Managing financial transparency is crucial when a borrower requests a detailed review of their mortgage impound account. An Escrow Account Analysis Inquiry Response Letter provides a professional explanation of surplus or deficiency calculations, ensuring regulatory compliance and clear communication. This guide outlines how to address homeowner concerns regarding payment adjustments and tax disbursements effectively. Below are some ready to use templates.

Image cover: Professional Escrow Account Analysis Inquiry Response Templates

Letter Samples List

- Escrow Shortage Explanation Response Letter

- Escrow Surplus Refund Inquiry Response Letter

- Property Tax Increase Escrow Analysis Letter

- Insurance Premium Adjustment Escrow Response Letter

- Escrow Account Analysis Dispute Resolution Letter

- Annual Escrow Analysis Statement Clarification Letter

- Escrow Account Waiver Inquiry Response Letter

- Escrow Monthly Payment Adjustment Explanation Letter

- Supplemental Tax Assessment Escrow Response Letter

- Private Mortgage Insurance Removal Escrow Letter

- Escrow Reserve Cushion Requirement Response Letter

- Escrow Account Closure Inquiry Response Letter

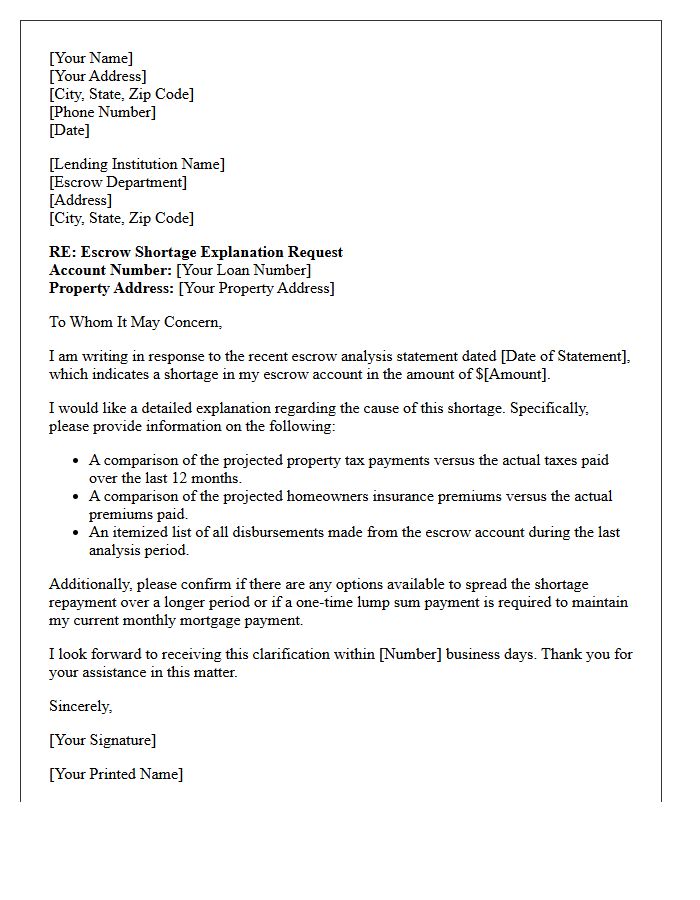

Escrow Shortage Explanation Response Letter

An Escrow Shortage Explanation Response Letter addresses a deficiency in your mortgage impound account. This document clarifies why your monthly payment increased, often due to rising property taxes or insurance premiums. To resolve this, you can typically choose to pay the shortage balance as a one-time lump sum or spread the cost over twelve months. Reviewing your annual escrow analysis statement alongside this letter ensures your servicer's calculations are accurate and helps you maintain a balanced housing budget while avoiding future payment shocks.

