Receiving a Home Equity Line of Credit appraisal shortfall denial letter occurs when your property's current market value is insufficient to secure the requested loan amount. This rejection often results from declining neighborhood trends or property condition issues. Understanding the specific reasons for this valuation gap is essential for filing a successful appeal. To help you respond effectively, below are some ready to use templates.

Image cover: Responding to a HELOC Denial Due to Low Property Valuation: Letter Samples and Templates

Letter Samples List

- Home Equity Line of Credit Appraisal Shortfall Denial Letter

- Insufficient Collateral Value Adverse Action Letter

- Notice of Action Taken for HELOC Appraisal Deficit Letter

- Home Equity Loan Maximum Loan to Value Exceeded Denial Letter

- Reconsideration of Value Appeal Rejection Letter

- Secondary Mortgage Appraisal Shortfall Decline Letter

- Inadequate Property Valuation HELOC Denial Letter

- Notice of Credit Denial Due to Insufficient Equity Letter

- Appraisal Shortfall Counteroffer Notification Letter

- HELOC Application Rejection for Inadequate Collateral Letter

- Property Valuation Shortfall Equity Loan Decline Letter

- Statement of Credit Denial for Home Equity Line of Credit Letter

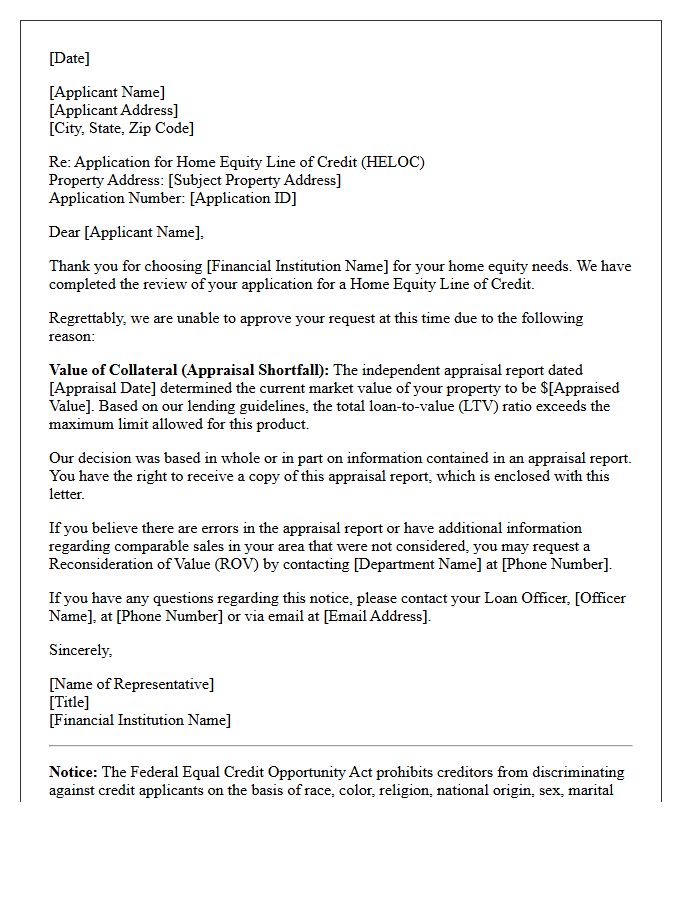

Home Equity Line of Credit Appraisal Shortfall Denial Letter

A Home Equity Line of Credit (HELOC) appraisal shortfall denial letter notifies an applicant that their property's appraised value is too low to support the requested loan amount. This occurs when the combined loan-to-value (CLTV) ratio exceeds the lender's maximum threshold. To address this, homeowners can request a reconsideration of value by providing new comparable sales data or evidence of recent property improvements. Alternatively, reducing the requested credit limit or paying down the primary mortgage can help secure approval despite a valuation discrepancy.

Insufficient Collateral Value Adverse Action Letter

An Insufficient Collateral Value Adverse Action Letter is a formal notice sent to loan applicants when a credit request is denied because the appraisal or asset value does not adequately secure the debt. Under the Equal Credit Opportunity Act, lenders must provide this written explanation within thirty days. It informs the borrower that the collateral's worth fell below the required loan-to-value ratio, making the risk unacceptable. Understanding this document is crucial for identifying if the rejection was due to property valuation issues rather than personal creditworthiness.

