Filing a formal grievance letter for failed wire transfer processing is essential when a bank fails to execute your transaction promptly. This document protects your consumer rights and creates a legal record of the financial institution's negligence or technical errors. If your funds are delayed or missing, follow our professional guide. Below are some ready to use templates.

Image cover: Formal Wire Transfer Grievance Letter Samples and Professional Templates

Letter Samples List

- Grievance Letter for Failed Domestic Wire Transfer Processing

- Formal Complaint Letter for Unprocessed International Wire Transfer

- Dispute Letter for Delayed Corporate Wire Transfer Processing

- Customer Grievance Letter for Rejected SWIFT Transfer Processing

- Escalation Letter for Unresolved Wire Transfer Failure

- Official Grievance Letter for Missing Interbank Wire Transfer Funds

- Notification Letter for Failed Business Wire Transfer Execution

- Demand Letter for Reversal of Failed Wire Transfer Fees

- Notice Letter of Grievance for Incomplete Cross-Border Wire Transfer

- Client Grievance Letter for Erroneous Wire Transfer Processing

- Resolution Request Letter for Failed High-Value Wire Transfer

- Appeal Letter for Denied Wire Transfer Investigation

- Institutional Grievance Letter for Systemic Wire Transfer Failures

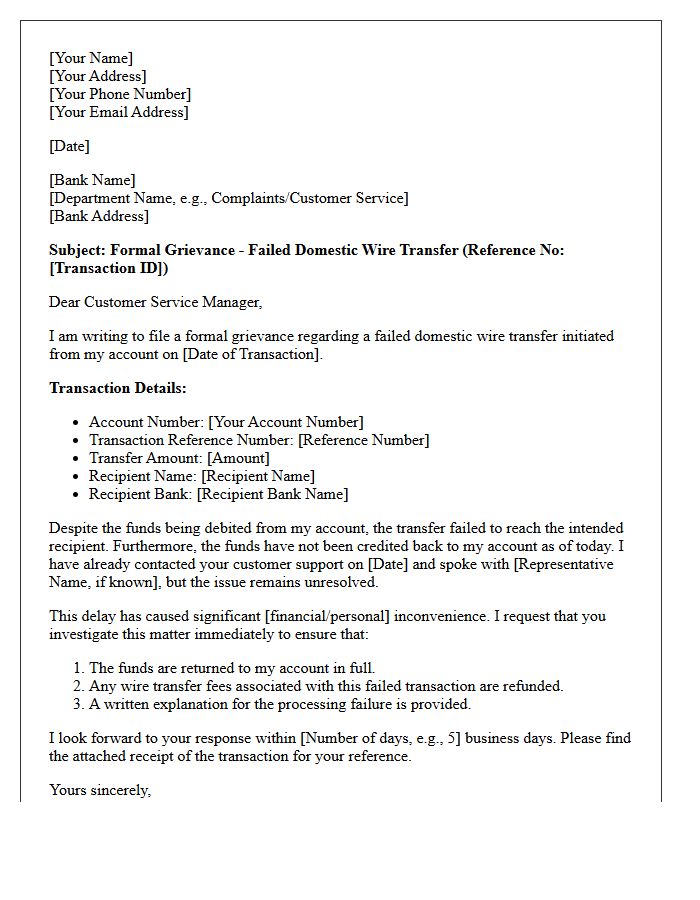

Grievance Letter for Failed Domestic Wire Transfer Processing

A formal grievance letter is essential when a bank fails to process a domestic wire transfer correctly. Clearly state the transaction date, exact amount, and reference number. Explicitly describe the bank's error, such as a processing delay or incorrect routing. Demand an immediate trace and reversal of funds while requesting compensation for any resulting financial losses or late fees. Documentation serves as vital legal evidence if you must escalate the dispute to regulatory authorities or ombudsmen to ensure a swift resolution and fund recovery.

