Handling a Transaction Dispute Investigation Response Letter requires precise documentation and clear communication to resolve payment conflicts effectively. This guide explains how to present evidence, address merchant claims, and protect your financial rights during a bank inquiry. Learn the essential components of a professional rebuttal to ensure a fair review. Below are some ready to use templates.

Image cover: Effective Merchant Responses: Transaction Dispute Investigation Letter Samples and Templates

Letter Samples List

- Provisional Credit Approval Letter

- Transaction Dispute Claim Denial Letter

- Fraud Investigation Final Decision Letter

- Provisional Credit Revocation Letter

- ATM Dispense Error Investigation Response Letter

- ACH Unauthorized Transaction Response Letter

- Partial Credit Adjustment Resolution Letter

- Dispute Investigation Additional Information Request Letter

- Duplicate Billing Dispute Resolution Letter

- Identity Theft Investigation Response Letter

- Merchant Refund Confirmation Letter

- Cancelled Subscription Dispute Response Letter

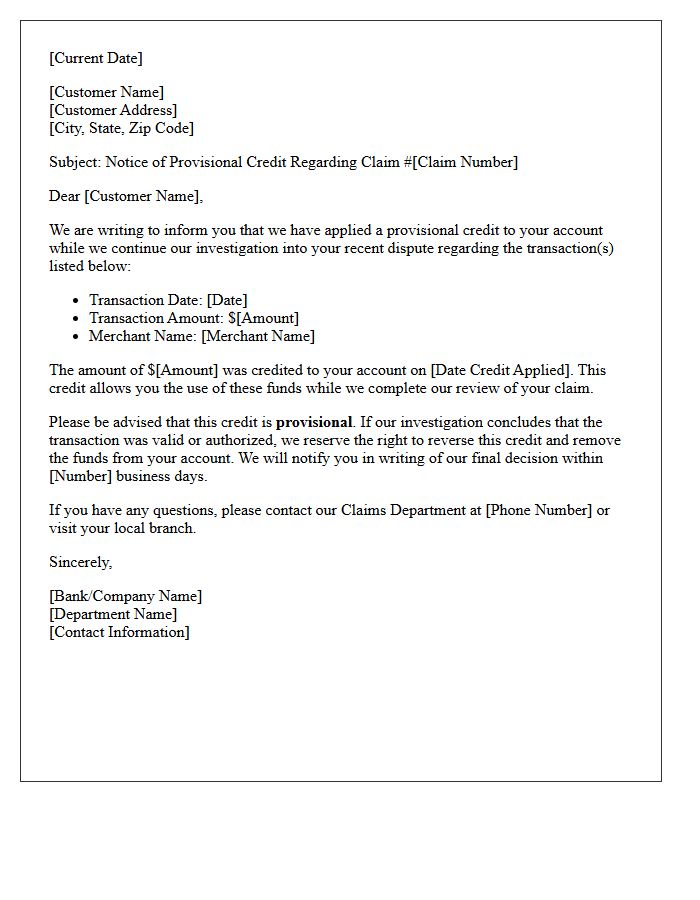

Provisional Credit Approval Letter

A Provisional Credit Approval Letter is a non-binding document issued by a lender indicating that a borrower likely qualifies for a loan based on preliminary financial screening. It outlines estimated loan amounts, interest rates, and specific contingencies that must be met before final funding. While it strengthens a buyer's position during negotiations, it does not guarantee a formal contract. Final validation requires a comprehensive underwriting process, including property appraisals and full verification of income and assets to ensure all lending criteria are satisfied.