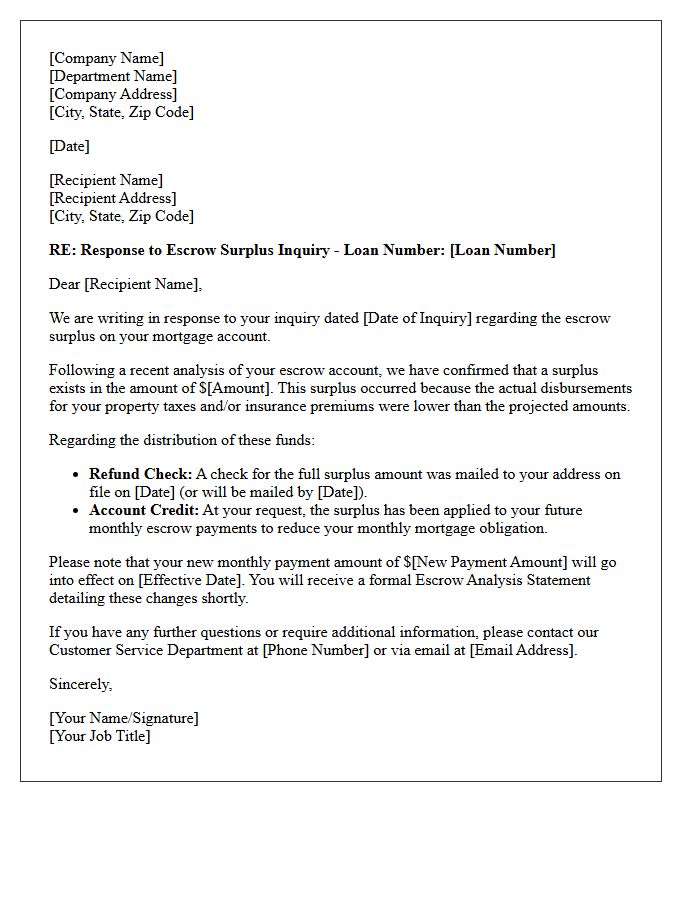

Escrow Surplus Refund Inquiry Response Letter

An Escrow Surplus Refund Inquiry Response Letter is a formal document sent by a mortgage servicer to explain an escrow overage. It confirms that the balance in your impound account exceeds the required minimum, typically due to lower than expected property taxes or insurance premiums. The letter details the specific amount to be returned, the scheduled disbursement date, and how the surplus will be delivered-usually via a check or a direct credit to your principal balance. Understanding this statement ensures your mortgage payments remain accurate following your annual escrow analysis.

