A Final Demand for Payment is the ultimate formal notice sent to a business debtor before escalating to legal action or professional debt collection. This critical document establishes a firm deadline for settling commercial arrears to protect your company's cash flow and legal rights. To help you resolve outstanding balances quickly, below are some ready to use template.

Image cover: Commercial Debt Final Demand: Templates and Professional Samples

Letter Samples List

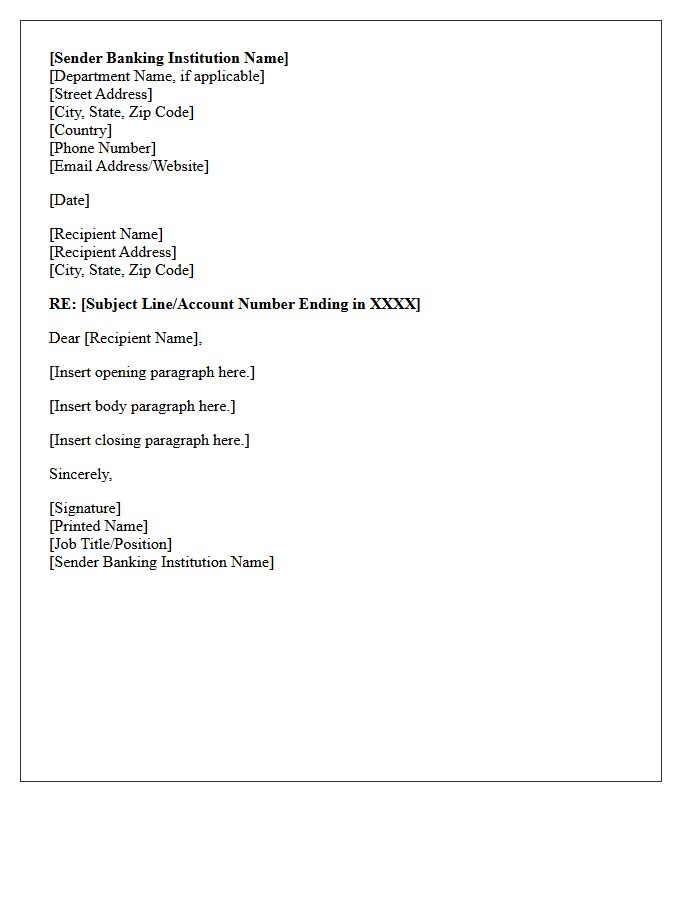

- Sender Banking Institution Name and Address

- Date of Final Demand Letter Issuance

- Debtor Commercial Business Name and Address

- Subject Letter for Final Demand on Commercial Debt

- Formal Salutation to the Commercial Debtor

- Reference to the Specific Corporate Account Number

- Declaration of the Outstanding Principal Balance

- Itemization of Accumulated Interest and Penalties

- Demand for Immediate Payment in Full

- Specific Final Deadline for Debt Remittance

- Notice of Impending Legal Action and Asset Seizure

- Direct Contact Information for the Recovery Department

- Formal Closing Statement of the Letter

- Signature of the Authorized Bank Collection Officer

Sender Banking Institution Name and Address

When initiating a wire transfer, providing the correct Sender Banking Institution Name and Address is essential for transaction security and regulatory compliance. This information identifies the originating bank, ensuring funds are traced correctly through the global financial network. You must include the bank's full legal title and the physical headquarters address or specific branch location to prevent processing delays. For international transfers, these details work alongside the SWIFT/BIC code to verify the source of capital, helping institutions adhere to anti-money laundering (AML) protocols and ensuring your payment is processed smoothly.

Date of Final Demand Letter Issuance

The Date of Final Demand Letter Issuance is a critical legal milestone marking the formal conclusion of informal recovery attempts. It serves as the official commencement for calculating statutory deadlines and pre-litigation notice periods. This specific date establishes the final window for a debtor to resolve outstanding obligations before formal legal action or litigation begins. Accurate documentation of this issuance is essential for maintaining a clear evidentiary trail and ensuring procedural compliance in judicial proceedings or formal debt collection workflows.

