If you have received an Unsecured Personal Loan Excessive Existing Obligations Denial Letter, it means your debt-to-income ratio is too high for new credit. Lenders issue this notice when your current financial commitments pose a significant repayment risk. Understanding this rejection is the first step toward improving your credit profile. To help you respond effectively, below are some ready to use template.

Image cover: How to Handle a Personal Loan Rejection Due to High Debt: Templates and Guidance

Letter Samples List

- High Debt-To-Income Ratio Unsecured Personal Loan Denial Letter

- Excessive Open Credit Obligations Unsecured Personal Loan Denial Letter

- Insufficient Income For Existing Debt Unsecured Personal Loan Denial Letter

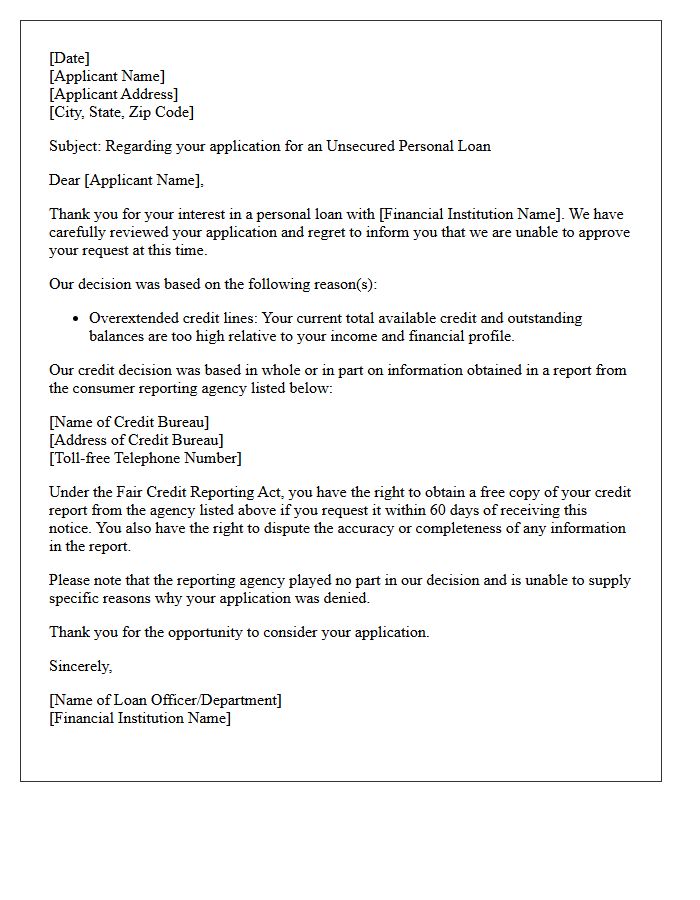

- Overextended Credit Lines Unsecured Personal Loan Denial Letter

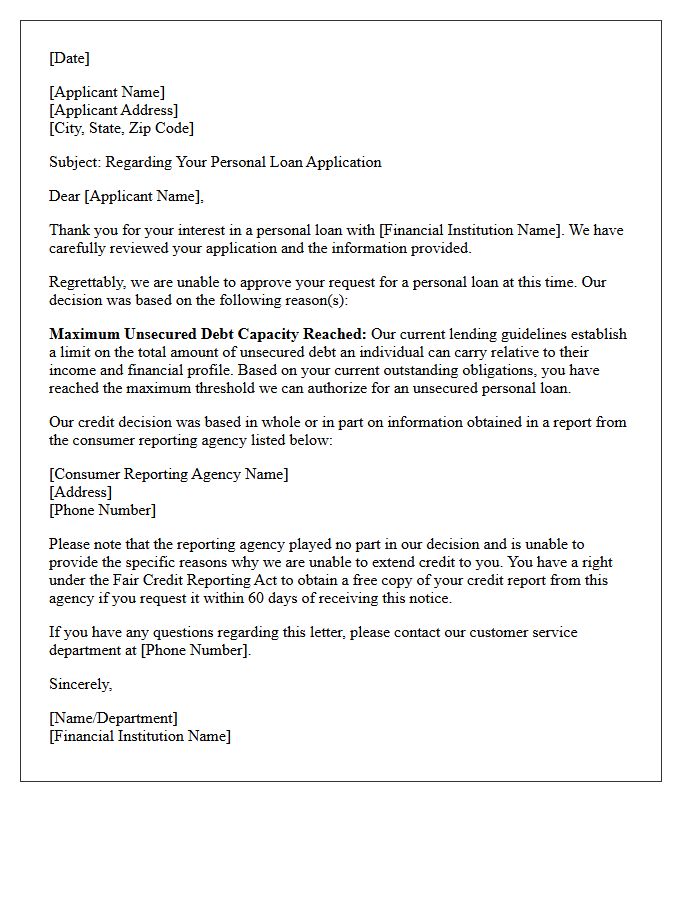

- Maximum Unsecured Debt Capacity Reached Personal Loan Denial Letter

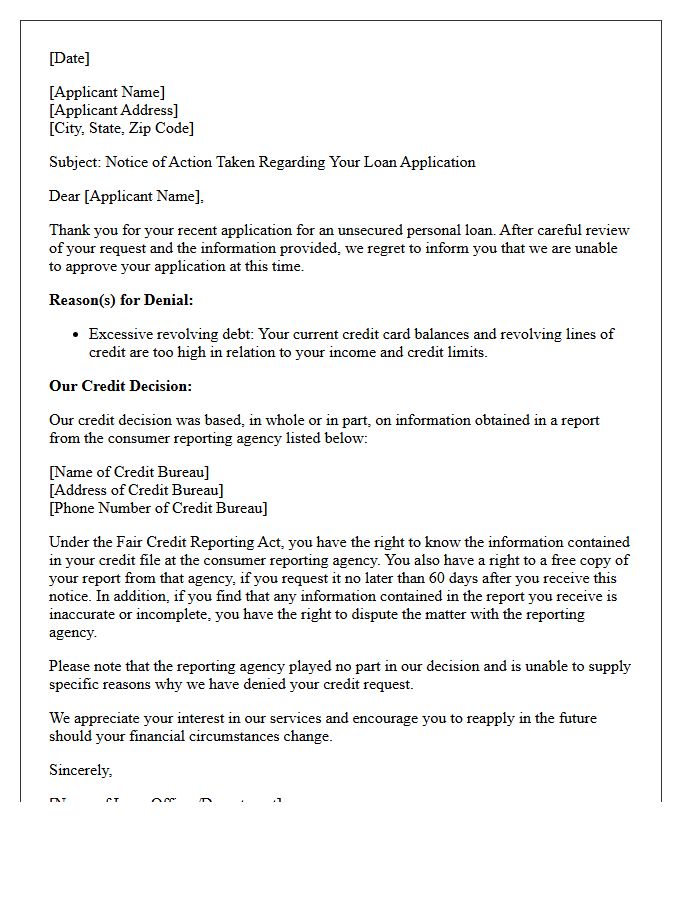

- Excessive Revolving Debt Unsecured Personal Loan Denial Letter

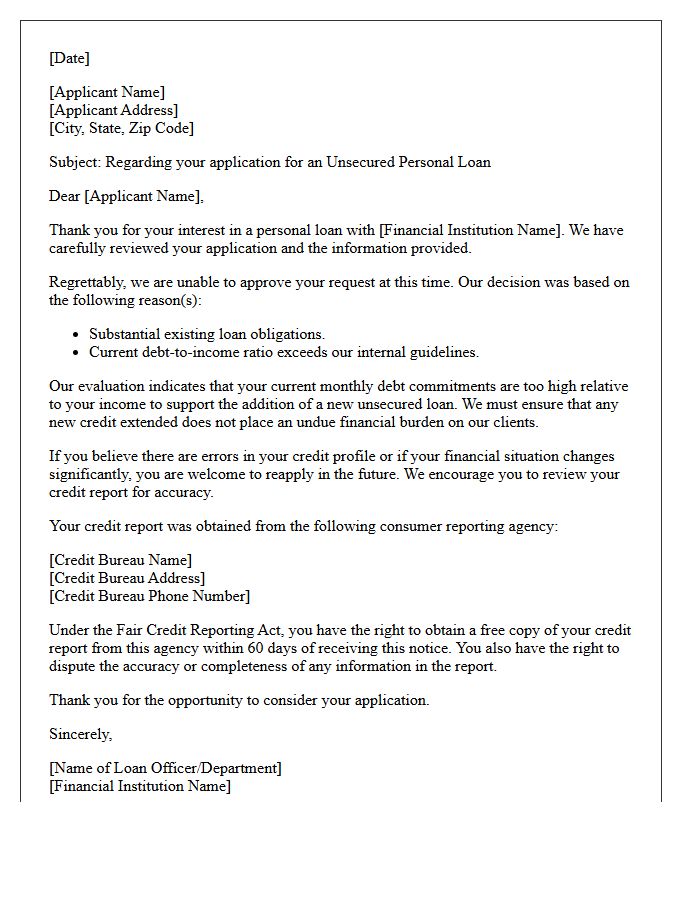

- Substantial Existing Loan Obligations Unsecured Personal Loan Denial Letter

- General Excessive Existing Obligations Unsecured Personal Loan Denial Letter

- Insufficient Deficit Income Unsecured Personal Loan Denial Letter

- High Monthly Debt Payments Unsecured Personal Loan Denial Letter

- Internal Policy Limit Exceeded Existing Debt Unsecured Personal Loan Denial Letter

