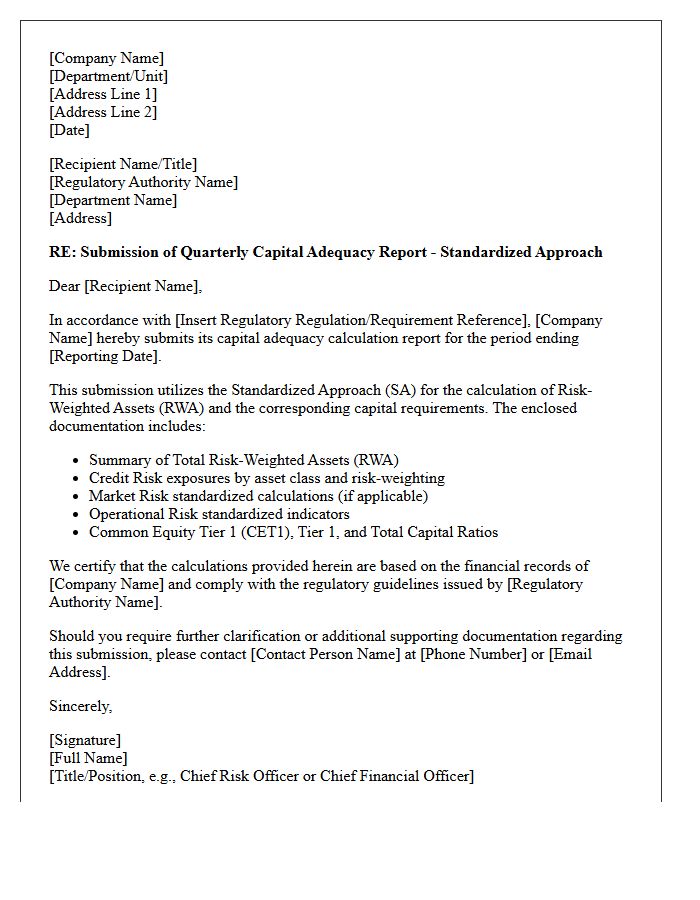

Standardized Approach Capital Calculation Submission Letter

The Standardized Approach Capital Calculation Submission Letter is a formal regulatory document used by banking institutions to report risk-weighted assets. It ensures compliance with Basel III frameworks by detailing how credit, market, and operational risks are measured using standardized formulas. This submission is critical for maintaining regulatory capital adequacy and transparency with financial supervisors. Accuracy in this letter is essential, as it validates the bank's internal safety buffers against potential losses, ensuring financial stability within the global banking system.

