A Notification of Collateral Repossession is a formal legal document issued by lenders when a borrower defaults on a secured loan. This notice informs the debtor that their asset has been seized to satisfy the outstanding debt obligations. Understanding your legal rights and the required timelines is essential during this process. To assist you, below are some ready to use template.

Image cover: Professional Collateral Repossession Notice Templates and Examples

Letter Samples List

- Letter of Intent to Repossess Collateral

- Final Demand Letter Prior to Collateral Repossession

- Official Notification Letter of Asset Repossession

- Letter of Default and Right to Cure Before Repossession

- Notice Letter of Impending Collateral Seizure

- Voluntary Surrender Letter for Pledged Collateral

- Pre-Repossession Grace Period Notice Letter

- Third-Party Repossession Agency Authorization Letter

- Post-Repossession Letter of Intent to Sell Collateral

- Right of Redemption Letter Following Asset Repossession

- Deficiency Balance Notification Letter After Repossession Sale

- Collateral Repossession Cancellation Letter Upon Account Settlement

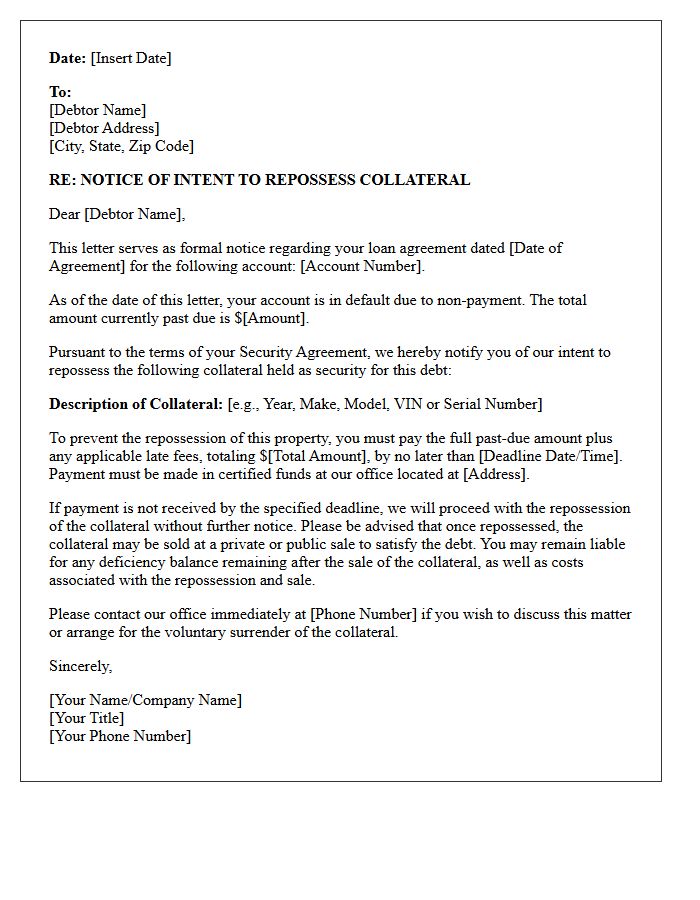

Letter of Intent to Repossess Collateral

A Letter of Intent to Repossess Collateral is a formal legal notice sent by a creditor to a debtor in default. It serves as a final warning that the lender plans to seize secured assets, such as a vehicle or property, to satisfy an unpaid debt. This document typically outlines the default amount, provides a specific deadline for payment, and explains the debtor's right to redemption. Receiving this letter is a critical signal to take immediate action or seek legal counsel to prevent the loss of personal property.