- Recently Acquired Debt Obligations Unsecured Personal Loan Denial Letter

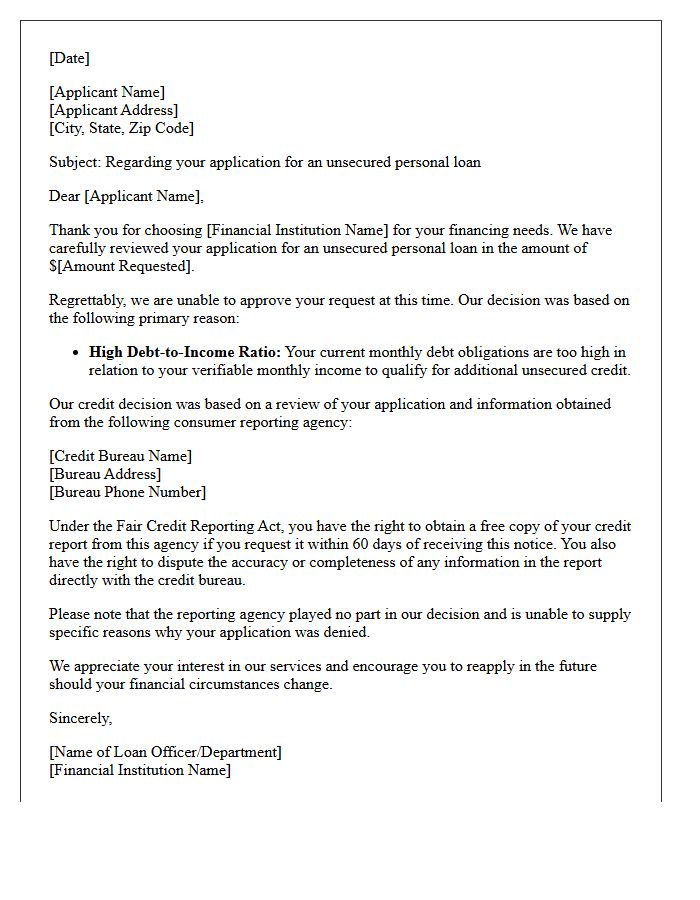

High Debt-To-Income Ratio Unsecured Personal Loan Denial Letter

Receiving a denial letter for an unsecured personal loan often stems from a high debt-to-income (DTI) ratio. This metric signals to lenders that your current monthly obligations consume too much of your gross monthly income, making additional repayment risky. Since unsecured loans lack collateral, financial stability is paramount. To improve your chances for future approval, focus on reducing existing balances or increasing your earnings. Reviewing your adverse action notice helps identify specific thresholds needed to meet creditworthiness standards and lower your perceived default risk effectively.