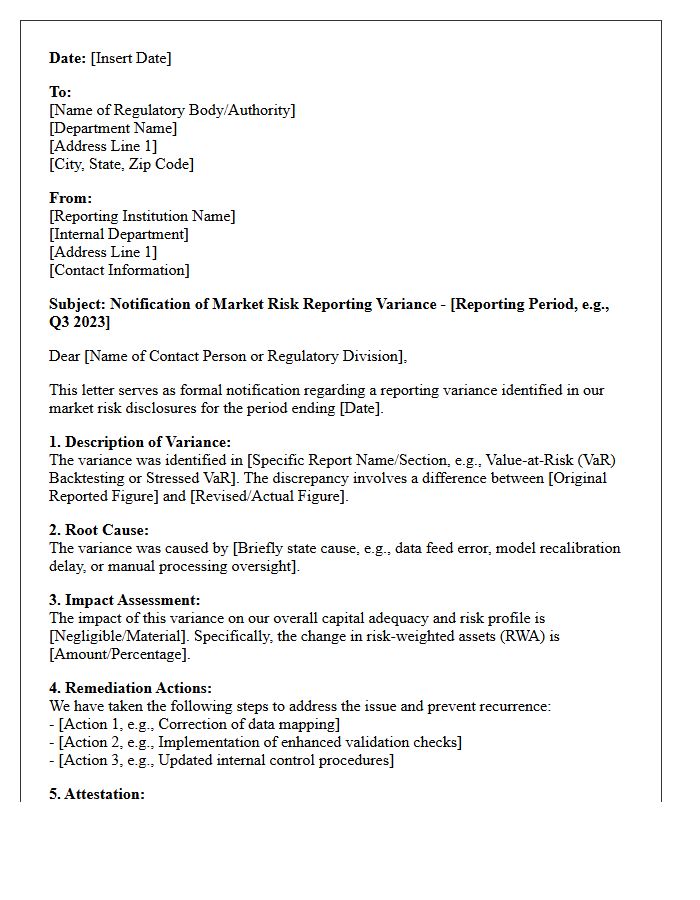

Regulatory Market Risk Reporting Variance Letter

A Regulatory Market Risk Reporting Variance Letter is a formal request submitted by financial institutions to regulators, such as the Federal Reserve or OCC. It seeks permission to deviate from standard reporting requirements when internal risk models or data constraints justify a technical exception. This document is crucial for maintaining regulatory compliance while ensuring that market risk capital calculations accurately reflect a firm's specific portfolio profile. Obtaining an approved variance prevents reporting errors and ensures alignment between institutional risk management practices and official oversight mandates.

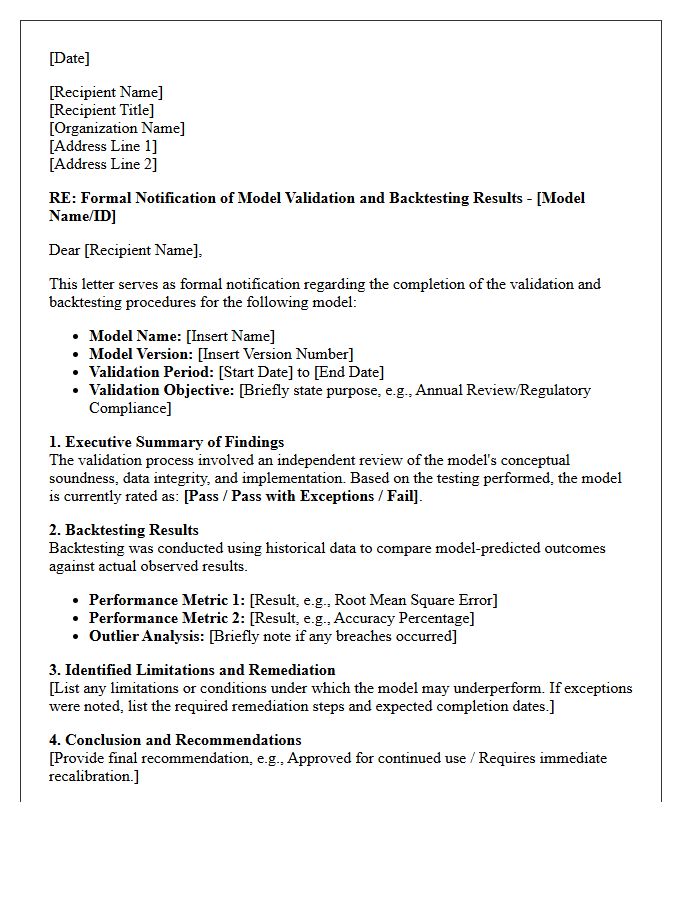

Model Validation and Backtesting Results Letter

A Model Validation and Backtesting Results Letter provides critical regulatory assurance regarding a financial model's accuracy. This document summarizes independent statistical testing to verify that predictive outputs align with historical realities. It highlights model performance, identifies potential limitations, and outlines required remediation actions. For stakeholders, this letter serves as essential evidence of risk management compliance, ensuring that decision-making tools remain robust, reliable, and transparent under various market conditions. Clear communication of these findings is vital for maintaining institutional governance standards and mitigating operational risks effectively.

