If you suspect errors in your repayment schedule, a formal Grievance Letter for Miscalculation of Loan Amortization is essential to protect your finances. Inaccurate interest calculations or misapplied payments can lead to significant overcharging. This guide explains how to identify accounting discrepancies and demand a professional audit from your lender. To simplify the process, below are some ready to use templates.

Image cover: Loan Amortization Error: Formal Grievance Letter Templates and Dispute Samples

Letter Samples List

- Grievance Letter for Incorrect Interest Rate Application on Loan Amortization

- Grievance Letter for Uncredited Payment Causing Loan Amortization Miscalculation

- Grievance Letter for Miscalculation of Principal Balance in Amortization Schedule

- Grievance Letter for Improper Adjustment of Variable Rate Loan Amortization

- Grievance Letter for Erroneous Fee Inclusion in Amortization Calculation

- Grievance Letter for Incorrect Loan Term Length in Amortization Schedule

- Grievance Letter for Misapplied Extra Principal Payment in Amortization Statement

- Grievance Letter for Escrow Miscalculation Affecting Monthly Amortization

- Grievance Letter for Compound Interest Miscalculation on Loan Amortization

- Grievance Letter for System Error Causing Loan Amortization Miscalculation

- Grievance Letter for Refinance Amortization Miscalculation After Loan Restructuring

- Grievance Letter for Overcharged Amortization Installment Due to Bank Error

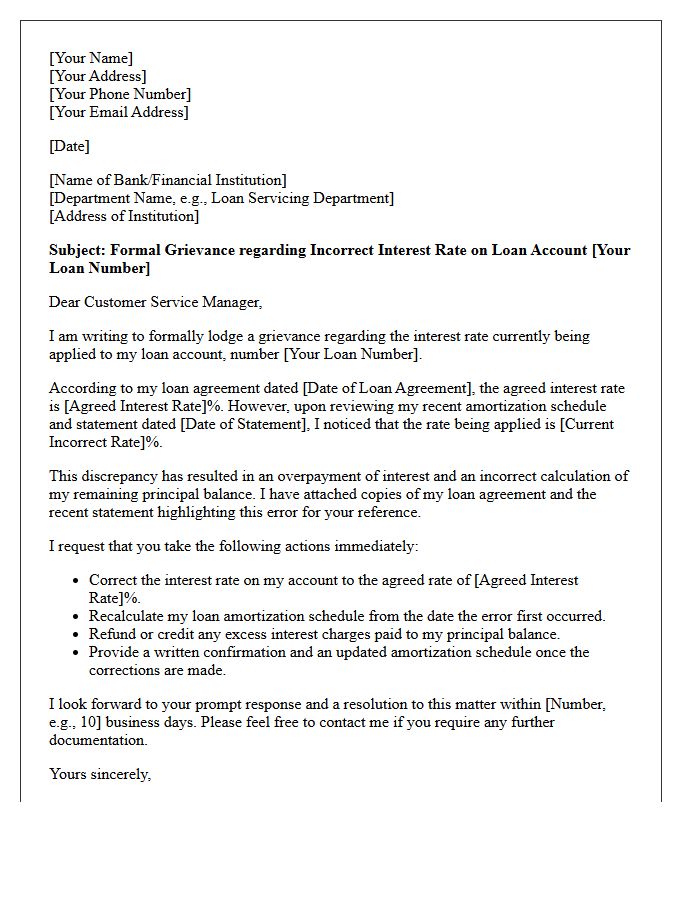

Grievance Letter for Incorrect Interest Rate Application on Loan Amortization

A formal grievance letter is essential for disputing an incorrect interest rate applied to your loan amortization. You must clearly state your account details, identify the discrepancy between the agreed contract and the current charges, and request a formal recalculation. Providing documented evidence, such as original loan agreements or payment schedules, strengthens your claim. This document serves as a legal record, ensuring the financial institution acknowledges the error and adjusts the amortization schedule to reflect the accurate rate, preventing long-term financial loss and ensuring fair debt servicing.