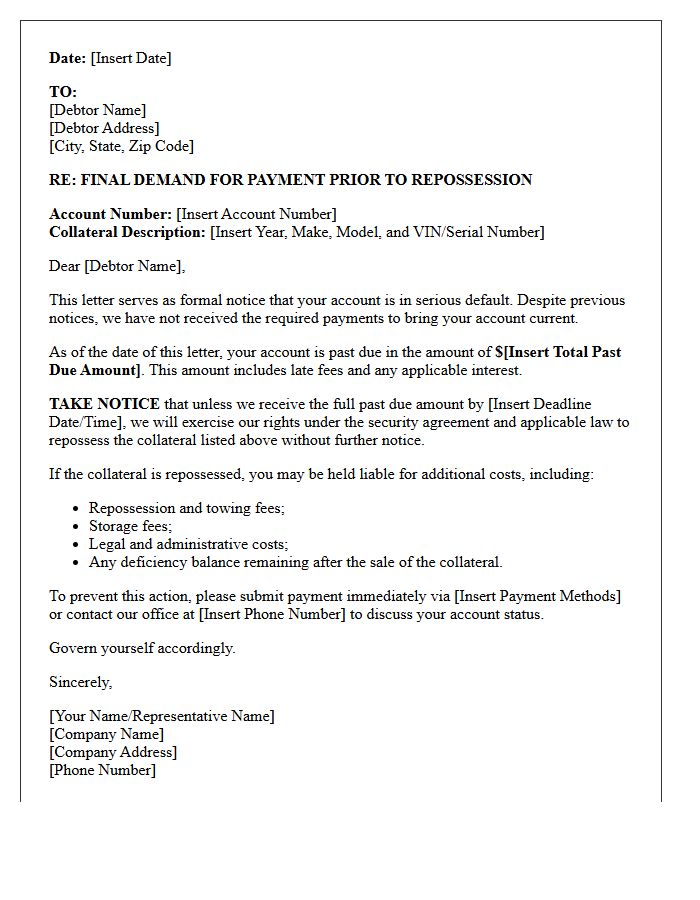

Final Demand Letter Prior to Collateral Repossession

A Final Demand Letter is a formal legal notice issued before a lender initiates collateral repossession. This document serves as the last opportunity for a debtor to cure a default, typically through full payment or specific remedial action, within a strict deadline. It outlines the intent to seize assets, such as vehicles or equipment, used to secure the loan. Receiving this letter indicates that the grace period has ended and legal recovery actions are imminent, potentially leading to significant credit damage and additional collection costs if left unaddressed.

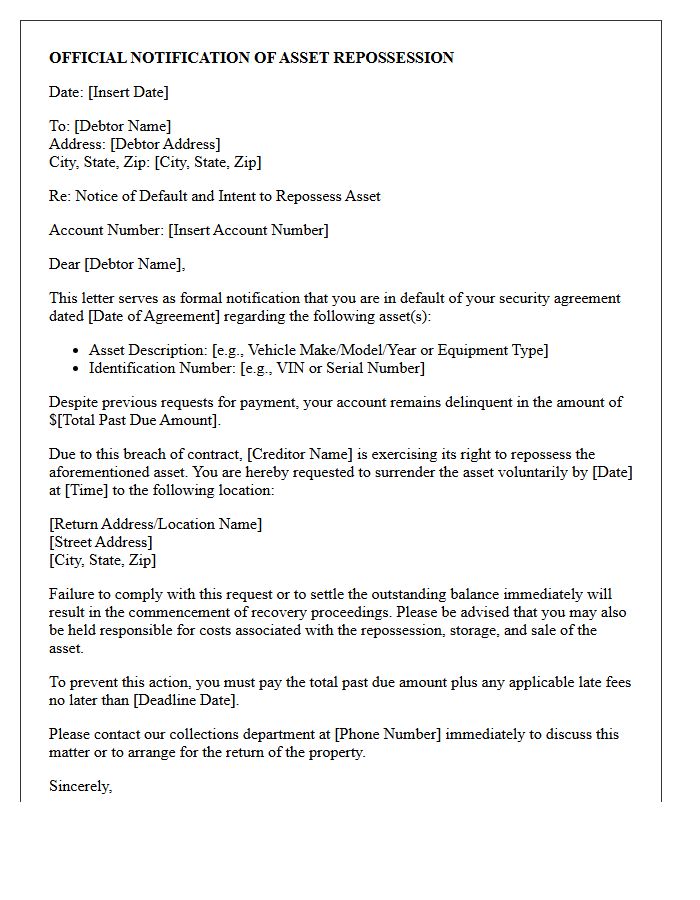

Official Notification Letter of Asset Repossession

An Official Notification Letter of Asset Repossession is a formal legal document issued by a creditor when a borrower defaults on a secured loan. It signifies the lender's intent to seize collateral, such as a vehicle or property, to recover outstanding debt. This notice typically details the specific default reason, the deadline to cure the deficiency, and potential legal consequences. Receiving this letter is critical, as it serves as the final warning before physical seizure occurs, highlighting the urgent need for professional legal counsel or immediate repayment negotiations to protect your rights.