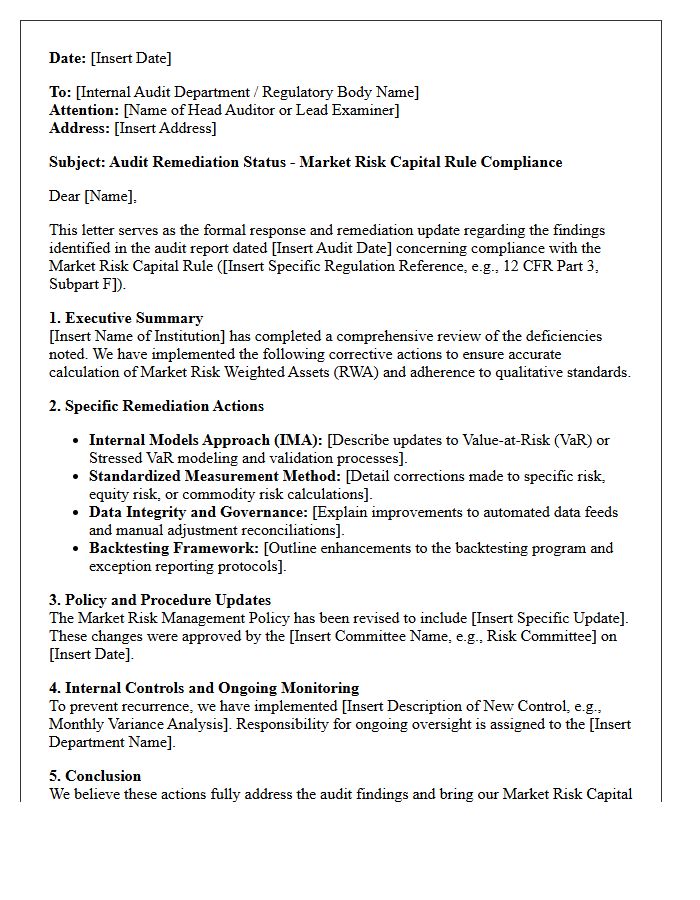

Market Risk Capital Rule Audit Remediation Letter

A Market Risk Capital Rule Audit Remediation Letter serves as a formal response to regulatory findings regarding a financial institution's capital adequacy frameworks. It outlines specific corrective actions to address deficiencies in risk modeling, data integrity, or internal controls. Banks must ensure regulatory compliance by providing clear timelines and measurable milestones for fixing identified gaps. Failure to adequately resolve these issues can lead to increased capital charges or enforcement actions. Effective remediation demonstrates robust governance and ensures that market risk exposures are accurately calculated and sufficiently covered by high-quality capital reserves.

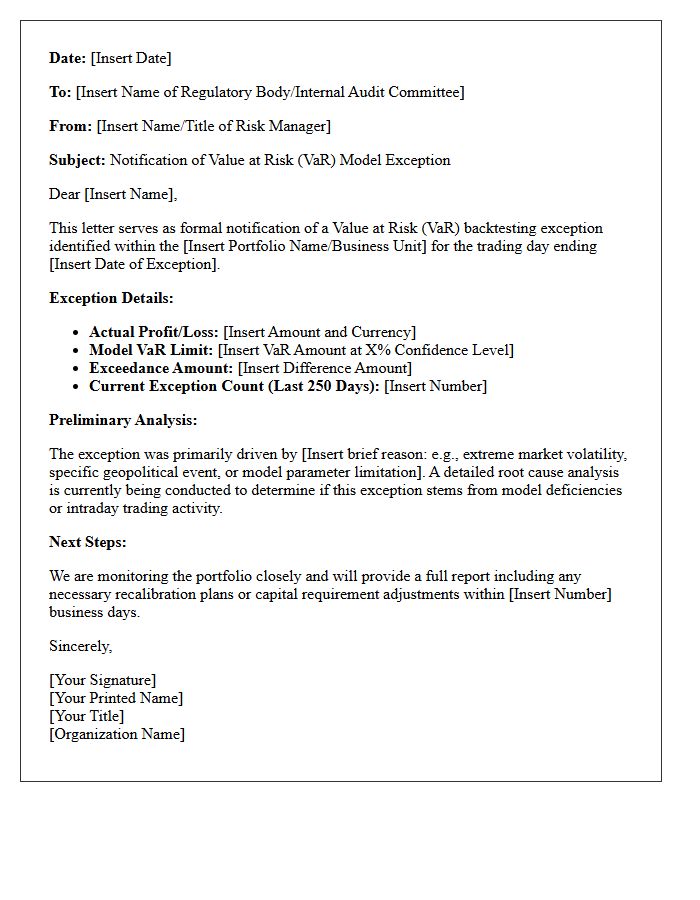

Value at Risk Model Exception Notification Letter

A Value at Risk (VaR) Exception Notification Letter is a formal communication issued when actual portfolio losses exceed predicted model thresholds. This backtesting failure indicates that the risk management model may have underestimated market volatility or exposure. Regulatory frameworks, such as Basel III, require firms to report these breaches to oversight bodies immediately. Frequent exceptions can lead to higher capital requirements and necessitate a mandatory review of the model's internal parameters to ensure financial stability and accurate risk forecasting.

