Dealing with negative banking history can be challenging. This guide provides an effective ChexSystems Derogatory Mark Inquiry Response Letter to help you dispute inaccuracies and restore your financial standing. Learn how to communicate formally with reporting agencies to clear your record and regain access to traditional checking accounts. Below are some ready to use templates.

Image cover: Proven Dispute Letter Templates for Removing ChexSystems Derogatory Marks

Letter Samples List

- ChexSystems Inquiry Acknowledgment Letter

- ChexSystems Derogatory Mark Investigation Initiation Letter

- Verified Derogatory Mark Retention Letter

- Erroneous ChexSystems Mark Removal Letter

- ChexSystems Account Update and Modification Letter

- Additional Documentation Request Letter

- Suspected Account Fraud Investigation Letter

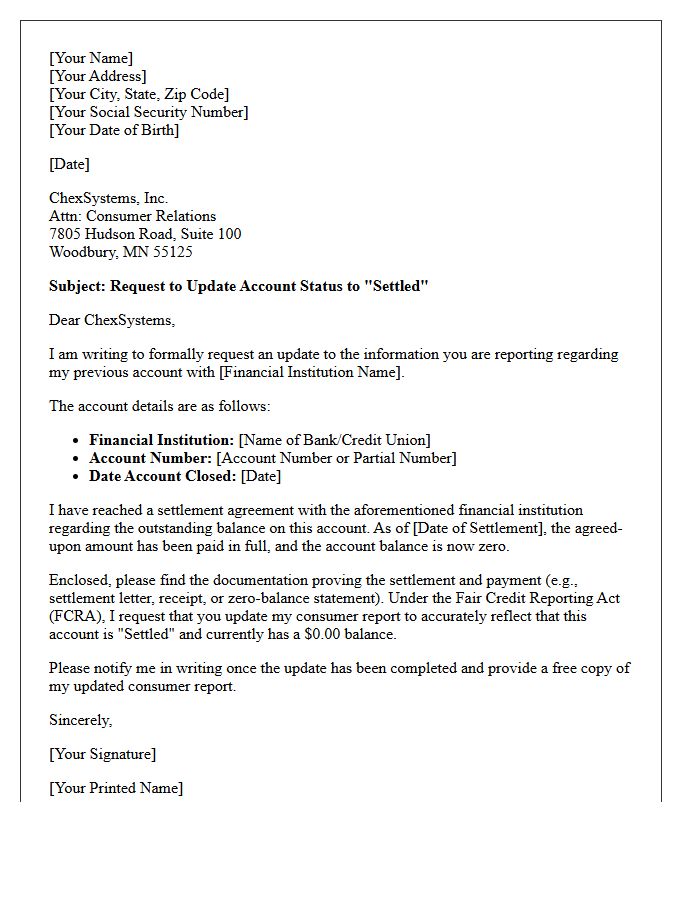

- Settled Account Balance ChexSystems Update Letter

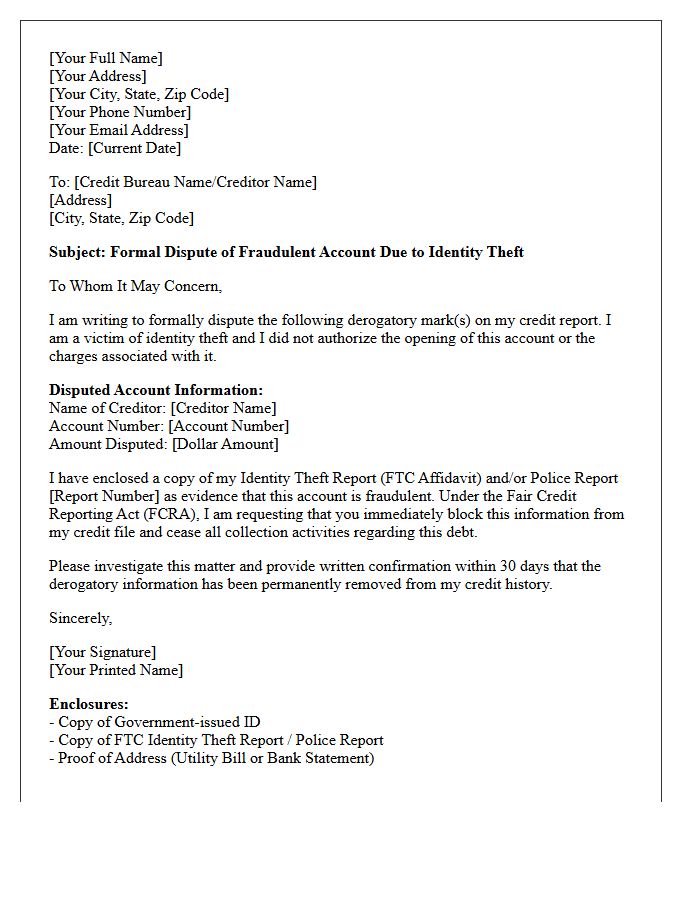

- Identity Theft Derogatory Mark Resolution Letter

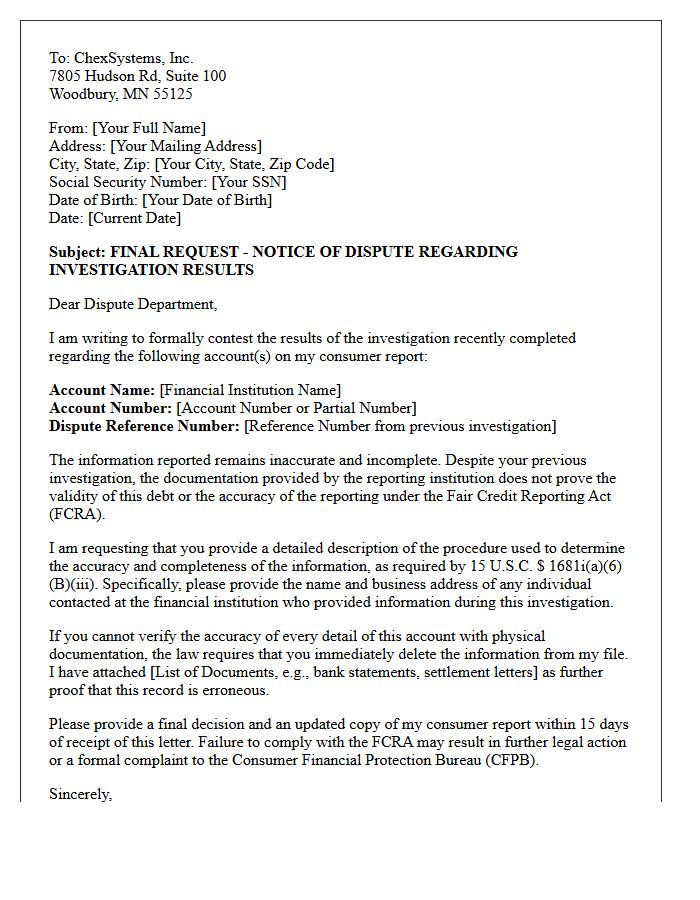

- ChexSystems Dispute Final Decision Letter

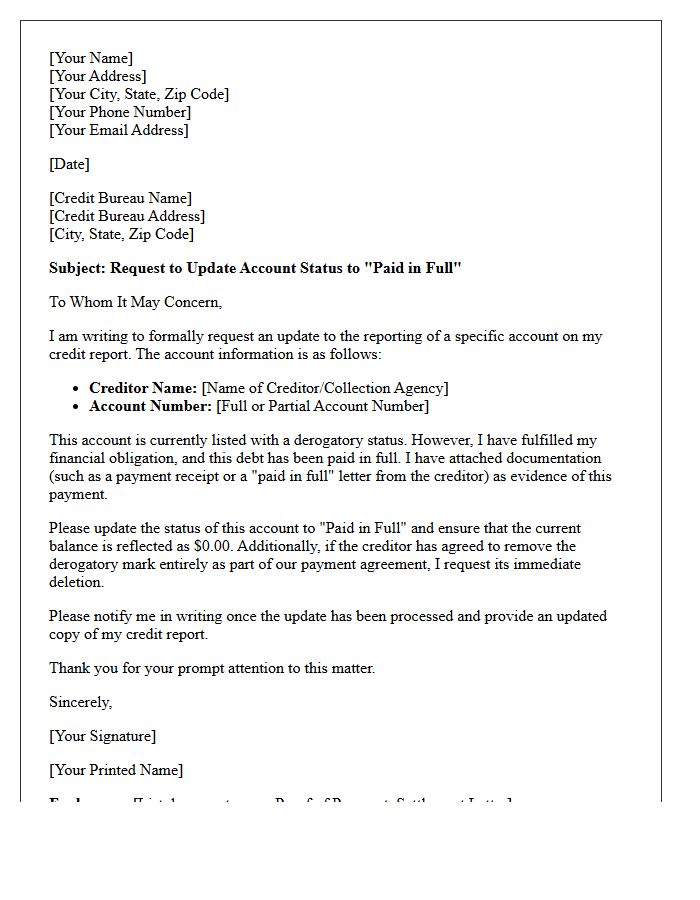

- Paid in Full Derogatory Mark Update Letter

- Bank Error Derogatory Mark Deletion Letter

- Incomplete Inquiry Rejection Letter

- Overdraft Fee Dispute Resolution Letter

- Frivolous ChexSystems Dispute Notification Letter