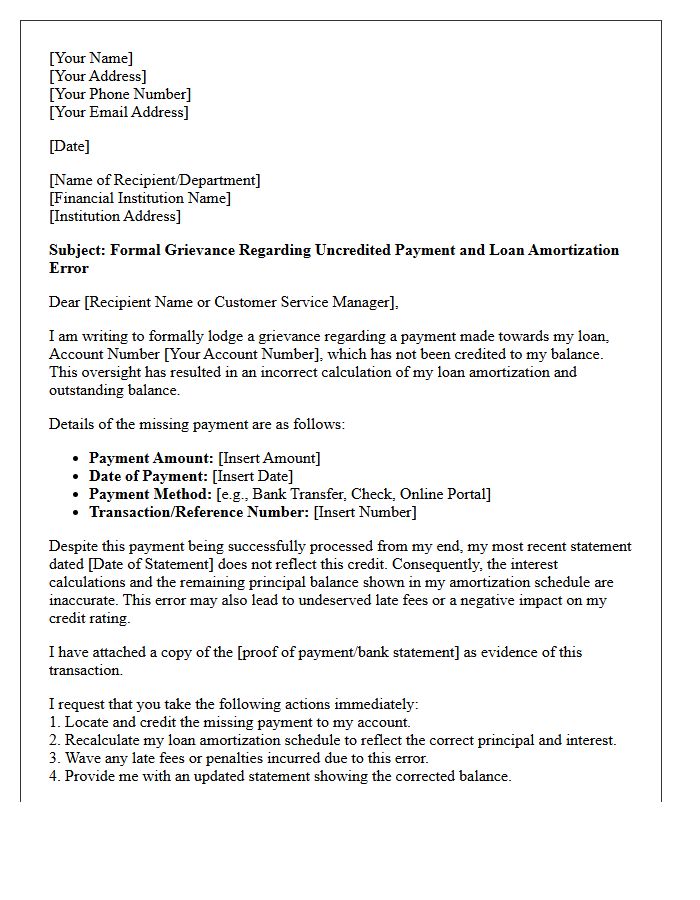

Grievance Letter for Uncredited Payment Causing Loan Amortization Miscalculation

When sending a grievance letter for an uncredited payment, you must provide proof of transaction, such as a bank receipt or reference number. Clearly state that the missing credit has caused a loan amortization miscalculation, leading to incorrect interest charges or penalties. Formally request an immediate account reconciliation to rectify the balance and update your payment schedule. Ensure you specify the exact date and amount of the payment to facilitate a swift correction and prevent further financial discrepancies or negative impacts on your credit score.

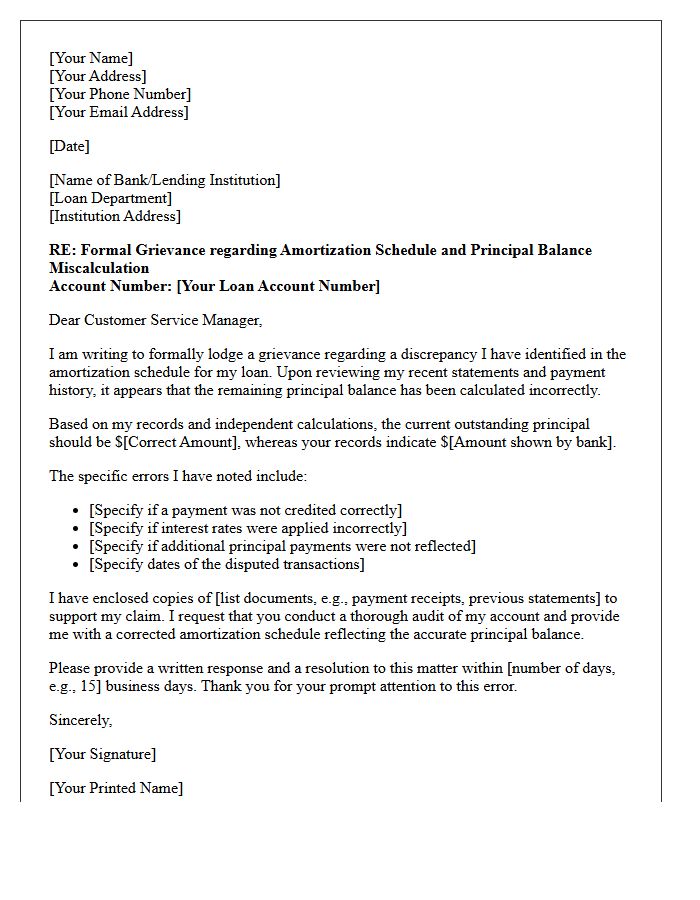

Grievance Letter for Miscalculation of Principal Balance in Amortization Schedule

A formal grievance letter for miscalculated principal balances addresses errors in loan tracking. It is essential to clearly identify the discrepancy between your records and the lender's amortization schedule. Explicitly request a detailed recalculation and provide evidence of past payments to ensure your equity is correctly reported. This document serves as legal notice to protect your consumer rights and rectify financial inaccuracies that could lead to overpayment or extended loan terms. Timely submission is critical to preventing compounded interest errors and maintaining accurate credit reporting records.

Grievance Letter for Improper Adjustment of Variable Rate Loan Amortization

A grievance letter for improper variable rate loan amortization addresses calculation errors following interest rate changes. It is crucial to formally dispute discrepancies where monthly payments fail to reflect current market benchmarks or contract terms. Clearly state your account details, identify the specific miscalculation, and request a detailed payment breakdown. This legal document serves as a protective record, compelling lenders to rectify incorrect principal balances and ensure your amortization schedule aligns with the legal loan agreement, preventing long-term financial loss due to administrative oversight.

Grievance Letter for Erroneous Fee Inclusion in Amortization Calculation

A formal grievance letter serves as essential documentation to contest an erroneous fee integrated into your amortization schedule. This written notice formally requests a recalculation of your payment structure to ensure accuracy and financial transparency. It is crucial to clearly identify the disputed charge, provide supporting evidence, and demand an immediate adjustment to the principal and interest breakdown. Sending this letter via certified mail creates a legal paper trail, protecting your consumer rights and preventing long-term financial loss due to unauthorized billing errors by the lending institution.