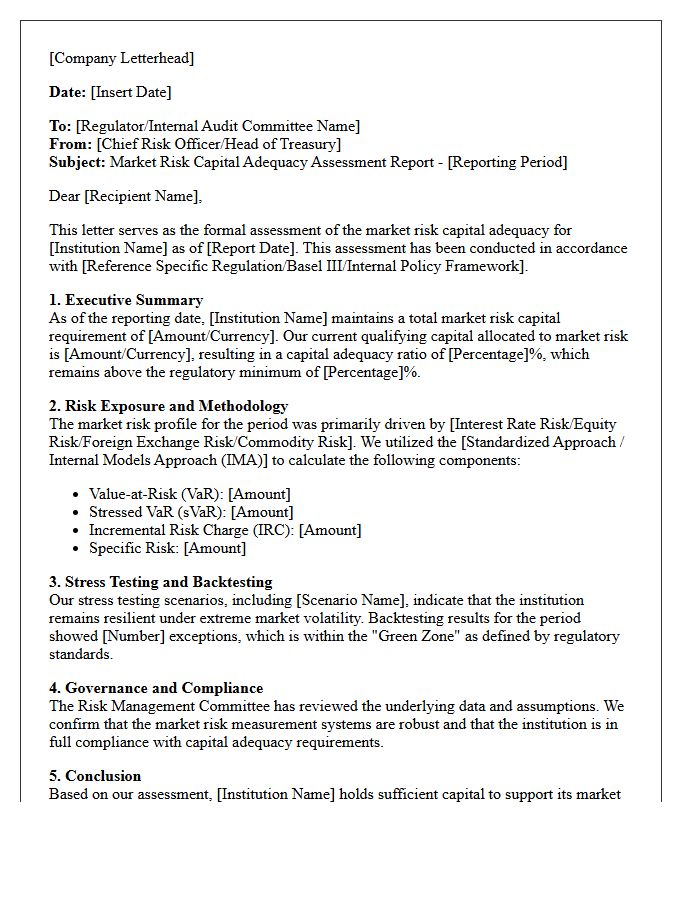

Market Risk Capital Adequacy Assessment Letter

A Market Risk Capital Adequacy Assessment Letter is a formal regulatory communication used to evaluate if a financial institution holds sufficient capital to cover potential losses from market volatility. It focuses on the Internal Models Approach (IMA) or standardized methods to quantify risks in trading books. This document ensures banks maintain a liquidity buffer against interest rate shifts, equity fluctuations, and foreign exchange risks. Regulatory bodies use this assessment to verify solvency, ensuring the firm can withstand extreme economic stress while maintaining compliance with international Basel III standards.