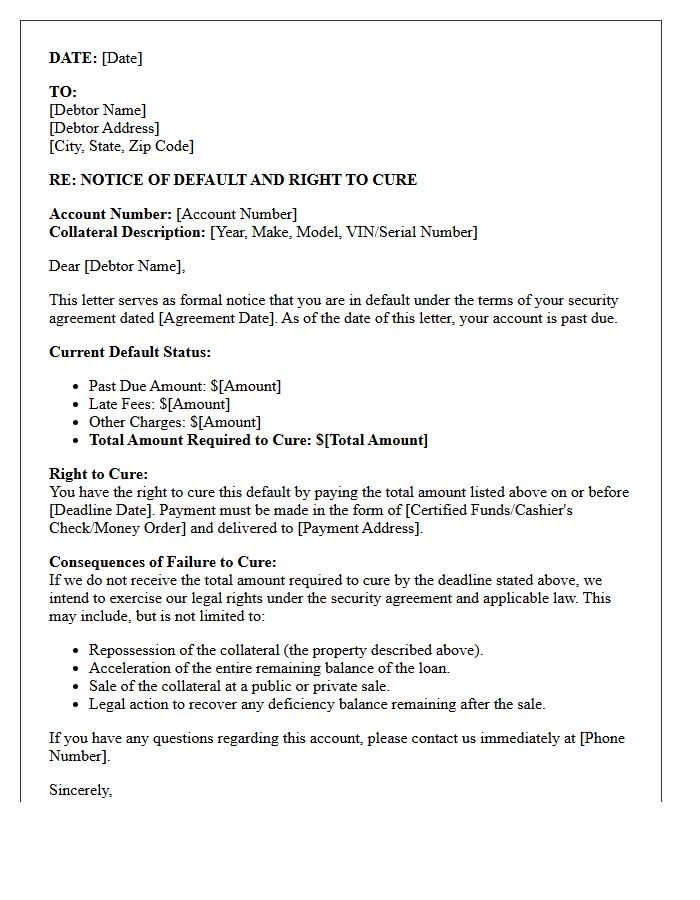

Letter of Default and Right to Cure Before Repossession

A Letter of Default is a formal notice sent by a creditor when a borrower misses payments. This document serves as a legal warning before a vehicle or property is seized. The most critical element is the Right to Cure, which grants the borrower a specific timeframe-typically 15 to 30 days-to pay the overdue balance and late fees. Successfully exercising this right reinstates the contract and prevents immediate repossession. Ignoring this notice waives your protections, allowing the lender to reclaim the collateral without further court intervention.