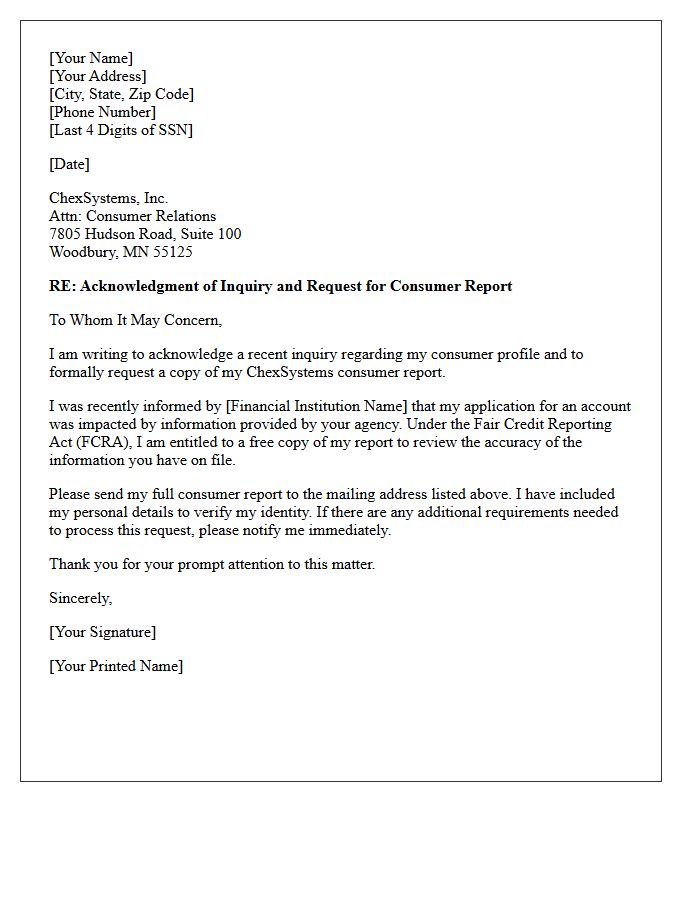

ChexSystems Inquiry Acknowledgment Letter

A ChexSystems Inquiry Acknowledgment Letter confirms that a financial institution has requested your consumer report to evaluate an application for a new account. This document acts as a formal notification of recent activity on your file. It is essential to review this letter to ensure the inquiry was authorized by you, as unauthorized requests may indicate identity theft. If the information is incorrect, you have the right to dispute the inquiry directly with ChexSystems to maintain an accurate banking history and protect your future financial accessibility.