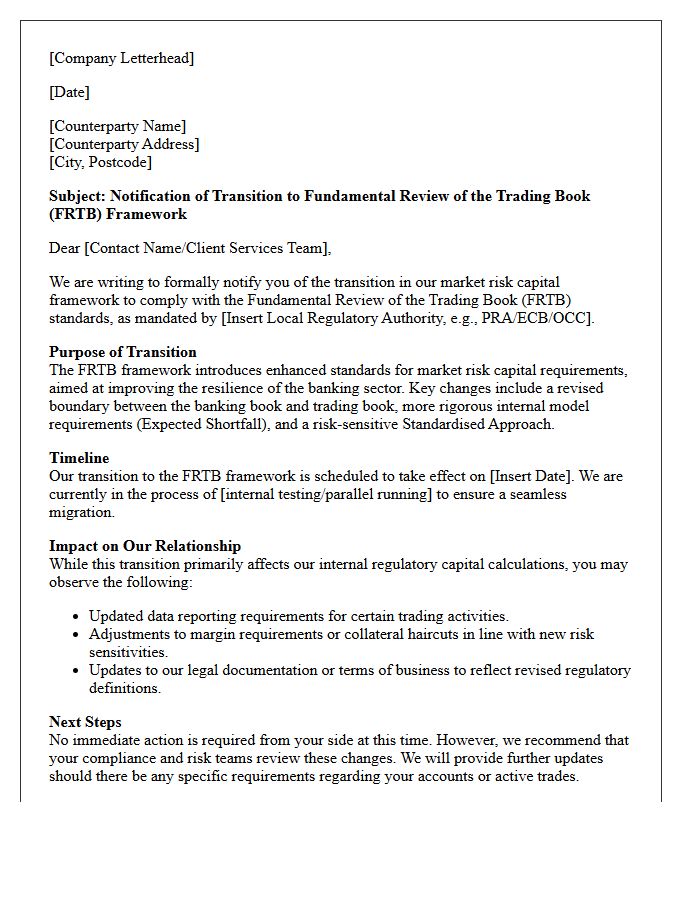

Fundamental Review of the Trading Book Transition Letter

The Fundamental Review of the Trading Book (FRTB) Transition Letter outlines the mandatory shift toward enhanced market risk frameworks. It serves as a regulatory roadmap for financial institutions to align internal models and standardized approaches with Basel III standards. Key highlights include requirements for capital adequacy, data integrity, and strict reporting timelines. Banks must prioritize the Internal Model Approach (IMA) validation or the Standardized Approach (SA) implementation to ensure compliance. Understanding this transition is vital for mitigating regulatory risk and optimizing capital charges in a volatile trading environment.

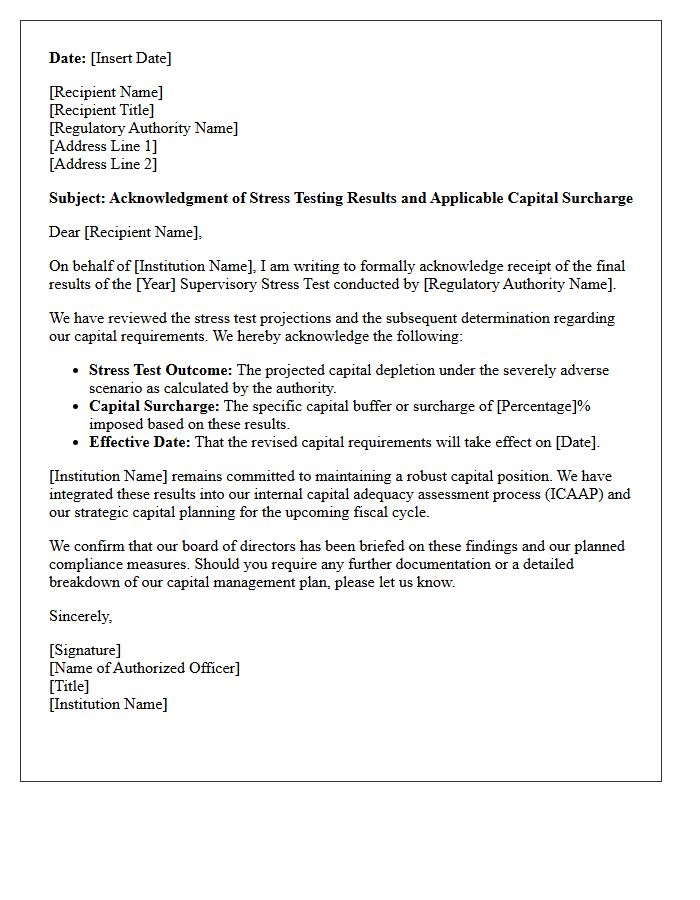

Stress Testing and Capital Surcharge Acknowledgment Letter

A Stress Testing and Capital Surcharge Acknowledgment Letter is a formal document where financial institutions confirm their regulatory compliance with capital adequacy requirements. It acknowledges the results of rigorous stress tests, which evaluate a bank's ability to withstand economic crises. By signing, the entity accepts specific capital surcharges imposed by regulators like the Federal Reserve to mitigate systemic risk. This letter serves as a binding commitment to maintain sufficient buffers, ensuring the institution remains solvent and stable during periods of extreme financial volatility and market distress.