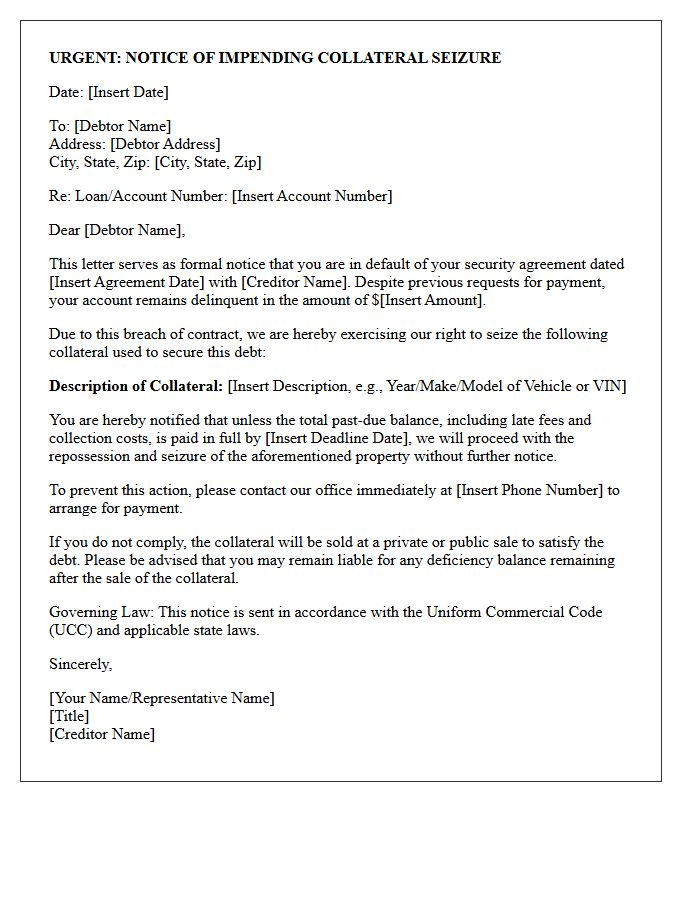

Notice Letter of Impending Collateral Seizure

A Notice Letter of Impending Collateral Seizure is a formal warning issued by a creditor indicating their intent to repossess assets due to loan default. This legal document specifies a deadline for the borrower to settle outstanding debts or face the loss of secured property, such as a vehicle or home. To prevent immediate seizure, it is crucial to communicate with the lender, seek legal counsel, or arrange a repayment plan before the notice period expires. Acting quickly is the best way to protect your financial interests and retain ownership of your collateral.

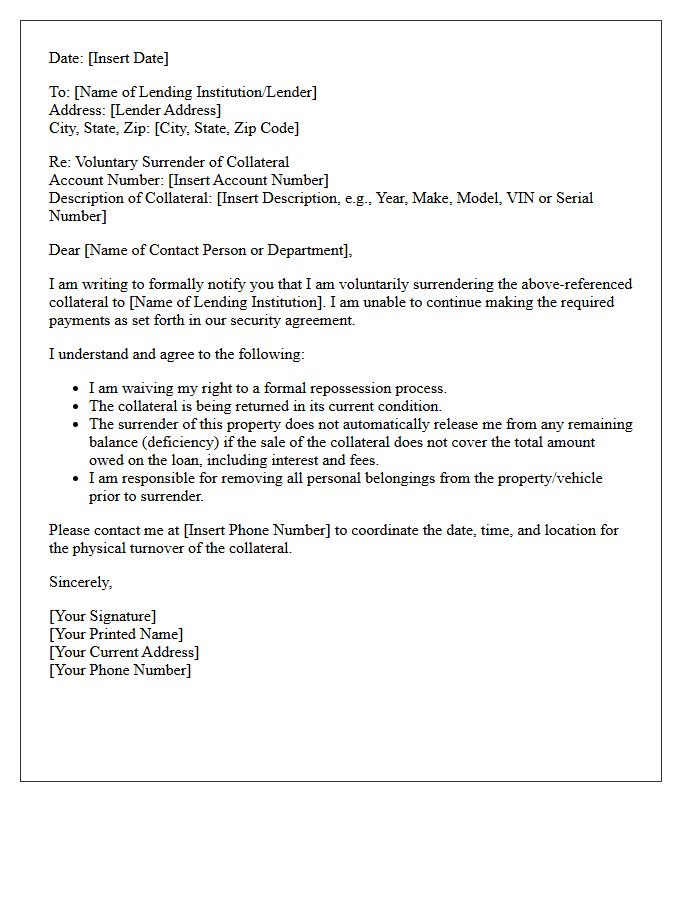

Voluntary Surrender Letter for Pledged Collateral

A Voluntary Surrender Letter is a formal legal document used by a borrower to return pledged collateral to a lender after defaulting on a loan. By proactively giving up the asset, you may reduce repossession costs and mitigate further damage to your credit score. However, this action does not automatically waive a deficiency balance. If the sale of the asset fails to cover the total debt, you remain liable for the remaining amount. Always request a written release of liability to clarify your financial obligations after the transfer.

