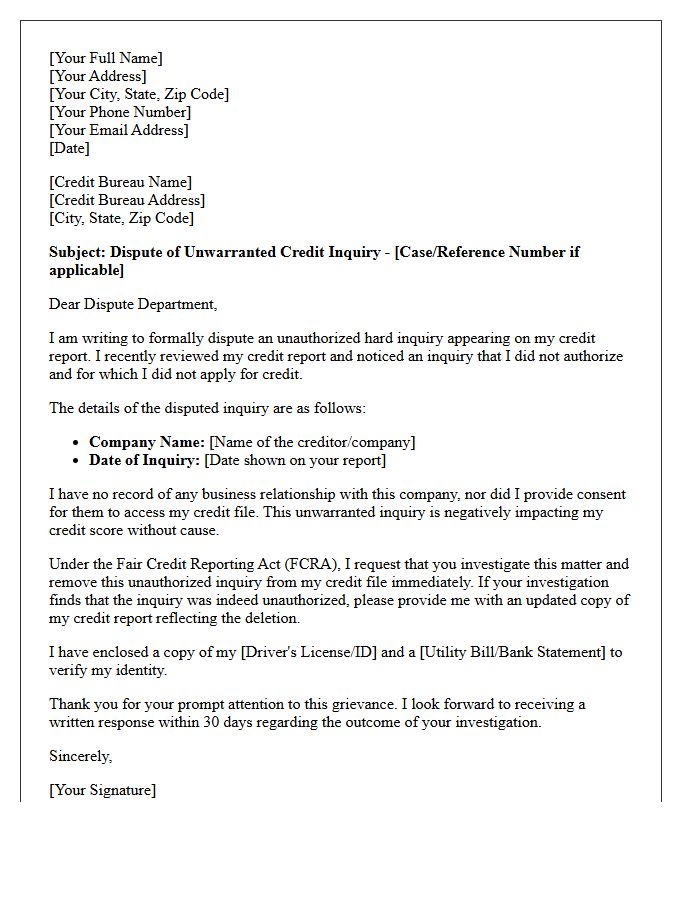

If an unauthorized credit check has negatively impacted your financial standing, you must take action. A formal Grievance Letter for Unwarranted Credit Score Inquiry is the most effective tool to dispute inaccuracies and demand the removal of "hard pulls" from your report. Protecting your credit score ensures better loan terms and financial health. To help you begin, below are some ready to use templates.

Image cover: Professional Templates to Dispute Unauthorized Hard Credit Inquiries