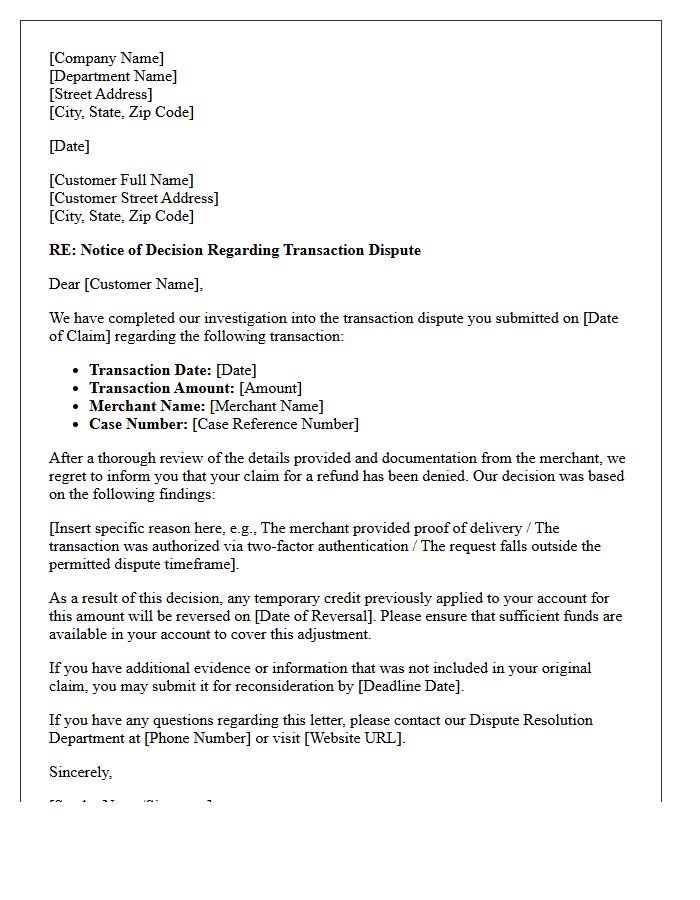

Transaction Dispute Claim Denial Letter

A Transaction Dispute Claim Denial Letter is a formal notification from a financial institution stating that your request to reverse a charge has been rejected. It typically outlines the specific reasoning for the decision, such as insufficient evidence, merchant verification, or missed filing deadlines. Upon receiving this, it is crucial to review the appeal process and the documentation used during the investigation. You have a legal right to request all evidence the bank relied upon to reach their conclusion to determine if further action or a formal re-evaluation is possible.

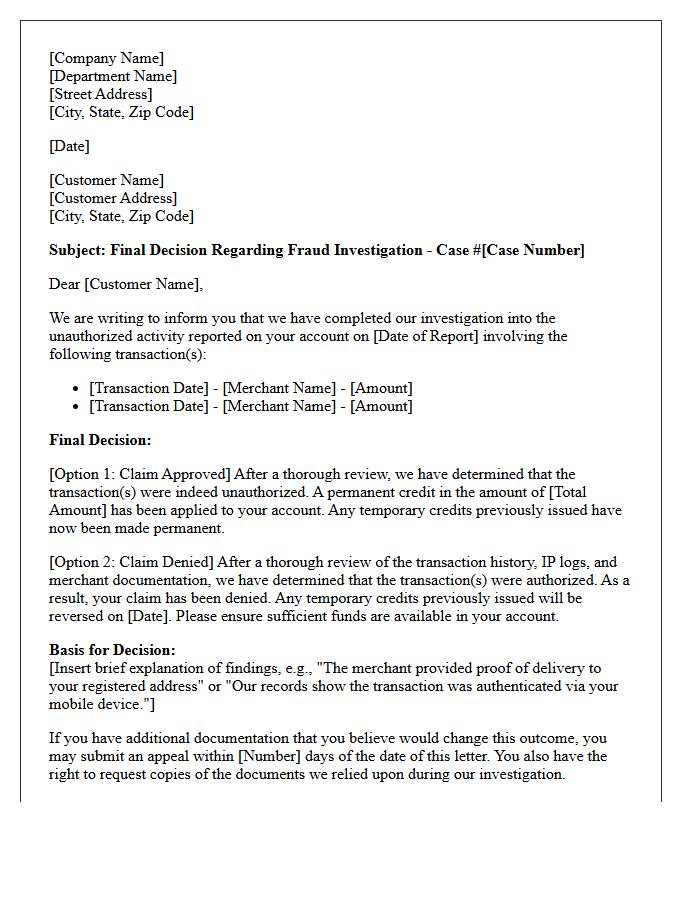

Fraud Investigation Final Decision Letter

A Fraud Investigation Final Decision Letter serves as the formal notification of a financial institution's ultimate ruling on a reported unauthorized transaction. This document clearly states whether the claim was approved, denied, or partially granted based on internal evidence. It typically outlines the reasoning behind the verdict, details regarding permanent account adjustments, and the consumer's right to request documents used during the process. Understanding this letter is essential for protecting your legal rights and determining if further appeals or regulatory escalations are necessary to resolve the dispute.