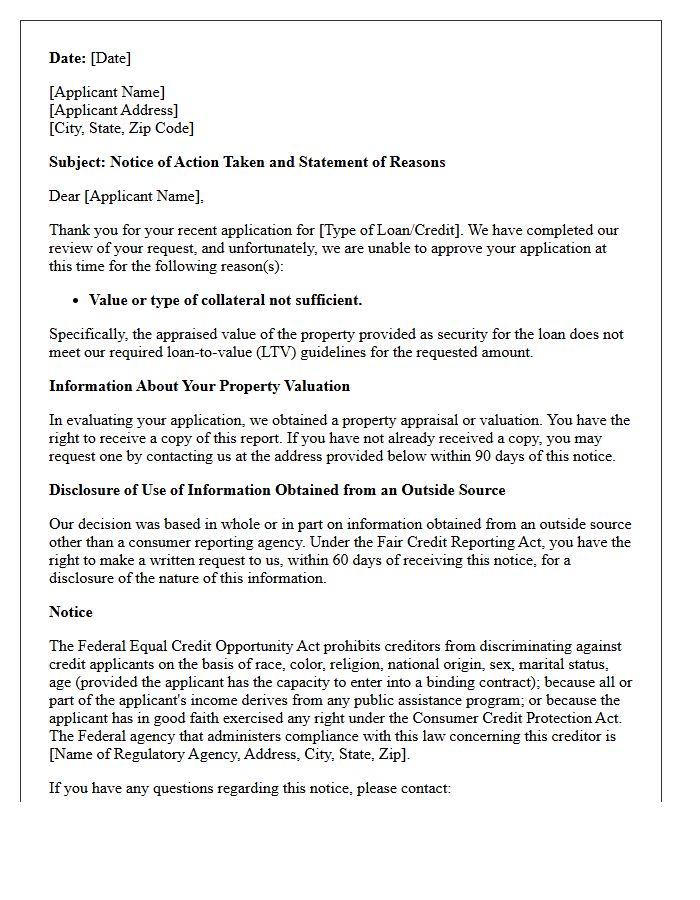

Notice of Action Taken for HELOC Appraisal Deficit Letter

A Notice of Action Taken for a HELOC appraisal deficit is a formal notification issued when your Home Equity Line of Credit application is denied or modified due to insufficient property value. Lenders provide this letter to explain that the current market appraisal resulted in a loan-to-value ratio that does not meet their risk requirements. This document is a regulatory requirement under the Equal Credit Opportunity Act, ensuring transparency regarding valuation discrepancies. Understanding this notice allows you to dispute errors, provide comparable sales data, or seek a secondary valuation to secure approval.

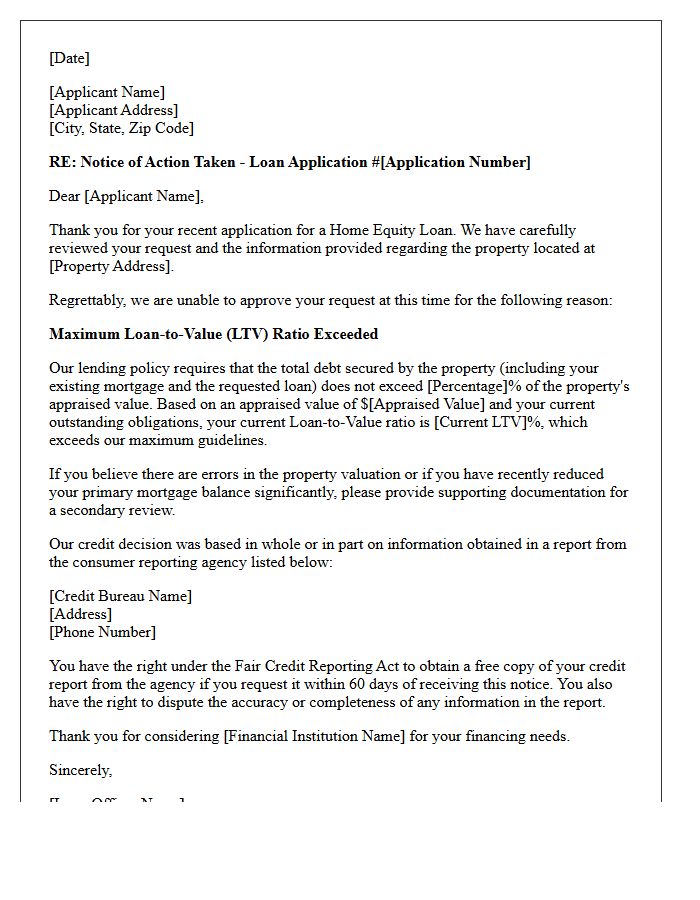

Home Equity Loan Maximum Loan to Value Exceeded Denial Letter

Receiving a Home Equity Loan denial letter due to exceeding the maximum loan-to-value ratio means your property's equity is insufficient to secure the requested amount. Lenders typically cap total debt at 80-90% of the home's appraised worth. When your combined mortgage balance and new loan exceed this limit, the application is rejected to mitigate financial risk. To resolve this, you can appeal the appraisal, pay down existing principal, or wait for market values to increase before reapplying for the funds.