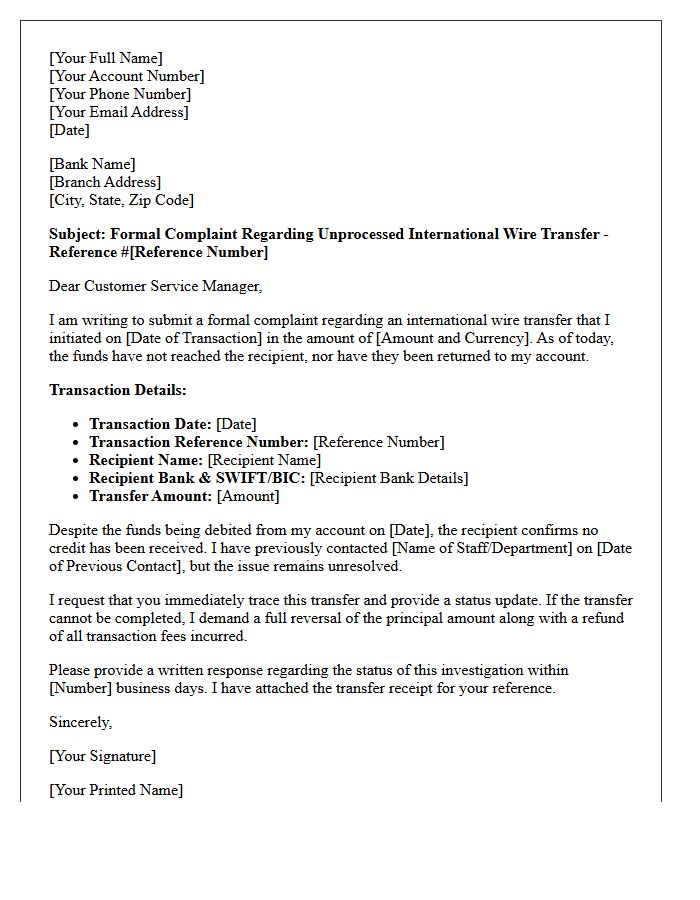

Formal Complaint Letter for Unprocessed International Wire Transfer

When drafting a formal complaint letter for an unprocessed international wire transfer, you must provide the transaction reference number and precise dates. Clearly state the amount, currency, and beneficiary details to ensure the bank can track the funds. Demand an immediate payment trace or a status update regarding the delay. Emphasize the financial impact caused by the failure to fulfill the transfer request. Conclude by requesting a formal written response within a specific timeframe to maintain a legal record of your dispute for potential regulatory escalation.

