A Construction Loan Lack of Builder Credentials Denial Letter is a formal notice sent by lenders when a contractor fails to meet required professional standards or licensing criteria. This rejection ensures financial safety by verifying the builder's expertise and stability before funding starts. Understanding these requirements helps applicants address deficiencies and resubmit successfully. Below are some ready to use templates.

Image cover: Official Notice: Construction Loan Denial Due to Insufficient Builder Credentials

Letter Samples List

- Construction Loan Denial Letter Due To Unapproved Builder Credentials

- Insufficient Builder Experience Construction Loan Decline Letter

- Unlicensed Contractor Construction Loan Adverse Action Letter

- Non-Approved Builder Construction Loan Rejection Letter

- Inadequate Builder Bonding And Insurance Construction Loan Denial Letter

- Builder Financial Instability Construction Loan Decline Letter

- Builder Capacity Mismatch Construction Loan Adverse Action Letter

- Unsatisfactory Builder Background Check Construction Loan Denial Letter

- Unverified Builder References Construction Loan Rejection Letter

- Missing Builder Warranty Certification Construction Loan Decline Letter

- Commercial Construction Loan Denial Letter For Inadequate Builder Qualifications

- Builder Regulatory Non-Compliance Construction Loan Adverse Action Letter

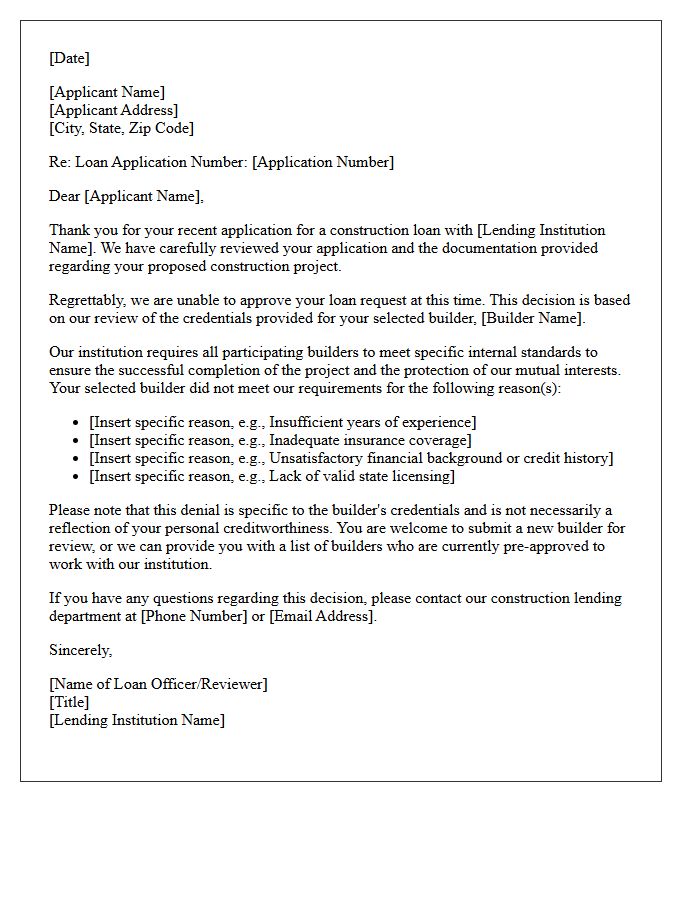

Construction Loan Denial Letter Due To Unapproved Builder Credentials

Receiving a construction loan denial letter due to unapproved builder credentials means the lender's risk assessment flagged your contractor's background. Financial institutions require vetted builders to ensure project completion and structural integrity. Common reasons include insufficient experience, poor credit history, or lack of proper licensing and insurance. This rejection protects the bank's investment from potential liens or abandonment. To resolve this, you must either provide additional documentation to clear your builder's standing or select a pre-approved contractor who meets the lender's rigorous stability and performance standards.

