Responding to a Credit Limit Increase Inquiry requires a professional approach to address customer requests or provide necessary financial documentation. Whether you are approving, denying, or requesting more information, a clear communication strategy maintains positive relationships and ensures regulatory compliance. Understanding the right tone and structure is essential for efficiency. Below are some ready to use templates.

Image cover: Professional Templates for Responding to Credit Limit Increase Inquiries

Letter Samples List

- Approved Credit Limit Increase Response Letter

- Declined Credit Limit Increase Response Letter

- Partial Credit Limit Increase Approval Letter

- Pending Credit Limit Increase Review Letter

- Credit Limit Increase Income Verification Request Letter

- Conditional Credit Limit Increase Approval Letter

- Credit Limit Increase Additional Documentation Request Letter

- Insufficient Credit History Limit Increase Denial Letter

- Delinquent Account Credit Limit Increase Rejection Letter

- Pre-Approved Credit Limit Increase Notification Letter

- High Debt-To-Income Credit Limit Increase Denial Letter

- Account Too New For Credit Limit Increase Response Letter

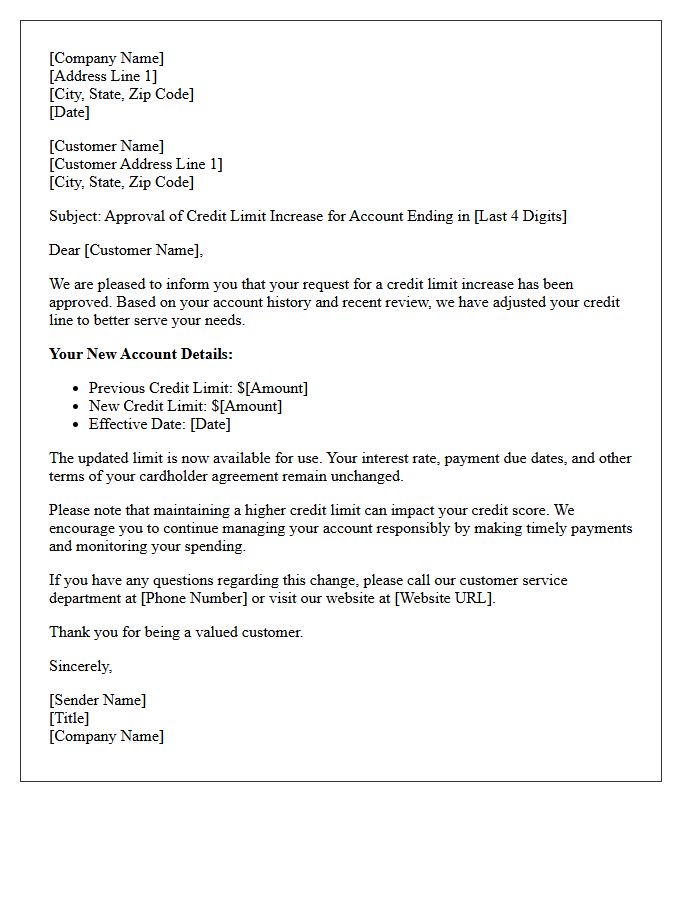

Approved Credit Limit Increase Response Letter

An Approved Credit Limit Increase Response Letter is a formal notification confirming that a financial institution has granted your request for a higher borrowing capacity. This document specifies your new credit limit, the effective date, and any updated terms or interest rates. Receiving this approval can improve your credit utilization ratio, potentially boosting your credit score. It is essential to review the letter to ensure you understand your increased spending power while maintaining responsible repayment habits to avoid accruing excessive high-interest debt.