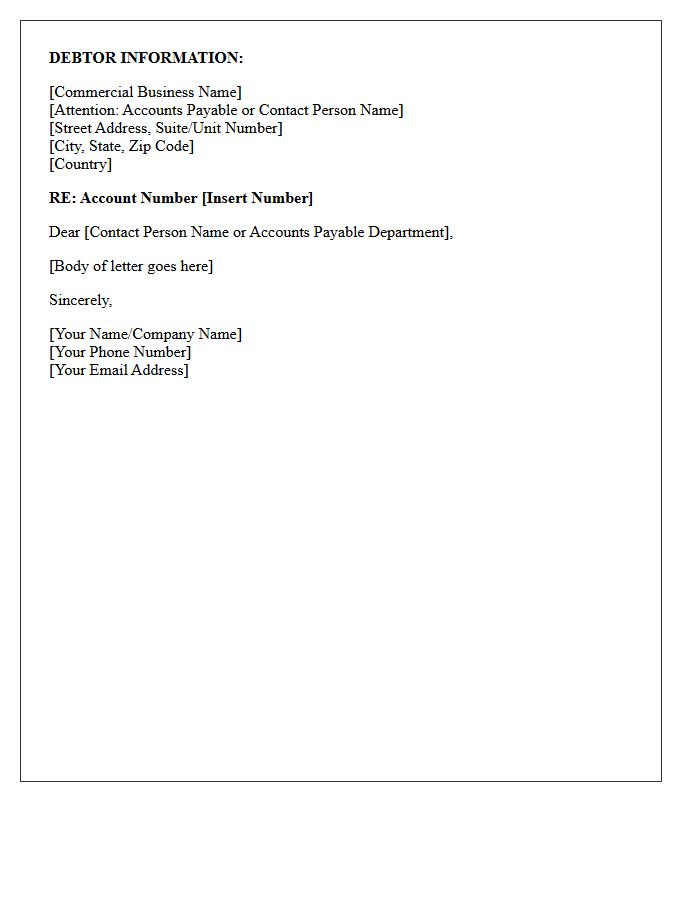

Debtor Commercial Business Name and Address

When recording a security interest, the Debtor Commercial Business Name must exactly match the legal entity name found on official public organic records, such as the Articles of Incorporation. Even minor spelling errors or missing suffixes like "Inc." or "LLC" can render a filing seriously misleading and legally ineffective. Additionally, the registered business address identifies the correct jurisdiction for filing. Providing precise, verified information ensures the secured party maintains priority status and protects their legal claim against the entity's assets in the event of a default.