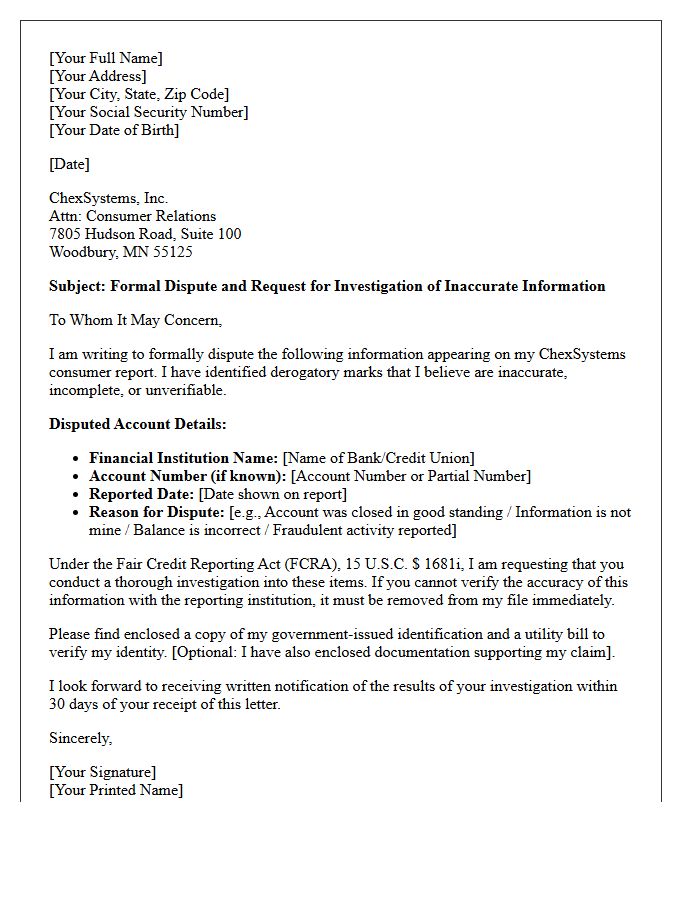

ChexSystems Derogatory Mark Investigation Initiation Letter

A ChexSystems Derogatory Mark Investigation Initiation Letter is a formal dispute sent to credit reporting agencies to challenge banking inaccuracies. This document mandates a reinvestigation of negative entries, such as unpaid overdrafts or suspected fraud, that prevent you from opening new accounts. Under the Fair Credit Reporting Act, agencies must verify the data's accuracy within thirty days. Using this letter is a critical step to restoring your financial reputation and regaining access to standard banking services by ensuring your consumer report reflects strictly verified information.