Letter Samples List

- Grievance Letter for Unauthorized Retail Bank Credit Inquiry

- Formal Letter of Complaint Regarding Unwarranted Hard Credit Pull

- Dispute Letter for Unapproved Credit Bureau Inquiry by Bank

- Grievance Letter Addressing Unwarranted Mortgage Credit Check

- Notice Letter of Unauthorized Credit Score Access by Financial Institution

- Demand Letter for Removal of Unwarranted Banking Credit Inquiry

- Letter of Grievance for Unconsented Auto Loan Credit Pull

- Bank Grievance Letter Concerning Fraudulent Credit Report Inquiry

- Official Letter Disputing Unwarranted Credit Card Application Inquiry

- Letter of Objection to Unauthorized Bank Credit Score Inquiry

- Grievance Letter for Unjustified Commercial Loan Credit Check

- Consumer Grievance Letter Requesting Deletion of Unwarranted Credit Inquiry

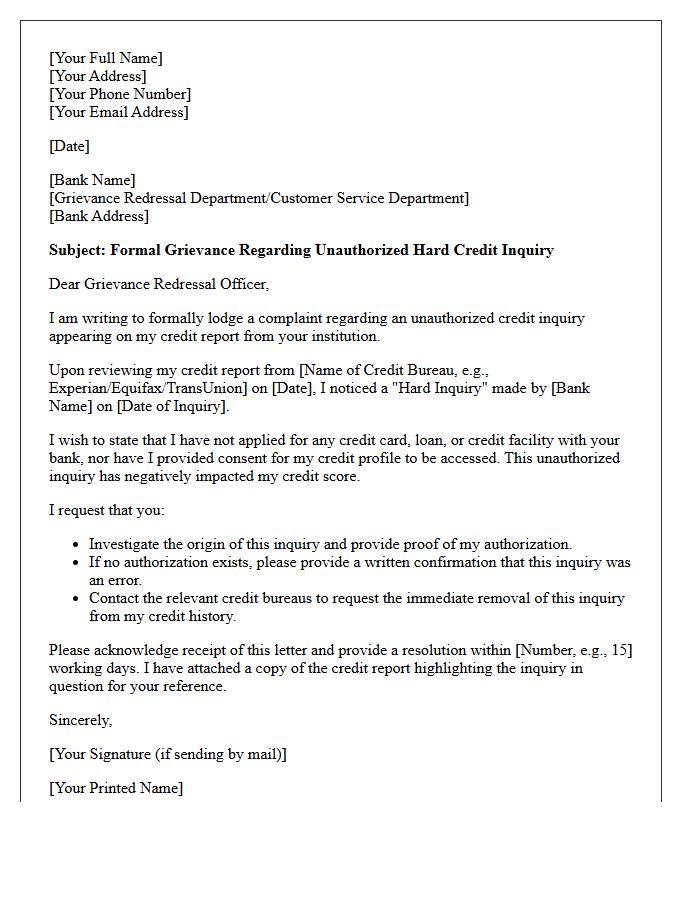

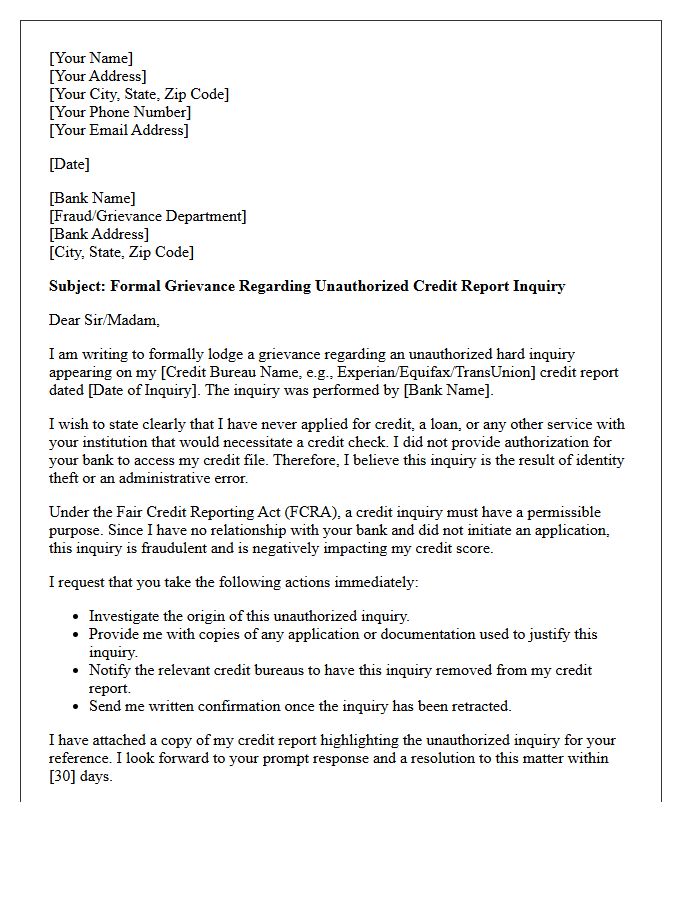

Grievance Letter for Unauthorized Retail Bank Credit Inquiry

When drafting a grievance letter for an unauthorized credit inquiry, you must formally dispute the entry with both the retail bank and credit bureaus. Clearly state that you did not provide explicit consent for the hard pull, which negatively impacts your credit score. Demand a formal investigation and the immediate removal of the inaccurate record under the Fair Credit Reporting Act. Include your personal details, the specific date of the inquiry, and a request for written confirmation once the correction is finalized to ensure your financial profile remains protected.

Formal Letter of Complaint Regarding Unwarranted Hard Credit Pull

If an unauthorized inquiry appears on your report, you must send a Formal Letter of Complaint Regarding Unwarranted Hard Credit Pull to the creditor and credit bureaus. Clearly state that you did not provide permissible purpose for the credit check. Demand the immediate removal of the inquiry to protect your credit score from unnecessary point deductions. Include your identifying details and a copy of your credit report highlighting the error. Under the Fair Credit Reporting Act (FCRA), reporting agencies are legally obligated to investigate and delete inaccurate or unverified data.

