A Right to Cure Default Notice is a formal legal notification sent to a borrower, providing a specific timeframe to rectify a contract breach or missed payment before acceleration occurs. This essential document protects consumer rights and ensures transparency in lending agreements. To help you draft an effective notice, below are some ready to use templates.

Image cover: Essential Right to Cure Default Notice Templates and Samples

Letter Samples List

- Commercial Loan Payment Default Right To Cure Letter

- Residential Mortgage Delinquency Right To Cure Letter

- Auto Financing Contract Default Right To Cure Letter

- Small Business Line Of Credit Breach Right To Cure Letter

- Personal Promissory Note Default Right To Cure Letter

- Equipment Lease Agreement Default Right To Cure Letter

- Credit Card Account Arrears Right To Cure Letter

- Breach Of Financial Covenant Right To Cure Letter

- Commercial Real Estate Loan Default Right To Cure Letter

- Construction Loan Milestone Default Right To Cure Letter

- Overdraft Account Settlement Right To Cure Letter

- Secured Guaranty Default Right To Cure Notice Letter

Commercial Loan Payment Default Right To Cure Letter

A Commercial Loan Payment Default Right to Cure Letter is a formal legal notice sent by lenders to borrowers after a missed payment. This document outlines the specific breach of contract and provides a mandatory grace period to rectify the delinquency. Understanding this letter is critical because it represents the final opportunity to restore the loan's standing before the lender initiates foreclosure or acceleration. Borrowers must act within the stated timeframe to avoid legal action, additional penalties, or the loss of their commercial property collateral.

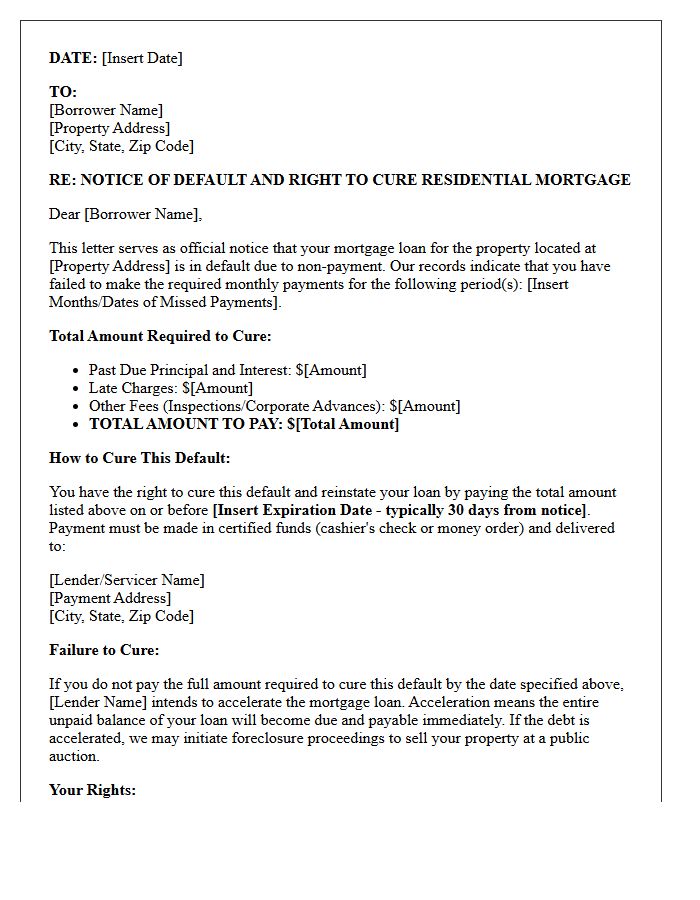

Residential Mortgage Delinquency Right To Cure Letter

A Residential Mortgage Delinquency Right to Cure Letter is a mandatory legal notice sent to borrowers who fall behind on payments. This document serves as a formal warning before foreclosure proceedings begin, granting a specific timeframe-typically 30 to 90 days-to pay the overdue balance. It must detail the exact amount owed, any late fees, and the deadline for payment. Receiving this letter is a critical opportunity for homeowners to reinstate their loan and maintain ownership by resolving the default according to state-specific consumer protection laws.