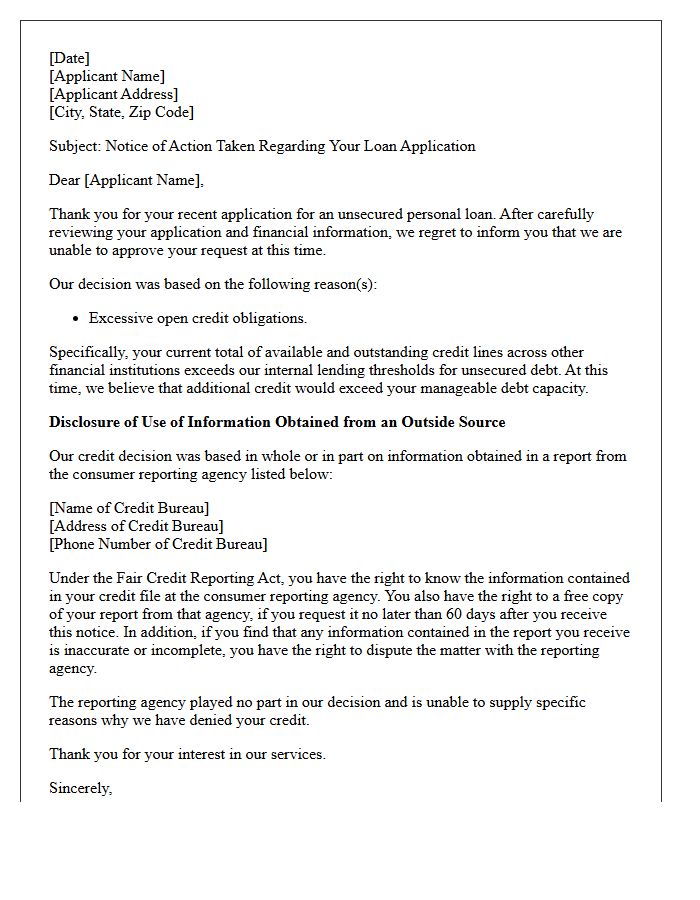

Excessive Open Credit Obligations Unsecured Personal Loan Denial Letter

Receiving a denial letter for an unsecured personal loan often cites excessive open credit obligations as the primary reason. This indicates that your debt-to-income ratio or total available credit lines are too high for the lender's risk profile. Even if you maintain a good payment history, having too many active accounts or high balances suggests potential financial strain. To improve your chances for future approval, consider reducing outstanding balances or closing unused accounts to lower your total credit exposure and demonstrate better repayment capacity to financial institutions.

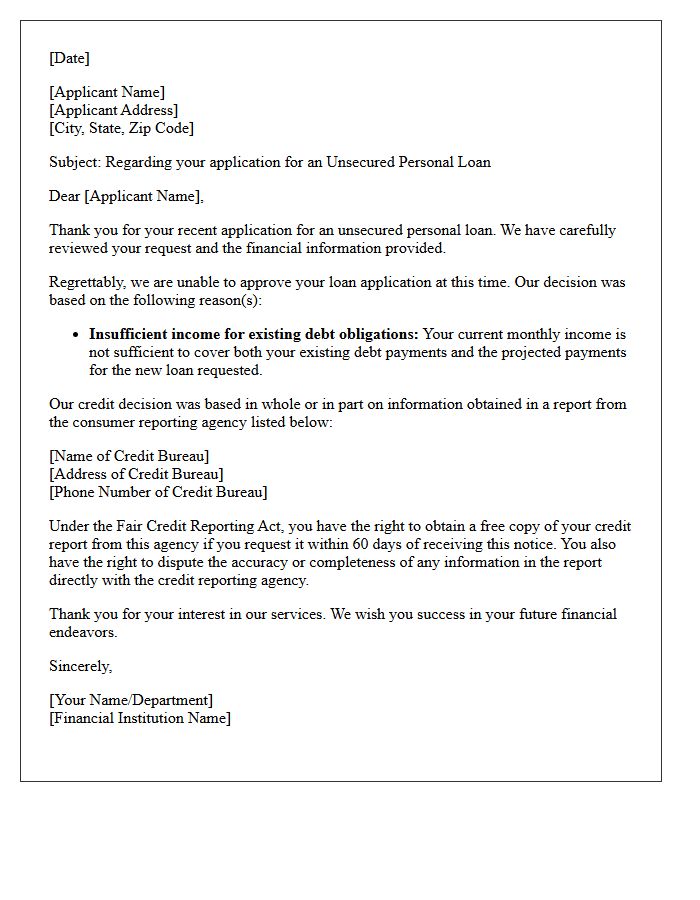

Insufficient Income For Existing Debt Unsecured Personal Loan Denial Letter

Receiving an unsecured personal loan denial due to insufficient income means your current earnings cannot comfortably cover existing debt obligations and a new monthly payment. Lenders use the Debt-to-Income (DTI) ratio to assess financial risk. This letter indicates that your repayment capacity is overextended, making additional credit a default risk. To improve future approval odds, focus on debt consolidation, increasing your documented income, or paying down high-interest credit card balances to lower your total debt burden before reapplying for financing.