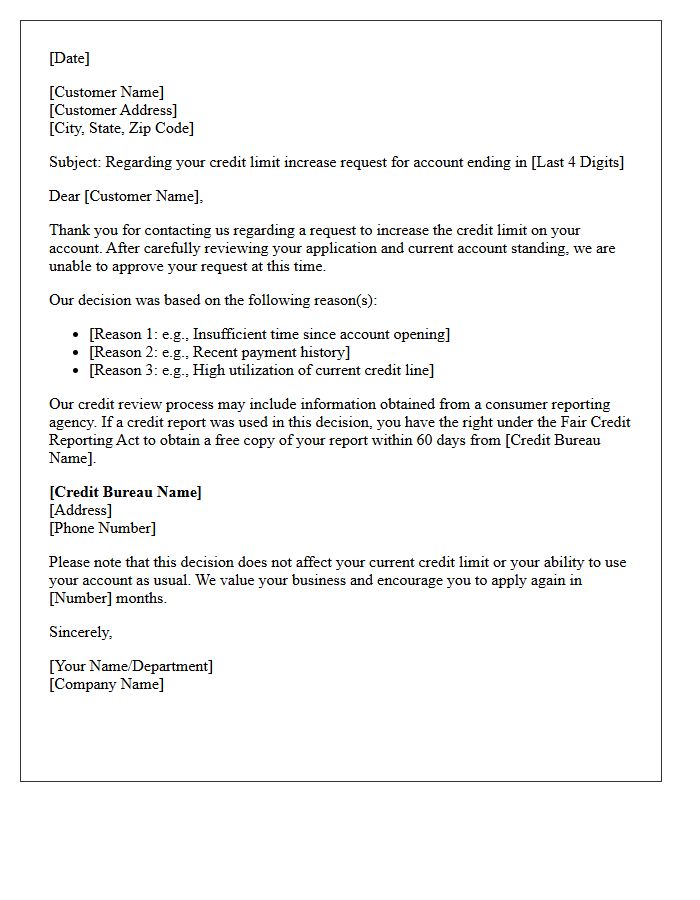

Declined Credit Limit Increase Response Letter

A declined credit limit increase response letter is a formal notice explaining why a lender denied your request. The most critical element is the adverse action notice, which outlines specific reasons such as low credit scores or insufficient income. Reviewing this document helps you identify financial weaknesses to improve your standing. By law, lenders must disclose if a credit report influenced their decision. Use this feedback to rectify errors or adjust spending habits before reapplying, ensuring you maintain a healthy debt-to-income ratio for future approvals.

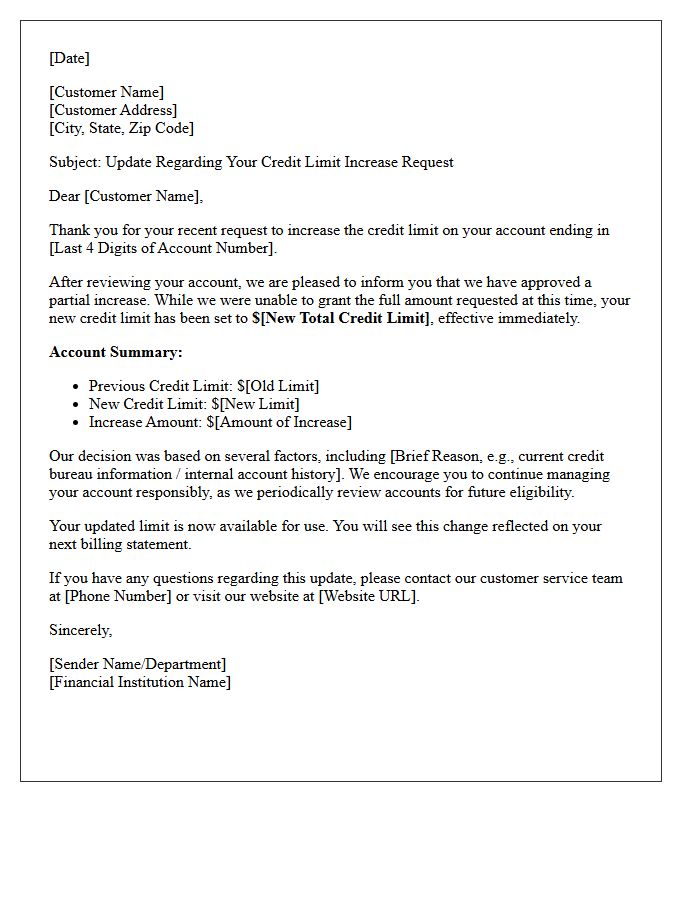

Partial Credit Limit Increase Approval Letter

A partial credit limit increase approval letter informs you that your lender granted an incremental raise rather than your full requested amount. This occurs when a financial institution's risk assessment determines you qualify for some additional capital but do not yet meet the criteria for the maximum total. It is important to review the terms and conditions provided, as accepting the partial approval still impacts your debt-to-income ratio and may influence future eligibility for higher limits based on your ongoing repayment history and credit score stability.

Pending Credit Limit Increase Review Letter

A Pending Credit Limit Increase Review Letter indicates your issuer is evaluating your request manually. This status often requires additional documentation, such as updated income verification or recent tax forms, to determine creditworthiness. Receiving this notice does not mean a denial; it simply signifies that automated algorithms need human oversight. To expedite the process, respond quickly to any information requests. Once the review concludes, you will receive a final decision via mail or your online portal regarding your new credit capacity and updated terms.