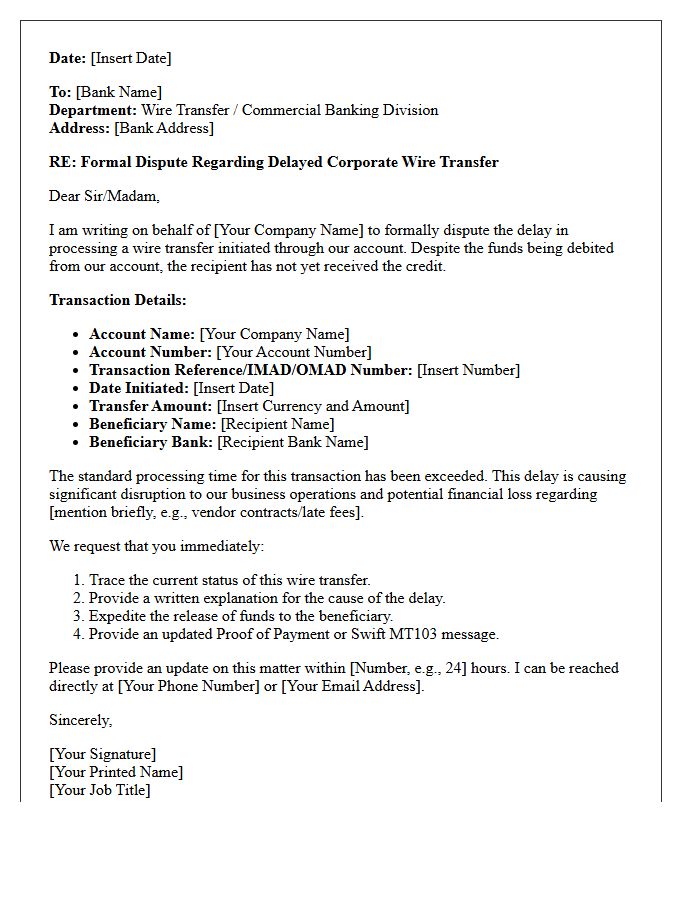

Dispute Letter for Delayed Corporate Wire Transfer Processing

When sending a dispute letter for a delayed corporate wire transfer, timing and accuracy are critical. Clearly state the transaction reference number, the exact amount, and the date the funds were initiated. Explicitly cite the bank's failure to meet its processing deadlines and demand an immediate status update or reversal of the funds. Mention potential financial losses or breach of contract risks to ensure the institution prioritizes your claim. Providing full supporting documentation of the transfer ensures the compliance department can expedite the investigation and resolve the processing error quickly.

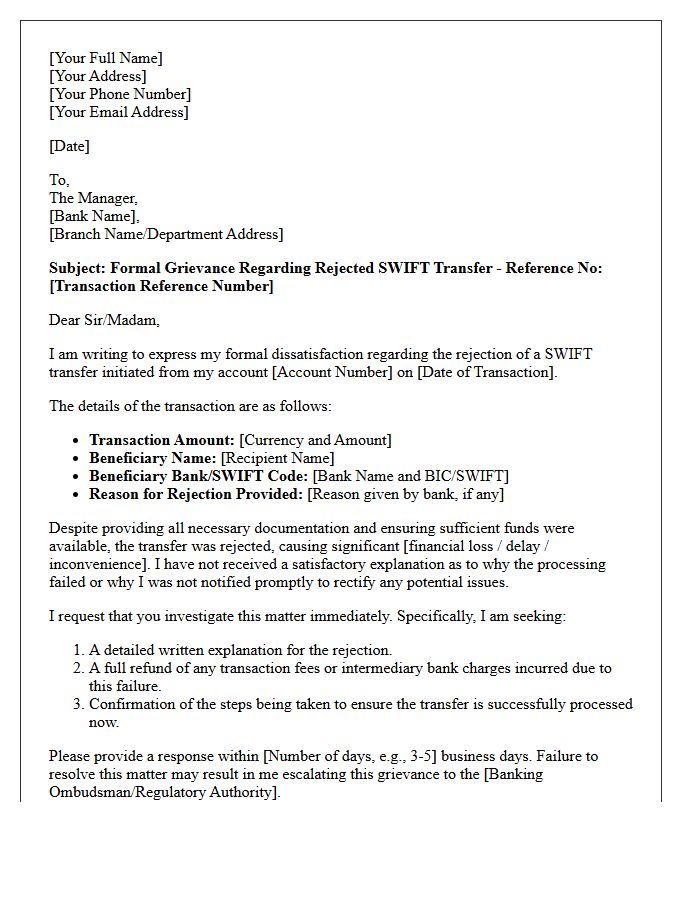

Customer Grievance Letter for Rejected SWIFT Transfer Processing

When drafting a customer grievance letter for a rejected SWIFT transfer, clearly state the Transaction Reference Number and exact amount. Explicitly demand a detailed rejection reason from the bank to identify if the issue stems from incorrect intermediary details, compliance flags, or insufficient documentation. Formally request the immediate reversal of funds, including any deducted processing fees, to your original account. Maintain a professional tone and specify a reasonable timeframe for a resolution before escalating the matter to a financial ombudsman or regulatory authority to ensure consumer protection rights.

Escalation Letter for Unresolved Wire Transfer Failure

An escalation letter is a formal document sent to senior bank management when a wire transfer fails and standard support channels offer no resolution. It should clearly outline the transaction details, including the reference number, date, and exact amount. Highlight the financial impact of the delay and set a specific deadline for a response. By demanding a formal investigation and a trace on the funds, you hold the institution accountable and prioritize your case for immediate review. Maintaining a professional tone is essential for achieving a swift and successful recovery.