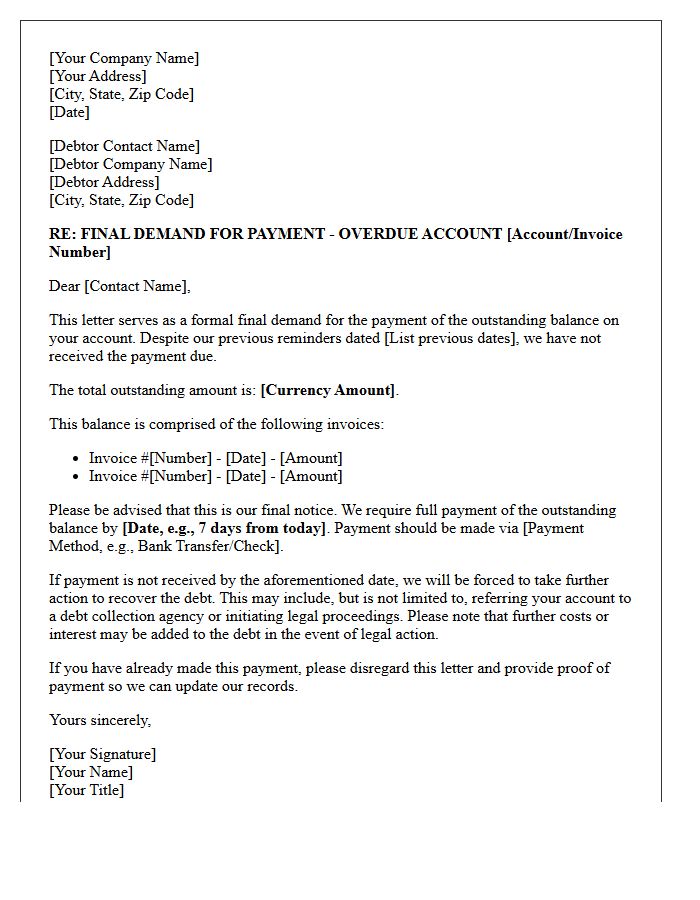

Subject Letter for Final Demand on Commercial Debt

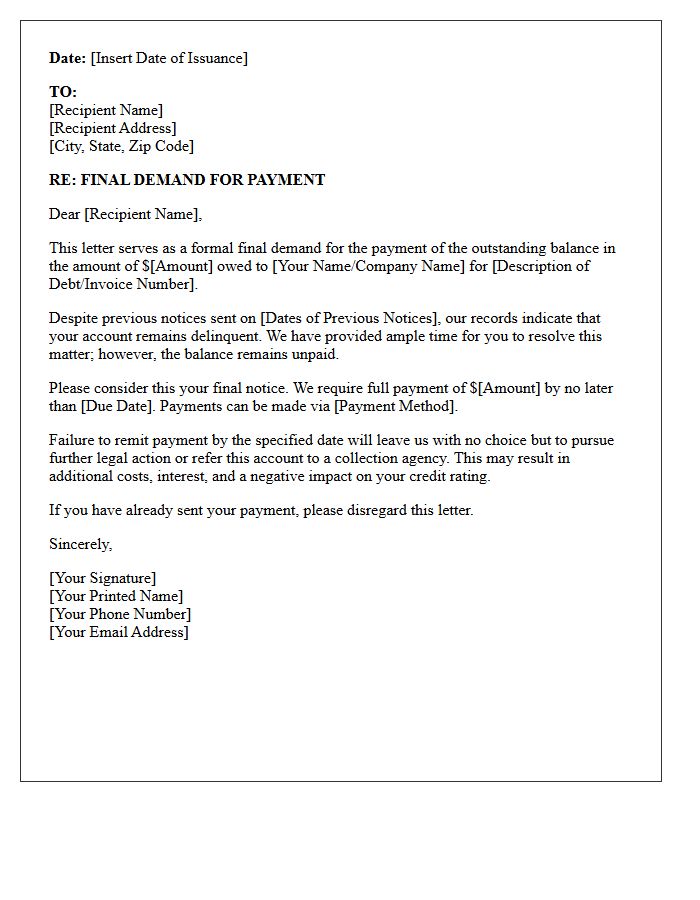

A Final Demand Letter is a critical legal document used to recover unpaid commercial debt before initiating litigation. It serves as a formal notice, clearly stating the outstanding balance, original due date, and a firm deadline for payment. By explicitly mentioning "late payment interest" and potential legal action, it creates urgency and provides evidence of a good-faith attempt to settle out of court. This letter is essential for professional debt collection, ensuring compliance with commercial regulations while protecting your business's cash flow and legal rights during the recovery process.

Formal Salutation to the Commercial Debtor

When drafting a formal salutation to a commercial debtor, professionalism is vital to maintain legal enforceability and professional decorum. Address the recipient using their full legal name or official title to ensure clarity in communication. Using a neutral opening like "Dear [Name]" or "To the Management of [Company]" establishes a serious tone for debt recovery efforts. Avoid informal language to preserve the credibility of your claim and ensure the correspondence meets standard business protocols for potential future litigation.

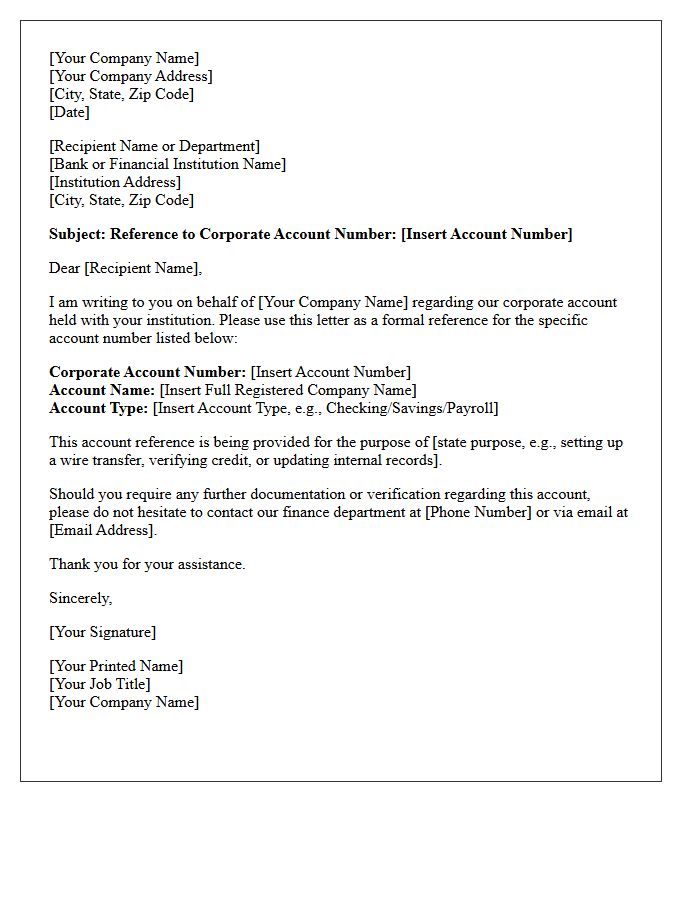

Reference to the Specific Corporate Account Number

When conducting business transactions, the Specific Corporate Account Number serves as a unique identifier for your organization's financial profile. It is essential for ensuring that payments and official records are accurately matched to the correct entity. Always include this reference in wire transfers and billing correspondence to prevent processing delays. Keeping this number secure yet accessible simplifies financial reconciliation and enhances the efficiency of corporate auditing processes. Providing the correct reference ensures your corporate identity remains verified across all global banking and regulatory platforms.