Credit Limit Increase Income Verification Request Letter

A credit limit increase income verification request letter is a formal document sent by a lender to confirm your financial capacity before granting a higher spending threshold. This verification process ensures your debt-to-income ratio remains sustainable. When submitting this request, include recent pay stubs, tax returns, or bank statements as evidence of stable earnings. Providing accurate data increases your chances of approval while maintaining your creditworthiness. Always ensure the letter is professional and clearly states your updated annual income to support your request for a higher credit limit.

Conditional Credit Limit Increase Approval Letter

A Conditional Credit Limit Increase Approval Letter notifies a borrower that their request is provisionally approved, pending specific requirements. To finalize the higher limit, you must typically provide updated income verification or maintain a clean payment history for a set period. It is crucial to review all stipulations carefully, as failure to meet these terms will result in a formal denial. This document serves as a legal notice that the increase is not yet permanent until all underwriting conditions are fully satisfied by the account holder.

Credit Limit Increase Additional Documentation Request Letter

A Credit Limit Increase Additional Documentation Request Letter is a formal notice sent by a lender when they require proof of financial stability before approving a higher spending limit. This typically occurs when your reported income, employment status, or debt-to-income ratio needs verification. Providing the requested pay stubs, tax returns, or bank statements promptly is essential for the review process. Submitting accurate documents helps lenders assess your creditworthiness and ensures your account remains in good standing while seeking additional borrowing capacity.

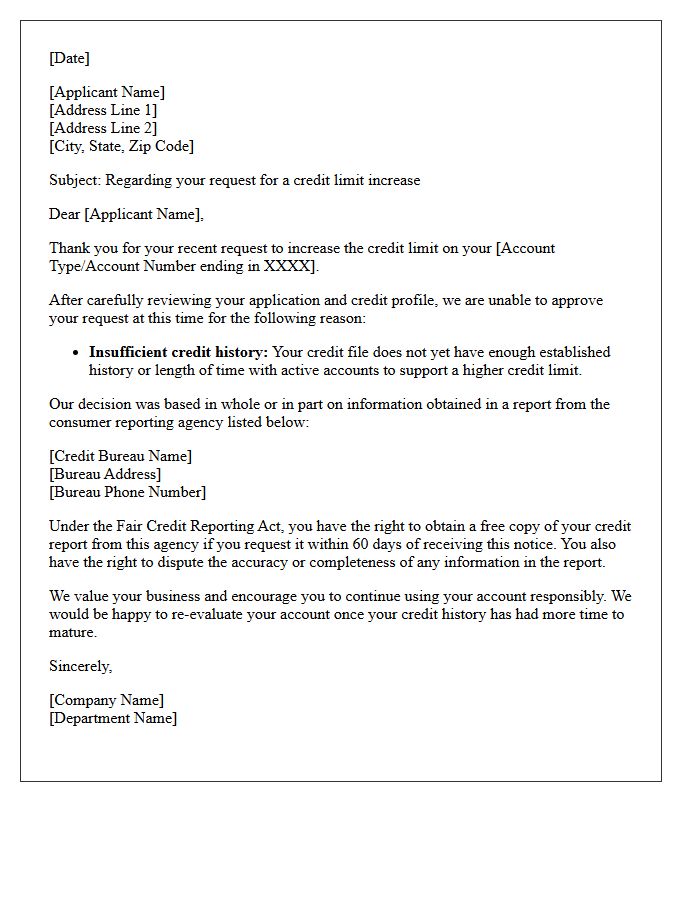

Insufficient Credit History Limit Increase Denial Letter

An Insufficient Credit History denial letter indicates that your credit report lacks enough data for lenders to assess your risk level. This typically occurs when you have too few active accounts or your credit file is too thin. To address this, focus on building a longer track record by maintaining consistent payment history over time. Consider using a secured card or becoming an authorized user to expand your profile. Lenders prioritize long-term financial stability, so patience is key when seeking a higher credit limit to improve your purchasing power and score.