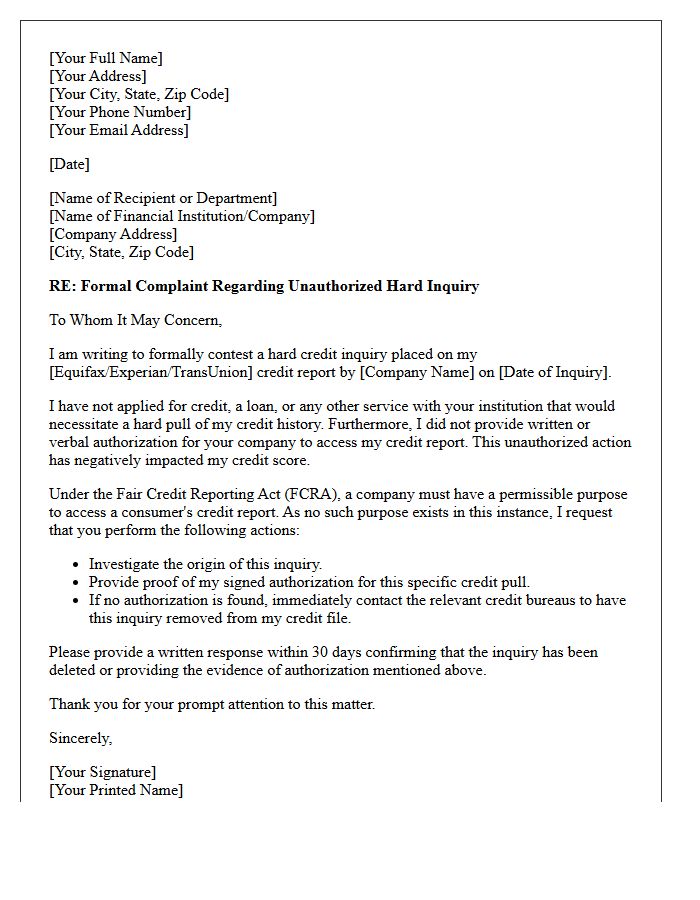

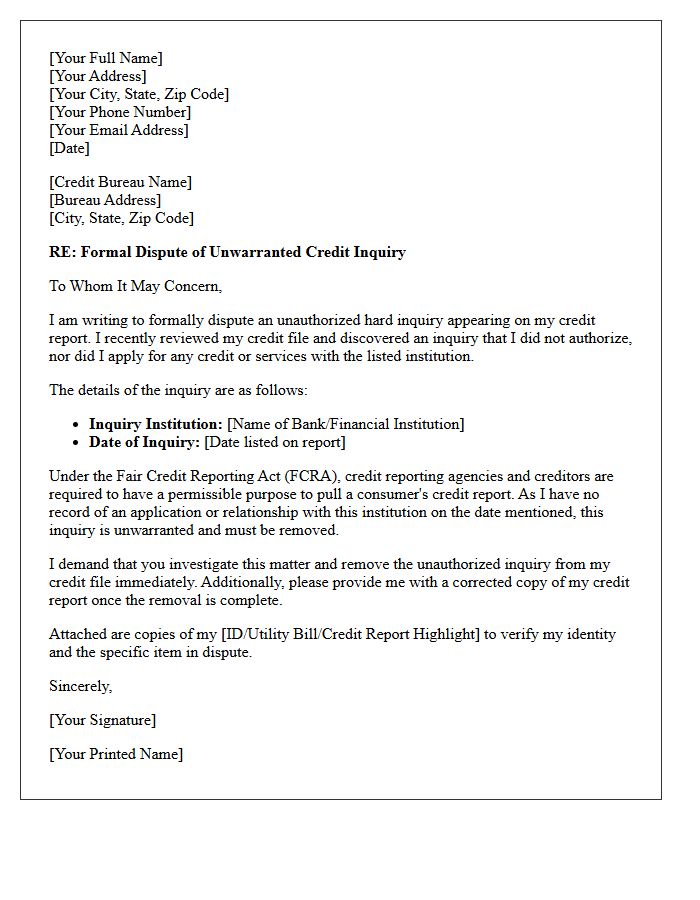

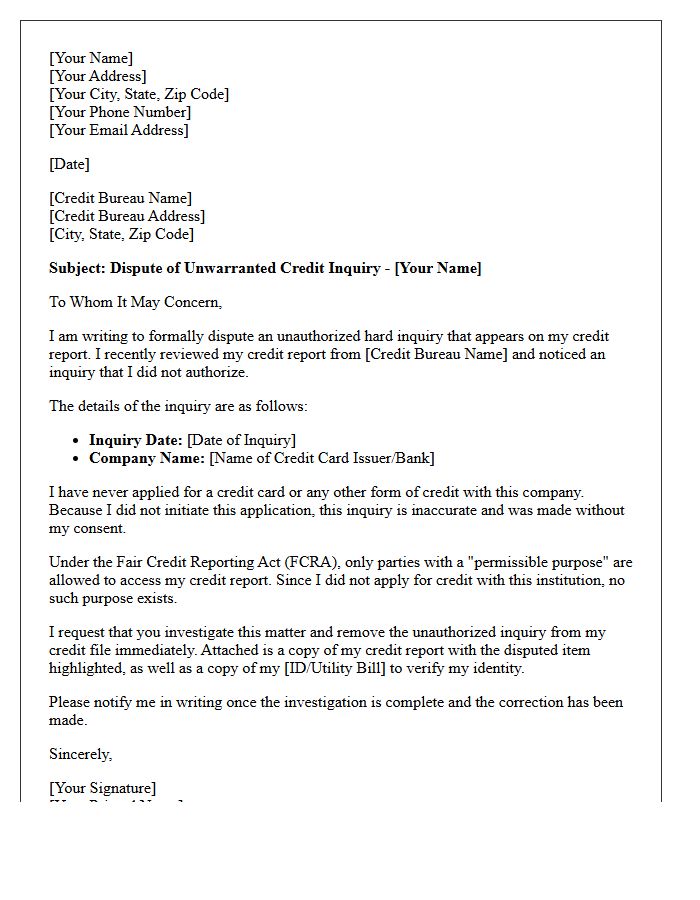

Dispute Letter for Unapproved Credit Bureau Inquiry by Bank

Filing a dispute letter is essential when a bank performs an unapproved hard inquiry on your credit report. These unauthorized checks can lower your credit score and remain visible for two years. Under the Fair Credit Reporting Act (FCRA), consumers have the right to challenge any inquiry made without permissible purpose. You must demand that the credit bureau remove the inquiry if the financial institution cannot provide written proof of your authorization. Promptly addressing these errors protects your creditworthiness and helps prevent potential identity theft or administrative mistakes by lenders.