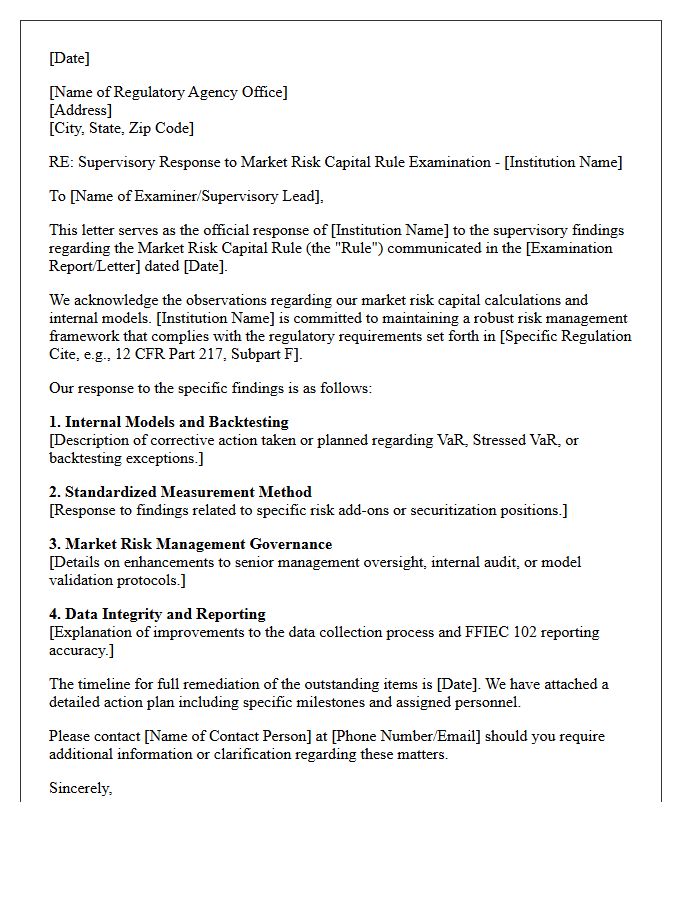

Market Risk Capital Rule Supervisory Response Letter

The Supervisory Response Letter serves as the official regulatory feedback regarding a banking organization's internal models for market risk. Under the Market Risk Capital Rule, this document outlines specific conditions, model limitations, and required capital add-ons. It is the primary mechanism through which regulators approve or restrict the use of proprietary models for calculating risk-weighted assets. Financial institutions must strictly adhere to the mandates within this letter to ensure regulatory compliance and maintain adequate capital buffers against potential trading losses and market volatility.

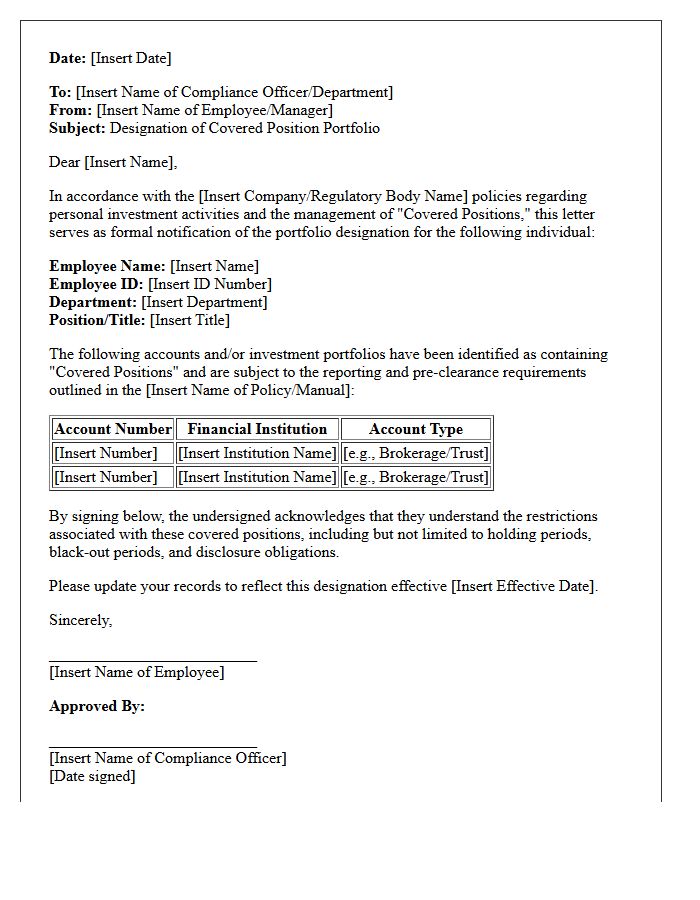

Covered Position Portfolio Designation Letter

A Covered Position Portfolio Designation Letter is a formal document used by financial institutions to identify specific assets held for risk management. It officially designates which securities are part of a trading portfolio versus those held for investment. This classification is crucial for regulatory compliance, specifically under Basel III standards and the Volcker Rule, to determine capital requirements. By clearly labeling these positions, firms ensure accurate market risk assessments and maintain transparency with financial regulators regarding their liquidity and hedging strategies.