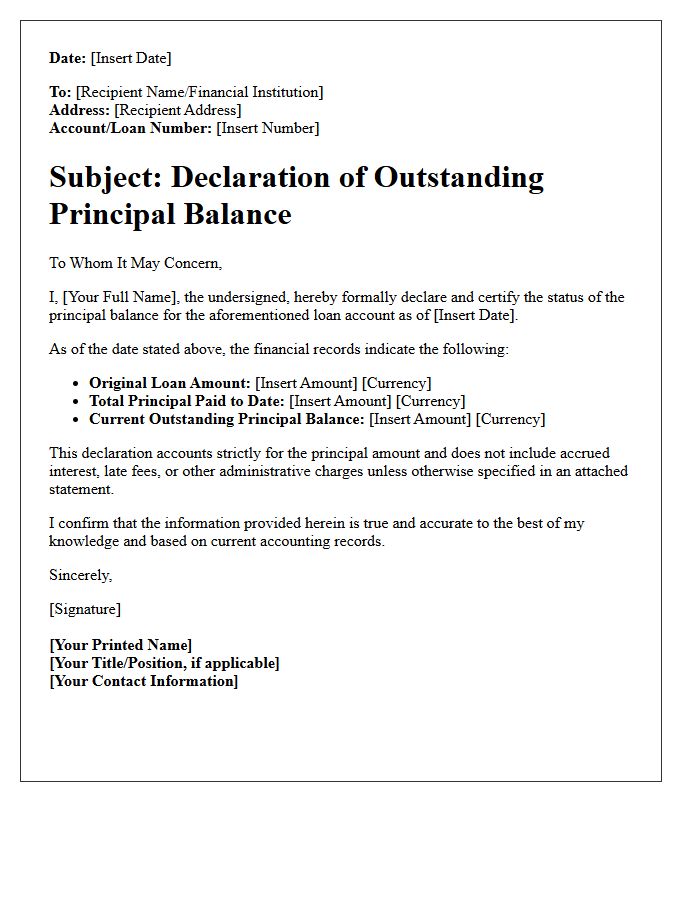

Declaration of the Outstanding Principal Balance

A Declaration of the Outstanding Principal Balance is a formal document verifying the exact remaining debt on a loan or mortgage. It excludes future interest, providing a precise payoff figure essential for refinancing, property sales, or legal settlements. This statement ensures transparency between lenders and borrowers, confirming that all prior payments were correctly applied. Understanding this figure is vital for financial planning, as it represents the actual capital required to satisfy the lien and clear the title of the asset.

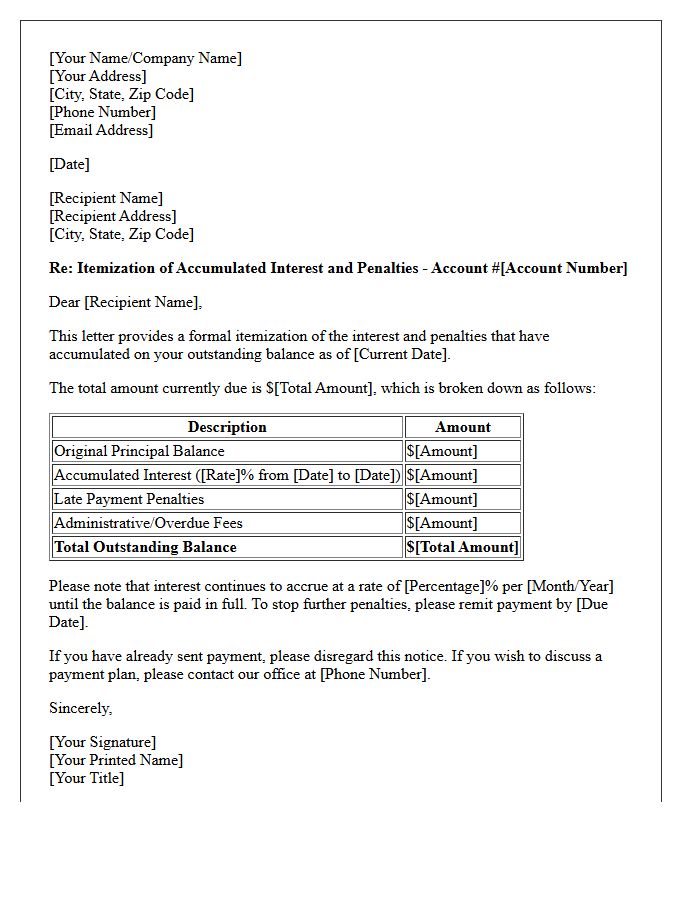

Itemization of Accumulated Interest and Penalties

Taxpayers must understand that an Itemization of Accumulated Interest and Penalties provides a detailed breakdown of additional charges added to a primary tax debt. Interest is typically calculated based on the outstanding balance, while penalties accrue due to late filing or payment. Reviewing this document is essential for verifying calculation accuracy and identifying potential eligibility for abatement. Keeping precise records ensures financial transparency and helps individuals manage their total tax liability effectively by understanding exactly how much is owed beyond the original principal amount.