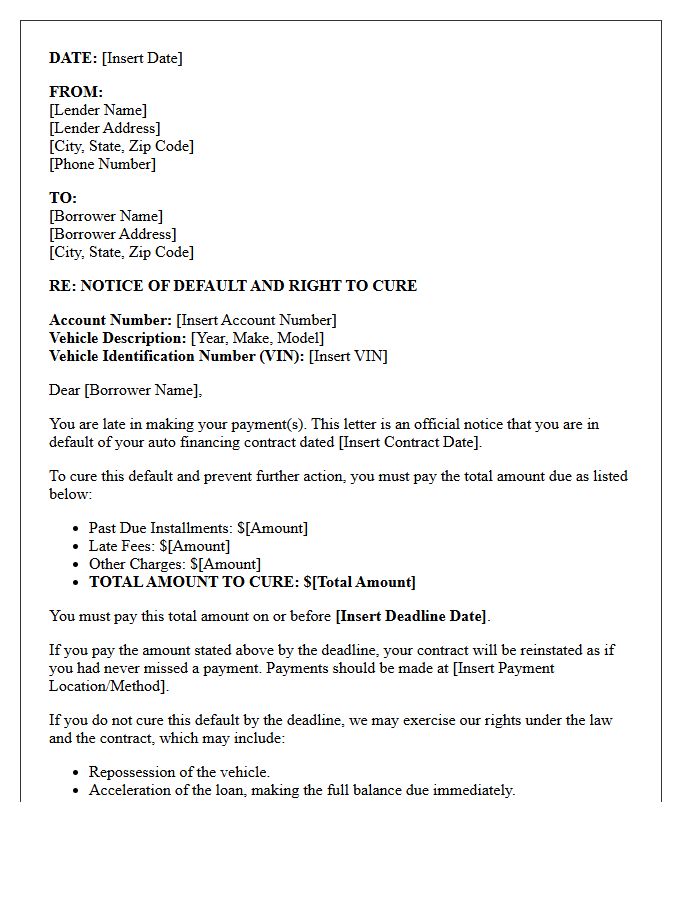

Auto Financing Contract Default Right To Cure Letter

An Auto Financing Contract Default Right to Cure Letter is a mandatory legal notice sent by lenders when a borrower misses payments. This document grants you a specific timeframe, typically fifteen to thirty days, to pay the delinquent amount and reinstate your loan agreement. Receiving this letter is critical because it serves as the final warning before repossession of the vehicle occurs. Acting promptly by paying the requested balance or contacting the creditor can prevent the loss of your car and protect your credit score from severe long-term damage.

Small Business Line Of Credit Breach Right To Cure Letter

A Small Business Line of Credit Breach Right to Cure Letter is a formal legal notice sent by a lender when a borrower defaults on their agreement. This document is crucial because it provides the debtor a specific timeframe to rectify the violation, such as making overdue payments, before the lender accelerates the debt or seizes collateral. Understanding your contractual obligations and responding within the designated grace period is essential to prevent permanent default status and protect your business credit score from severe long-term damage.