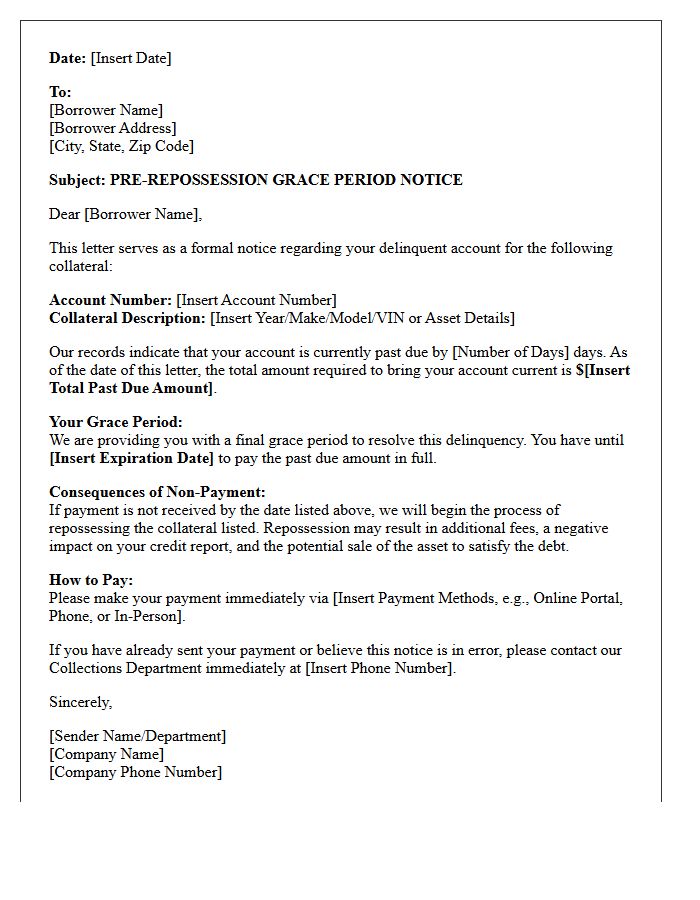

Pre-Repossession Grace Period Notice Letter

A Pre-Repossession Grace Period Notice Letter is a critical legal document sent by lenders to borrowers in default. This notice grants a specific timeframe, typically required by state law, to cure the delinquency before the vehicle is seized. It must detail the exact amount owed, including late fees, and provide a clear deadline for payment. Receiving this letter is your final opportunity to exercise reinstatement rights and prevent the loss of your asset. Promptly communicating with your creditor after receiving this mandatory warning is essential to maintaining ownership and protecting your credit score.

