Receiving an Auto Loan Inadequate Collateral Notice of Denial means the vehicle's appraised value is too low to secure the requested loan amount. Lenders use this to mitigate risk when the asset doesn't sufficiently back the debt. Understanding this specific rejection reason is the first step toward improving your financing options. To assist your communication with lenders, below are some ready to use templates.

Image cover: Auto Loan Denial Templates: Managing Inadequate Collateral Notices

Letter Samples List

- Auto Loan Inadequate Collateral Denial Letter

- Notice of Denial for Inadequate Auto Collateral Letter

- Vehicle Value Insufficient Loan Rejection Letter

- Secured Auto Loan Collateral Shortfall Denial Letter

- Used Auto Loan Inadequate Collateral Notification Letter

- Bank Notice of Auto Loan Denial Due to Collateral Letter

- Inadequate Vehicle Equity Auto Loan Denial Letter

- Auto Financing Insufficient Collateral Rejection Letter

- Commercial Auto Loan Collateral Deficiency Denial Letter

- Auto Refinance Inadequate Appraisal Denial Letter

- Negative Equity Auto Loan Application Denial Letter

- Vehicle Financing Collateral Requirement Unmet Denial Letter

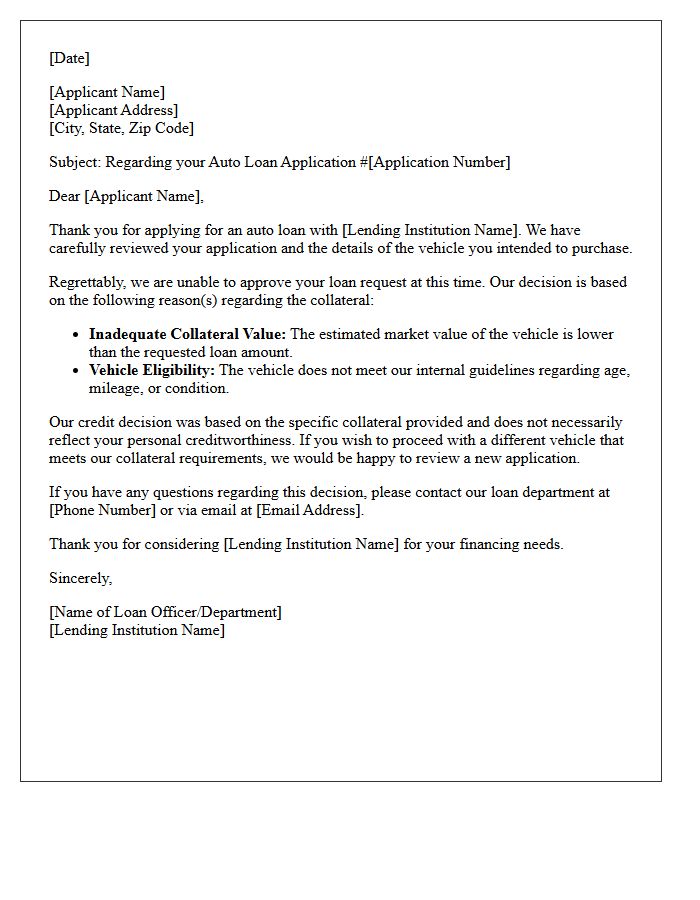

Auto Loan Inadequate Collateral Denial Letter

An Auto Loan Inadequate Collateral Denial Letter is a formal notice sent when a lender rejects your application because the vehicle's appraised value is too low compared to the requested loan amount. This occurs if the car is overpriced, in poor condition, or exceeds mileage limits. To resolve this, you may need to increase your down payment, choose a different vehicle, or negotiate a lower purchase price to improve the loan-to-value (LTV) ratio and meet the lender's strict security requirements for financing.