Official Grievance Letter for Missing Interbank Wire Transfer Funds

An Official Grievance Letter is a formal document used to initiate a trace for missing interbank wire transfers. When funds fail to arrive within forty-eight hours, you must provide your bank with the IMAD/OMAD reference number and a specific timeline of the transaction. This letter serves as a legal record, forcing the financial institution to investigate potential routing errors or compliance holds. Clearly state the sender details, receiving account information, and the exact amount to ensure a swift resolution and recovery of your capital.

Notification Letter for Failed Business Wire Transfer Execution

A notification letter regarding a failed business wire transfer is a critical security alert issued by your financial institution. It signifies that an outgoing payment was rejected due to incorrect banking details, insufficient funds, or potential fraud detection. To prevent financial loss or operational delays, you must immediately verify the recipient's account information and contact your bank's support team. Acting quickly ensures the integrity of your cash flow and helps confirm whether the transaction failure was a technical error or a targeted cybersecurity threat like business email compromise.

Demand Letter for Reversal of Failed Wire Transfer Fees

When a bank error causes a transaction failure, a formal Demand Letter for Reversal of Failed Wire Transfer Fees is essential for recovery. This document clearly outlines the transaction details, the specific error made by the financial institution, and the exact amount of unjust fees charged. By formally requesting a refund in writing, you create a legal paper trail that holds the bank accountable. Highlighting your consumer rights and the bank's failure to execute instructions ensures a professional approach to reclaiming lost funds and correcting account balances effectively.

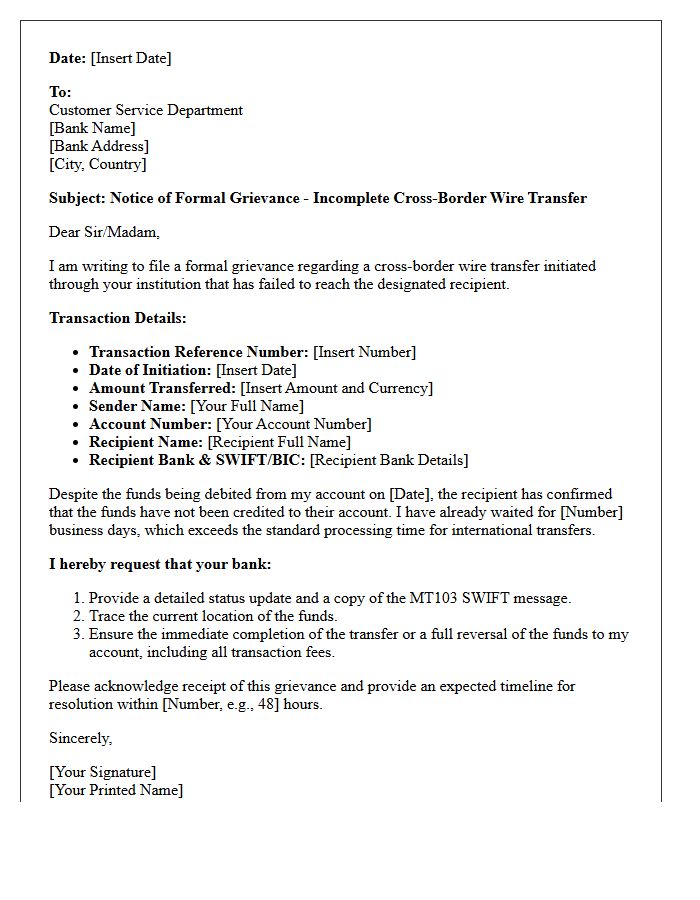

Notice Letter of Grievance for Incomplete Cross-Border Wire Transfer

A Notice Letter of Grievance is a formal document sent to a financial institution to report an incomplete cross-border wire transfer. It serves as a legal record of your dispute regarding missing funds or processing delays. The letter should clearly state the transaction reference number, amount, and date. Under international banking regulations, filing this notice obligates the bank to conduct a formal investigation into the routing error. Promptly submitting this grievance is essential for tracking lost international payments and initiating reimbursement or fund recovery processes.