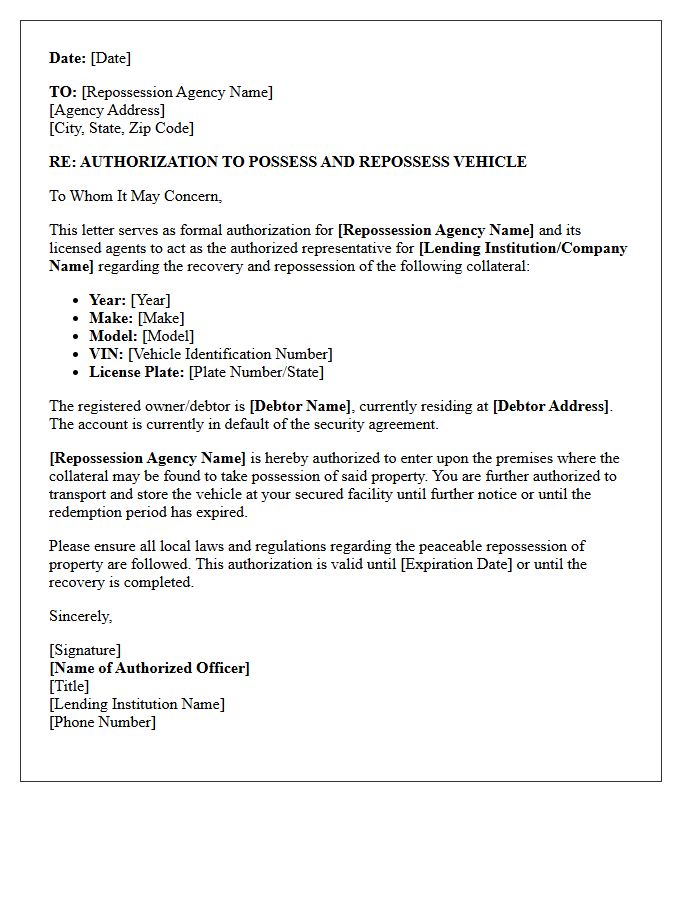

Third-Party Repossession Agency Authorization Letter

A Third-Party Repossession Agency Authorization Letter is a legal document granting a recovery firm the official mandate to seize collateral on behalf of a creditor. This letter serves as formal permission for agents to act as authorized representatives, ensuring compliance with privacy laws and state regulations. It must include specific details such as the debtor's information, asset description, and the scope of authority. Presenting this document is essential to verify the legality of the recovery process and to protect all parties from potential liability or wrongful repossession claims.

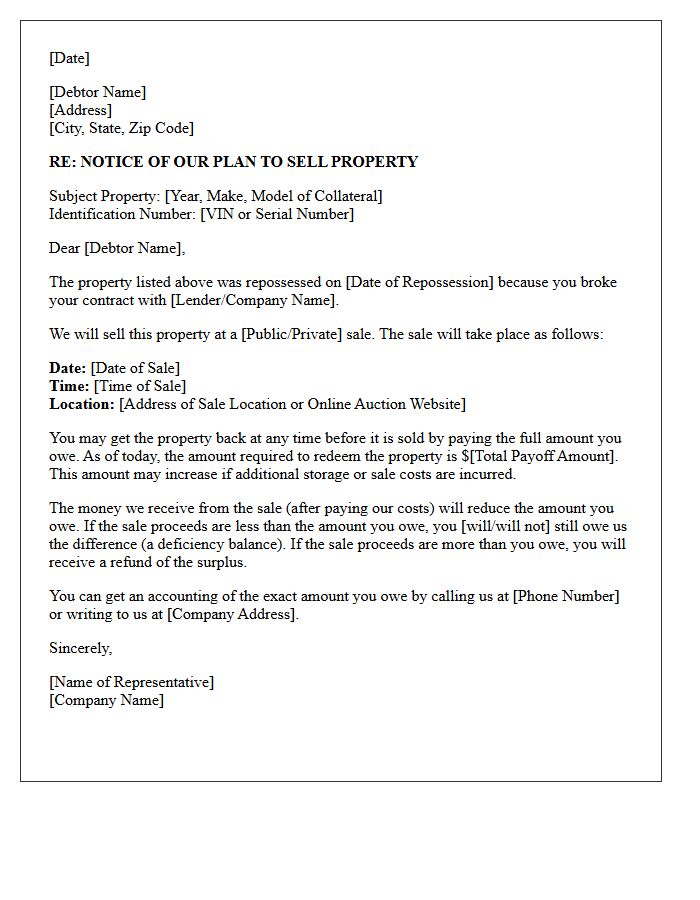

Post-Repossession Letter of Intent to Sell Collateral

A post-repossession letter of intent to sell collateral is a critical legal notice sent by a lender to a borrower. It officially declares the creditor's plan to dispose of the seized asset, usually through a private sale or public auction. This document is mandatory under the Uniform Commercial Code (UCC) to ensure transparency. It must specify the time, date, and location of the sale, while informing the borrower of their right to redeem the property by paying the full debt balance before the transaction is finalized.