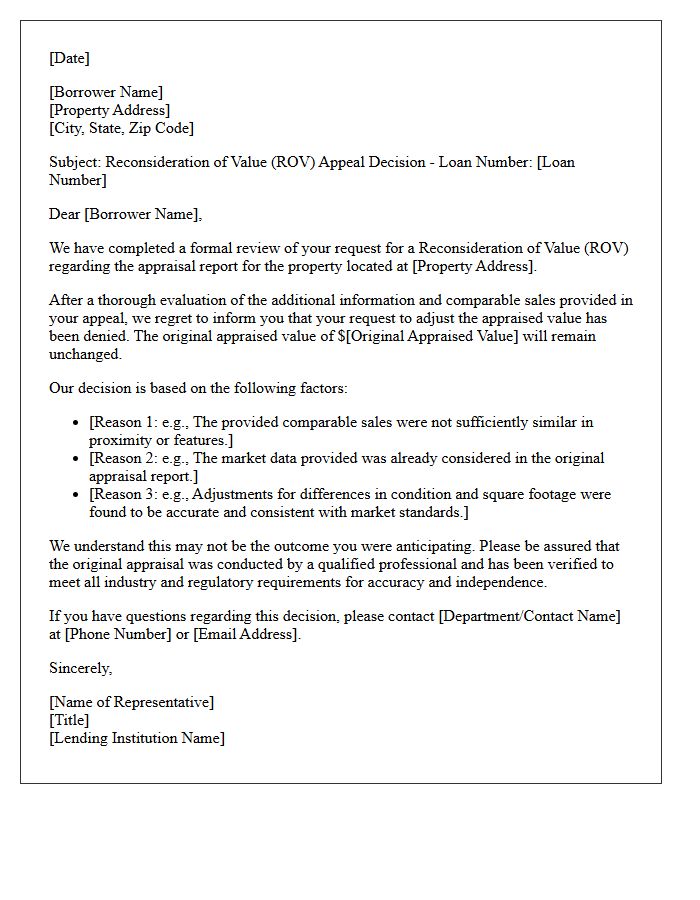

Reconsideration of Value Appeal Rejection Letter

Receiving a Reconsideration of Value (ROV) Appeal Rejection Letter means the lender has upheld the original appraisal despite your submitted evidence. The most critical step is to review the specific reasoning provided for the denial. Common causes include using non-comparable properties or failing to prove material errors in the initial report. If the rejection persists, you may request a second appraisal or file a formal complaint with state regulators. Understanding the appraisal guidelines is essential to determining if further escalation or a new loan application is necessary.