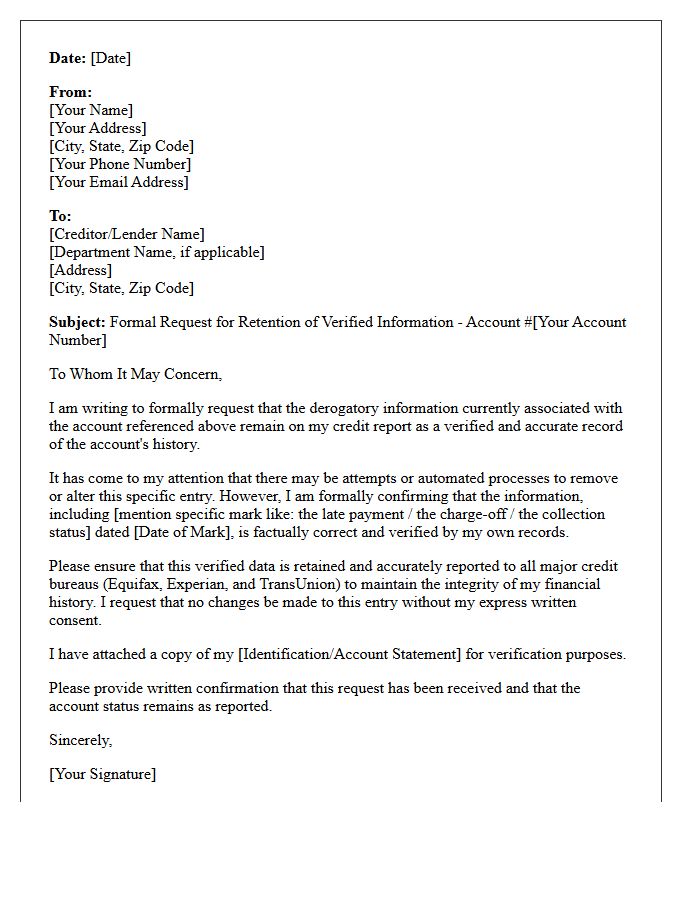

Verified Derogatory Mark Retention Letter

A Verified Derogatory Mark Retention Letter is a formal notice from a credit bureau confirming that negative information, such as late payments or collections, will remain on your report. This occurs after a dispute investigation concludes the data is accurate and verifiable by the creditor. Understanding this document is crucial because it signifies that the Fair Credit Reporting Act requirements have been met, meaning the mark will persist until the legal reporting period expires. To improve your score, you must focus on future positive credit behavior rather than further basic disputes.

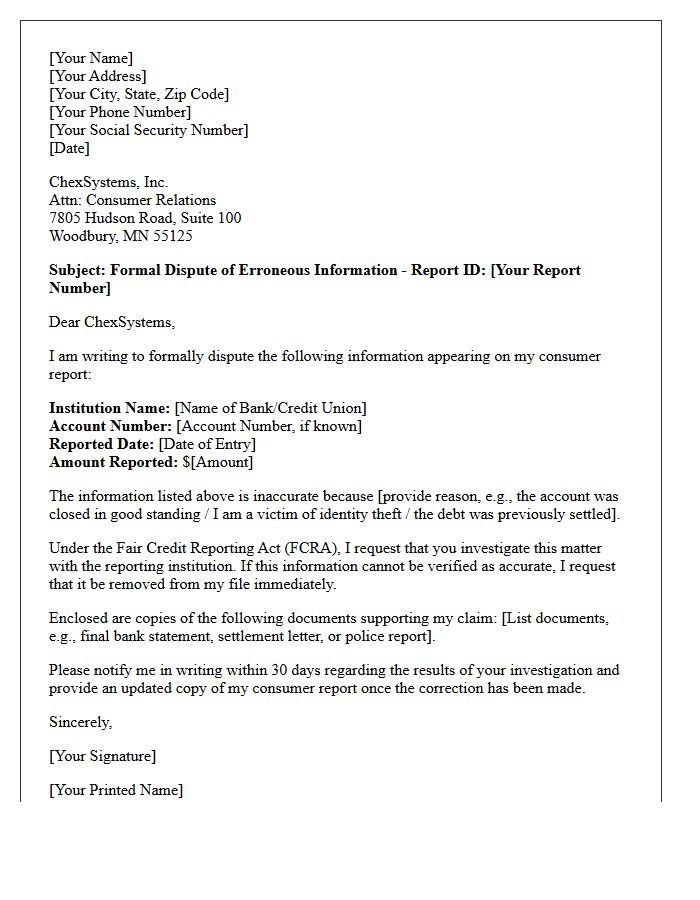

Erroneous ChexSystems Mark Removal Letter

An Erroneous ChexSystems Mark Removal Letter is a formal dispute document used to challenge inaccurate reporting on your consumer banking file. Under the Fair Credit Reporting Act, you have the right to demand that banks and credit bureaus delete unsubstantiated or false negative entries. Sending this letter is the first step toward restoring your banking reputation and regaining the ability to open new checking accounts. Ensure you include evidence of the error and request a complete investigation to clear your name from their database within thirty days.