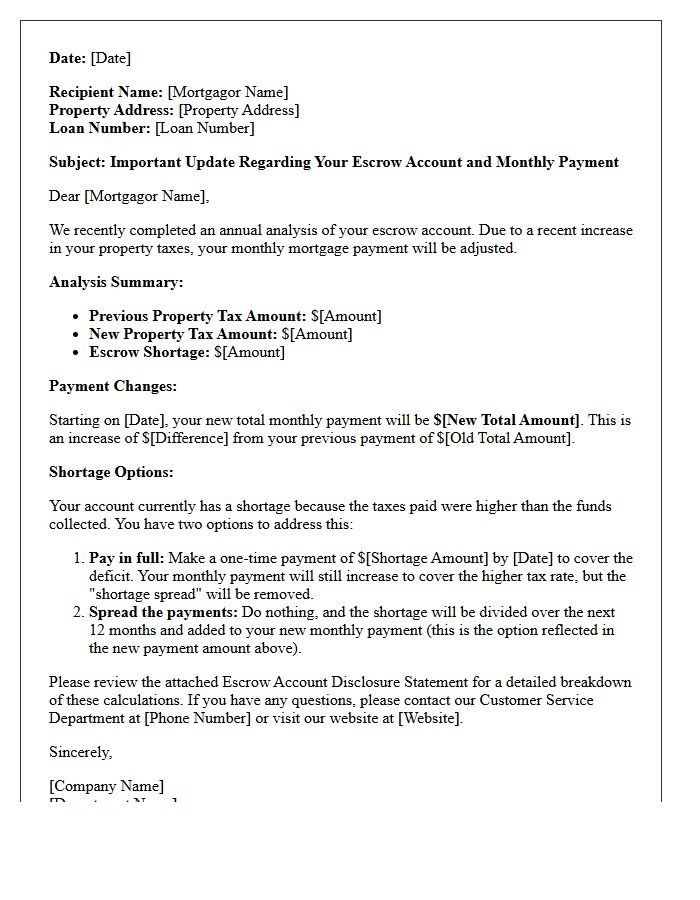

Property Tax Increase Escrow Analysis Letter

A Property Tax Increase Escrow Analysis Letter notifies homeowners of a shortage in their mortgage account due to rising assessments. When taxes climb, your monthly payment must increase to cover the deficit and maintain a minimum cushion required by lenders. You typically have two options: pay the entire shortage as a lump sum to keep payments stable or spread the balance over the next year, which significantly raises your monthly bill. Reviewing this document immediately ensures you understand your new financial obligations and avoids unexpected late fees or escrow imbalances.

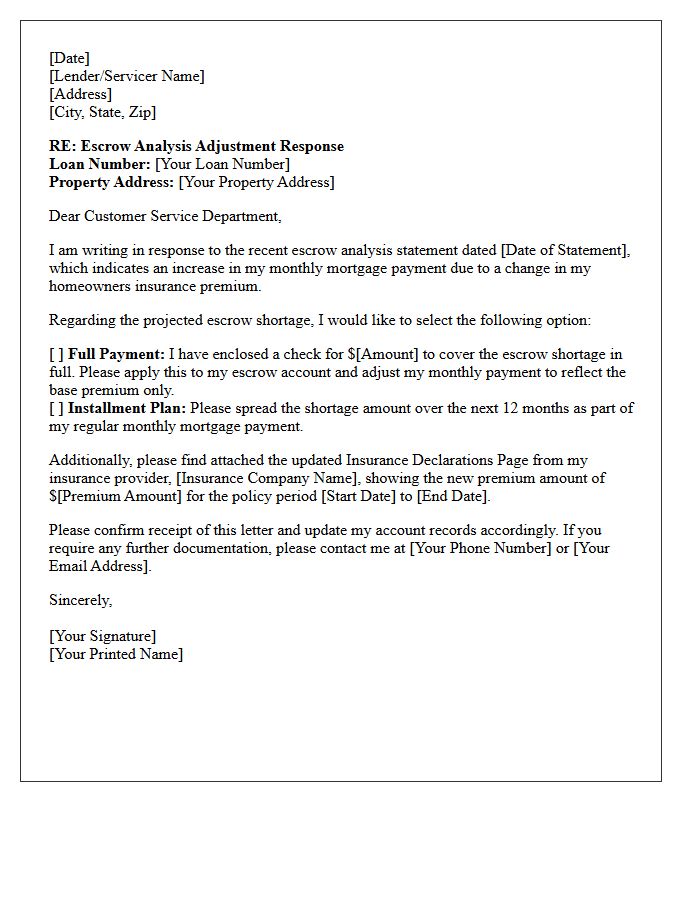

Insurance Premium Adjustment Escrow Response Letter

An Insurance Premium Adjustment Escrow Response Letter is a formal document sent by a mortgage servicer to a homeowner. It explains changes in monthly mortgage payments resulting from fluctuations in property insurance costs. When premiums increase, an escrow shortage occurs, requiring a payment adjustment to cover the deficit. This letter details the new escrow analysis, updated payment amounts, and options to pay the shortage as a lump sum or through installments. Understanding this notice is essential for maintaining an accurate mortgage account and avoiding unexpected financial surprises.