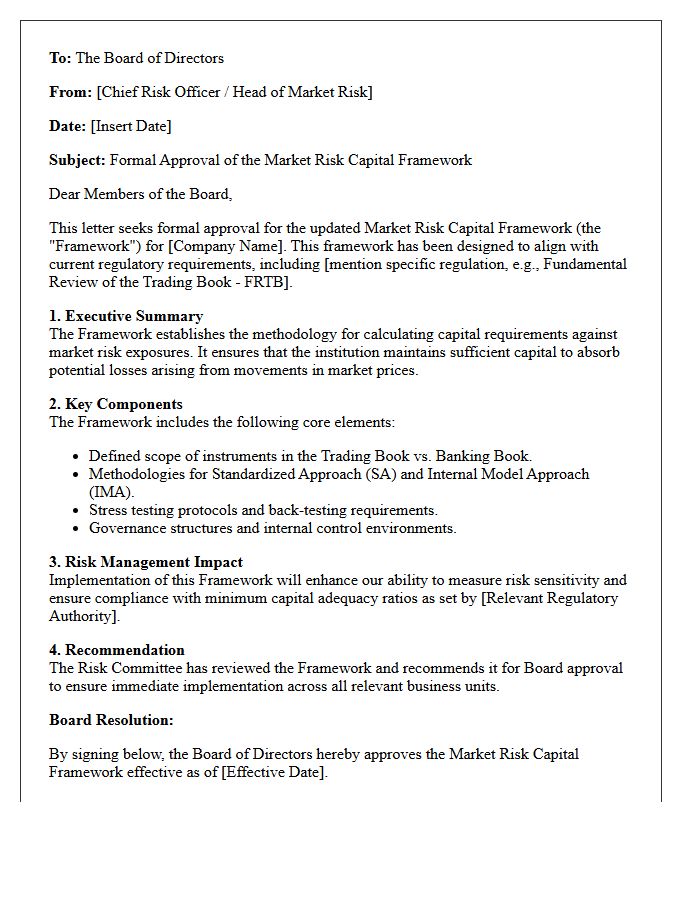

Market Risk Capital Framework Board Approval Letter

The Market Risk Capital Framework Board Approval Letter is a critical regulatory document confirming that a financial institution's governing body has reviewed and authorized internal risk management models. It ensures compliance with Fundamental Review of the Trading Book (FRTB) standards, validating that capital requirements align with actual market exposure. This letter demonstrates fiduciary oversight and institutional accountability, confirming that senior leadership understands the methodologies used to calculate Risk-Weighted Assets (RWA). Obtaining formal board approval is a mandatory step for banks seeking regulatory permission to use internal models for calculating market risk capital.

What is the purpose of the Market Risk Capital Rule Letter?

The Market Risk Capital Rule Letter provides formal guidance to banking organizations on complying with regulatory capital requirements for portfolios subject to market risk, ensuring that institutions hold sufficient capital against potential losses from price fluctuations.

Which financial institutions are subject to the Market Risk Capital Rule?

The rule generally applies to banking organizations with significant trading activity, specifically those with aggregate trading assets and liabilities equal to 10% or more of total assets, or those exceeding a specified total dollar threshold in trading activity.

How does the rule define "covered positions" for capital calculation?

Covered positions include all assets and liabilities held for the purpose of short-term resale, profiting from short-term price movements, or hedging other trading positions, excluding certain non-trading assets such as real estate or consumer loans.

What methodologies are permitted for calculating market risk capital requirements?

Institutions may use a combination of internal models, such as Value-at-Risk (VaR) and Stressed VaR, or standardized measurements for specific risk components to determine their total risk-weighted assets for market risk.

What are the reporting requirements under the Market Risk Capital Rule?

Banking organizations must provide regular public disclosures and regulatory reports that detail their market risk management framework, the structure of their internal models, and the specific capital charges allocated to different risk categories.

Comments