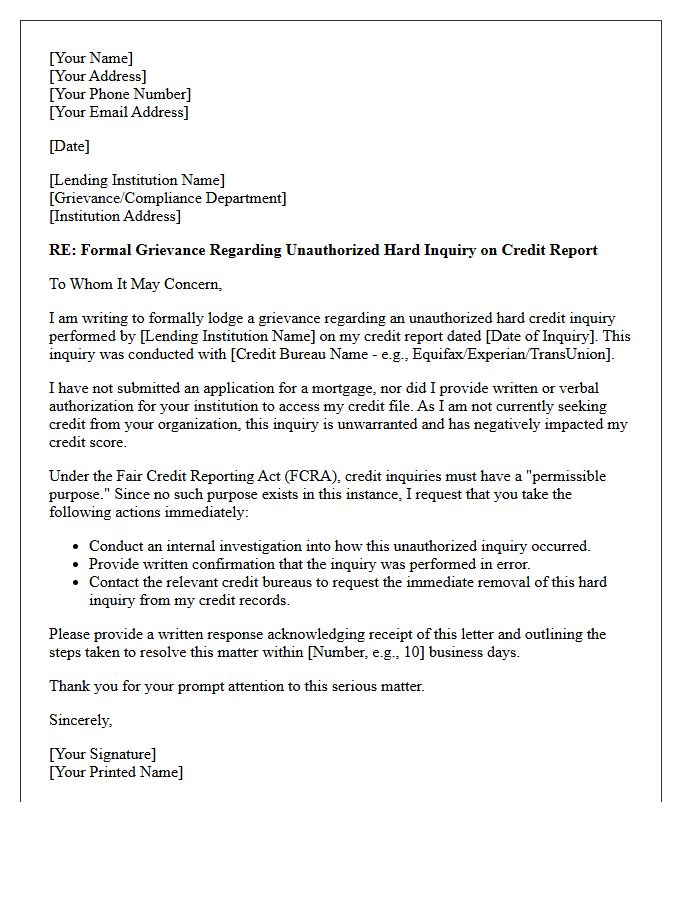

Grievance Letter Addressing Unwarranted Mortgage Credit Check

Sending a formal grievance letter regarding an unwarranted mortgage credit check is essential to protect your financial reputation. Unauthorized inquiries can lower your credit score and impact future loan eligibility. Your letter should clearly state that you did not provide explicit consent for the hard pull, demanding an immediate investigation and removal of the inquiry from all credit bureau reports. Under the Fair Credit Reporting Act, lenders must have a permissible purpose to access your data. Documenting this dispute ensures a paper trail to restore your credit standing effectively.

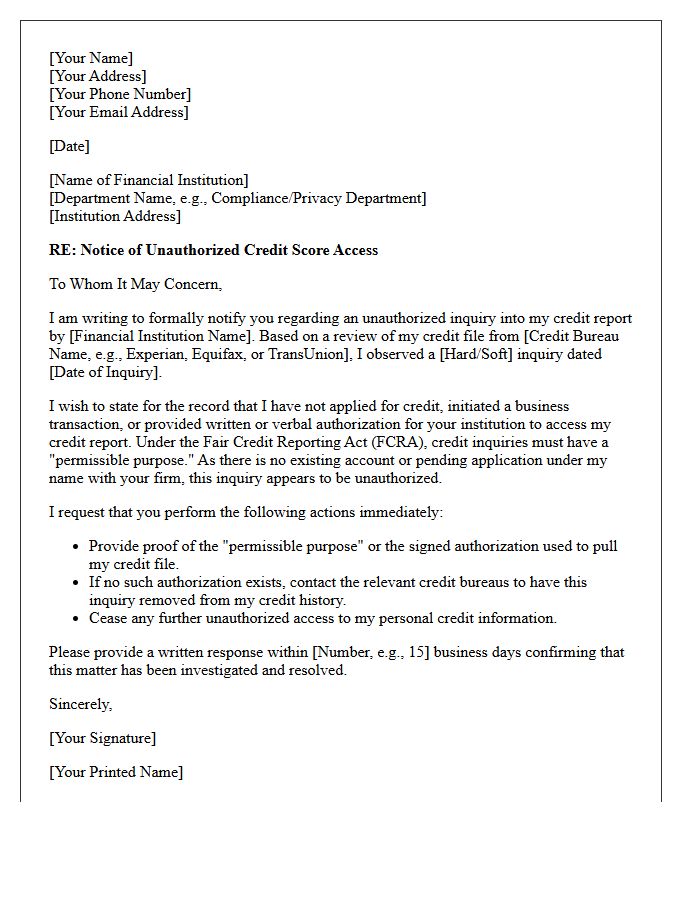

Notice Letter of Unauthorized Credit Score Access by Financial Institution

If you receive a Notice of Unauthorized Credit Score Access, it means a financial institution viewed your credit report without a permissible purpose. This breach of privacy requires immediate attention under the Fair Credit Reporting Act (FCRA). You should verify if the access was a clerical error or a sign of potential identity theft. Review your credit reports for suspicious activity, consider placing a security freeze on your files, and contact the institution to demand a formal explanation to protect your financial reputation and sensitive data.

Demand Letter for Removal of Unwarranted Banking Credit Inquiry

A demand letter for the removal of an unwarranted banking credit inquiry is a formal legal request sent to financial institutions or credit bureaus. Its primary purpose is to challenge unauthorized hard pulls that negatively impact your credit score. Under the Fair Credit Reporting Act (FCRA), lenders must have a permissible purpose to access your report. If an inquiry was made without consent or due to error, this document serves as an official notice to dispute the entry and demand its immediate deletion to restore your creditworthiness and protect your financial reputation.