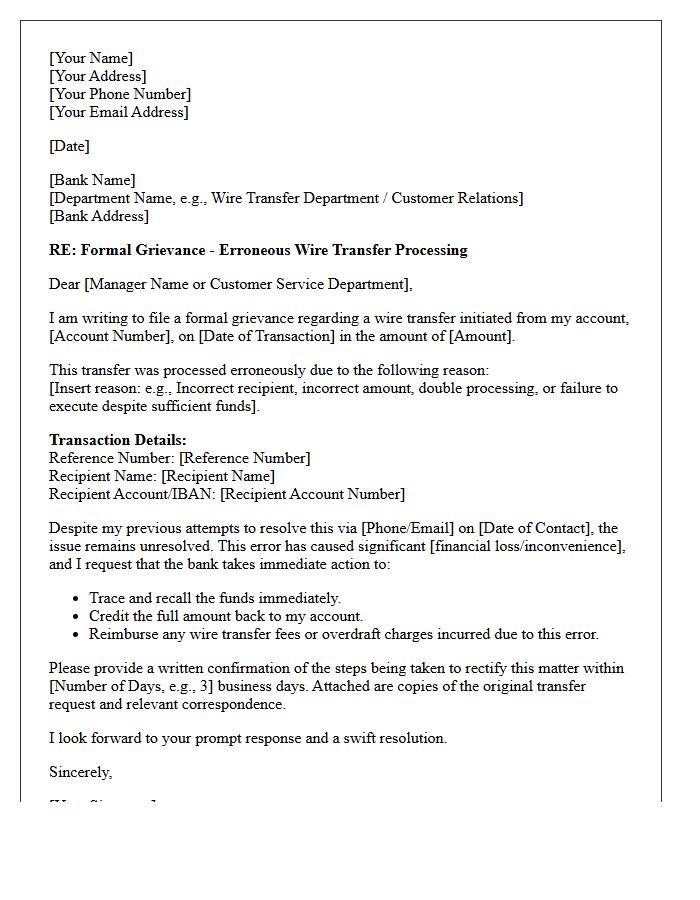

Client Grievance Letter for Erroneous Wire Transfer Processing

A client grievance letter for erroneous wire transfer processing is a formal legal notice used to dispute financial inaccuracies. It must clearly state the transaction details, including the date, amount, and reference number. To ensure a prompt resolution, highlight the specific banking error and demand an immediate reversal or correction of funds. Providing supporting documentation is essential for regulatory compliance and consumer protection. Sending this letter via certified mail creates a vital paper trail for potential legal recourse or formal escalation to financial authorities if the bank fails to rectify the mistake.