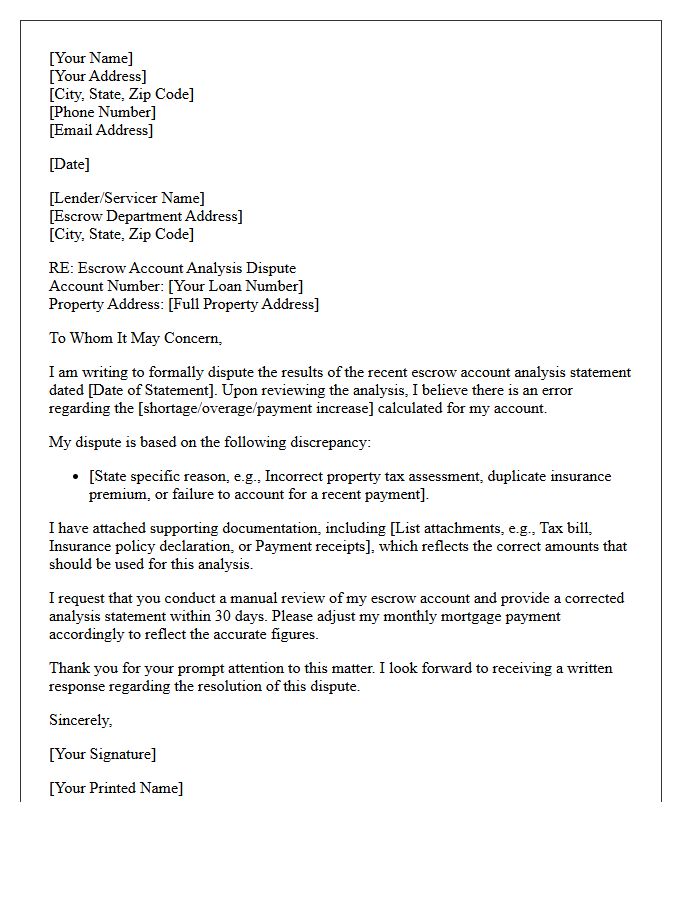

Escrow Account Analysis Dispute Resolution Letter

An Escrow Account Analysis Dispute Resolution Letter is a formal document sent to mortgage servicers to challenge inaccurate calculations regarding taxes or insurance. It serves as a legal notice to rectify errors in projected shortages, surpluses, or monthly payment spikes. Clearly state the specific discrepancy and include supporting evidence to ensure regulatory compliance under RESPA. This written communication protects homeowners from overpaying and forces lenders to conduct a manual review of the escrow impound account for financial accuracy and transparency.

