Protecting your financial reputation requires a swift, professional Identity Theft Claim Investigation Response Letter. When disputing unauthorized transactions, a formal rebuttal ensures creditors re-examine fraudulent activity with the required legal scrutiny. This guide outlines how to structure your response to resolve disputes effectively and restore your credit standing. To help you get started quickly, below are some ready to use templates.

Image cover: Professional Templates for Identity Theft Investigation Response Letters

Letter Samples List

- Identity Theft Claim Acknowledgment Letter

- Identity Theft Affidavit Request Letter

- Request For Additional Investigation Documentation Letter

- Provisional Credit Issuance Notification Letter

- Identity Theft Investigation Status Update Letter

- Favorable Identity Theft Claim Resolution Letter

- Identity Theft Claim Denial And Conclusion Letter

- Provisional Credit Revocation Notice Letter

- Fraudulent Account Closure Confirmation Letter

- Compromised Account Transfer And Resolution Letter

- Credit Bureau Identity Theft Dispute Resolution Letter

- Final Identity Theft Investigation Determination Letter

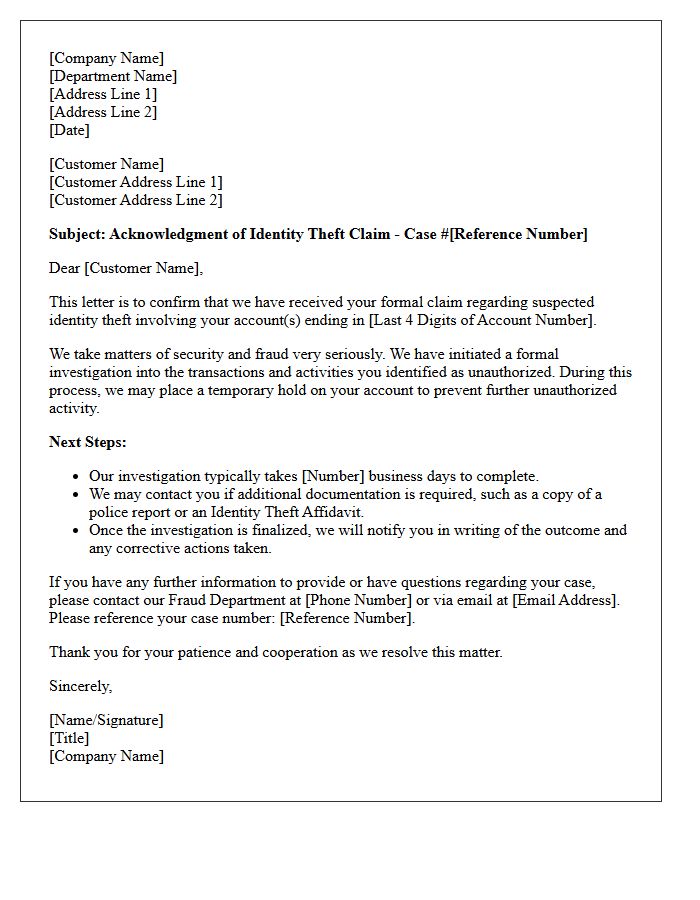

Identity Theft Claim Acknowledgment Letter

An Identity Theft Claim Acknowledgment Letter is a formal document sent by financial institutions to confirm they have received your fraud report. This official notification serves as critical evidence that your dispute process has legally commenced. It typically outlines the next steps, provides a tracking number, and specifies the investigation timeframe required under consumer protection laws. Retain this letter as a vital part of your identity recovery records to ensure your rights are protected while the bank reviews unauthorized transactions or compromised accounts.

