Receiving an Incomplete Application Administrative Loan Rejection Letter occurs when essential financial documents or signatures are missing. Lenders issue these formal notices to pause the underwriting process until all requirements are satisfied. Understanding these compliance letters helps applicants rectify errors and expedite future approvals. To help you draft a professional response, below are some ready to use template.

Image cover: Professional Templates for Incomplete Loan Application Rejection Letters

Letter Samples List

- Missing Income Verification Administrative Loan Rejection Letter

- Unsigned Application Form Administrative Loan Rejection Letter

- Expired Identification Document Administrative Loan Rejection Letter

- Incomplete Tax Return Documentation Administrative Loan Rejection Letter

- Missing Bank Statements Administrative Loan Rejection Letter

- Unverified Employment History Administrative Loan Rejection Letter

- Missing Guarantor Signature Administrative Loan Rejection Letter

- Incomplete Personal Information Administrative Loan Rejection Letter

- Failure To Submit Requested Documents Administrative Loan Rejection Letter

- Incomplete Property Appraisal Administrative Loan Rejection Letter

- Unanswered Information Request Administrative Loan Rejection Letter

- Missing Insurance Policy Proof Administrative Loan Rejection Letter

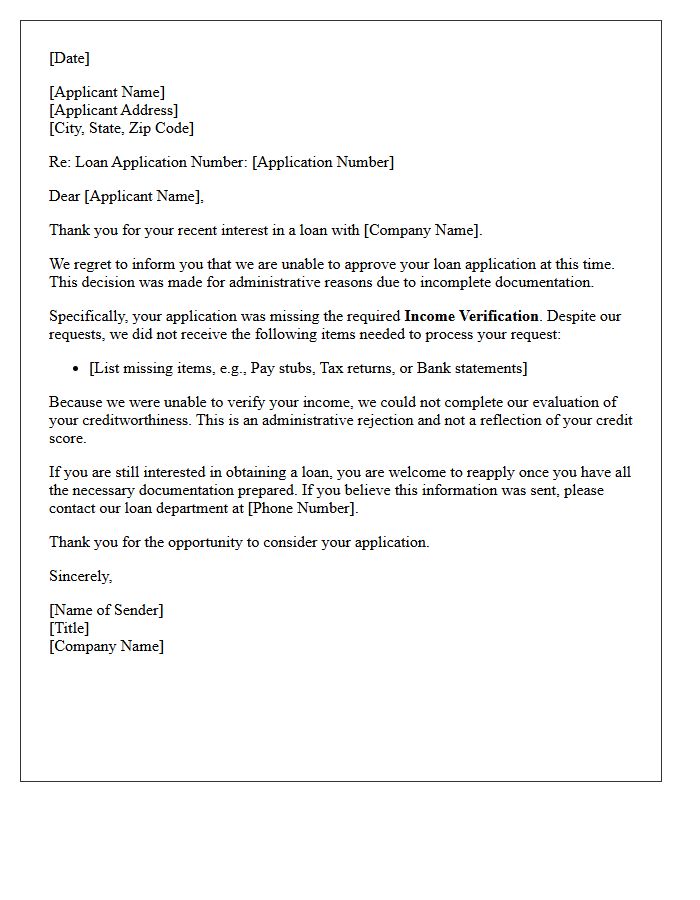

Missing Income Verification Administrative Loan Rejection Letter

A Missing Income Verification letter is a formal notice stating your loan application was rejected due to insufficient financial documentation. Lenders require proof of earnings to assess your debt-to-income ratio and repayment capacity. This administrative rejection occurs when submitted documents, like pay stubs or tax returns, are incomplete, expired, or unverifiable. To resolve this, you must promptly provide the requested evidence to appeal the decision. Ensuring your income records are accurate and transparent is the most critical step in securing loan approval and demonstrating financial stability to the underwriter.