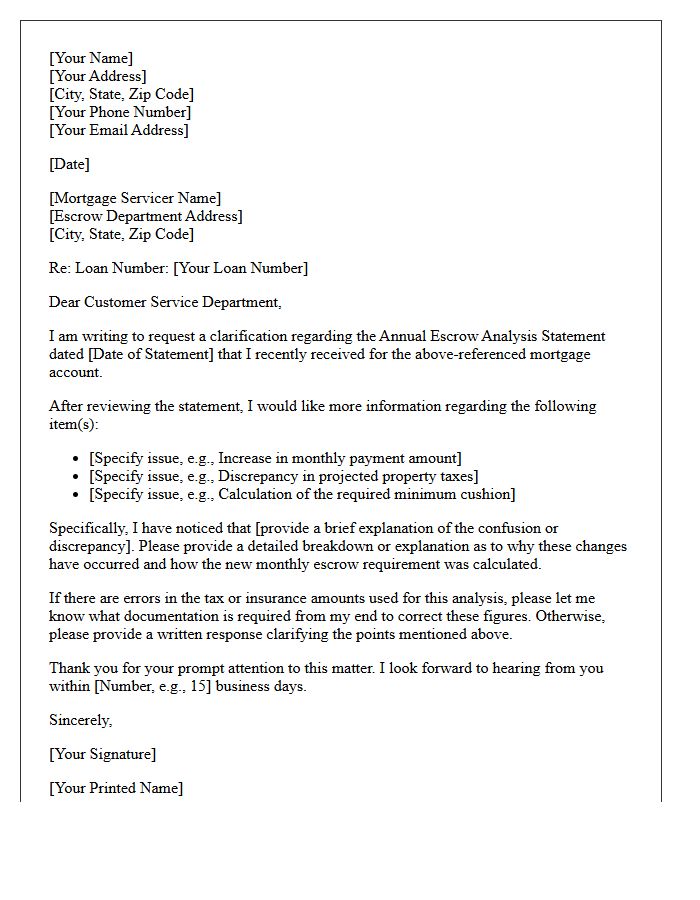

Annual Escrow Analysis Statement Clarification Letter

The Annual Escrow Analysis Statement Clarification Letter is a crucial document that explains changes in your monthly mortgage payment. It bridges the gap between complex tax or insurance adjustments and your actual billing. Understanding this letter helps you identify an escrow shortage or surplus early. It details how fluctuations in property values or premium hikes impact your impound account balance. Reviewing this clarification ensures you understand why your payment increased and helps you manage your long-term homeownership costs effectively without unexpected financial surprises.

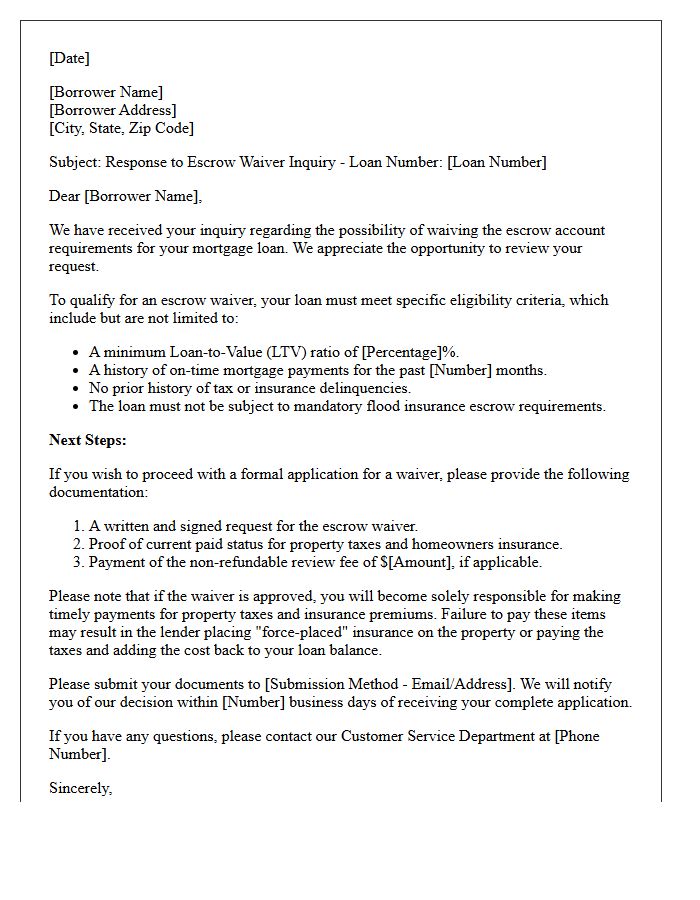

Escrow Account Waiver Inquiry Response Letter

An Escrow Account Waiver Inquiry Response Letter is a formal notification from a lender regarding a borrower's request to manage their own property taxes and insurance. This document outlines the specific eligibility criteria, such as maintaining a certain loan-to-value ratio and a history of timely payments. It serves as a definitive confirmation of whether the escrow waiver is approved or denied. Understanding this response is crucial for homeowners who prefer direct financial control, ensuring they meet all servicing requirements to avoid potential default or forced-place insurance policies.