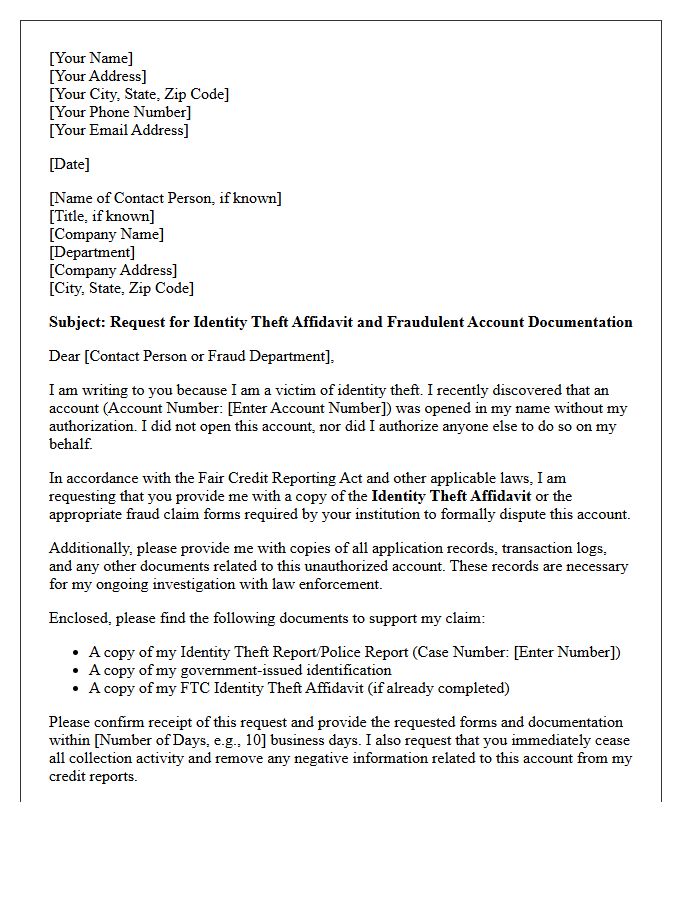

Identity Theft Affidavit Request Letter

An Identity Theft Affidavit Request Letter is a formal document sent to creditors or financial institutions to report fraudulent accounts opened in your name. This letter serves as official notification that you are a victim of fraud, demanding an investigation into the disputed activity. It should be accompanied by a government-issued Identity Theft Report to provide legal weight. Sending this request is a critical step to clear your credit record, stop unauthorized debt collection, and restore your financial integrity after personal information has been compromised.

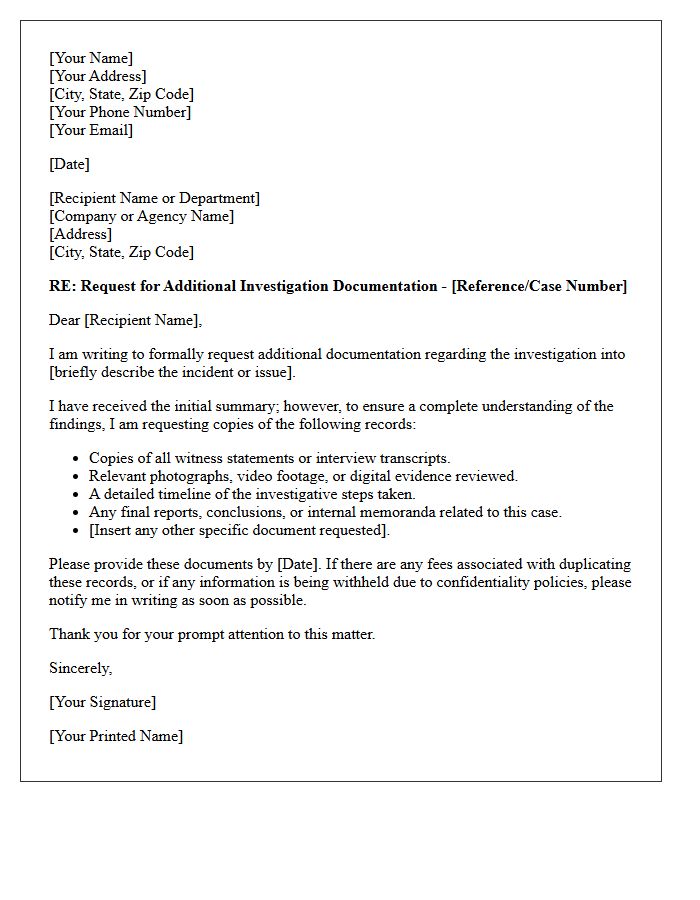

Request For Additional Investigation Documentation Letter

A Request for Additional Investigation Documentation Letter is a formal response sent to an insurance company or entity when a claim is denied or delayed. The primary purpose of this letter is to demand transparency by requesting the specific evidence, reports, and internal logs used to make a decision. By formally asking for these records, you ensure due process and create a paper trail for potential legal action. This document is essential for uncovering errors in the investigation process and challenging unfair claim adjustments effectively.