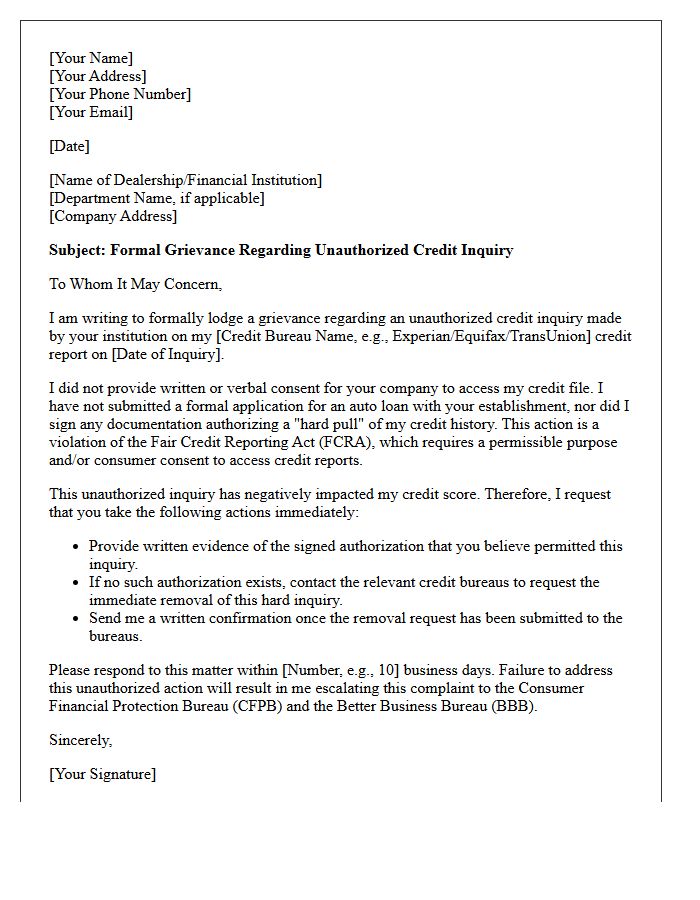

Letter of Grievance for Unconsented Auto Loan Credit Pull

If a lender performs an unauthorized hard credit inquiry for an auto loan, you must submit a formal Letter of Grievance to dispute the error. This document notifies the financial institution and credit bureaus of a Fair Credit Reporting Act (FCRA) violation. Clearly state that you did not provide written consent for the pull and demand the immediate removal of the inquiry from your credit profile. Correcting these unauthorized marks is essential to protecting your credit score and ensuring your financial report remains accurate and compliant with federal consumer protection laws.

Bank Grievance Letter Concerning Fraudulent Credit Report Inquiry

A formal bank grievance letter is essential for disputing an unauthorized credit inquiry that negatively impacts your credit score. You must clearly state that the hard pull occurred without your consent and demand its immediate removal. Attach a copy of your credit report highlighting the error and provide proof of identity to expedite the investigation. Under the Fair Credit Reporting Act, financial institutions are legally obligated to rectify fraudulent reporting. Submitting this dispute in writing creates a vital paper trail to protect your financial reputation and restore your creditworthiness.

Official Letter Disputing Unwarranted Credit Card Application Inquiry

Submitting an official credit dispute letter is essential when you identify an unauthorized hard inquiry on your credit report. This formal document notifies credit bureaus that you did not apply for the card, protecting your credit score from unnecessary dips. Clearly state that the application was unwarranted and request immediate removal to prevent potential identity theft. Providing supporting documentation ensures the bureau investigates and corrects the error promptly. Acting quickly maintains your financial reputation and ensures your credit history remains accurate and secure against fraudulent activity.