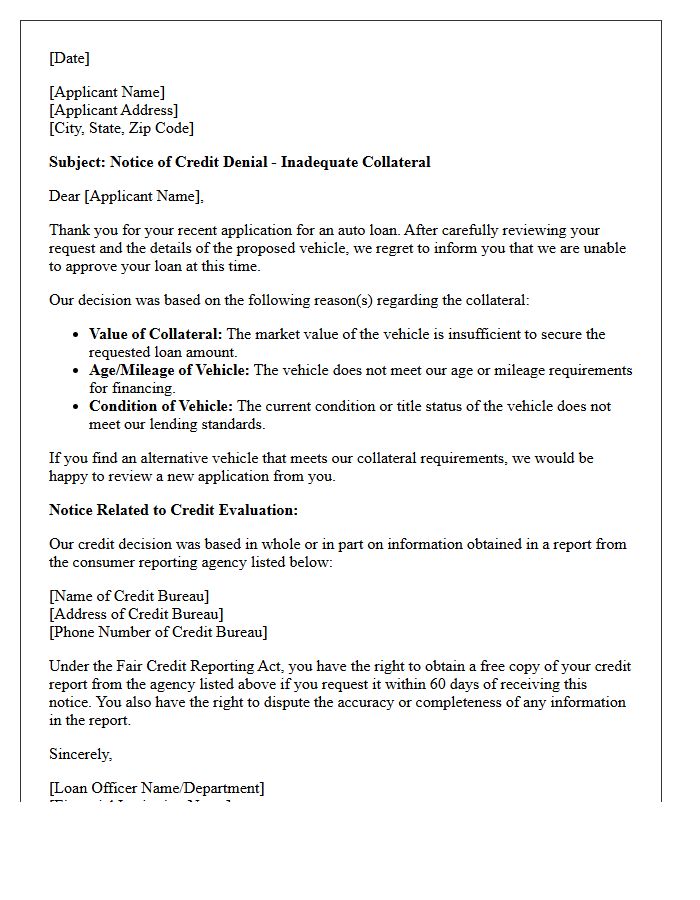

Notice of Denial for Inadequate Auto Collateral Letter

A Notice of Denial for Inadequate Auto Collateral is a formal letter issued by a lender when a loan application is rejected because the vehicle's value is insufficient to secure the requested debt. Key factors often include the car's high mileage, excessive age, or a low book value compared to the purchase price. To resolve this, applicants may need to provide a larger down payment, choose a more valuable vehicle, or offer additional security to satisfy the lender's risk requirements and loan-to-value ratios.

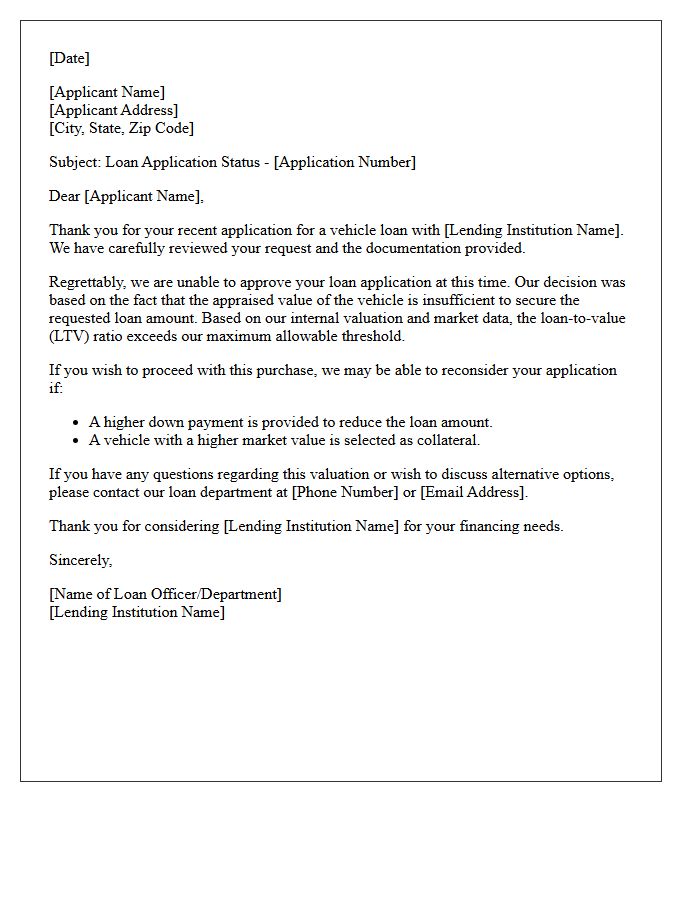

Vehicle Value Insufficient Loan Rejection Letter

A vehicle value insufficient loan rejection letter informs an applicant that their financing was denied because the collateral's appraised worth is lower than the requested loan amount. Lenders use a Loan-to-Value (LTV) ratio to mitigate financial risk, ensuring the car sufficiently secures the debt. If the purchase price exceeds the market value, the equity gap becomes too high for approval. Receiving this notice allows borrowers to renegotiate the sale price, provide a larger down payment, or select a different vehicle that aligns with the bank's valuation standards.

Secured Auto Loan Collateral Shortfall Denial Letter

A Secured Auto Loan Collateral Shortfall Denial Letter informs applicants that their loan request was rejected because the vehicle's market value is insufficient to secure the requested financing. Lenders require a specific loan-to-value ratio to mitigate risk. If the car's appraisal is lower than the purchase price or loan amount, it creates a collateral shortfall. To resolve this, borrowers may need to provide a larger down payment, select a different vehicle, or seek a co-signer to strengthen the application and offset the security gap identified by the financial institution.

Used Auto Loan Inadequate Collateral Notification Letter

A Used Auto Loan Inadequate Collateral Notification Letter informs borrowers that their vehicle's current market value has fallen below the required loan-to-value ratio. This formal notice often triggers a demand for additional collateral or a principal reduction payment to secure the debt. Lenders issue this when market volatility or excessive wear reduces the asset's worth, potentially leading to a technical default if the equity gap is not resolved promptly. Understanding this document is crucial for maintaining loan compliance and preventing vehicle repossession.