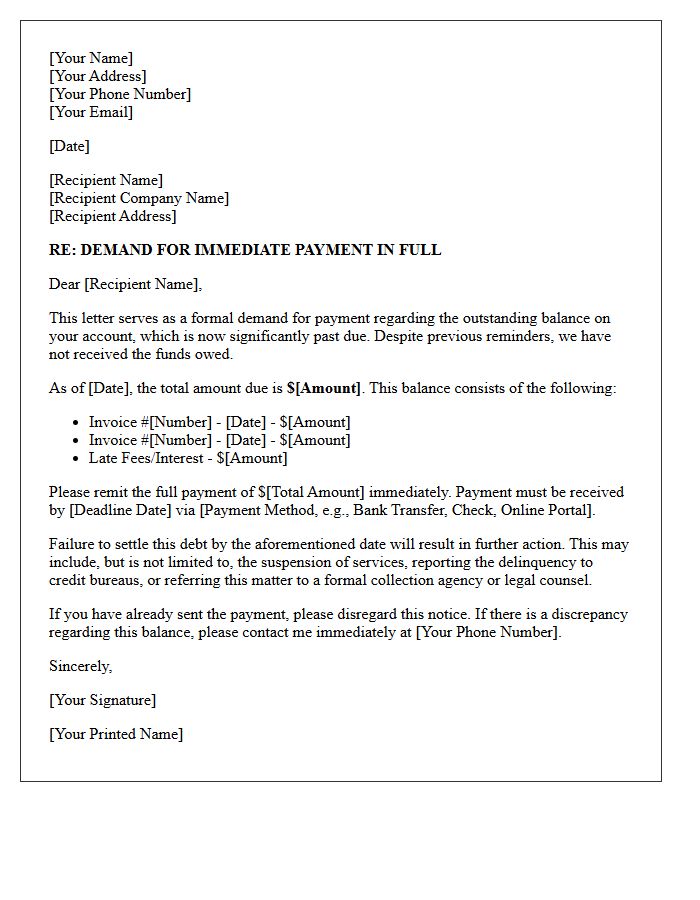

Demand for Immediate Payment in Full

A demand for immediate payment in full is a formal legal notice issued when a borrower defaults on a contract. This process, often triggered by an acceleration clause, mandates the total outstanding balance be paid at once rather than through installments. Failure to comply typically leads to severe consequences, including foreclosure, asset repossession, or litigation. Receiving this notice signifies that the grace period has ended, making it critical to seek legal counsel or negotiate a settlement immediately to avoid further financial penalties and permanent credit damage.

Specific Final Deadline for Debt Remittance

The Specific Final Deadline for debt remittance is the absolute cutoff date for settling outstanding financial obligations. Missing this statutory maturity date can trigger severe consequences, including late penalties, legal action, or a total forfeiture of rights. It is essential to verify whether the deadline follows the accrual method or a grace period policy. Ensuring payment reaches the creditor before this terminal window closes is vital for maintaining a positive credit standing and avoiding involuntary collection procedures or litigation risks.