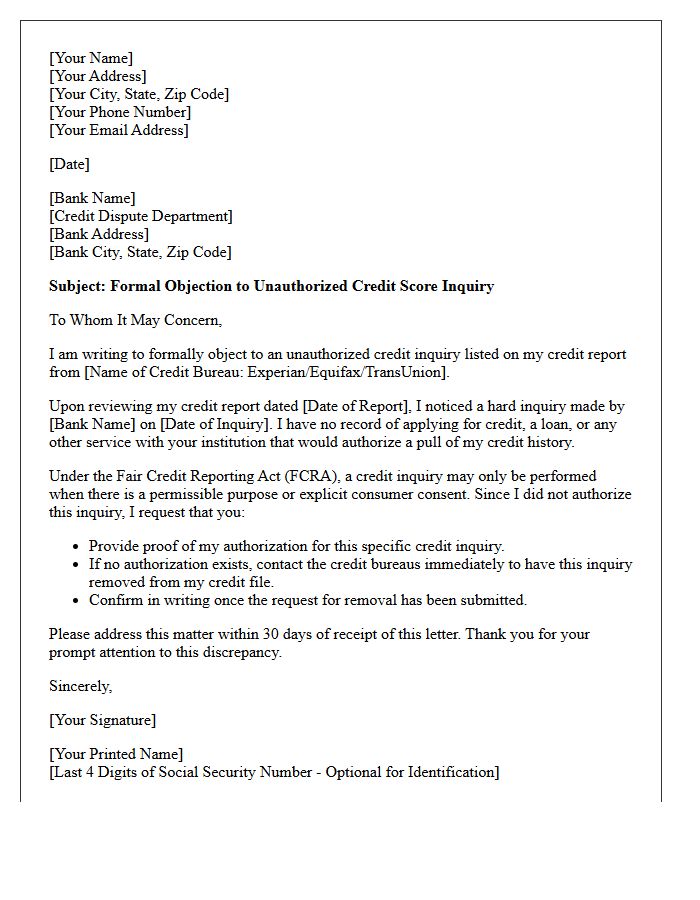

Letter of Objection to Unauthorized Bank Credit Score Inquiry

A letter of objection is a formal document used to dispute an unauthorized credit inquiry initiated by a financial institution. Under the Fair Credit Reporting Act, banks must have a permissible purpose before accessing your credit file. If you identify a hard pull you did not consent to, sending this letter forces the bank to provide proof of authorization or request its removal from your report. Promptly addressing these errors is essential because excessive inquiries can lower your credit score and impact future loan eligibility.

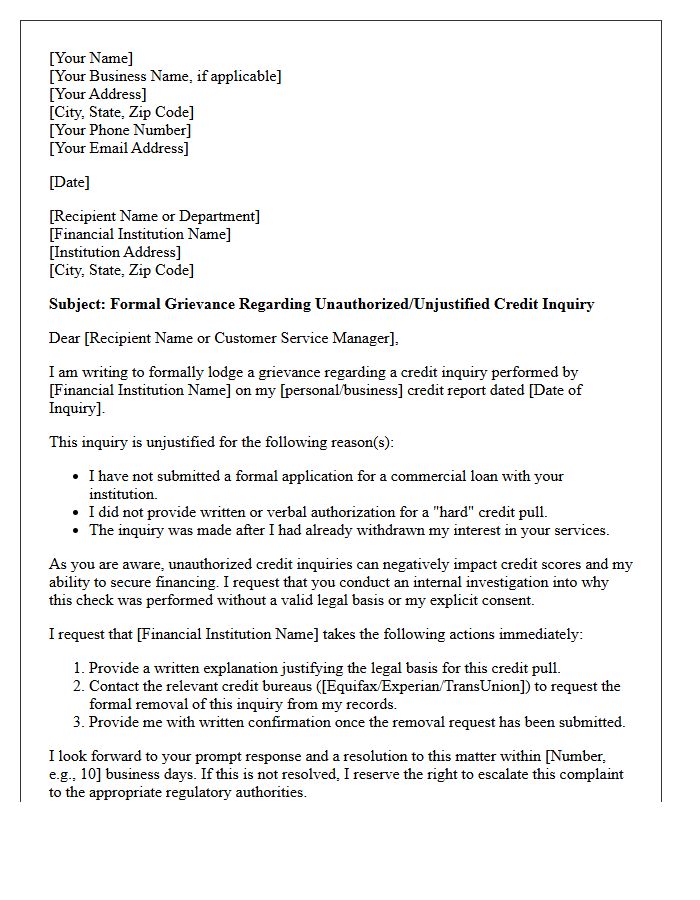

Grievance Letter for Unjustified Commercial Loan Credit Check

An unjustified credit inquiry can negatively impact your business credit score. When drafting a grievance letter, clearly state that the hard pull was unauthorized or performed without a legitimate permissible purpose. Demand the immediate removal of the inquiry from your credit report by citing a breach of the Fair Credit Reporting Act. Include specific details like the date of the check and the financial institution involved. This formal written protest serves as essential evidence for dispute resolution and protecting your company's future borrowing capacity.