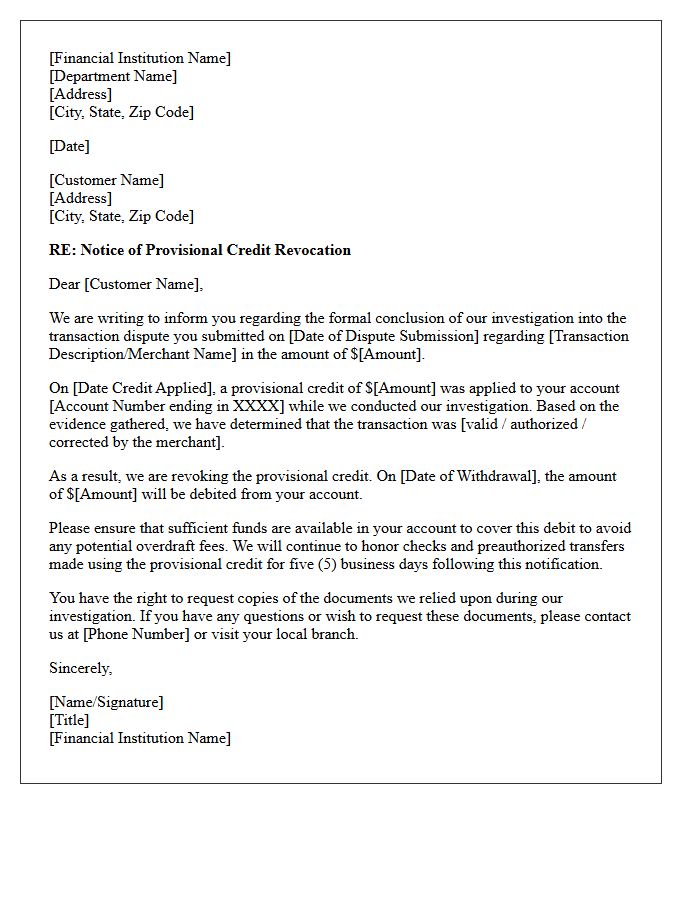

Provisional Credit Revocation Letter

A Provisional Credit Revocation Letter is a formal notice sent by a bank when a temporary credit issued during a transaction dispute is removed. This occurs if the investigation determines the charge was legitimate or if the merchant provided evidence against the claim. Once revoked, the disputed amount is debited from your account, potentially leading to overdrafts. It is crucial to review the reasons provided in the letter and submit additional documentation within the specified timeframe if you wish to appeal the final decision.