Bank Notice of Auto Loan Denial Due to Collateral Letter

Receiving a bank notice of auto loan denial due to collateral means your application was rejected because the vehicle's value or condition did not meet lender standards. This often occurs when the loan-to-value (LTV) ratio is too high, or the car is considered too old or high-mileage. To resolve this, you may need to provide a larger down payment, choose a newer vehicle, or verify the car's appraisal accuracy to ensure it sufficiently secures the debt according to bank risk policies.

Inadequate Vehicle Equity Auto Loan Denial Letter

An Inadequate Vehicle Equity Auto Loan Denial Letter informs applicants that their collateral value is insufficient to secure the requested financing. This typically occurs when the loan-to-value (LTV) ratio is too high, meaning the car's worth is lower than the total loan amount. Lenders issue this adverse action notice to mitigate risk. To resolve this, you can increase your down payment, choose a less expensive vehicle, or provide a trade-in with positive equity to bridge the financial gap and satisfy the lender's internal security requirements.

Auto Financing Insufficient Collateral Rejection Letter

An Auto Financing Insufficient Collateral Rejection Letter informs an applicant that their loan request was denied because the vehicle's market value is too low relative to the requested loan amount. Lenders use the Loan-to-Value (LTV) ratio to assess risk; if the car cannot sufficiently secure the debt, the collateral is deemed inadequate. This notice, required under the Equal Credit Opportunity Act, ensures transparency regarding why the asset failed to meet underwriting standards. To resolve this, borrowers may need a higher down payment or a vehicle with better equity.

Commercial Auto Loan Collateral Deficiency Denial Letter

A Commercial Auto Loan Collateral Deficiency Denial Letter is a formal notification issued by lenders when the vehicle's appraised value fails to meet the required loan-to-value ratio. This collateral deficiency signifies that the asset provides insufficient security for the requested financing amount. To resolve this, applicants may need to provide a larger down payment, offer additional guarantees, or select a different vehicle. Understanding this document is crucial for adjusting your business financing strategy and addressing under-collateralization risks identified during the underwriting process.

Auto Refinance Inadequate Appraisal Denial Letter

Receiving an Auto Refinance Inadequate Appraisal Denial Letter means your lender determined the vehicle's current market value is too low to support the requested loan amount. This typically results from a high Loan-to-Value (LTV) ratio, where the outstanding debt exceeds the car's appraised worth. To resolve this, you can provide comparable sales data to dispute the valuation, decrease the principal by making a cash down payment, or improve the vehicle's condition. Reviewing the specific valuation report mentioned in the letter is essential to identify potential errors in mileage or trim level.

Negative Equity Auto Loan Application Denial Letter

A negative equity auto loan denial letter indicates that your current vehicle's loan balance exceeds its market value, creating a "underwater" status. Lenders often reject applications when this deficiency balance is rolled into a new loan, as it increases the total loan-to-value (LTV) ratio beyond acceptable risk limits. Receiving this notice means the financial institution views the negative equity as a significant collateral risk. To improve future approval odds, consider making a larger down payment or paying down your existing principal to reduce the total debt burden before reapplying.

Vehicle Financing Collateral Requirement Unmet Denial Letter

A vehicle financing denial letter citing an unmet collateral requirement indicates that the specific automobile failed to meet the lender's safety, age, or mileage standards. Even with strong credit, a loan can be rejected if the vehicle's valuation is lower than the requested amount or if the title has restrictive brands. This adverse action notice protects lenders from funding assets with insufficient resale value. If denied, you should review the vehicle's condition or select a newer model that aligns with the institution's risk guidelines and loan-to-value parameters.

Why was my auto loan denied due to inadequate collateral?

An auto loan denial for inadequate collateral occurs when the vehicle's current market value is lower than the requested loan amount. This often happens if the purchase price is inflated, the vehicle has high mileage, or the loan-to-value (LTV) ratio exceeds the lender's internal risk thresholds.

How is the value of the vehicle determined for my loan application?

Lenders determine vehicle value using industry-standard valuation guides such as Kelley Blue Book (KBB), NADA, or Black Book. They consider the year, make, model, trim level, mileage, and overall condition to establish the maximum amount they are willing to finance.

What can I do if I receive a Notice of Denial for inadequate collateral?

If your application is denied, you can lower the loan amount by providing a larger down payment, choosing a vehicle with a lower purchase price, or finding a car with lower mileage and a higher book value to improve the loan-to-value ratio.

Does a denial for inadequate collateral affect my credit score?

The denial itself does not impact your credit score; however, the hard inquiry performed by the lender during the application process may cause a temporary, minor dip in your score. The specific reason for denial (collateral) is not recorded on your credit report.

Can I appeal a collateral-based loan denial with an independent appraisal?

While most high-volume lenders rely strictly on automated valuation guides, some local banks or credit unions may allow an appeal. You may provide a detailed vehicle history report or proof of recent upgrades, though the lender is not legally required to change their valuation based on an independent appraisal.

Comments