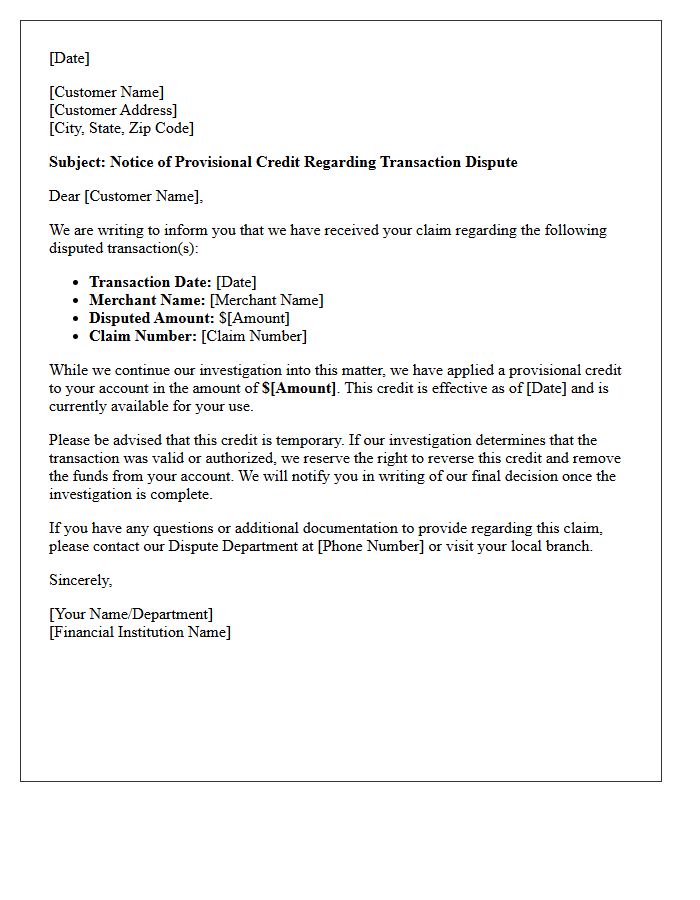

Provisional Credit Issuance Notification Letter

A Provisional Credit Issuance Notification Letter informs consumers that a bank has temporarily restored funds to their account during an ongoing ATM or debit card dispute investigation. Under Regulation E, financial institutions must provide this temporary credit if the inquiry exceeds ten business days. This letter confirms the specific amount credited and outlines the conditional nature of the funds. If the bank ultimately determines no error occurred, they reserve the legal right to reverse the credit and withdraw the funds from the account after providing proper notice.