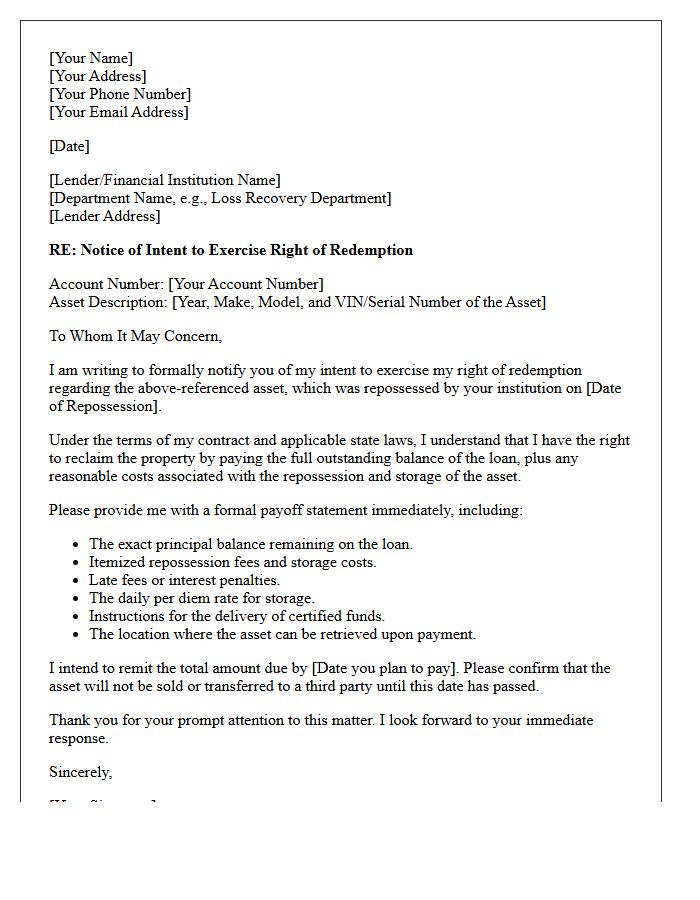

Right of Redemption Letter Following Asset Repossession

A Right of Redemption letter is a formal notice sent to a borrower after asset repossession, outlining the legal path to reclaim property. This document specifies the total payoff amount, including the outstanding loan balance, late fees, and storage costs. To successfully redeem the asset, the debtor must pay the full sum by the stated deadline. Understanding your state's specific statutory window is critical, as failure to act allows the lender to sell the collateral at auction to satisfy the debt.

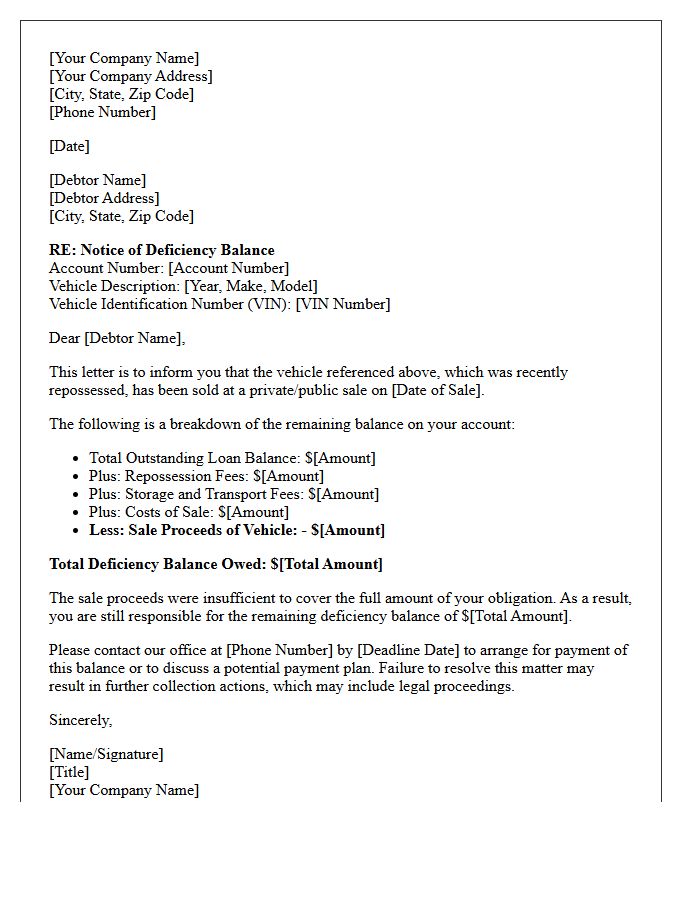

Deficiency Balance Notification Letter After Repossession Sale

A deficiency balance notification letter is a legal document sent by lenders after selling a repossessed vehicle. It informs you if the sale price failed to cover your total loan balance, late fees, and recovery costs. This notice must provide a detailed accounting of the transaction and state the final amount you still owe. Understanding this letter is crucial because it serves as the basis for future collection actions or lawsuits. Always verify the math and check local consumer protection laws to ensure the lender followed proper repossession and notification procedures.