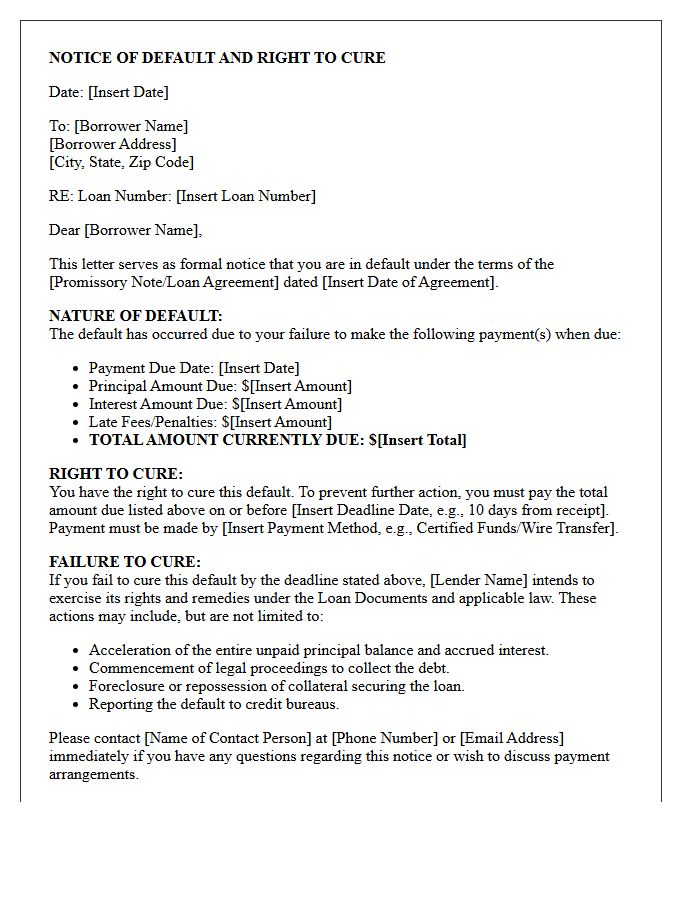

Personal Promissory Note Default Right To Cure Letter

A Personal Promissory Note Default Right To Cure Letter is a formal legal notice issued when a borrower misses a payment. Its primary purpose is to provide the debtor a specific grace period to rectify the default before the lender initiates acceleration or legal action. This document must clearly state the total amount overdue, including late fees, and the exact deadline for payment. Issuing this letter is often a mandatory procedural requirement dictated by state laws or the original loan agreement to protect consumer rights before permanent foreclosure or litigation begins.

Equipment Lease Agreement Default Right To Cure Letter

An Equipment Lease Agreement Default Right To Cure Letter is a formal legal notice sent when a lessee breaches contract terms, such as missing payments. This formal notification provides a specific timeframe, or "cure period," for the lessee to rectify the violation before the lessor initiates repossession or litigation. Understanding your contractual obligations is vital, as failing to act within the allotted window can result in lease acceleration, significant penalties, and the loss of essential business machinery. Always verify state-specific laws regarding your legal right to remedy defaults.

Credit Card Account Arrears Right To Cure Letter

A credit card account arrears Right to Cure letter is a formal legal notice sent when a borrower defaults on payments. This document serves as a final opportunity to restate the account by paying the past-due balance within a specific timeframe, typically thirty days. Receiving this notice is critical because it acts as a mandatory precursor to aggressive debt collection or legal action. To protect your consumer rights and avoid account acceleration, you must respond or provide the required payment before the deadline specified in the letter.

