Receiving a guarantor credit unworthiness loan rejection letter indicates that a co-signer's financial profile failed to meet lender requirements. This notification explains how poor credit scores or high debt-to-income ratios impacted the application outcome. Understanding these specific grounds for refusal is essential for improving future approval chances. To help you draft or understand these notices, below are some ready to use template.

Image cover: Declined Loan Application: Guarantor Credit Standards Notification Templates

Letter Samples List

- Guarantor Credit Unworthiness Loan Rejection Letter

- Notice of Loan Denial Due to Guarantor Credit Letter

- Unfavorable Guarantor Credit History Loan Rejection Letter

- Commercial Loan Declination Based on Guarantor Credit Letter

- Insufficient Guarantor Credit Score Loan Rejection Letter

- Guarantor Financial Ineligibility Loan Denial Letter

- Adverse Action and Guarantor Credit Rejection Letter

- Unqualified Guarantor Loan Application Rejection Letter

- Co-Signer Credit Unworthiness Loan Decline Letter

- Primary Guarantor Credit Failure Loan Rejection Letter

- Guarantor Credit Check Failure Loan Denial Letter

- Business Loan Rejection Due to Guarantor Credit Letter

- Inadequate Guarantor Credit Profile Loan Rejection Letter

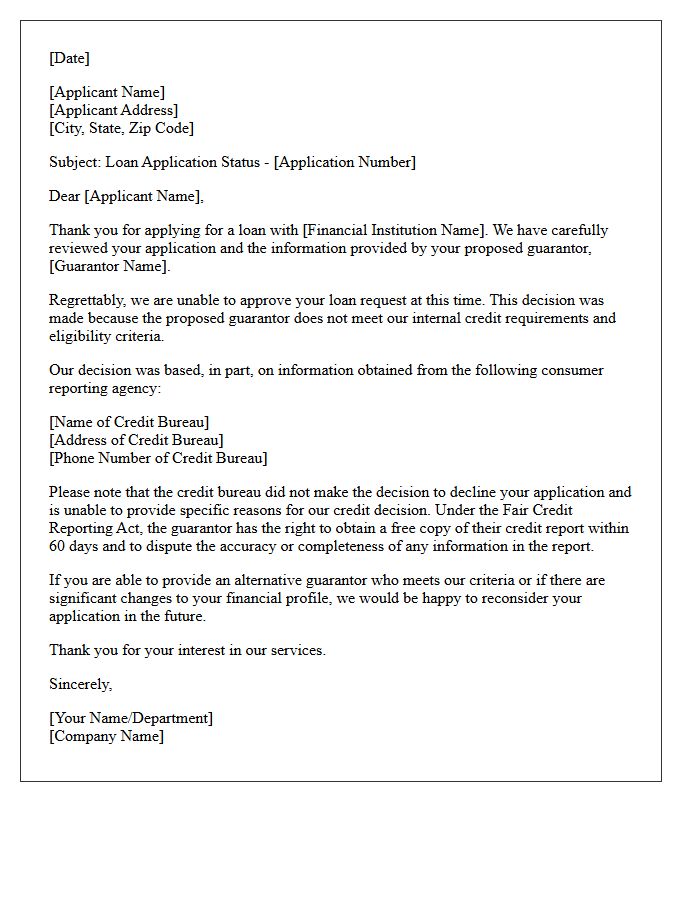

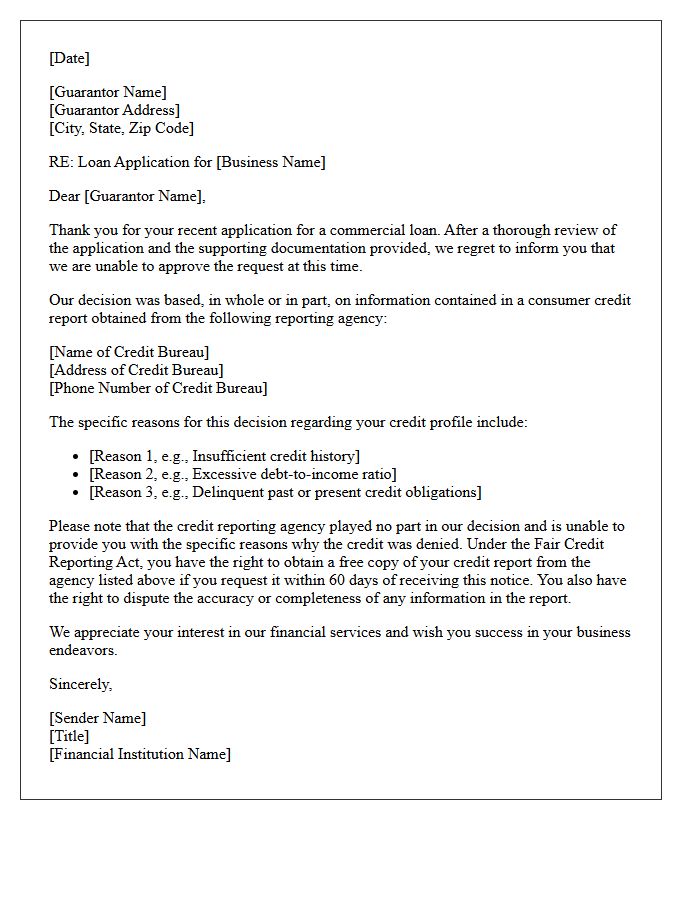

Guarantor Credit Unworthiness Loan Rejection Letter

A Guarantor Credit Unworthiness Loan Rejection Letter officially informs an applicant that their loan request was denied due to the guarantor's poor financial standing. Lenders issue this notice when the cosigner fails to meet specific credit score requirements or debt-to-income benchmarks. This document is essential for transparency, often citing the Adverse Action notice guidelines. It protects the lender from high-risk defaults while advising the borrower to seek an alternative guarantor with a stronger repayment history to improve future approval chances.