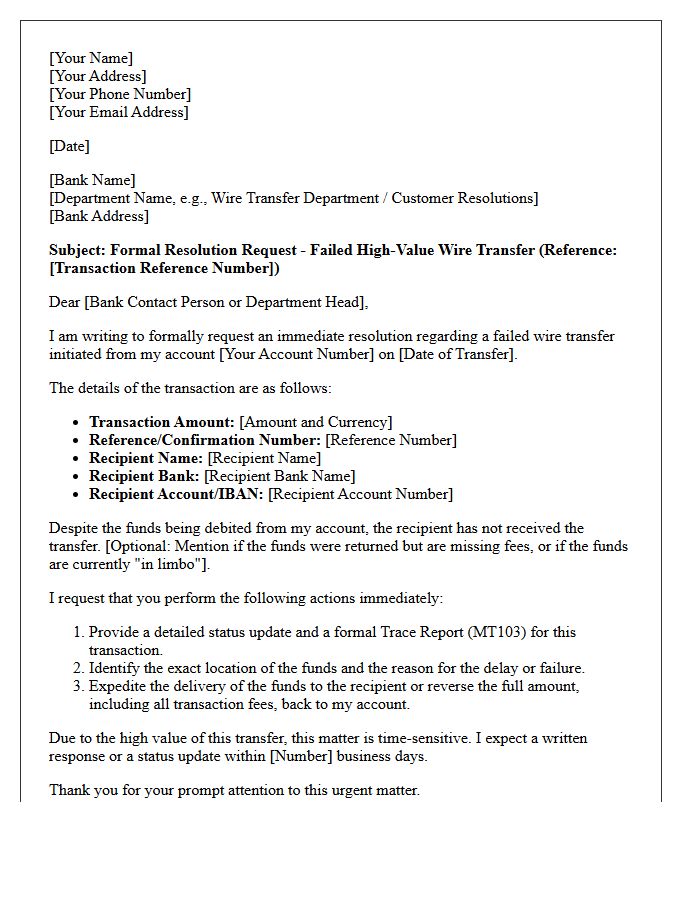

Resolution Request Letter for Failed High-Value Wire Transfer

A Resolution Request Letter is a formal document sent to a bank to rectify a failed high-value wire transfer. It must clearly state the transaction reference number, exact amount, and date of the incident. To expedite recovery, include evidence of the failed status and specify your demand for an immediate reversal or credit. Formally documenting the error creates a critical legal paper trail, ensuring the financial institution remains accountable under banking regulations while protecting your capital from prolonged processing delays or lost funds during transit.

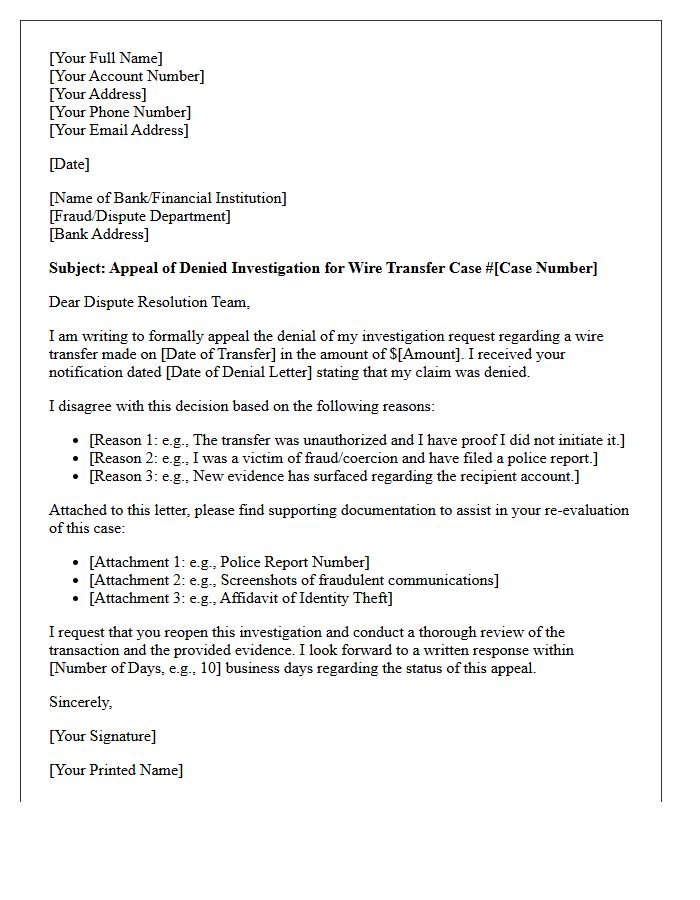

Appeal Letter for Denied Wire Transfer Investigation

When drafting an Appeal Letter for Denied Wire Transfer Investigation, you must provide clear new evidence or specific documentation that contradicts the bank's initial findings. Clearly state your case reference number and outline any discrepancies in the transaction timeline. Focus on demonstrating that the transfer was unauthorized or that a technical error occurred. Highlighting a breach of consumer protection regulations, such as the Electronic Fund Transfer Act, can strengthen your position. Maintain a professional tone and request a formal re-evaluation of your claim to recover your missing funds effectively.