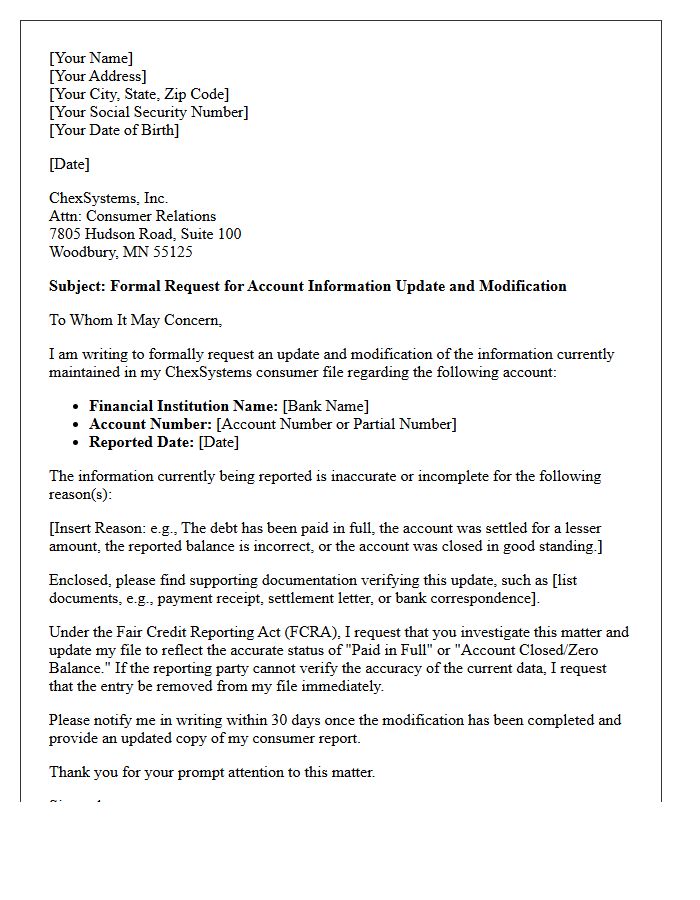

ChexSystems Account Update and Modification Letter

A ChexSystems Account Update and Modification Letter is a formal request used to correct inaccurate data or outdated information in your consumer report. When financial institutions report errors, such as paid debts still showing as outstanding, this letter compels the agency to verify and update your file under the Fair Credit Reporting Act. Ensuring your records are modified is essential for regaining banking eligibility and opening new checking accounts. Always include supporting documentation, like a settlement letter, to ensure the modification is processed quickly and accurately by the reporting agency.

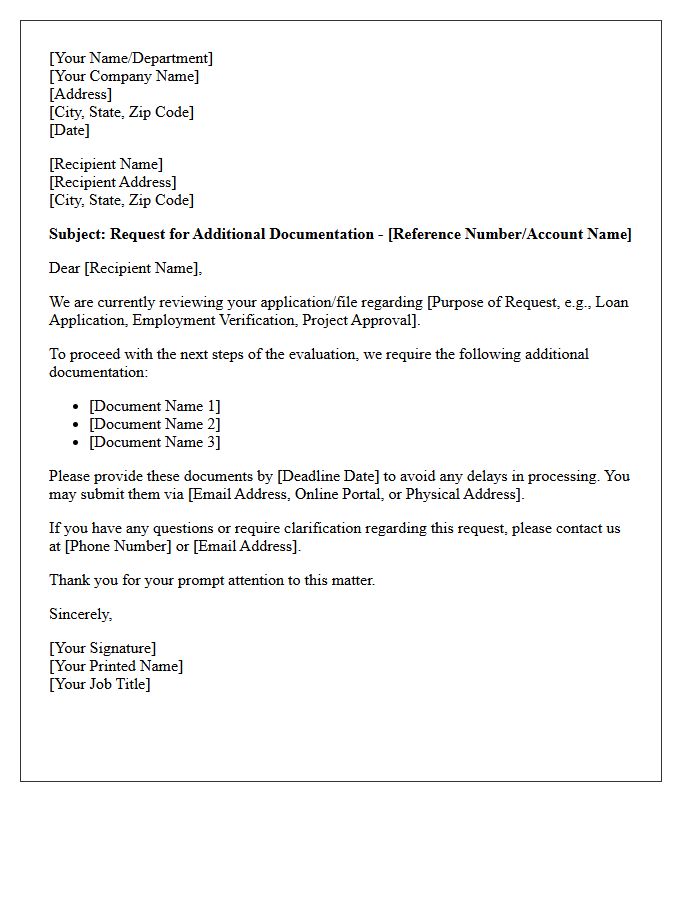

Additional Documentation Request Letter

An Additional Documentation Request (ADR) letter is a formal notification from a Medicare Administrative Contractor or insurance payer seeking further clinical records to support a claim. It is crucial to provide a timely and complete response within the specified deadline, typically 45 days. Failure to submit the requested evidence, such as medical necessity proof or physician signatures, often results in automatic claim denials and financial recoupment. Proper documentation management ensures compliance and protects your organization's revenue cycle from audit-related losses.