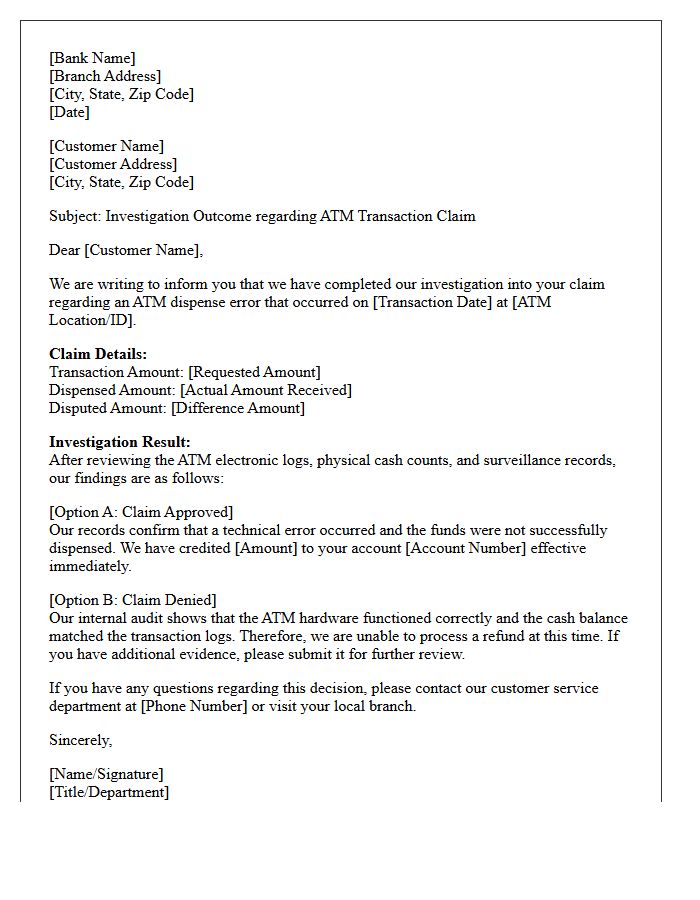

ATM Dispense Error Investigation Response Letter

An ATM Dispense Error Investigation Response Letter is a formal notification sent by a bank to a customer regarding a reported transaction failure. This document confirms whether the disputed amount will be credited back to the account after a technical audit. It outlines the findings of the investigation, including transaction logs and physical cash reconciliation. If the claim is denied, the letter must provide a clear explanation for the discrepancy. Understanding this response is crucial for ensuring financial accuracy and protecting consumer rights during banking disputes.

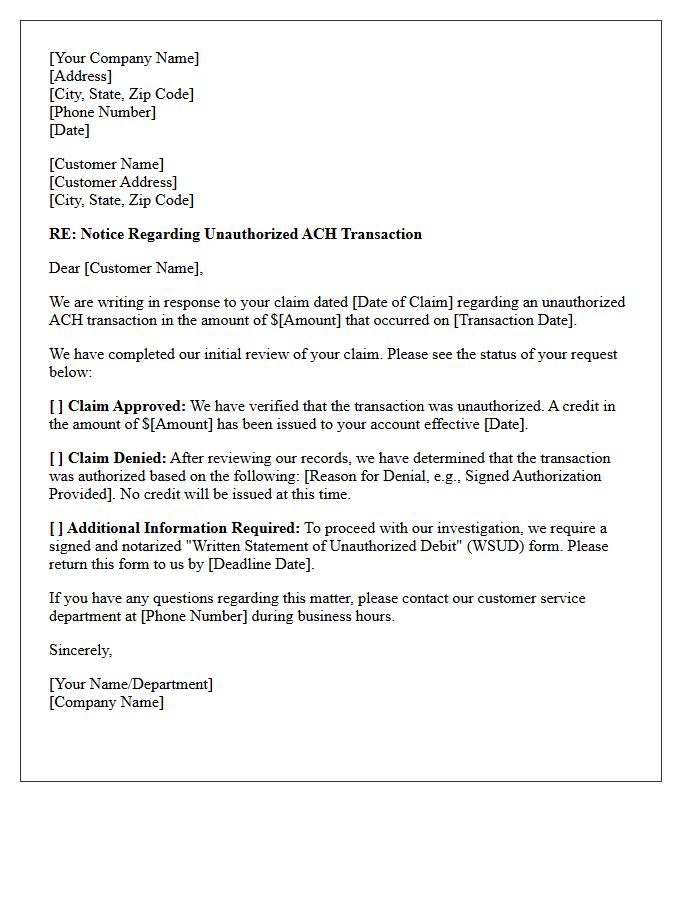

ACH Unauthorized Transaction Response Letter

An ACH Unauthorized Transaction Response Letter is a formal document sent by a financial institution to notify a merchant or originator that a transaction was disputed by the account holder. This notice usually includes a specific Return Reason Code, such as R05, R07, or R10, indicating the debit was not permitted. Upon receipt, businesses must immediately cease future originations for that account to remain NACHA compliant. To challenge a claim, you must provide a valid Letter of Authorization or a digital signature proving the customer gave explicit consent for the transfer.