Overextended Credit Lines Unsecured Personal Loan Denial Letter

Receiving an overextended credit lines denial letter indicates that lenders perceive your current debt-to-income ratio or total credit limits as too risky. Even with a good payment history, having excessive open accounts suggests a high potential for default. To improve your chances for an unsecured personal loan, focus on reducing outstanding balances and closing unused accounts to lower your aggregate exposure. Reviewing your credit report for inaccuracies regarding your limits is essential, as financial stability is the primary factor lenders evaluate when determining your borrowing capacity for non-collateralized debt.

Maximum Unsecured Debt Capacity Reached Personal Loan Denial Letter

Receiving a denial letter stating you have reached your maximum unsecured debt capacity means lenders believe your current non-collateralized liabilities are too high relative to your income. This decision is based on your debt-to-income ratio and total credit exposure. To improve your chances for future approval, focus on paying down existing credit card balances or personal loans. Reducing your aggregate debt load demonstrates better financial stability and lowers the risk for potential creditors, eventually allowing you to qualify for additional funding once your credit utilization decreases significantly.

Excessive Revolving Debt Unsecured Personal Loan Denial Letter

Receiving a denial letter for an unsecured personal loan often cites excessive revolving debt as the primary cause. This indicates that your current credit card balances are too high relative to your limits, signaling potential repayment risk to lenders. High credit utilization negatively impacts your credit score and debt-to-income ratio. To improve your chances for future approval, focus on paying down existing balances and avoiding new charges. Lowering your revolving debt demonstrates financial stability and increases your creditworthiness, making you a more attractive candidate for unsecured financing options.

Substantial Existing Loan Obligations Unsecured Personal Loan Denial Letter

Receiving a denial letter for an unsecured personal loan often cites substantial existing loan obligations as the primary reason. This indicates that your current debt-to-income ratio is too high, signaling to lenders that taking on additional unsecured debt poses a significant default risk. To improve your chances for future approval, focus on debt consolidation or aggressive repayment to lower your total liabilities. Reviewing your credit report for accuracy is also essential, as debt capacity is a critical factor in determining your overall financial stability and creditworthiness during the application process.

General Excessive Existing Obligations Unsecured Personal Loan Denial Letter

Receiving a denial letter for an unsecured personal loan due to general excessive existing obligations indicates a high debt-to-income ratio. This means your current financial commitments are too large relative to your earnings, posing a significant default risk. Lenders prioritize your ability to manage additional monthly payments without overextending your budget. To improve future approval chances, focus on debt consolidation or aggressive repayment strategies to lower your total liabilities. Reviewing your credit report for inaccuracies regarding your repayment capacity is also a vital step in addressing this specific loan rejection.

Insufficient Deficit Income Unsecured Personal Loan Denial Letter

An Insufficient Deficit Income denial letter indicates your monthly cash flow is inadequate to cover a new unsecured personal loan. Lenders calculate your debt-to-income ratio to ensure you can manage repayments without collateral. Receiving this notice means your net income, after current expenses, leaves a negative balance or lacks the required margin for additional debt. To improve future approval odds, focus on increasing total income, paying down existing credit balances, or requesting a smaller loan amount to align with your verified financial capacity.

High Monthly Debt Payments Unsecured Personal Loan Denial Letter

Receiving an unsecured personal loan denial letter often cites high monthly debt payments as the primary cause. This indicates a high debt-to-income (DTI) ratio, suggesting your current financial obligations consume too much of your monthly earnings to safely manage additional credit. Lenders view this as a significant default risk. To improve future approval odds, focus on debt consolidation, paying down existing balances, or increasing your documented income. Reducing your fixed monthly liabilities demonstrates better repayment capacity, making you a more attractive candidate for unsecured financing in the future.

Internal Policy Limit Exceeded Existing Debt Unsecured Personal Loan Denial Letter

Receiving an internal policy limit exceeded denial indicates your total existing debt surpasses the lender's specific threshold for risk. This decision is based on an internal cap regarding the maximum aggregate exposure allowed for an unsecured personal loan. Even with a high credit score, surpassing these internal limits suggests you carry too much unsecured liability relative to your income or the bank's internal criteria. To improve future approval odds, focus on reducing current balances or increasing your documented income to meet the lender's specific underwriting requirements.