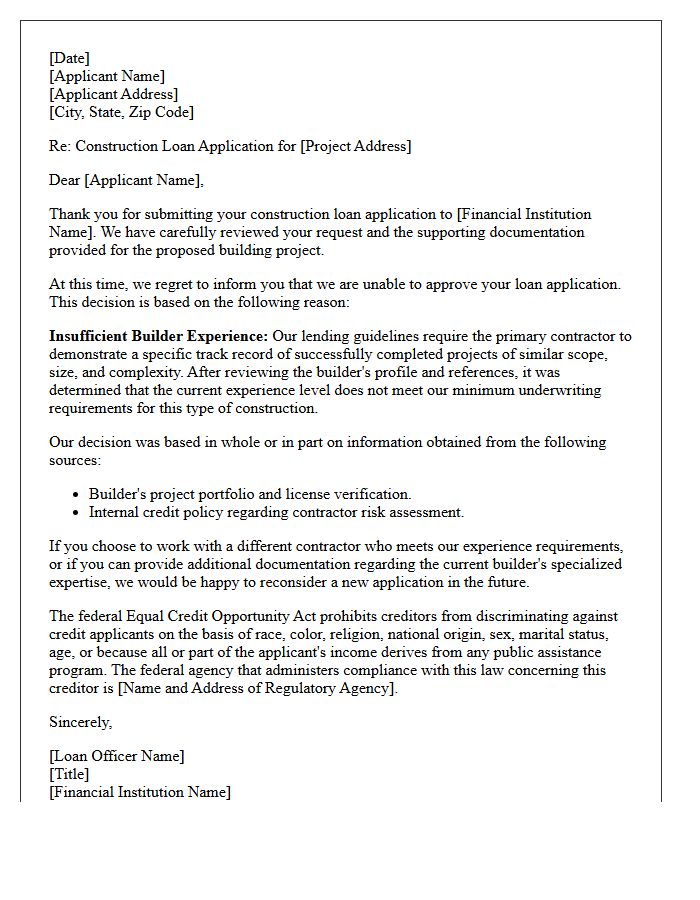

Insufficient Builder Experience Construction Loan Decline Letter

An Insufficient Builder Experience construction loan decline letter signifies that the lender deems the contractor's track record inadequate for the project's scope. Financial institutions prioritize risk mitigation by evaluating a builder's operational history, completed project volume, and industry references. If a builder lacks documented success with similar residential builds, the loan is often rejected to prevent potential default or project abandonment. To resolve this, applicants must either provide more comprehensive builder resumes, proof of specialized certifications, or select a more experienced contractor to secure financing approval.

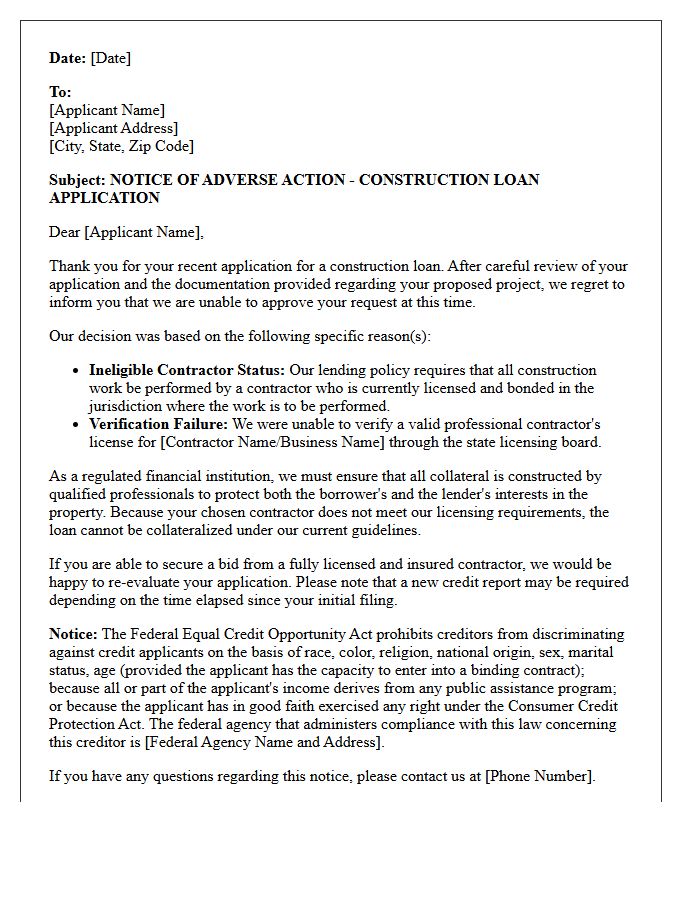

Unlicensed Contractor Construction Loan Adverse Action Letter

An Adverse Action Letter is a mandatory notice issued when a construction loan is denied due to an unlicensed contractor. Lenders require valid licensing to mitigate risk and ensure legal compliance. Receiving this document means the application failed underwriting standards specifically related to the builder's credentials. To move forward, borrowers must typically replace the professional with a licensed contractor or provide proof of current state certification. This formal notification protects consumers by clearly stating the denial reason, allowing for corrective measures in the financing process.

Non-Approved Builder Construction Loan Rejection Letter

Receiving a Non-Approved Builder Construction Loan Rejection Letter typically means the lender's risk assessment found the contractor's financial stability, licensing, or track record insufficient. Lenders prioritize project security and must ensure the builder can complete the work within budget and timeframe. If your builder is rejected, you may need to provide additional vetting documentation, request a formal appeal, or select a pre-approved contractor to secure financing. Understanding specific underwriting guidelines is essential to resolving the denial and moving forward with your home construction project successfully.

Inadequate Builder Bonding And Insurance Construction Loan Denial Letter

An Inadequate Builder Bonding and Insurance construction loan denial letter signifies that a contractor fails to meet the lender's risk mitigation requirements. Lenders mandate specific general liability insurance, workers' compensation, and performance bonds to protect their investment against potential project abandonment or structural defects. If a builder lacks sufficient coverage limits or financial stability, the bank will reject the loan application to avoid financial exposure. Applicants must ensure their contractor provides verified insurance certificates and robust surety bonds to satisfy underwriting criteria and secure project financing approval.