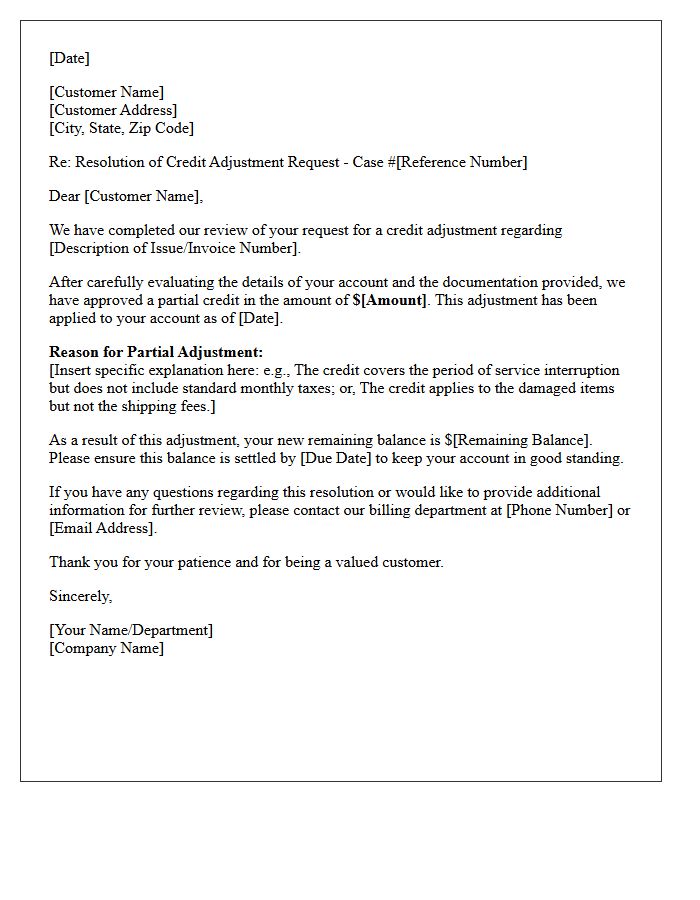

Partial Credit Adjustment Resolution Letter

A Partial Credit Adjustment Resolution Letter is a formal notification from a creditor or service provider confirming a limited refund or account correction. Unlike a full reversal, this document specifies the exact amount credited back to the consumer after a dispute or billing error review. It serves as official documentation for your financial records, outlining the remaining balance and the reasoning behind the specific adjustment. Carefully reviewing this letter ensures that the agreed-upon settlement aligns with your account statement and helps maintain accurate credit reporting consistency.

Dispute Investigation Additional Information Request Letter

A Dispute Investigation Additional Information Request Letter is a formal notice sent by a credit bureau or financial institution when submitted evidence is insufficient. To protect your consumer rights, you must respond promptly with the requested documentation, such as billing statements or identity proof. Failure to provide these specifics often leads to the investigation being closed without resolution. Providing clear, verifiable evidence ensures a thorough review of your claim, helping to correct inaccuracies and maintain an accurate credit report or account history effectively.

Duplicate Billing Dispute Resolution Letter

A Duplicate Billing Dispute Resolution Letter is a formal document used to rectify erroneous charges occurring when a vendor bills twice for the same service. To ensure a quick recovery of funds, clearly state the transaction dates, invoice numbers, and the specific amount overcharged. Attaching proof of payment, such as bank statements or receipts, is essential for a successful resolution. Send this letter via certified mail to maintain a legal paper trail, protecting your consumer rights and ensuring your financial records remain accurate and balanced.

Identity Theft Investigation Response Letter

An Identity Theft Investigation Response Letter is a formal document sent by a business or credit bureau after reviewing a fraud claim. It is crucial to verify if the disputed accounts were removed or corrected. If the investigation concludes the activity was legitimate, you must provide additional identity theft reports or police documentation to appeal the decision. Always keep a copy of this correspondence to maintain a legal paper trail for your financial recovery and to ensure your credit report accuracy is fully restored under federal law.

Merchant Refund Confirmation Letter

A Merchant Refund Confirmation Letter serves as official written proof that a business has initiated a repayment to a customer. This document is essential for tracking transaction reversals and resolving potential disputes with banks. It typically includes the transaction date, the total amount returned, and the original order reference. For consumers, this letter provides financial security by confirming when funds will reappear in their account. Always retain this confirmation as a formal receipt to ensure accounting accuracy and to verify that the refund process is successfully completed.