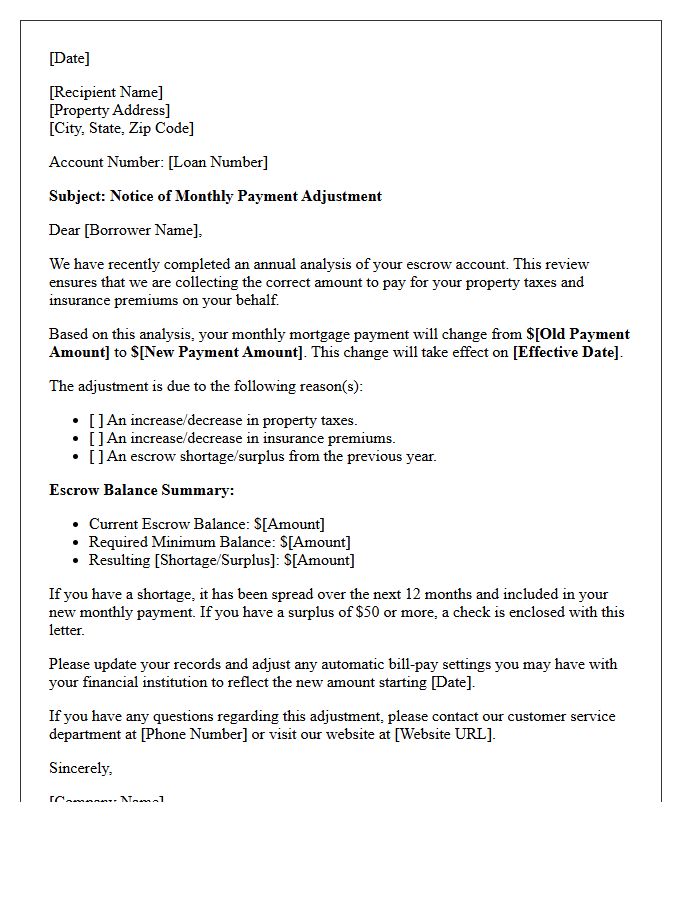

Escrow Monthly Payment Adjustment Explanation Letter

An Escrow Monthly Payment Adjustment Explanation Letter notifies homeowners of changes to their mortgage payments due to an annual analysis. This document details shifts in property taxes or insurance premiums that create a surplus or a shortage in your account. If your escrow balance falls below the required minimum, your monthly installment will increase to cover the gap. Carefully reviewing this disclosure statement ensures you understand why your payment fluctuated and helps you budget for upcoming housing expenses effectively.