Builder Financial Instability Construction Loan Decline Letter

Receiving a Builder Financial Instability Construction Loan Decline Letter indicates your lender has identified significant solvency risks or negative credit data regarding your contractor. Banks prioritize collateral security; if a builder faces bankruptcy or cash flow issues, the project may never reach completion. This rejection protects you from funding a failing business. To move forward, you must address these concerns by requesting a detailed financial audit from the builder or, more commonly, selecting a new, financially stable contractor to secure loan approval and ensure project viability.

Builder Capacity Mismatch Construction Loan Adverse Action Letter

A Builder Capacity Mismatch occurs when a lender determines a contractor lacks the financial or operational resources to complete a project. If this leads to a formal rejection, the lender must issue an Adverse Action Letter. This document is a legal requirement under the Equal Credit Opportunity Act, explaining why the financing was denied. It protects borrowers by ensuring transparency regarding the builder's risk profile or insufficient liquidity. Understanding this mismatch helps borrowers select qualified professionals who meet stringent institutional standards for successful project delivery and loan approval.

Unsatisfactory Builder Background Check Construction Loan Denial Letter

Receiving an Unsatisfactory Builder Background Check Construction Loan Denial Letter indicates that the lender identified significant risks regarding your contractor. This adverse action occurs when a builder fails to meet financial stability, licensing, or creditworthiness standards required by the financial institution. Lenders issue these denials to protect their collateral from potential mechanic's liens or project abandonment. If your loan is rejected for this reason, you must either find a vetted contractor with a proven track record or request specific details from the lender to address the background discrepancies.

Unverified Builder References Construction Loan Rejection Letter

Receiving an Unverified Builder References Construction Loan Rejection Letter indicates that the lender cannot confirm the contractor's professional history or reliability. Financial institutions require verified track records to mitigate risk before approving funding. If a builder fails the vetting process due to unreachable references or incomplete documentation, the loan will be denied. To resolve this, applicants must provide a builder with a proven portfolio and verifiable client testimonials to satisfy the lender's strict underwriting criteria and secure the necessary financing for their construction project.

Missing Builder Warranty Certification Construction Loan Decline Letter

A Missing Builder Warranty Certification is a critical document deficiency that frequently triggers a Construction Loan Decline Letter. Lenders require this formal guarantee to ensure the property meets structural standards and protects their collateral. Without a valid warranty from a licensed builder, the financial risk becomes too high for underwriters, leading to an immediate application rejection. To resolve this, borrowers must obtain the specific certification or HUD-compliant documentation required by the lender to secure funding and proceed with the home building process.

Commercial Construction Loan Denial Letter For Inadequate Builder Qualifications

Receiving a commercial construction loan denial letter due to inadequate builder qualifications signifies that the lender deems your contractor too risky. To mitigate financial exposure, banks evaluate a builder's track record, balance sheets, and bonding capacity. If a contractor lacks experience with similar project scales or has poor credit, the loan is rejected. To resolve this, you must either provide additional documentation proving the builder's expertise or replace the contractor with one who meets the bank's stringent underwriting standards and operational requirements to ensure successful project completion.

Builder Regulatory Non-Compliance Construction Loan Adverse Action Letter

A builder regulatory non-compliance construction loan adverse action letter is a formal notice issued by a lender when a project is rejected due to legal violations. This document informs the applicant that the contractor failed to meet specific building codes, licensing requirements, or local zoning regulations. Receiving this letter signifies that the builder's lack of authorization or safety adherence creates excessive financial risk. To proceed, borrowers must typically resolve the documented compliance failures or select a new builder who fully adheres to all regulatory standards to secure funding.

Why was my construction loan denied due to builder credentials?

Lenders require builders to meet specific standards for experience, licensing, and financial stability to protect the collateral. Your loan was likely denied because the selected contractor failed to provide valid state licenses, adequate general liability insurance, or a proven track record of completing similar residential projects.

Can I appeal a loan denial based on a builder's lack of professional standing?

Yes, you can appeal by providing additional documentation that addresses the lender's specific concerns. This may include the builder's updated certificates of insurance, a comprehensive project portfolio, professional references, or a verified resume demonstrating their experience with the specific type of construction planned.

What are the minimum builder requirements to qualify for a construction loan?

Most lenders require a builder to have a valid state contractor's license, a minimum of 2-5 years of experience, and a "clean" background check regarding past litigation. Additionally, the builder must typically provide a detailed line-item cost estimate and a signed contract that aligns with current market values.

Does a builder's credit history affect my construction loan approval?

Yes, lenders often perform a financial review of the builder to ensure they have the liquidity to manage project expenses and pay subcontractors. If a builder has a history of bankruptcies, significant tax liens, or poor credit, the lender may deny the loan to avoid the risk of mechanic's liens or project abandonment.

How do I resolve a construction loan denial if my builder is disqualified?

If your builder cannot meet the lender's credentialing criteria, your primary options are to select a different contractor who is already on the lender's approved list or to find a builder who can pass the vetting process. Once a qualified builder is secured, you can resubmit your application for a new credit decision.

Comments