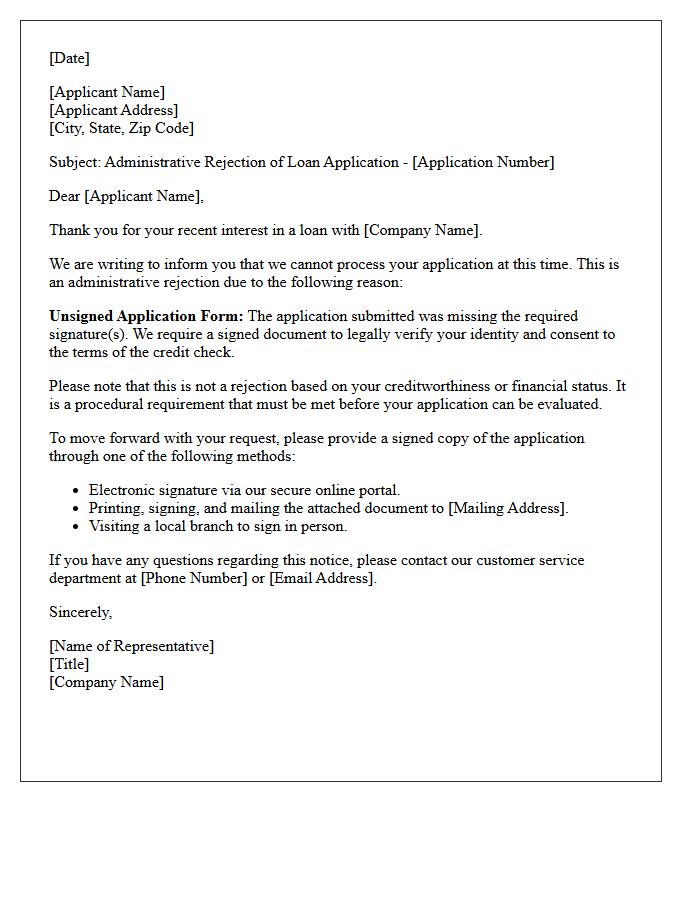

Unsigned Application Form Administrative Loan Rejection Letter

An unsigned application form is a common administrative reason for receiving a loan rejection letter. Lenders require a valid signature to legally process your request and verify consent. This administrative denial does not reflect your creditworthiness but indicates an incomplete submission. To resolve this, you must review the rejection notice, sign the document physically or electronically as required, and resubmit it promptly. Ensuring all forms are fully executed prevents unnecessary processing delays and improves your chances of approval during the underwriting stage.

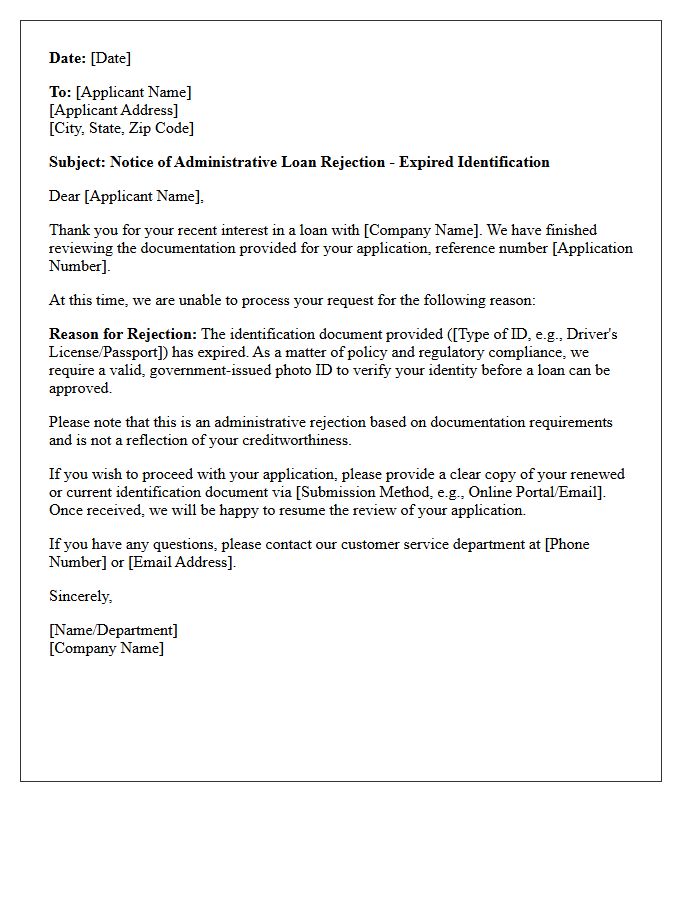

Expired Identification Document Administrative Loan Rejection Letter

An Expired Identification Document Administrative Loan Rejection Letter is a formal notification from a lender stating that a credit application cannot proceed due to invalid credentials. Financial institutions require current government-issued IDs to comply with Know Your Customer (KYC) regulations and anti-fraud laws. This rejection is administrative rather than credit-based, meaning it does not reflect your financial reliability. To resolve this, you must provide a valid, unexpired photo ID to restart the verification process. Ensuring your documentation is up-to-date is essential for successful identity authentication and loan approval.

Incomplete Tax Return Documentation Administrative Loan Rejection Letter

An Incomplete Tax Return Documentation Administrative Loan Rejection Letter notifies applicants that their financing request was denied due to missing or unverifiable IRS records. Lenders require full transcripts to assess creditworthiness and income stability. Receiving this notice means your file lacked critical schedules or signatures necessary for processing. To rectify this administrative denial, you must provide the complete, certified tax documents requested. Ensuring all financial disclosures are comprehensive and match reported figures is essential to successfully appeal the decision or resubmit your loan application for future approval.