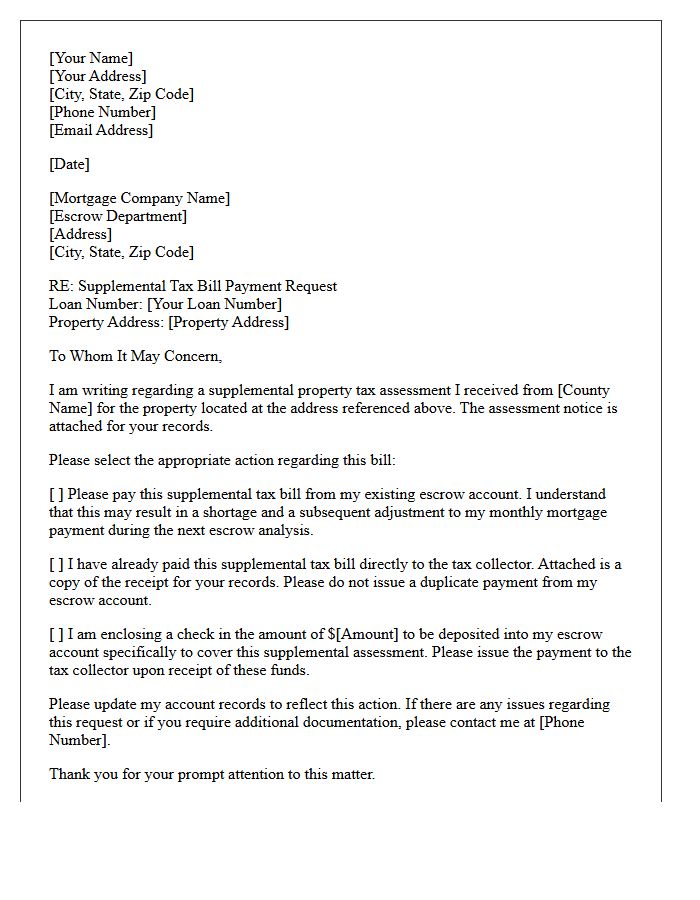

Supplemental Tax Assessment Escrow Response Letter

A Supplemental Tax Assessment Escrow Response Letter is a critical document sent to your mortgage servicer to manage unexpected property tax increases. When a property is reassessed after a purchase or construction, the supplemental bill often falls outside standard escrow calculations. Sending this response ensures your lender adjusts your escrow account or pays the one-time bill directly from available funds. Failure to provide this notice can lead to delinquent taxes, penalties, or sudden spikes in your monthly mortgage payment to cover the resulting escrow shortage.

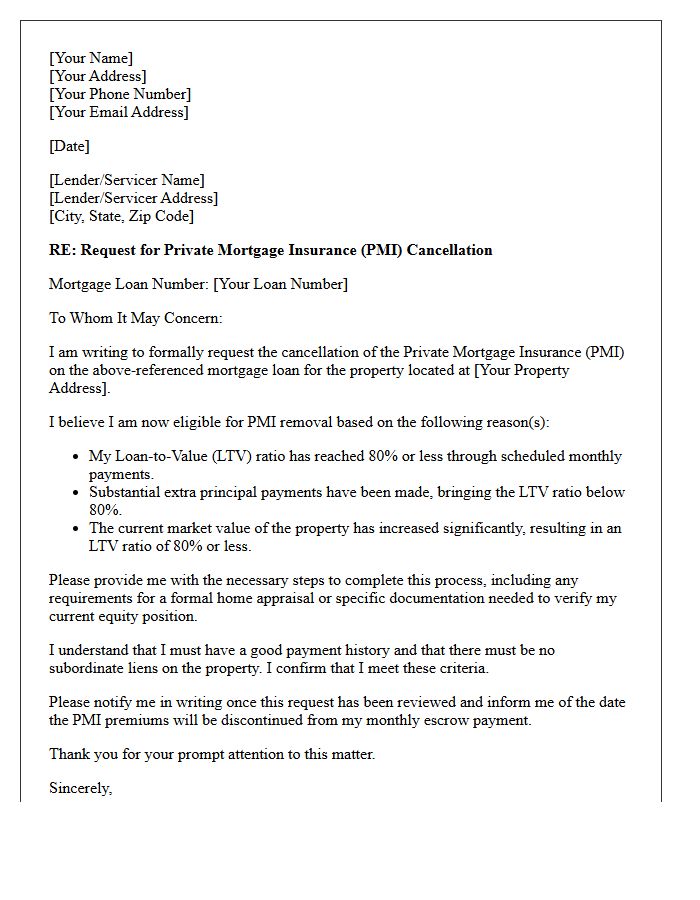

Private Mortgage Insurance Removal Escrow Letter

A private mortgage insurance (PMI) removal escrow letter is a formal request sent to your lender to cancel PMI premiums once you reach 20% home equity. To qualify, you must have a proven payment history and potentially provide a new appraisal to verify current market value. Federal law requires automatic termination at 78% loan-to-value, but a written letter can expedite the process and improve monthly cash flow. Always ensure your request follows specific servicer guidelines to successfully remove this additional cost from your monthly mortgage statement.