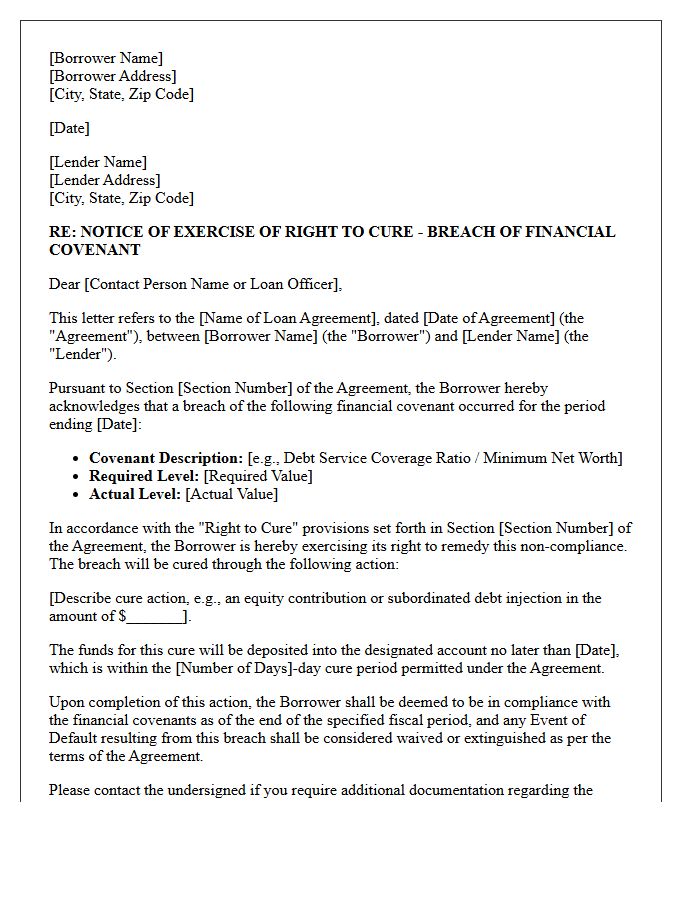

Breach Of Financial Covenant Right To Cure Letter

A Breach of Financial Covenant Right to Cure Letter is a formal legal notification issued when a borrower fails to meet specific financial ratios. This document outlines the default event while specifying the contractual timeframe allowed to rectify the violation. Utilizing a cure right, often through an equity injection or debt restructuring, prevents immediate loan acceleration. It is a critical mechanism for maintaining liquidity and avoiding foreclosure. Borrowers must strictly adhere to the remedy period defined in the credit agreement to restore compliance and preserve the lending relationship.

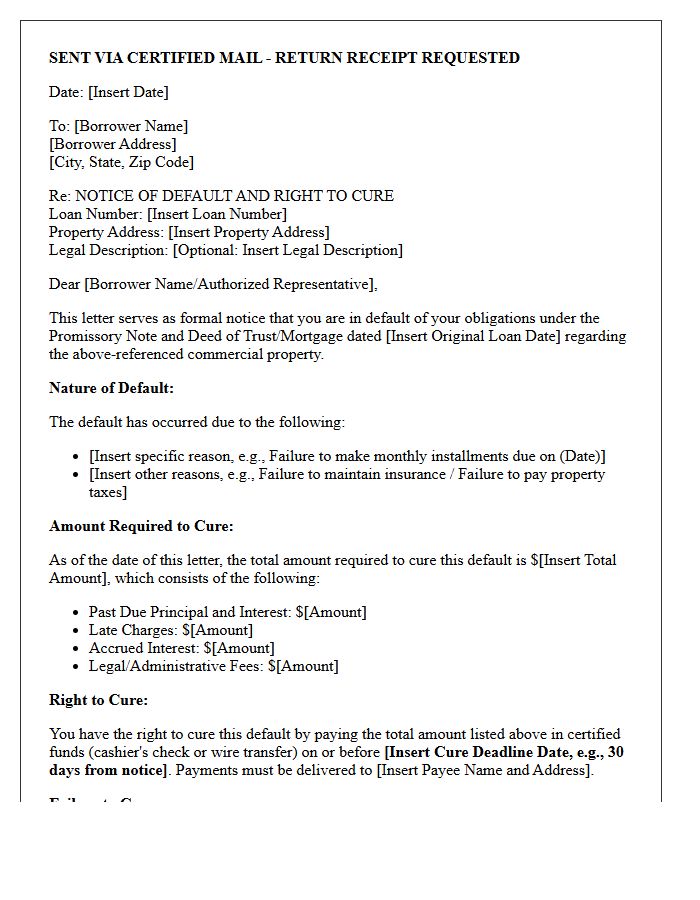

Commercial Real Estate Loan Default Right To Cure Letter

A Right to Cure Letter is a formal legal notice sent by lenders when a borrower defaults on a commercial mortgage. This document specifies the exact nature of the breach, such as missed payments or covenant violations. Crucially, it outlines a specific grace period during which the borrower can rectify the default to avoid foreclosure or loan acceleration. Understanding the strictly defined timelines within this letter is vital for protecting your property interests and maintaining the legal standing of your commercial real estate investment during financial distress.