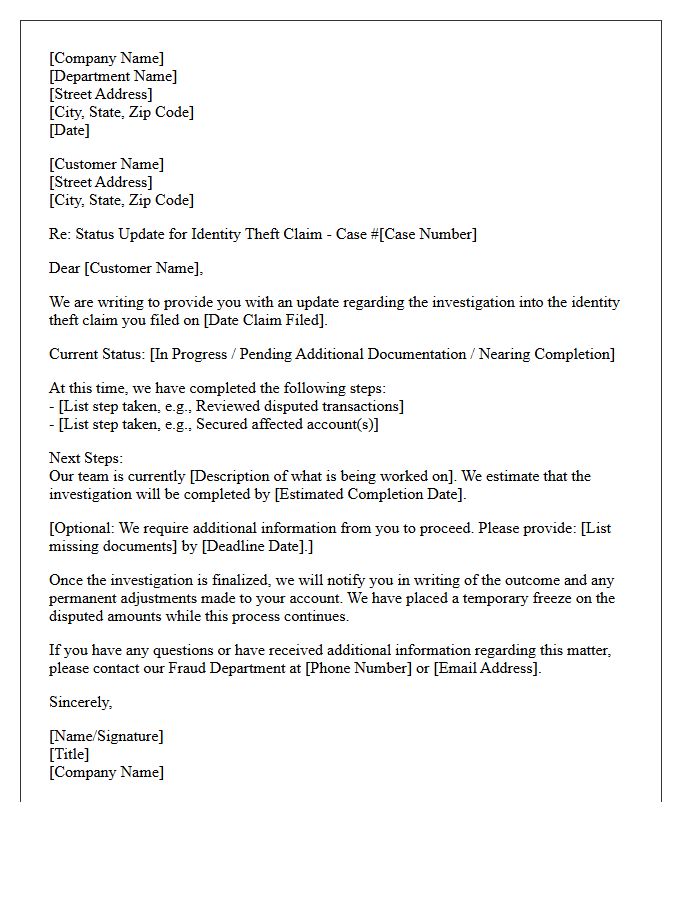

Identity Theft Investigation Status Update Letter

An Identity Theft Investigation Status Update Letter provides essential notification regarding the current progress of a fraud inquiry. This document informs victims whether their case is active, pending further evidence, or closed. It is a critical record for legal protection and credit restoration. Consumers should review the letter to ensure all disputed transactions are being addressed by the financial institution. Keeping these updates organized helps maintain a clear audit trail, which is vital for clearing one's name and restoring financial integrity after a security breach occurs.

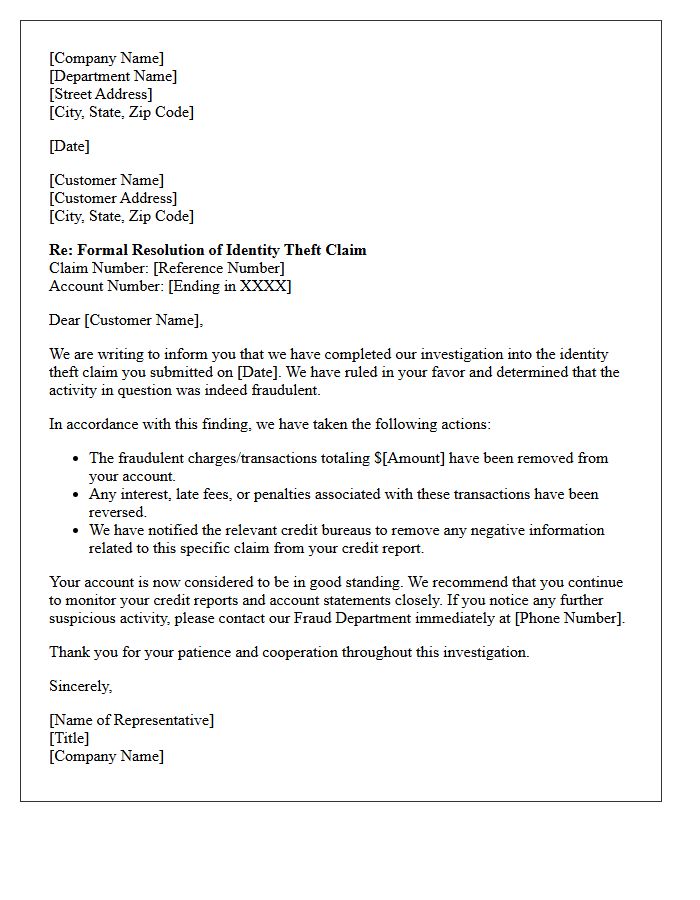

Favorable Identity Theft Claim Resolution Letter

A Favorable Identity Theft Claim Resolution Letter serves as official confirmation that a financial institution has validated your dispute. This document proves that fraudulent charges were removed and your account was restored. It is essential to keep this letter as permanent legal evidence to protect your credit score from future errors. If a collection agency pursues the debt later, presenting this resolution ensures your financial exoneration and prevents further liability. Always verify that the letter explicitly states the investigation is closed and the balance is corrected.