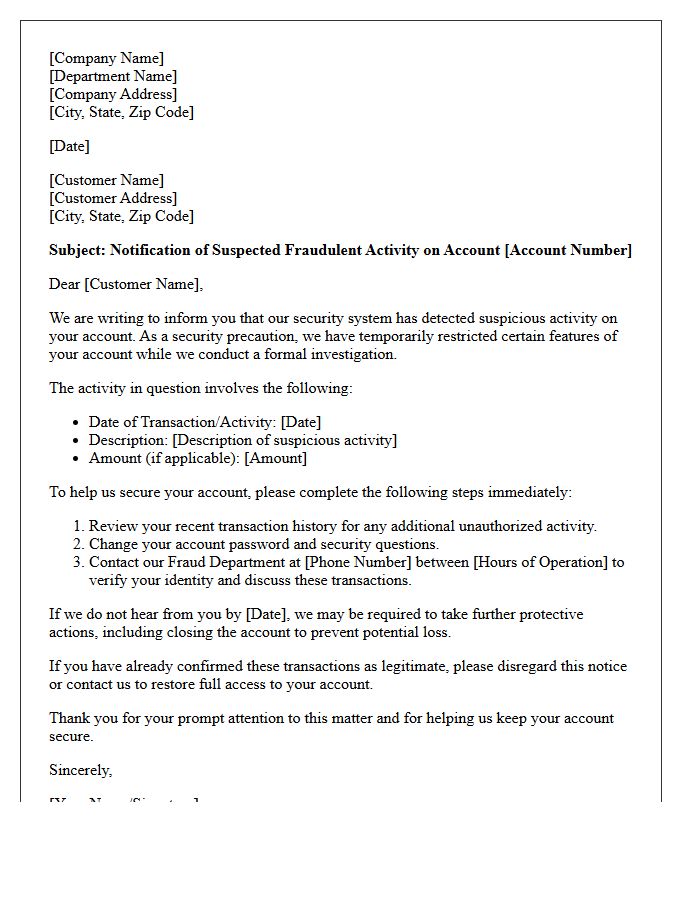

Suspected Account Fraud Investigation Letter

A Suspected Account Fraud Investigation Letter is a formal notification from a financial institution regarding unauthorized activity on your account. It serves to protect your assets by temporarily restricting access while a security review is conducted. Upon receipt, you must verify your identity and confirm specific transactions to resolve the issue. Always contact your bank through official channels to ensure the letter is legitimate and avoid potential phishing scams. Prompt communication is essential to securing your funds and restoring full account functionality after a security breach.

Settled Account Balance ChexSystems Update Letter

A Settled Account Balance ChexSystems Update Letter is a formal request sent to reporting agencies to ensure your banking history accurately reflects a resolved debt. When you settle an account for less than the full amount, banks often fail to update your record promptly. Sending this written dispute along with proof of payment forces ChexSystems to update your status to "settled in full" or "paid." This is a critical step for restoring your financial reputation and regaining the ability to open new checking or savings accounts at major financial institutions.

Identity Theft Derogatory Mark Resolution Letter

An Identity Theft Derogatory Mark Resolution Letter is a formal document sent to credit bureaus to challenge fraudulent accounts caused by stolen information. Under the Fair Credit Reporting Act, you must include a copy of your Identity Theft Report or police affidavit to mandate the removal of inaccurate data. This letter blocks unauthorized entries from appearing on your credit history, ensuring your score recovers. Clearly list every disputed transaction and request a permanent deletion of all non-consensual marks to restore your financial standing and protect your legal rights effectively.

ChexSystems Dispute Final Decision Letter

A ChexSystems Dispute Final Decision Letter is the official resolution regarding inaccuracies in your consumer banking report. Upon receiving this document, verify if the disputed records were deleted, updated, or validated as accurate. If the outcome is unfavorable, you have the legal right to add a brief consumer statement to your file. This letter is crucial for monitoring your banking reputation and ensuring you can open new accounts without denial. Always retain this correspondence as proof of correction should the same error reappear in the future.