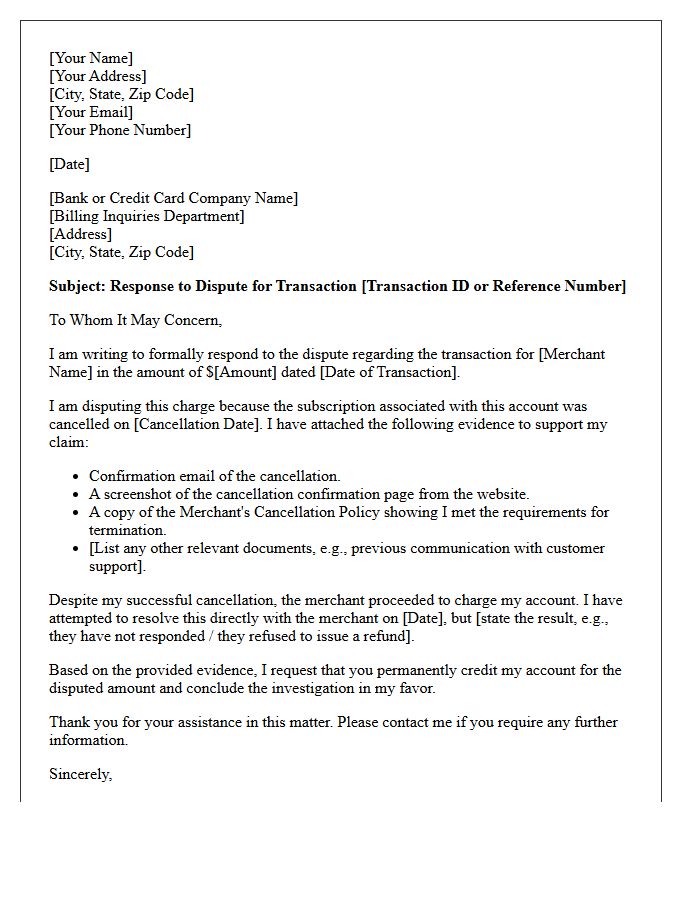

Cancelled Subscription Dispute Response Letter

When drafting a Cancelled Subscription Dispute Response Letter, you must provide clear evidence of cancellation. This document serves as a formal rebuttal to unauthorized charges occurring after a service was terminated. Essential components include the original cancellation confirmation number, the date of request, and relevant screenshots of communication. By presenting a factual timeline, you protect your consumer rights and facilitate a chargeback through your bank. Timeliness is critical; responding immediately ensures the financial institution can resolve the billing error and recover your funds efficiently.

What is a transaction dispute investigation response letter?

A transaction dispute investigation response letter is a formal document issued by a merchant or financial institution providing the findings and final decision regarding a contested charge. It outlines whether the dispute has been accepted, denied, or requires further evidence based on the investigation results.

What information should be included in a dispute response letter?

The letter should include the original transaction date, the specific transaction amount, the reference or case number, a summary of the investigation findings, and the final resolution. It should also clearly state any actions taken, such as a permanent credit or the re-billing of the transaction.

How long does it take to receive a response after a dispute is filed?

Under the Electronic Fund Transfer Act and Fair Credit Billing Act, financial institutions typically provide a formal response within 10 to 90 days. The specific timeline depends on the complexity of the investigation and whether a provisional credit was issued during the process.

Can a transaction dispute be reopened after a final response letter is sent?

Yes, a dispute can often be reopened if the consumer or merchant provides new, compelling evidence that was not available during the initial investigation. The response letter usually outlines the specific timeframe and procedure for appealing the decision.

What are common reasons for a dispute investigation to be denied?

A dispute is commonly denied if the merchant provides "compelling evidence" such as a signed delivery receipt, IP address tracking for digital goods, or proof that the transaction adhered to the merchant's posted cancellation policy. Failure to report the dispute within the legal timeframe can also lead to a denial.

Comments