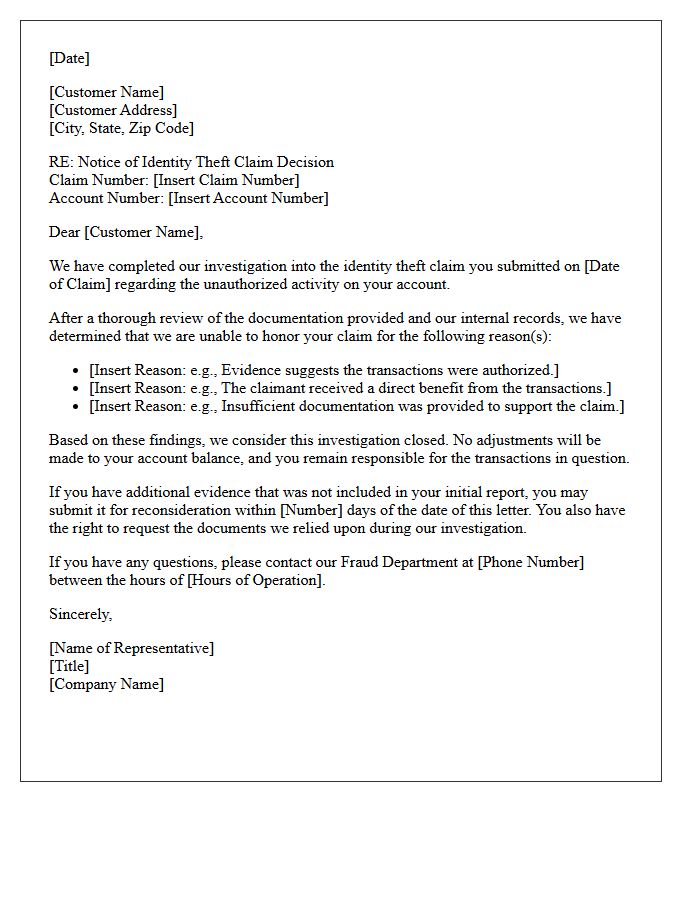

Identity Theft Claim Denial And Conclusion Letter

Receiving an Identity Theft Claim Denial And Conclusion Letter signifies that your financial institution has finished its investigation and refused your request for reimbursement. The most critical step is to review the reason for denial, which may cite a lack of evidence or claims of "authorized" transactions. You have a legal right to request all documentation used in their decision. To challenge this outcome, you must file a formal written appeal, provide additional police reports or identity theft affidavits, and strictly follow the timelines mandated by the Electronic Fund Transfer Act.

Provisional Credit Revocation Notice Letter

A Provisional Credit Revocation Notice Letter informs a consumer that a temporary credit issued during a billing error investigation has been reversed. This occurs when a financial institution determines that the disputed transaction was actually authorized or legitimate. The letter must clearly state the date the funds will be debited and explain the findings of the investigation. Under Regulation E, banks are required to provide this formal notification to ensure transparency and allow consumers time to cover potential overdrafts resulting from the reclaimed funds.

Fraudulent Account Closure Confirmation Letter

A Fraudulent Account Closure Confirmation Letter is a critical document used to verify that an unauthorized account opened in your name has been permanently terminated. This letter serves as official legal proof that you are not responsible for any debts or transactions associated with the identity theft incident. It is essential to retain this record to clear your credit report and resolve future disputes with financial institutions or credit bureaus. Always ensure the letter explicitly states the account balance is zero and the identity theft investigation is concluded.

Compromised Account Transfer And Resolution Letter

A Compromised Account Transfer and Resolution Letter is a formal document used to secure and restore unauthorized access to financial or personal accounts. It serves as official notification to institutions that identity theft has occurred, requesting an immediate freeze or transfer of funds to a new, secure account. Providing clear documentation of the breach helps expedite the recovery process and limits your legal liability for fraudulent transactions. Always include specific account details and police report references to ensure legal protection and successful dispute resolution with your bank.