Grievance Letter for Incorrect Loan Term Length in Amortization Schedule

A formal grievance letter is essential when you identify a discrepancy between your signed contract and the amortization schedule. Clearly state that the incorrect loan term violates your original agreement, as an extended duration leads to excessive interest charges. Demand an immediate correction to the repayment timeline to ensure financial accuracy. Attach copies of your loan documents as evidence to support your claim. This written record protects your consumer rights and serves as critical documentation should you need to escalate the dispute to regulatory authorities or legal counsel.

Grievance Letter for Misapplied Extra Principal Payment in Amortization Statement

A grievance letter for a misapplied extra principal payment is essential to correct errors in your amortization statement. Clearly state the exact payment date, amount, and account number to ensure the lender identifies the discrepancy. Demand a formal recalculation of interest and an updated schedule to reflect the reduced principal balance. This written notice serves as a legal record, protecting your equity and ensuring loan accuracy. Always request a written confirmation once the adjustment is finalized to verify that your additional funds were applied correctly toward the principal rather than future interest.

Grievance Letter for Escrow Miscalculation Affecting Monthly Amortization

When drafting a grievance letter for an escrow miscalculation, clearly identify the specific discrepancy affecting your monthly amortization. Formally request a detailed escrow analysis to rectify errors in tax or insurance projections. Ensure you include your loan number, evidence of overpayment, and a demand for a recalculation. Under the Real Estate Settlement Procedures Act (RESPA), lenders must investigate and respond to your Qualified Written Request within specific timelines to prevent financial strain and ensure accurate mortgage billing.

Grievance Letter for Compound Interest Miscalculation on Loan Amortization

A formal grievance letter is essential when you identify a compound interest miscalculation in your loan amortization. It serves as a legal notice to your lender, demanding a thorough audit of the repayment schedule. You must clearly highlight discrepancies between your contract terms and the applied interest rates. Providing evidence of the error ensures the bank corrects the principal balance and adjusts future payments. This document protects your consumer rights and provides a paper trail for potential regulatory complaints or legal action to recover overcharged funds.

Grievance Letter for System Error Causing Loan Amortization Miscalculation

When drafting a grievance letter for a loan amortization miscalculation caused by a system error, clearly identify the specific discrepancy between your contract and the current billing. Provide your account number and attach evidence, such as payment receipts or original loan schedules. Explicitly state that a technical glitch has led to incorrect interest charges or principal reduction. Formally request an immediate recalculation and a written explanation of the correction. This creates a documented paper trail essential for protecting your consumer rights and ensuring financial accuracy.

Grievance Letter for Refinance Amortization Miscalculation After Loan Restructuring

A grievance letter for refinance amortization miscalculations is essential when your lender applies incorrect terms after a loan restructuring. Formally notify the servicer to audit your payment schedule, ensuring the interest rate and principal balance align with your signed agreement. Precise documentation of the discrepancy prevents long-term financial loss from overpaid interest. Demand a corrected amortization schedule and an account adjustment to rectify equity errors. Sending this via certified mail establishes a legal paper trail, protecting your rights under consumer protection laws if the lender fails to resolve the accounting error promptly.

Grievance Letter for Overcharged Amortization Installment Due to Bank Error

A formal grievance letter serves as legal evidence when challenging an overcharged amortization installment caused by a bank error. It is essential to clearly state the discrepancy between the agreed schedule and the actual deduction. Include your account details, specific transaction dates, and supporting loan documents. Request an immediate rectification of the balance and a refund of any excess interest or penalties incurred. Sending this via registered mail ensures a paper trail, protecting your consumer rights and maintaining an accurate credit history during the dispute resolution process.

What should I include in a grievance letter for a loan amortization miscalculation?

Your letter should include your full name, loan account number, a clear description of the perceived error, copies of supporting payment records, and a formal request for a corrected amortization schedule.

How do I prove that my loan provider miscalculated my interest?

To prove a miscalculation, compare your bank's statement against your original promissory note. Use an independent amortization calculator to verify if the principal reduction and interest charges align with your agreed-upon interest rate and payment frequency.

What is the legal timeframe for a bank to respond to a loan grievance?

Most jurisdictions and banking regulations require lenders to acknowledge receipt of a formal grievance within 5 to 10 business days and provide a substantive written resolution or update within 30 days.

Can a miscalculation in loan amortization affect my credit score?

Yes, if a miscalculation results in the lender incorrectly reporting a late payment or an outstanding balance, it can negatively impact your credit score. Filing a formal grievance allows you to dispute these inaccuracies with credit bureaus.

What happens if the bank refuses to correct my amortization schedule?

If the lender denies the error after you have submitted a formal grievance, you can escalate the matter to your national financial ombudsman, a consumer protection agency, or seek legal counsel for a breach of contract.

Comments