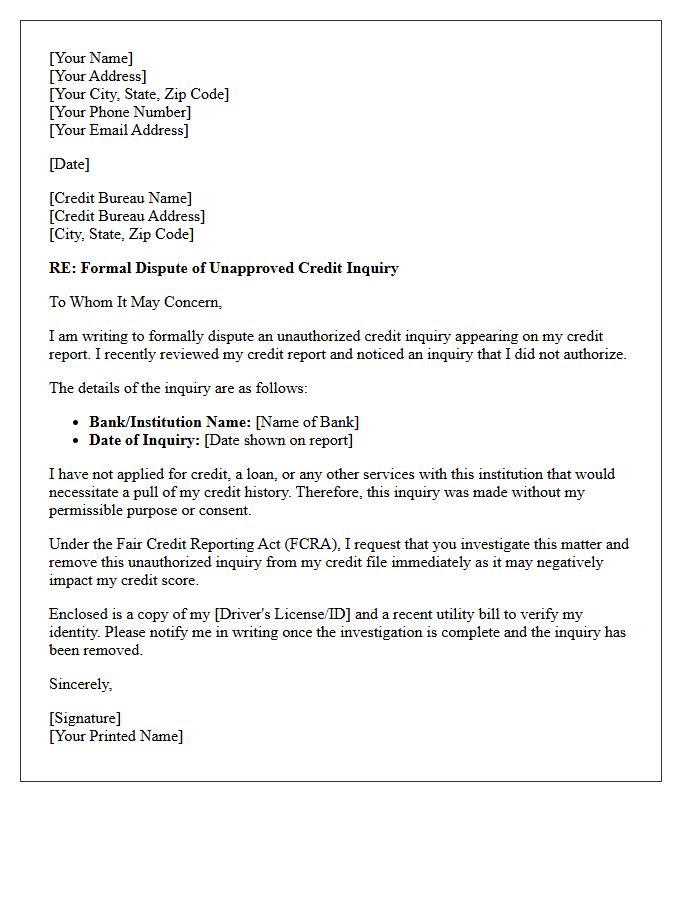

Consumer Grievance Letter Requesting Deletion of Unwarranted Credit Inquiry

A formal consumer grievance letter is essential to challenge an unauthorized credit inquiry that negatively impacts your credit score. You must clearly identify the unwarranted hard pull, provide the date of the occurrence, and state that no application for credit was initiated. Under the Fair Credit Reporting Act, bureaus are legally required to verify the legitimacy of all entries. Explicitly requesting the permanent deletion of the record helps restore your creditworthiness and protects against potential identity theft. Always include supporting documentation to expedite the investigation process.

What is a grievance letter for an unwarranted credit score inquiry?

A grievance letter for an unwarranted credit score inquiry is a formal written dispute sent to a creditor or credit bureau to challenge a "hard pull" on your credit report that was performed without your explicit consent or a permissible legal purpose.

How do I dispute an unauthorized hard inquiry on my credit report?

To dispute an unauthorized inquiry, you should mail a formal grievance letter to the institution that performed the search and the credit bureaus (Equifax, Experian, or TransUnion) requesting proof of authorization or the immediate removal of the inquiry from your file.

What information should be included in a credit inquiry dispute letter?

Your letter should include your full legal name, current address, the name of the company that performed the unauthorized inquiry, the specific date it occurred, and a clear statement asserting that you did not apply for credit or authorize the check.

Can an unwarranted credit inquiry be removed from my credit report?

Yes, if a creditor cannot provide documented proof that you authorized the credit check or that they had a valid legal reason under the Fair Credit Reporting Act (FCRA) to access your report, they are legally required to instruct the credit bureaus to remove the inquiry.

How long does a creditor have to respond to a grievance letter regarding a credit inquiry?

Under the Fair Credit Reporting Act (FCRA), credit bureaus and reporting entities generally have 30 to 45 days to investigate your dispute and provide a resolution regarding the unwarranted inquiry.

Comments