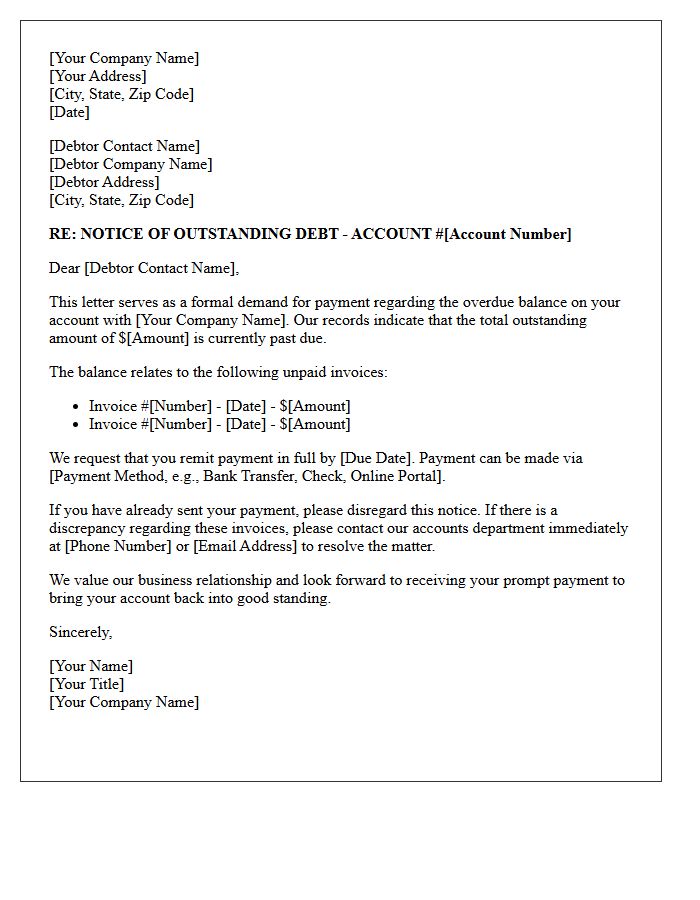

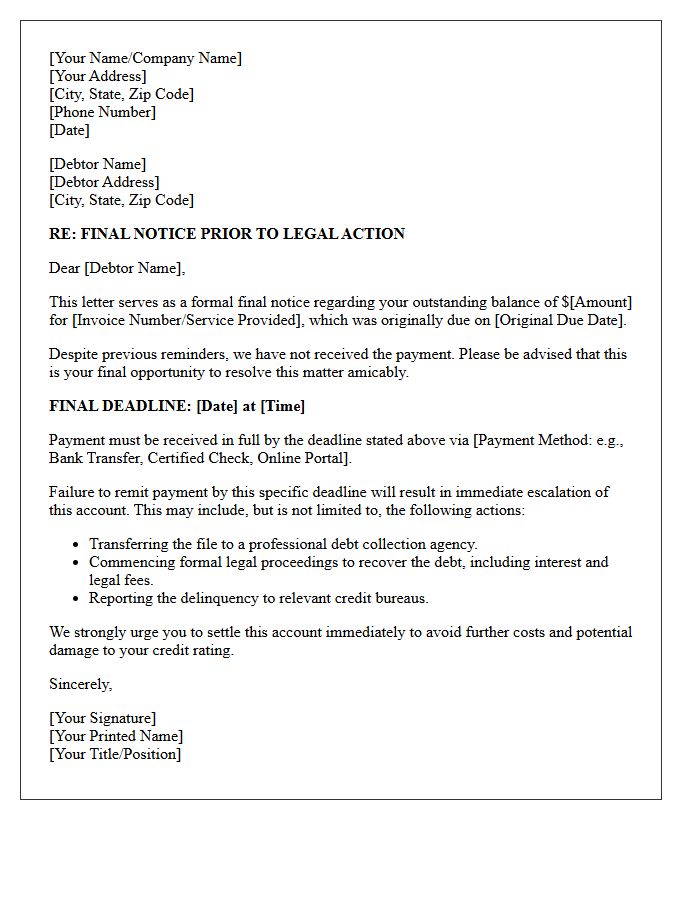

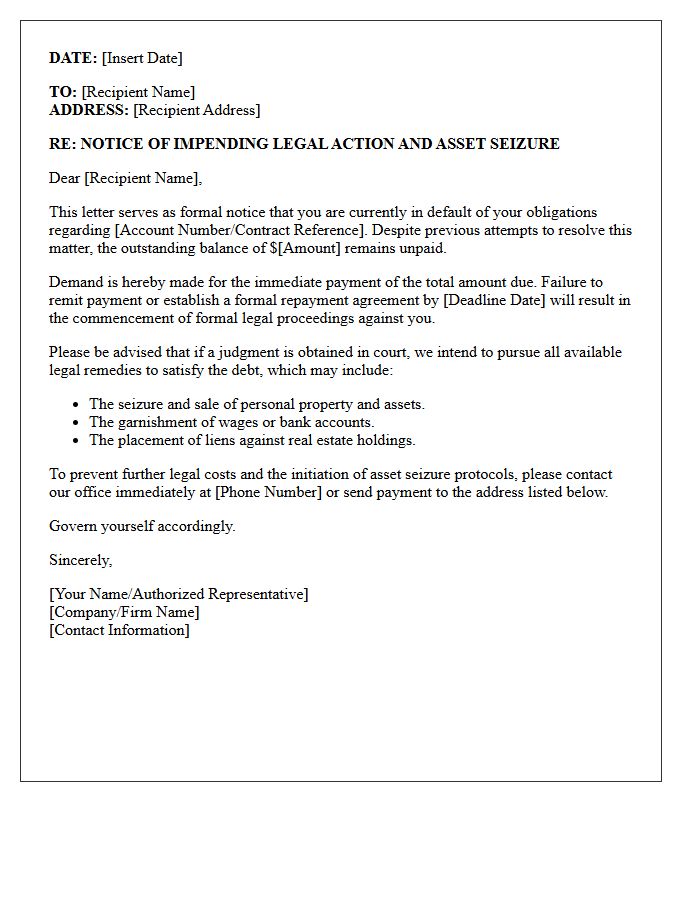

Notice of Impending Legal Action and Asset Seizure

A Notice of Impending Legal Action and Asset Seizure is a formal warning that a creditor or government agency intends to freeze bank accounts, garnish wages, or claim physical property to satisfy an outstanding debt. This document signals the final stage before litigation or enforcement actions begin. It is critical to verify the notice's authenticity immediately to avoid identity theft or fraudulent scams. Seeking legal counsel during this period is essential to negotiate settlements, file disputes, or protect exempt assets from being lawfully seized under judicial orders.