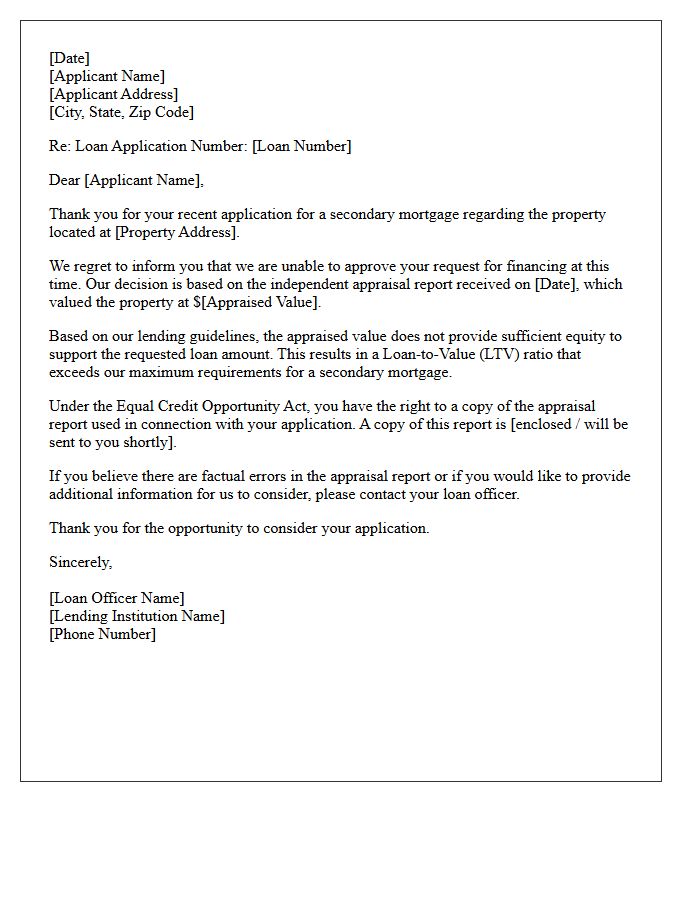

Secondary Mortgage Appraisal Shortfall Decline Letter

A Secondary Mortgage Appraisal Shortfall Decline Letter is a formal notice issued when a property's appraised value is lower than the contract price. This discrepancy creates a valuation gap, preventing the lender from approving the requested loan amount based on the loan-to-value ratio. Borrowers receiving this letter must either bridge the financial difference with a higher down payment, negotiate a lower sale price with the seller, or provide additional market data to dispute the appraisal results to secure financing.

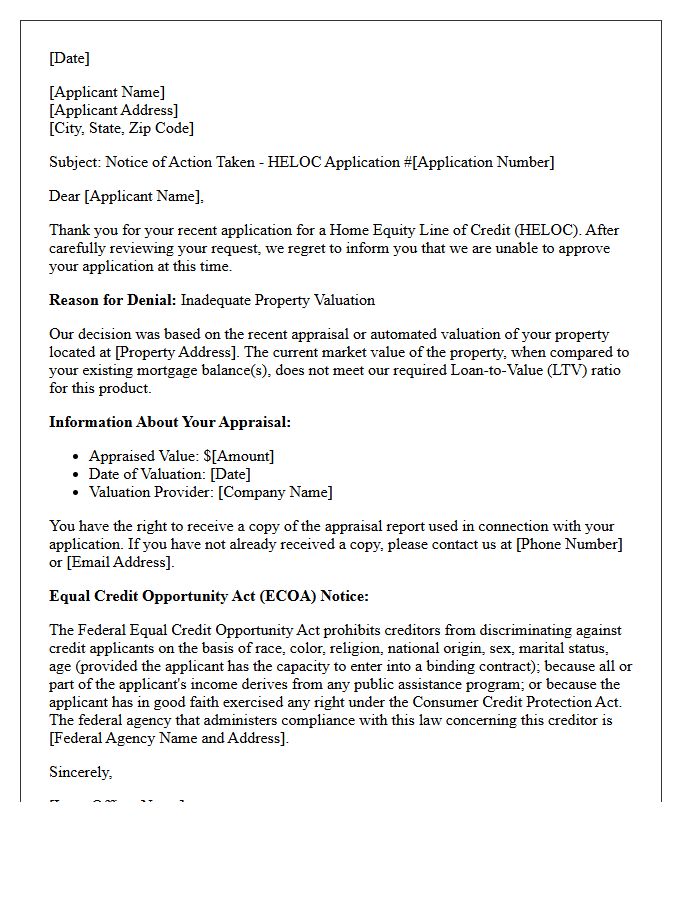

Inadequate Property Valuation HELOC Denial Letter

Receiving an Inadequate Property Valuation denial letter means your Home Equity Line of Credit was rejected because the appraisal came in lower than expected. Lenders use the Loan-to-Value (LTV) ratio to determine risk; if your home's market value is insufficient to secure the requested amount, the application is declined. To move forward, review the report for factual errors, provide comparable sales data for a reconsideration of value, or wait for market conditions to improve. Understanding your equity position is essential for a successful future application.

Notice of Credit Denial Due to Insufficient Equity Letter

A Notice of Credit Denial Due to Insufficient Equity is a formal rejection letter sent when a borrower lacks enough home equity to secure a loan. Lenders calculate the Loan-to-Value (LTV) ratio to assess risk; if the property's appraised value is too low relative to existing debt, the application is denied. This notice is a legal requirement under the Equal Credit Opportunity Act (ECOA), ensuring transparency. Borrowers should review the document to understand if declining market values or high mortgage balances prevented approval for refinancing or equity lines.