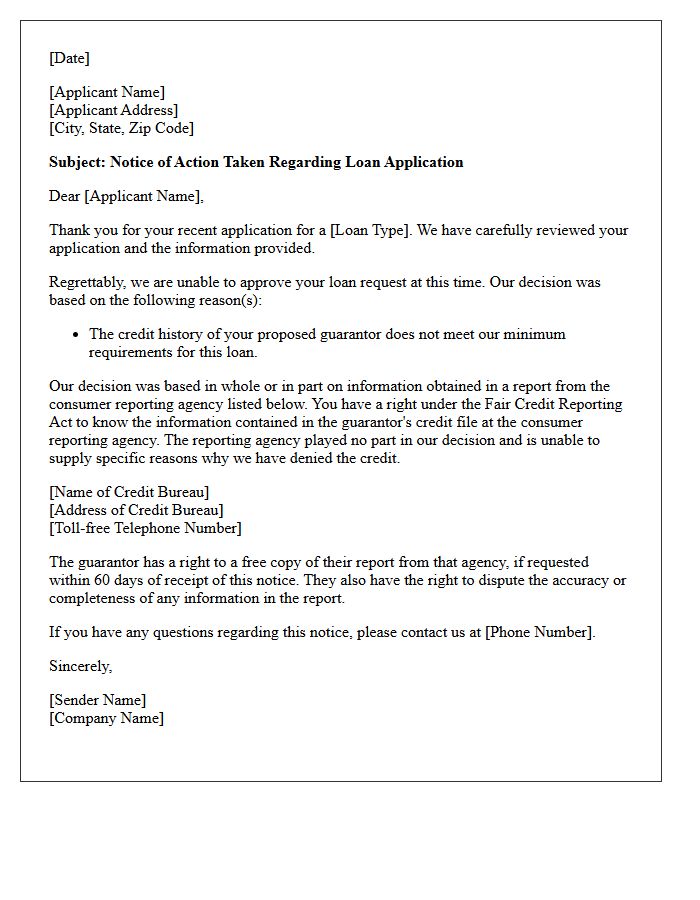

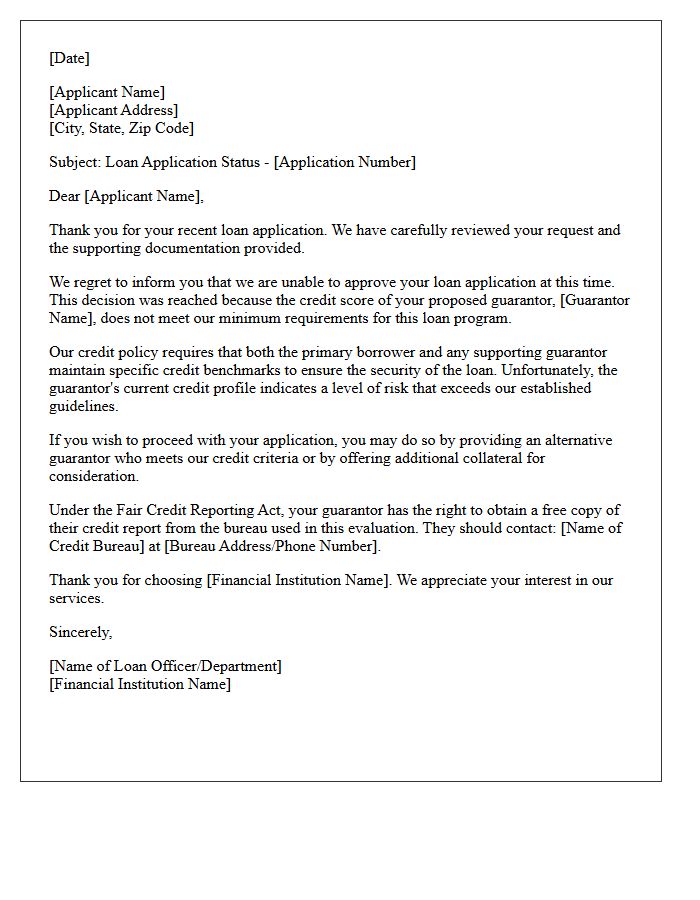

Notice of Loan Denial Due to Guarantor Credit Letter

A Notice of Loan Denial Due to Guarantor Credit is a formal letter issued by lenders when a loan application is rejected specifically because of a co-signer's adverse credit history. Under the Equal Credit Opportunity Act, the lender must provide an Adverse Action Notice explaining the decision. This letter identifies the credit reporting agency used and outlines the guarantor's rights to dispute inaccuracies. It protects the primary borrower's privacy while informing them that the guarantor's financial standing failed to meet the required underwriting standards for approval.

Unfavorable Guarantor Credit History Loan Rejection Letter

An Unfavorable Guarantor Credit History Loan Rejection Letter is a formal notice sent when a loan application is denied due to a co-signer's poor financial standing. Lenders prioritize creditworthiness to mitigate risk, and negative data-such as defaults or low scores-can disqualify an applicant. It is crucial to review the Adverse Action Notice provided, which explains the specific reasons for denial. Applicants should communicate with their guarantor to address errors or consider an alternative individual with a stronger repayment profile to improve their chances of future approval.

Commercial Loan Declination Based on Guarantor Credit Letter

A Commercial Loan Declination Based on Guarantor Credit Letter is a formal notice issued when a business loan application is rejected due to a backer's personal financial history. Lenders prioritize guarantor credibility because business entities often lack sufficient standalone credit. This letter specifies that the credit report of the individual guarantor failed to meet risk standards, citing factors like low scores or delinquencies. Understanding this document is vital for credit restoration and identifying specific financial weaknesses that must be addressed before reapplying for commercial financing.

Insufficient Guarantor Credit Score Loan Rejection Letter

An Insufficient Guarantor Credit Score Loan Rejection Letter is a formal notification stating that a loan application was denied because the co-signer failed to meet the required creditworthiness benchmarks. Lenders issue this document to explain that the guarantor's financial history poses too high a risk for the debt obligation. Key information includes the specific credit reporting agency used and the primary reasons for the low score. To improve future outcomes, the applicant should seek a new guarantor with a stronger credit profile or work on improving the existing co-signer's standing.