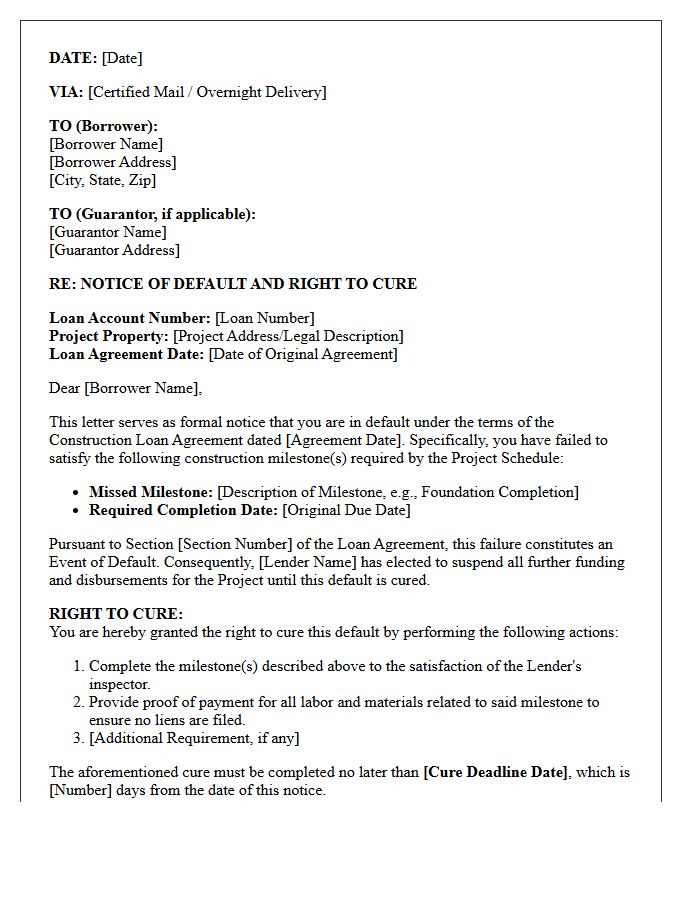

Construction Loan Milestone Default Right To Cure Letter

A Construction Loan Milestone Default Right To Cure Letter is a formal legal notice sent when a borrower fails to meet specific project deadlines. This document identifies the breach of contract and provides a mandatory period for the borrower to rectify the delay before the lender accelerates the loan or terminates funding. It serves as a critical procedural protection, ensuring transparency and offering a final opportunity to restore compliance. Understanding the cure period is essential for developers to avoid foreclosure and maintain project continuity during financial or operational setbacks.

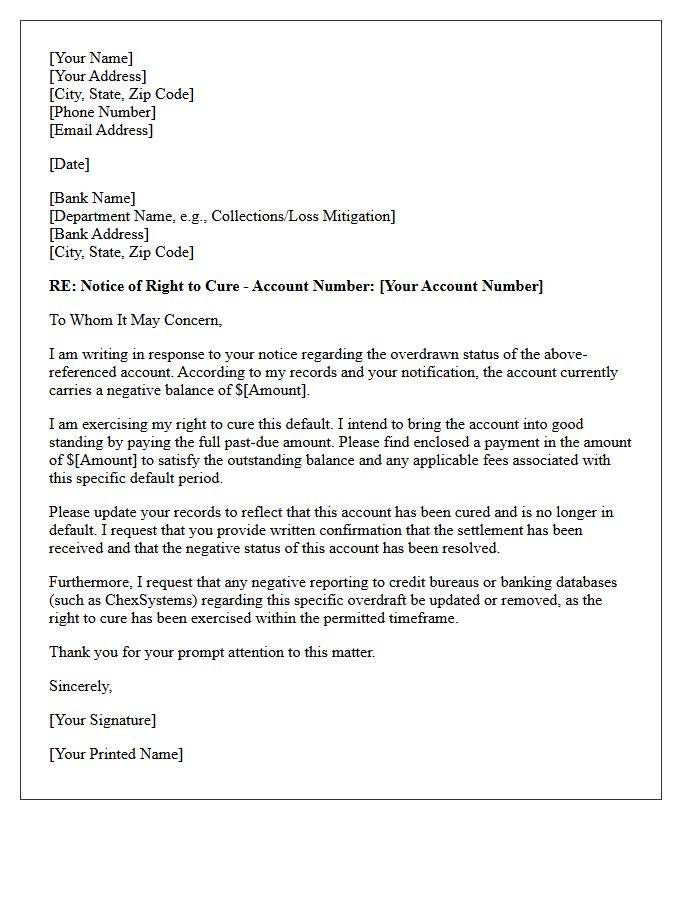

Overdraft Account Settlement Right To Cure Letter

An Overdraft Account Settlement Right To Cure Letter is a formal legal notice sent by financial institutions when a bank account remains overdrawn. This document is crucial because it grants you a specific timeframe to repay the outstanding balance before the bank takes further action. Receiving this letter is a final opportunity to resolve the debt and prevent the account from being permanently closed. Promptly addressing this notice helps you avoid negative reporting to credit bureaus and specialty agencies like ChexSystems, protecting your future ability to open banking accounts.