Credit Bureau Identity Theft Dispute Resolution Letter

A Credit Bureau Identity Theft Dispute Resolution Letter is a formal legal notice used to remove fraudulent accounts from your credit report. Under the Fair Credit Reporting Act, you must provide clear evidence, such as an Identity Theft Report or police filing, to prove the activity was unauthorized. Clearly list each inaccurate tradeline and request immediate deletion. Sending this document via certified mail ensures a tracking record. Once received, bureaus are legally obligated to investigate and block the reporting of fraud-related information, protecting your financial reputation and credit score integrity.

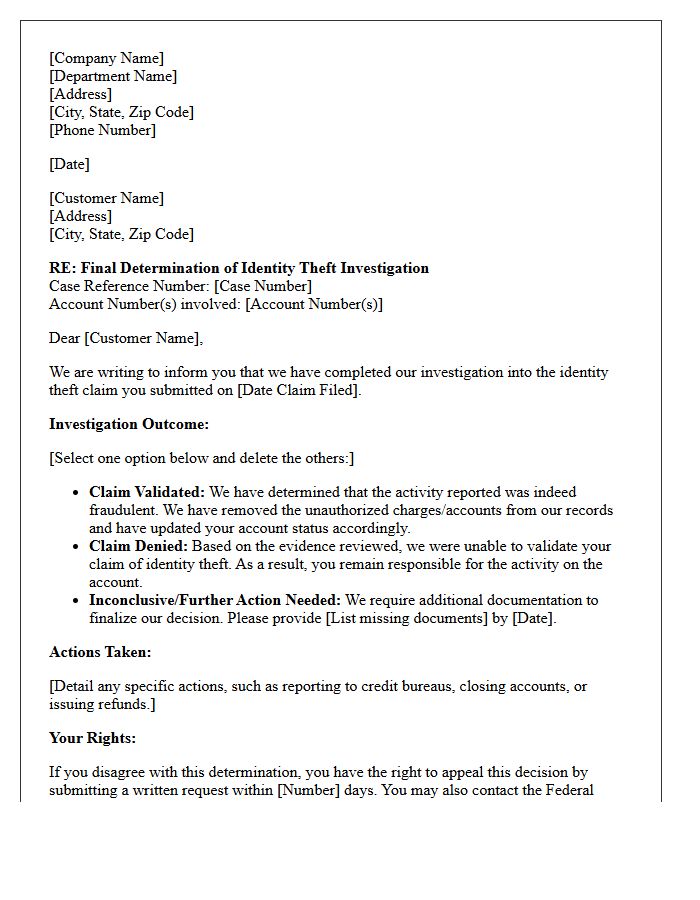

Final Identity Theft Investigation Determination Letter

A Final Identity Theft Investigation Determination Letter is the official resolution sent by a creditor or credit bureau. This document confirms the investigation results regarding fraudulent accounts or transactions reported by a victim. It states whether the claims were validated and if the disputed records will be permanently removed from your credit profile. You must keep this letter as legal evidence of your innocence to prevent future collection actions and to ensure your financial records remain accurate and secure following a security breach.

What should be included in an identity theft claim investigation response letter?

An identity theft claim investigation response letter should include the tracking or claim number, the final determination of the investigation, a summary of the evidence reviewed, and a clear explanation of whether the disputed transactions will be permanently removed or reinstated.

How long do financial institutions have to respond to an identity theft claim?

Under the Fair Credit Billing Act (FCBA) and Regulation E, financial institutions generally have 30 to 90 days to conduct an investigation and provide a written response letter detailing their findings and any corrective actions taken.

What does it mean if my identity theft claim investigation is "denied"?

A denial response indicates that the investigator found insufficient evidence of fraud or determined that the account holder authorized the transactions. The response letter must provide an explanation for this decision and inform the consumer of their right to request the documents used in the investigation.

How do I respond to a letter requesting more information for my identity theft claim?

You should promptly provide the requested documentation, such as a formal FTC Identity Theft Report, a police report, or an affidavit of forgery, to ensure the investigation continues within the legal timeframe and to strengthen your case for reimbursement.

Can an identity theft claim investigation response letter affect my credit score?

Yes. If the response letter confirms that the fraudulent activity was verified, the creditor must notify the credit bureaus to remove the negative information, which can help restore your credit score. If the claim is denied, the reported debt may remain on your credit report.

Comments