Missing Bank Statements Administrative Loan Rejection Letter

A Missing Bank Statements Administrative Loan Rejection Letter is a formal notice issued by lenders when a loan application cannot be processed due to incomplete financial documentation. This is an administrative denial rather than a credit-based rejection. To rectify this, applicants must promptly provide the specific missing monthly records to prove income stability and cash flow. Failing to submit these documents prevents underwriters from assessing repayment capacity. Always ensure all pages, including blank ones, are included to successfully appeal the decision and move the approval process forward.

Unverified Employment History Administrative Loan Rejection Letter

An Unverified Employment History letter is a formal notice stating that a loan application was denied because the lender could not confirm your job details. This typically occurs when a previous employer fails to respond to inquiries or payroll records are missing. This administrative rejection is not a final judgment on your creditworthiness but indicates a break in the verification chain. To resolve this, provide alternative documentation like tax returns, W-2 forms, or certified pay stubs to prove stable income and secure future approval.

Missing Guarantor Signature Administrative Loan Rejection Letter

Receiving a Missing Guarantor Signature Administrative Loan Rejection Letter indicates a formal denial based on incomplete documentation rather than poor credit. This notice signifies that the co-signer failed to execute the legally binding agreement required for security. Because this is an administrative error, the rejection is typically reversible. To rectify the status, you must ensure the guarantor provides a verified signature promptly. Addressing this compliance gap immediately allows the lender to resume processing your application without necessitating a completely new submission or manual underwriting review.

Incomplete Personal Information Administrative Loan Rejection Letter

An Incomplete Personal Information Administrative Loan Rejection Letter is a formal notice stating your application cannot be processed due to missing or unverified data. This administrative denial typically occurs when basic details, such as identity verification, contact information, or residency history, are omitted. Unlike credit-based rejections, this is often a procedural issue that can be resolved by providing the requested documentation. To proceed, applicants must carefully review the omission notice and resubmit the correct information promptly to ensure the lender can finalize their comprehensive financial evaluation.

Failure To Submit Requested Documents Administrative Loan Rejection Letter

Receiving a Failure to Submit Requested Documents administrative loan rejection letter means your application was denied due to incomplete paperwork rather than poor credit. This is a procedural denial indicating that the lender lacked necessary evidence, such as tax returns or income verification, to finalize their decision. To resolve this, review the letter's specific list of missing items and submit them immediately. Often, you can reopen the file or reapply without penalty once all documentation is provided. Timely communication with your loan officer is essential to prevent further processing delays.

Incomplete Property Appraisal Administrative Loan Rejection Letter

An Incomplete Property Appraisal Administrative Loan Rejection Letter notifies applicants that their mortgage request was denied due to missing or insufficient valuation data. This administrative denial occurs when the appraiser cannot access the interior, legal documents are absent, or required repairs remain unverified. It is not necessarily a final rejection of creditworthiness, but a procedural halt until the collateral assessment is finalized. To resolve this, borrowers must coordinate with the lender to provide missing information or reschedule a comprehensive inspection to meet underwriting guidelines.

Unanswered Information Request Administrative Loan Rejection Letter

An Unanswered Information Request administrative loan rejection occurs when a lender denies an application because the borrower failed to provide required documentation within a specific timeframe. This is not a reflection of creditworthiness, but a procedural denial. To resolve this, applicants should immediately review the notice of incompleteness, gather the missing records, and ask for a file reconsideration. Maintaining clear communication and meeting deadlines is essential to avoid permanent loan rejection due to administrative gaps in the underwriting process.

Missing Insurance Policy Proof Administrative Loan Rejection Letter

Receiving an administrative loan rejection due to missing insurance policy proof means your application is paused, not permanently denied. Lenders require proof of coverage to protect the collateral against potential risks. To resolve this, you must promptly provide a valid declarations page or insurance binder that lists the lender as the loss payee. Ensuring your policy meets the specific minimum coverage requirements outlined in your loan agreement is essential for successful reconsideration. Once documentation is verified, the administrative hold is typically lifted, allowing the funding process to continue toward final approval.

What does an "Incomplete Application" administrative rejection mean?

An administrative rejection for an incomplete application means your loan request was not evaluated on its financial merits because required documentation or specific data fields were missing from the submission.

Can I appeal a loan rejection based on an incomplete application?

Most lenders do not offer a formal appeal for administrative rejections; instead, you are typically encouraged to submit a new, complete application that includes all the missing information identified in your rejection letter.

Will an administrative rejection for an incomplete application hurt my credit score?

The rejection itself does not impact your credit score, but the hard inquiry performed when you initially applied may result in a temporary minor decrease in your overall credit rating.

How long do I have to provide missing documents after receiving a rejection notice?

Once a formal rejection letter is issued, the application is usually closed. You must generally restart the application process, although some lenders may allow a grace period of 30 days to reopen the file if the missing documents are provided promptly.

What are the most common reasons for an incomplete application rejection?

The most common reasons include missing tax returns, unsigned disclosure forms, lack of proof of income, or failure to provide valid identification documents required under federal "Know Your Customer" (KYC) regulations.

Comments