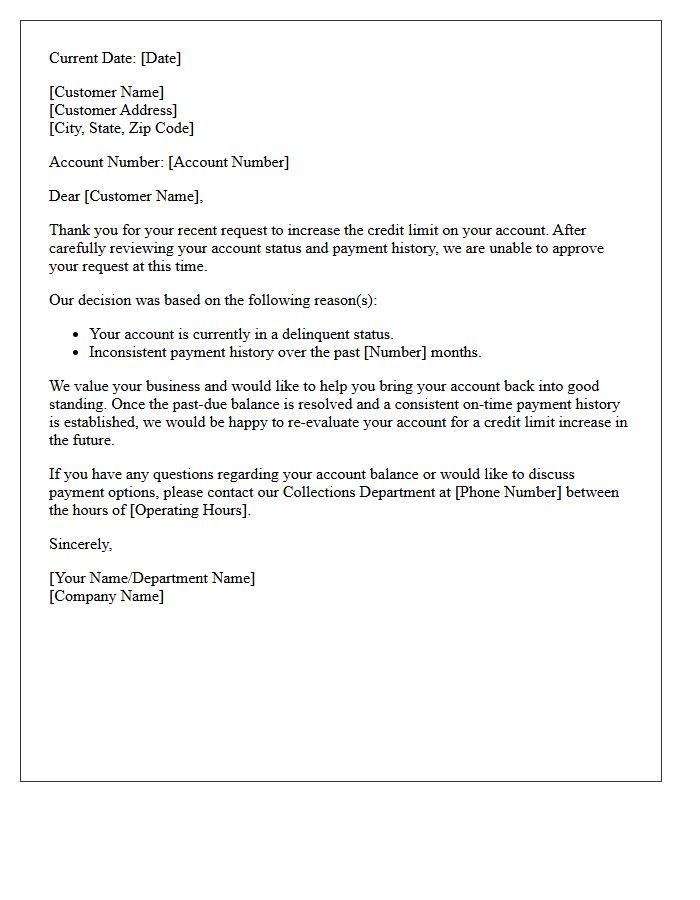

Delinquent Account Credit Limit Increase Rejection Letter

Receiving a Delinquent Account Credit Limit Increase Rejection Letter indicates that a financial institution has denied your request due to past-due payments. Lenders view delinquency as a high-risk indicator, suggesting instability in managing current debt. This formal notice typically cites your payment history or a low credit score as the primary reason for denial. To improve future eligibility, prioritize repaying overdue balances and maintaining consistent, on-time payments. Rectifying your account status is the most effective way to restore creditworthiness and eventually secure a higher credit limit.

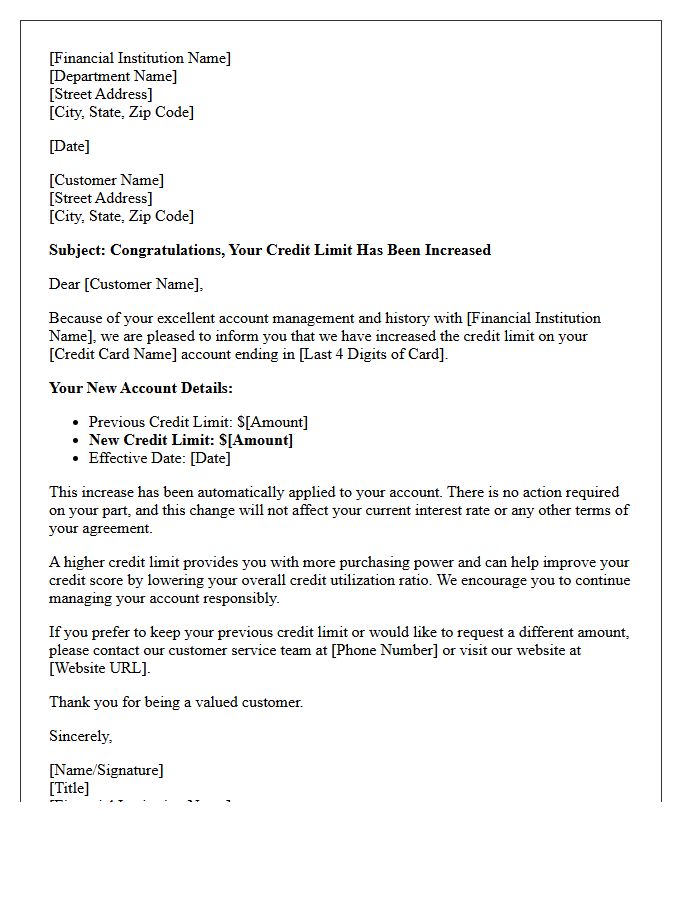

Pre-Approved Credit Limit Increase Notification Letter

A pre-approved credit limit increase notification letter informs you that your lender has already authorized a higher credit ceiling for your account based on your positive payment history. This offer is typically non-binding until you formally accept it. While it reflects financial stability, accepting the increase can improve your credit utilization ratio, potentially boosting your credit score. However, always verify if acceptance requires a hard credit inquiry, which might temporarily lower your score. Review the new terms carefully before confirming the upgrade to ensure continued financial health.