Paid in Full Derogatory Mark Update Letter

A Paid in Full Derogatory Mark Update Letter is a formal request sent to credit bureaus to ensure your report accurately reflects a zero balance. While paying a debt doesn't automatically remove negative history, updating the status to "Paid in Full" can improve your creditworthiness during manual reviews. This letter serves as essential documentation to dispute inaccuracies if a creditor fails to report the settlement. Consistently monitoring your credit score ensures that satisfied obligations are no longer listed as active collections or outstanding liabilities.

Bank Error Derogatory Mark Deletion Letter

A Bank Error Derogatory Mark Deletion Letter is a formal dispute sent to credit bureaus to remove inaccurate negative information caused by financial institution mistakes. If a bank incorrectly reported a late payment or default, this document serves as legal evidence to rectify your credit report. It must clearly outline the specific error, provide supporting documentation, and cite the Fair Credit Reporting Act to ensure compliance. Successfully restoring your credit score depends on professional communication and verifying that the lender acknowledges their administrative oversight in writing.

Incomplete Inquiry Rejection Letter

An Incomplete Inquiry Rejection Letter is a formal notice sent when a request lacks essential information to be processed. Its primary purpose is to maintain operational efficiency by informing the sender exactly which details are missing. A professional letter should clearly list the required documentation or data needed for reconsideration. Providing a specific deadline for resubmission helps streamline communication and prevents administrative delays. This transparent approach ensures that both parties understand the necessary steps to resolve the pending inquiry effectively and professionally.

Overdraft Fee Dispute Resolution Letter

An Overdraft Fee Dispute Resolution Letter is a formal request sent to your bank to contest unfair charges. This document should clearly state your account details, the specific transaction date, and the reason for the refund request, such as a processing error or a first-time waiver plea. Providing evidence of your positive banking history or proof of error increases the likelihood of success. Sending this written notice ensures a documented record of your claim, protecting your consumer rights while aiming to restore your account balance efficiently.

Frivolous ChexSystems Dispute Notification Letter

A Frivolous ChexSystems Dispute Notification Letter is a formal notice sent by the consumer reporting agency when they refuse to investigate your claim. This occurs if your dispute lacks sufficient evidence, contains repetitive information, or appears to be generated by a credit repair template without factual backing. To resolve this, you must resubmit your request with new documentation or specific proof of errors. Understanding this response is crucial for effectively clearing inaccurate banking history and restoring your ability to open new checking accounts at financial institutions.

What is a ChexSystems Derogatory Mark Inquiry Response Letter?

A ChexSystems Derogatory Mark Inquiry Response Letter is a formal written request sent to the consumer reporting agency to dispute inaccurate, outdated, or unverifiable negative information on your banking history report. This letter initiates a formal investigation to remove "derogatory marks" such as unpaid overdrafts, bounced checks, or account abuse flags that prevent you from opening new bank accounts.

How long does ChexSystems have to respond to a dispute inquiry?

Under the Fair Credit Reporting Act (FCRA), ChexSystems generally has 30 to 45 days to investigate your inquiry and provide a formal response. If they cannot verify the derogatory mark with the reporting financial institution within this timeframe, the negative information must be legally removed from your consumer file.

What information should be included in a ChexSystems dispute letter?

A professionally optimized response letter should include your full legal name, Social Security number, current mailing address, and the specific account number associated with the derogatory mark. You must clearly state the reason for the inquiry-such as "account not mine," "incorrect balance," or "information older than five years"-and attach supporting documentation like bank statements or a settlement release.

Can a derogatory mark be removed if the debt has been paid?

Yes, you can send a response letter requesting a status update to "Paid in Full" or "Settled." While paying a debt does not automatically delete the history, many consumers use a "Pay for Delete" negotiation where the bank agrees to remove the derogatory mark from ChexSystems entirely upon receipt of payment, which should be documented in your inquiry letter.

What are the most common reasons to send an inquiry response to ChexSystems?

The most common reasons include identity theft or fraud, reporting errors by the bank, items exceeding the five-year reporting limit, and instances where a consumer was never notified of the original debt. Sending a formal inquiry is the primary method for clearing your name to regain eligibility for standard checking and savings accounts.

Comments