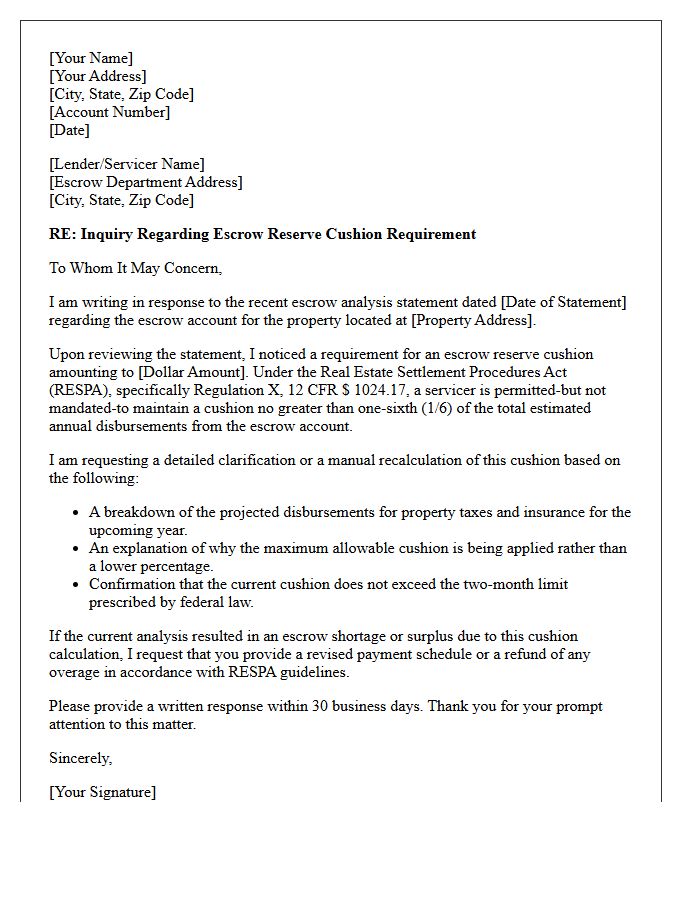

Escrow Reserve Cushion Requirement Response Letter

An Escrow Reserve Cushion Requirement Response Letter is a formal document sent to a mortgage lender to contest or clarify escrow shortages. It ensures your account complies with RESPA guidelines, which typically limit a cushion to two months of payments. Use this letter to request a detailed analysis of your account, challenge overages, or propose a repayment plan. Providing proof of payment for taxes or insurance can resolve discrepancies. Effectively responding helps maintain financial stability and prevents unnecessary increases in your monthly mortgage payment due to calculation errors.

Escrow Account Closure Inquiry Response Letter

An Escrow Account Closure Inquiry Response Letter serves as formal documentation confirming the termination of a third-party holding arrangement. It must clearly state the final disbursement of remaining funds, detailing who received the balance and the method of payment. Key information includes the official closure date, verification of settled obligations, and any potential tax implications or interest earned. This letter provides legal clarity for both parties, ensuring that all contractual contingencies were met before the account was deactivated and the professional relationship concluded.

What is an Escrow Account Analysis Inquiry Response Letter?

An Escrow Account Analysis Inquiry Response Letter is a formal document sent by a mortgage servicer to a borrower explaining the results of a review regarding tax payments, insurance premiums, and the required minimum balance of their escrow account.

Why did I receive a response regarding my escrow analysis?

You received this response because either an annual review was completed or you submitted an inquiry regarding changes in your monthly mortgage payment, a perceived shortage, or a surplus in your escrow funds.

What causes a shortage or surplus in an escrow account?

A shortage typically occurs when property taxes or insurance premiums increase beyond the previous year's estimates. Conversely, a surplus happens when these actual costs are lower than the projected amounts held in the account.

How does the escrow analysis affect my monthly mortgage payment?

If the analysis reveals a shortage, your monthly payment may increase to cover the deficit and the new projected costs. If there is a surplus, your monthly payment may decrease, and you may receive a refund check for the overage.

Can I request a re-analysis of my escrow account at any time?

Yes, you can submit a written request for an escrow re-analysis if you believe there has been a significant change in your property tax assessment or if you have switched to a lower-cost homeowners insurance provider.

Comments