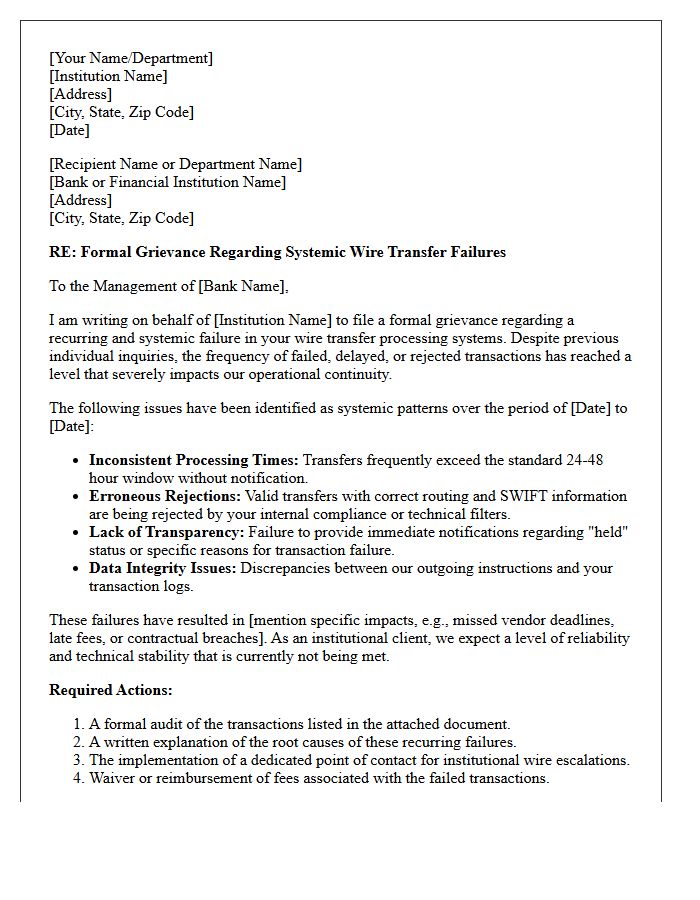

Institutional Grievance Letter for Systemic Wire Transfer Failures

An Institutional Grievance Letter is a formal legal instrument used to challenge systemic wire transfer failures within a financial organization. This document holds the institution accountable for chronic technical glitches, delayed settlements, or security breaches affecting multiple transactions. By citing consumer protection laws and regulatory non-compliance, the letter demands an immediate internal audit and structural remediation. Submitting this grievance is an essential step for exhausting administrative remedies before escalating the dispute to federal regulators or pursuing litigation to recover trapped capital and consequential damages caused by operational negligence.

What should be included in a grievance letter for a failed wire transfer?

A formal grievance letter should include your full name, account number, the transaction reference number (IMAD/OMAD), the exact date and amount of the transfer, and a clear description of the processing error or delay.

How long does a bank have to resolve a disputed wire transfer?

Under federal regulations like Regulation E, banks typically have 10 to 45 business days to investigate an error; however, for international wire transfers, the initial response to a formal grievance must often occur within 30 days of the report.

Can I claim a refund for fees if my wire transfer was not processed?

Yes, if the wire transfer failed due to a banking error or system failure, you are entitled to a full refund of the principal amount plus any transaction fees and taxes charged by the financial institution.

What is the most common reason for a wire transfer to fail?

Most wire transfers fail due to incorrect recipient information (such as an invalid IBAN or SWIFT code), insufficient funds to cover the transfer and fees, or a mismatch in the intermediary bank routing instructions.

What legal rights do I have if a bank loses my wire transfer?

Consumers are protected by the Electronic Fund Transfer Act (EFTA) and CFPB Remittance Rules, which require banks to investigate errors, provide status updates, and potentially provide compensation for financial losses caused by negligence.

Comments