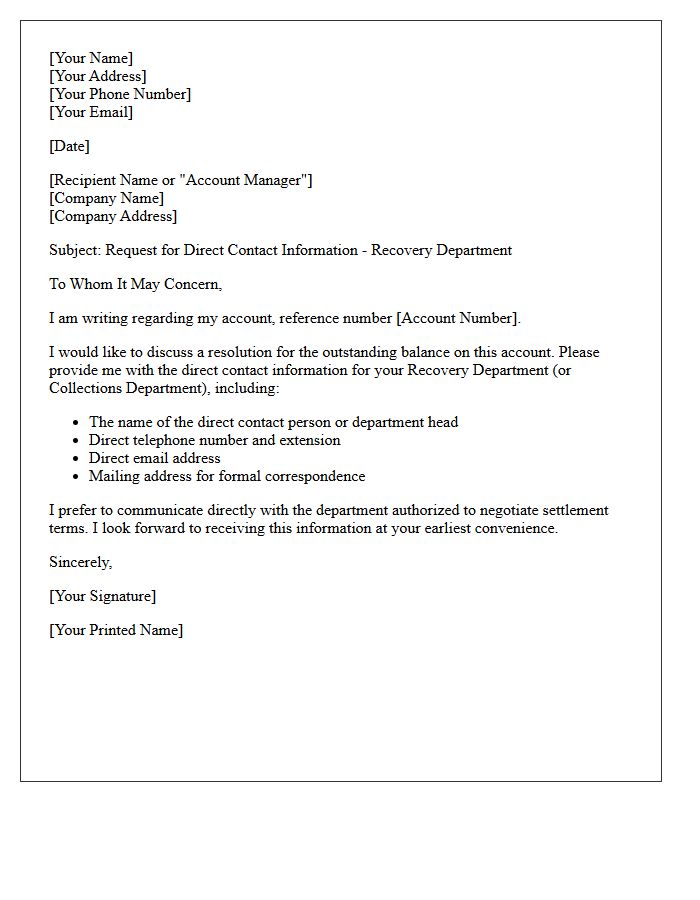

Direct Contact Information for the Recovery Department

Having Direct Contact Information for the Recovery Department is essential for resolving outstanding debts or account delinquencies efficiently. Direct access allows you to bypass general customer service queues, connecting you immediately with specialists authorized to negotiate payment plans or settlements. When calling, ensure you have your account number and financial details ready to expedite the debt resolution process. Utilizing verified direct lines or secure internal extensions ensures clear communication and faster account restoration, helping you maintain financial stability and protect your credit standing through professional, one-on-one assistance.