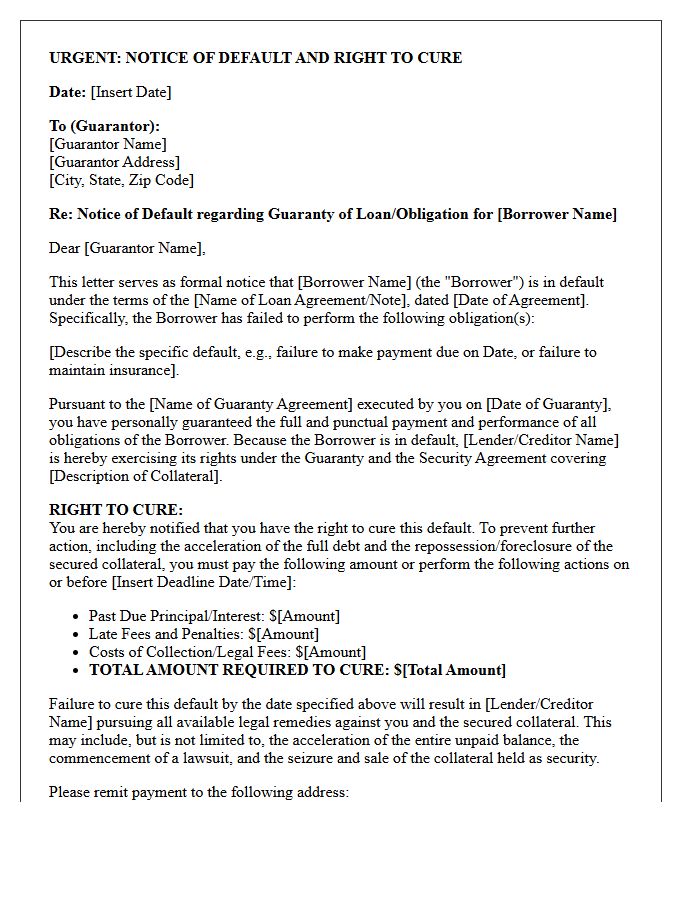

Secured Guaranty Default Right To Cure Notice Letter

A Secured Guaranty Default Right To Cure Notice Letter is a formal legal document issued when a borrower defaults on a loan. It notifies the guarantor that they have a specific period, known as the right to cure, to rectify the breach by making overdue payments or fixing contract violations. This notice is a mandatory step before a lender can accelerate the debt or seize collateral. Failing to respond within the timeframe allows the creditor to pursue full repayment, making timely remediation critical for protecting assets and maintaining the guaranty agreement terms.

What is a Right to Cure Default Notice?

A Right to Cure Default Notice is a formal legal notification sent to a borrower stating that they have breached their loan agreement, typically through non-payment, and providing a specific period of time to correct the default before foreclosure or repossession begins.

How long do I have to respond to a Right to Cure notice?

The time frame varies by state law and contract terms, but typically ranges from 20 to 30 days. During this period, the lender cannot legally pursue further collection actions or seizure of collateral if the required payment is made.

What happens if I do not cure the default by the deadline?

If the default is not cured within the designated timeframe, the lender may accelerate the loan, meaning the entire balance becomes due immediately. This usually serves as the final step before the commencement of foreclosure proceedings or vehicle repossession.

What information must be included in a Right to Cure Notice?

To be legally valid, the notice must clearly state the total amount required to bring the account current, the specific deadline for payment, the method of payment accepted, and the consequences of failing to take action.

Can a lender refuse payment once a Right to Cure Notice is issued?

No, if the borrower tenders the full amount specified in the notice within the legal cure period, the lender is legally obligated to accept the payment and reinstate the original terms of the loan agreement as if the default never occurred.

Comments