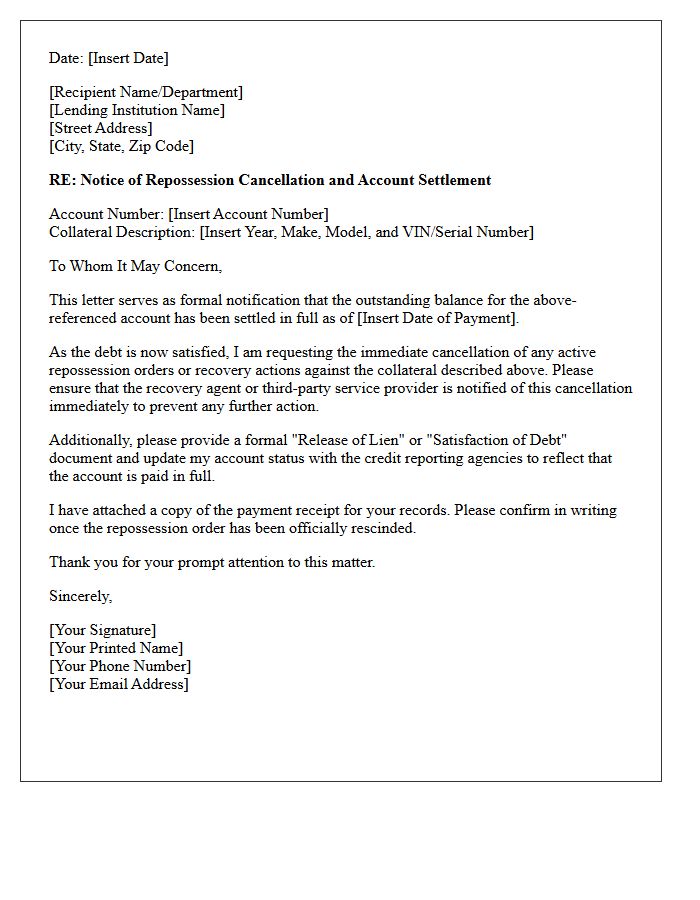

Collateral Repossession Cancellation Letter Upon Account Settlement

A Collateral Repossession Cancellation Letter serves as formal proof that a debt is fully paid, effectively halting any seizure actions. Once account settlement occurs, this document instructs recovery agents to cease collection efforts and release legal claims on the asset. It is a vital record for protecting your property rights and updating your credit history. Always ensure the lender provides this written confirmation promptly to prevent wrongful repossession and to verify that your financial obligations are officially satisfied, securing your ownership and peace of mind.

What is a Notification of Collateral Repossession?

A Notification of Collateral Repossession is a legal document sent by a lender to a borrower informing them that the asset used to secure a loan has been seized due to a default in payments or breach of contract.

What information is included in a repossession notice?

The notice typically includes a description of the seized collateral, the reason for the repossession, the total amount required to redeem the asset, and the date and location of any planned public or private sale of the property.

Can I get my property back after receiving a repossession notification?

Yes, borrowers usually have a specific timeframe to "redeem" the collateral by paying the full outstanding balance plus repossession fees, or to "reinstate" the loan by catching up on missed payments, depending on state law and the contract terms.

What happens if the sale of the repossessed item doesn't cover the loan balance?

If the collateral is sold for less than what is owed, the lender may issue a deficiency balance notice, holding the borrower responsible for the remaining debt plus legal and administrative costs.

How long does a lender have to send a notification after seizing collateral?

Under the Uniform Commercial Code (UCC), lenders are generally required to provide a written notice within a "reasonable" timeframe-often 10 days-before selling or disposing of the collateral to allow the borrower time to take action.

Comments