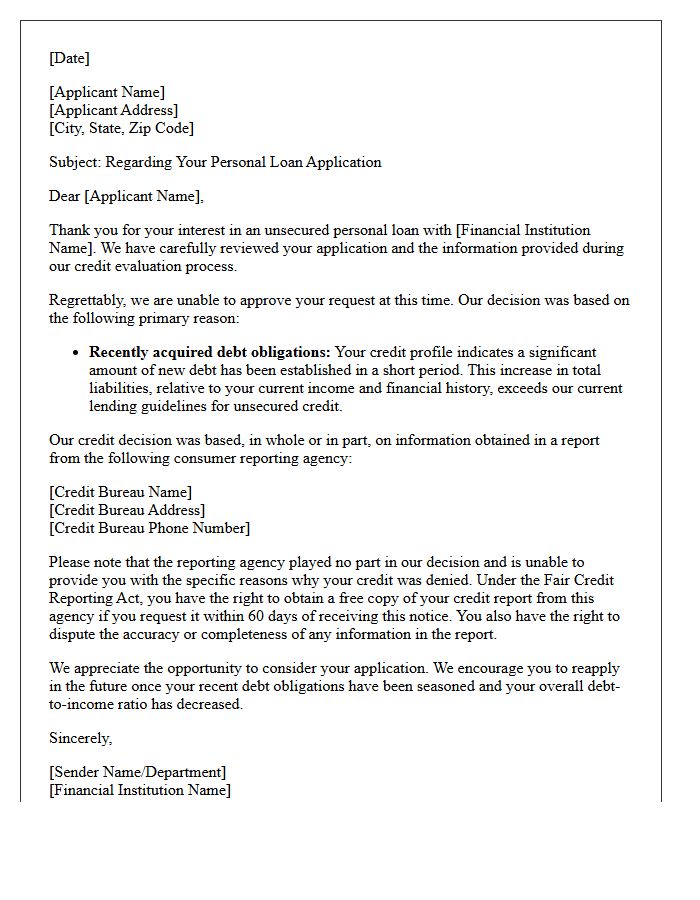

Recently Acquired Debt Obligations Unsecured Personal Loan Denial Letter

Receiving a denial letter for an unsecured personal loan often cites recently acquired debt obligations as the primary reason. This indicates that your debt-to-income ratio has increased too quickly, signaling high financial risk to lenders. Recent balances suggest a dependency on credit or potential overextension, making you less likely to manage new repayments. To improve your chances, focus on lowering current balances and avoiding new credit inquiries for at least six months. Reducing your total debt load demonstrates fiscal stability and improves your overall creditworthiness for future applications.

What does "excessive existing obligations" mean on my loan denial letter?

This phrase indicates that your current monthly debt payments, such as credit cards, student loans, or mortgages, are too high relative to your income. Lenders use this to determine that adding a new unsecured personal loan payment would exceed their allowable debt-to-income (DTI) threshold.

Can I still get an unsecured personal loan if I was denied for having too much debt?

Yes, but you will likely need to lower your debt-to-income ratio first. You can achieve this by paying down high-balance credit cards, increasing your verifiable income, or applying with a co-signer who has a lower debt load and strong credit profile.

How does my debt-to-income (DTI) ratio affect an unsecured loan application?

Since unsecured loans require no collateral, lenders rely heavily on your DTI ratio to ensure you have enough cash flow to cover the new installment. Most lenders prefer a DTI below 36% to 43%; exceeding these limits often results in an automatic denial for excessive obligations.

Will a denial for excessive existing obligations hurt my credit score?

The denial itself does not impact your credit score, but the "hard inquiry" generated when you applied may cause a temporary dip of five to ten points. To protect your score, avoid multiple rapid applications and focus on reducing your debt balances before reapplying.

How can I fix my "excessive obligations" status to qualify for a loan?

The most effective ways to fix this status are to pay off small balance accounts to eliminate monthly minimums, consolidate existing high-interest debt into lower payments, or update your application with secondary income sources like bonuses, alimony, or side-hustle earnings.

Comments