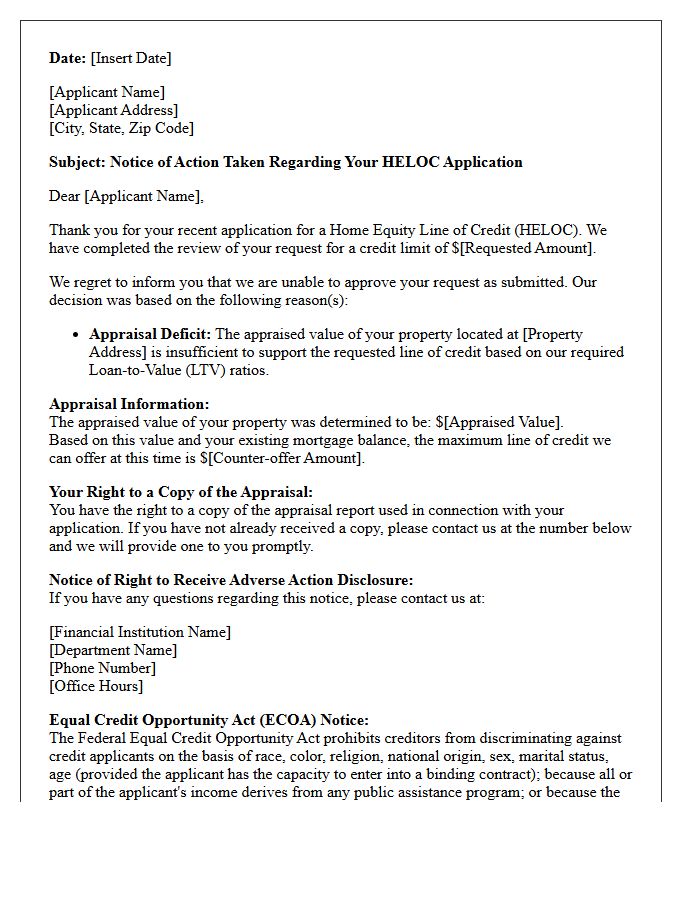

Appraisal Shortfall Counteroffer Notification Letter

An Appraisal Shortfall Counteroffer Notification Letter is a critical legal document used when a property's appraised value is lower than the agreed purchase price. It formally notifies the buyer of the valuation gap and proposes new terms, such as increasing the down payment or adjusting the sale price. This notice protects the seller's interests while offering a framework for renegotiation. Understanding this letter is essential for navigating financing hurdles and ensuring the mortgage approval process continues toward a successful closing despite a low appraisal.

HELOC Application Rejection for Inadequate Collateral Letter

Receiving a HELOC application rejection for inadequate collateral means the lender determined your home's current market value is insufficient to secure the requested credit line. This typically occurs when your Loan-to-Value (LTV) ratio is too high or property values have declined. The adverse action letter specifies that your available home equity does not meet strict underwriting guidelines. To resolve this, you can request a re-appraisal, pay down your existing mortgage balance, or apply for a smaller limit to align with the property's appraised worth.

Property Valuation Shortfall Equity Loan Decline Letter

Receiving a valuation shortfall letter means your lender's appraisal is lower than the purchase price. This discrepancy often leads to an equity loan decline because the loan-to-value ratio exceeds risk limits. To resolve this, you can appeal the appraisal with comparable sales, increase your cash deposit to cover the gap, or seek a second opinion from a different lender. Understanding this gap is crucial for securing financing and ensuring you do not overpay for the asset during the mortgage approval process.

Statement of Credit Denial for Home Equity Line of Credit Letter

A Statement of Credit Denial is a formal notice issued by lenders when your Home Equity Line of Credit application is rejected. Under the Equal Credit Opportunity Act (ECOA), lenders must provide specific reasons for the adverse action, such as a low credit score or insufficient equity. Reviewing this document is crucial for identifying financial discrepancies or areas needing improvement. Understanding these factors helps you address creditworthiness issues before reapplying, ensuring you can eventually leverage your home's value for flexible financing needs.

What is a HELOC appraisal shortfall denial letter?

A HELOC appraisal shortfall denial letter is a formal notification from a lender stating that your Home Equity Line of Credit application was rejected because the appraised value of your property was lower than required to support the requested loan amount.

How does a low appraisal impact my HELOC approval?

Lenders use the appraised value to calculate your Combined Loan-to-Value (CLTV) ratio; if the appraisal is too low, your remaining equity may not meet the lender's strict threshold, resulting in a denial letter based on insufficient collateral.

Can I dispute the valuation mentioned in my HELOC denial letter?

Yes, you can request a "Reconsideration of Value" (ROV) by providing the lender with updated comparable sales data or pointing out factual errors in the original appraisal report that may have led to the shortfall.

What are the most common reasons for a HELOC appraisal shortfall?

Common reasons include a lack of recent comparable home sales in your area, declining local market conditions, property distress, or the appraiser failing to account for high-value interior upgrades and renovations.

What should I do after receiving a HELOC denial due to a low appraisal?

Upon receiving the letter, you should review the appraisal for errors, consider paying down your primary mortgage to increase equity, wait for market conditions to improve, or apply with a different lender who may use a different valuation model.

Comments