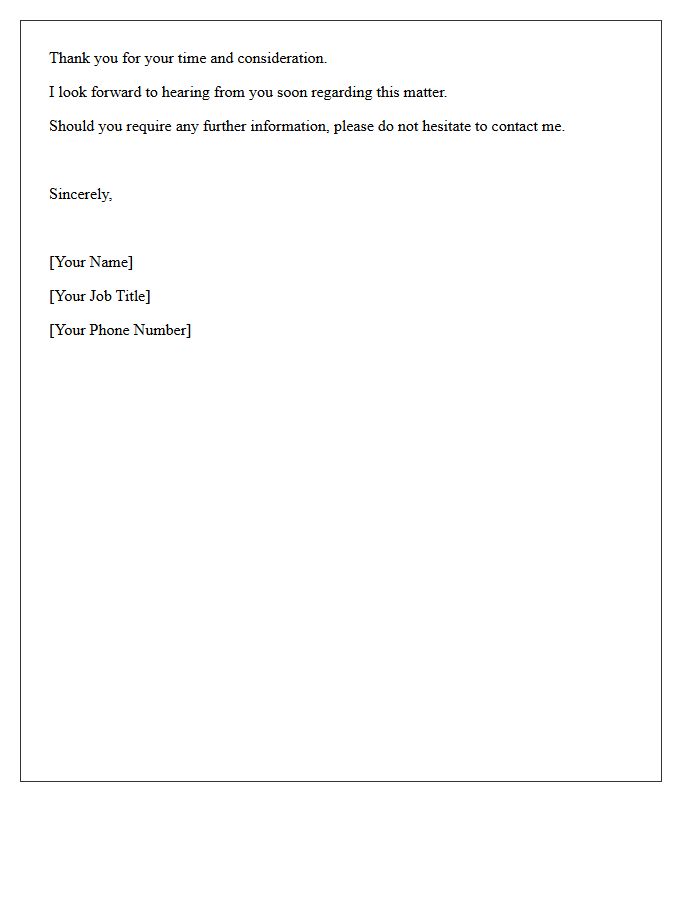

Formal Closing Statement of the Letter

A formal closing statement, or complimentary close, is essential for maintaining professional etiquette and signalizing the end of correspondence. The choice of phrase depends on your relationship with the recipient. Use "Yours faithfully" when the name is unknown and "Yours sincerely" for addressed individuals. In modern business, "Best regards" or "Respectfully" are widely accepted. Ensure the closing is followed by a comma, a space for your signature, and your printed name to ensure clarity and respect throughout the document.

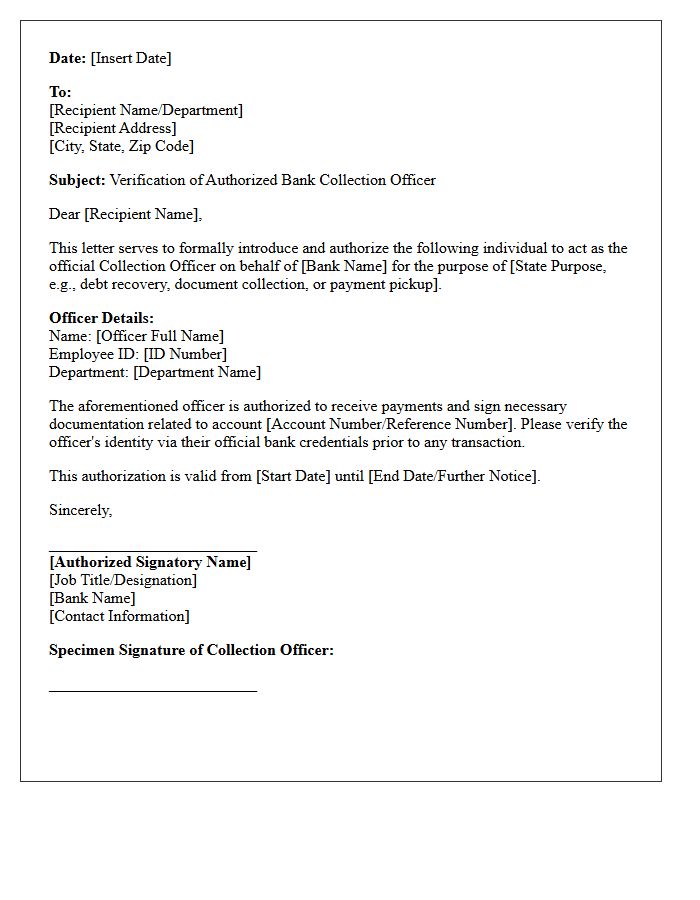

Signature of the Authorized Bank Collection Officer

The Signature of the Authorized Bank Collection Officer serves as a critical verification mechanism for financial transactions. This formal endorsement confirms that a payment has been officially received and processed by the institution. It ensures the authenticity of deposit slips or collection receipts, protecting both the client and the bank against fraud. When conducting over-the-counter transactions, always ensure this signature is present alongside the bank's official stamp to validate your proof of payment and maintain accurate legal records of the settled obligation.

What is a final demand for payment on commercial debt?

A final demand for payment is a formal notice sent by a creditor to a business debtor, serving as the last opportunity to settle an outstanding invoice before legal action is initiated or the account is referred to a collection agency.

What should be included in a commercial final demand letter?

A legally compliant final demand should include the total amount owed, the original invoice numbers, the specific due date for payment, the methods of payment accepted, and a clear statement of the consequences if the debt remains unpaid by the deadline.

How much time is typically given in a final demand notice?

In commercial debt collection, it is standard practice to provide a period of 7 to 14 days from the date of the letter for the debtor to clear the balance or enter into a formal payment plan.

Can I charge interest and late fees in a final demand for payment?

Yes, provided the original commercial contract or terms and conditions allow for it. In many jurisdictions, businesses are also entitled to claim statutory interest and reasonable debt recovery costs under late payment legislation.

What happens if a business ignores a final demand for payment?

If a business fails to respond to a final demand, the creditor typically proceeds with legal remedies, which may include filing a lawsuit for breach of contract, issuing a statutory demand, or initiating insolvency proceedings to recover the debt.

Comments