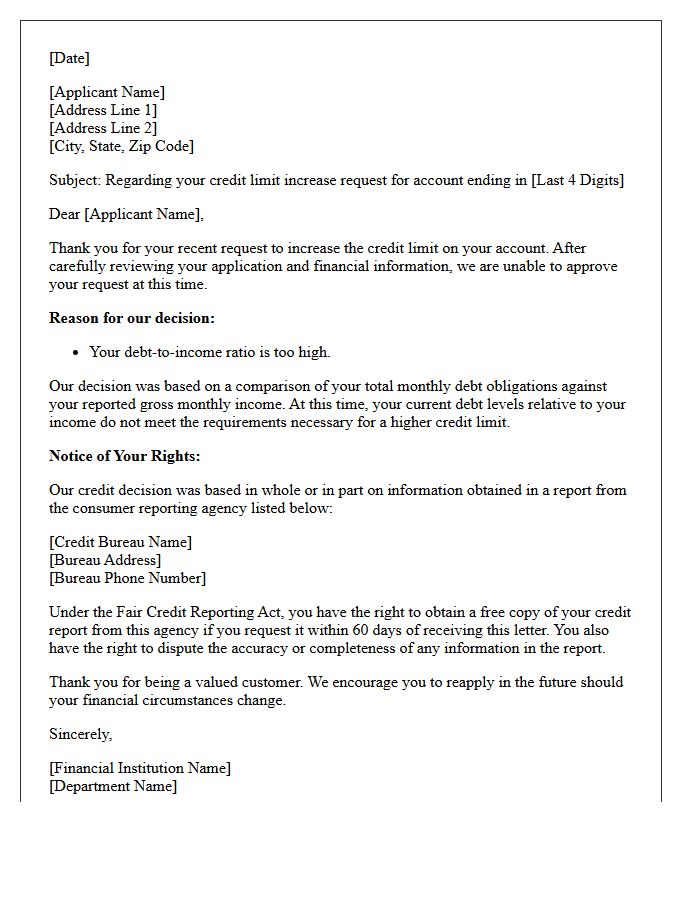

High Debt-To-Income Credit Limit Increase Denial Letter

Receiving a High Debt-To-Income (DTI) credit limit increase denial means your monthly debt obligations are too high relative to your gross income. Lenders perceive this imbalance as a financial risk, suggesting you may struggle to manage additional revolving credit. To improve your chances for future approval, focus on reducing outstanding balances or increasing your verifiable income. This denial does not impact your credit score, but it indicates that your current repayment capacity has reached its limit according to the creditor's internal risk assessment guidelines.

Account Too New For Credit Limit Increase Response Letter

An Account Too New response letter indicates your credit line remains fixed because the minimum seasoning period hasn't been met. Lenders typically require six months of consistent payment history to evaluate risk before granting a Credit Limit Increase. To improve future approval odds, maintain a low utilization ratio and ensure every payment is on time. Receiving this notice is not a denial based on creditworthiness, but rather a standard policy requiring more account longevity before the bank extends additional credit capacity to the cardholder.

What is a Credit Limit Increase Inquiry Response Letter?

A Credit Limit Increase Inquiry Response Letter is a formal document sent by a financial institution to a cardholder in response to a request for a higher credit line. It outlines whether the request was approved, denied, or if further information is required to make a decision.

What information is typically included in a response to a credit limit increase request?

The letter usually includes the decision (approval or denial), the new credit limit amount if applicable, the specific reasons for the decision, and the criteria used for the evaluation, such as credit score, payment history, and debt-to-income ratio.

How long does it take to receive a response letter after requesting a credit limit increase?

While some automated systems provide an instant decision online, a formal written response letter is typically mailed or electronically delivered within 7 to 10 business days of the initial inquiry.

Why was my credit limit increase request denied in the response letter?

Common reasons for denial cited in response letters include a low credit score, recent late payments, high credit utilization on existing accounts, insufficient income, or a credit profile that is too new with the lender.

Does receiving a credit limit increase inquiry response letter affect my credit score?

The letter itself does not affect your score; however, the process of the lender reviewing your request often involves a "hard inquiry" on your credit report, which may cause a temporary, slight decrease in your overall credit score.

Comments