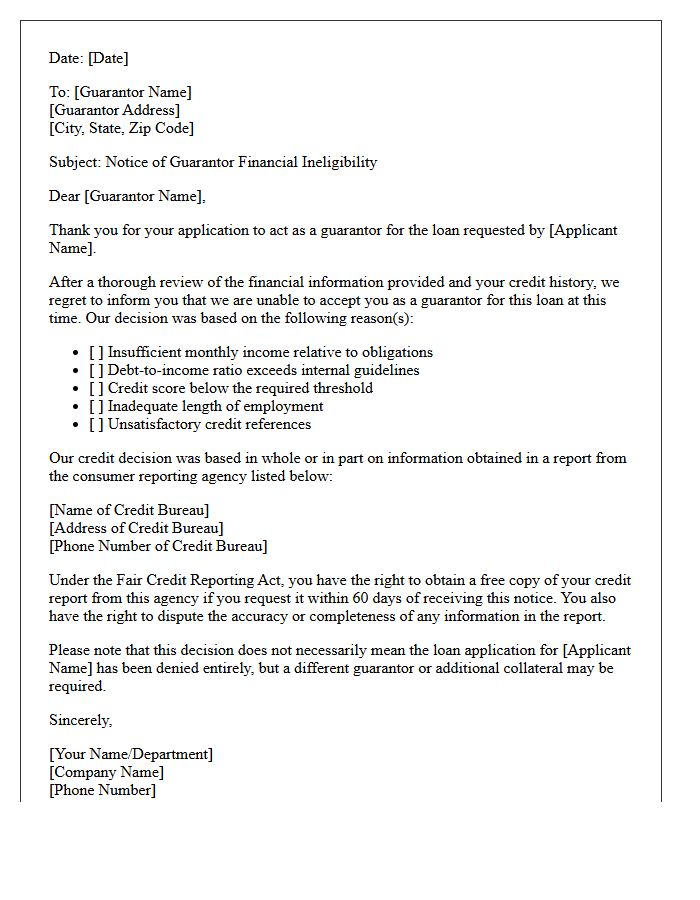

Guarantor Financial Ineligibility Loan Denial Letter

A Guarantor Financial Ineligibility Loan Denial Letter is a formal notice issued when a loan application is rejected due to the co-signer's poor credit or insufficient income. Lenders issue this adverse action notice to inform the primary borrower that their backer does not meet the necessary underwriting criteria. Understanding the specific denial reasons is crucial, as the guarantor may need to improve their debt-to-income ratio or credit score. To proceed, the applicant must typically find a more qualified guarantor or provide additional collateral to mitigate the lender's perceived risk.

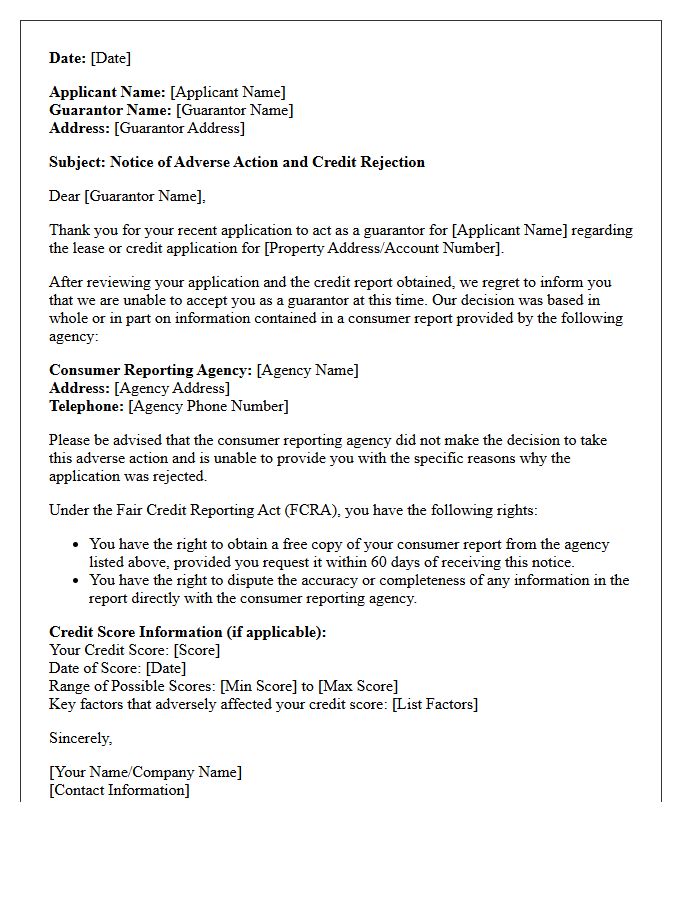

Adverse Action and Guarantor Credit Rejection Letter

When a business denies credit based on a Guarantor's financial history, federal law requires a formal Adverse Action Notice. This letter must clearly state the specific reasons for the rejection, such as a low credit score or insufficient income. Under the Equal Credit Opportunity Act (ECOA), lenders are obligated to provide the contact information of the credit bureau used. Transparent communication ensures legal compliance and allows the individual to address potential credit report inaccuracies or improve their financial standing for future applications.

Unqualified Guarantor Loan Application Rejection Letter

An Unqualified Guarantor Loan Application Rejection Letter serves as formal notice that a loan request was denied because the co-signer failed to meet specific eligibility criteria. Common reasons include a poor credit history, insufficient income, or unstable employment status of the guarantor. This document is essential for regulatory compliance, ensuring transparency regarding why the financial backing was deemed inadequate. Applicants should review the specific adverse action reasons provided to identify if they need to find a new creditworthy guarantor or improve their overall financial profile before reapplying for the debt instrument.

Co-Signer Credit Unworthiness Loan Decline Letter

A Co-Signer Credit Unworthiness Loan Decline Letter is a formal notification issued when a loan application is rejected due to the guarantor's poor financial standing. It is crucial to understand that even if the primary borrower has sufficient income, the lender may deny credit if the co-signer fails to meet specific credit score or debt-to-income thresholds. Under the Fair Credit Reporting Act, the letter must disclose which credit bureau provided the data. This document protects the lender from risk and informs both parties about the specific adverse action taken.

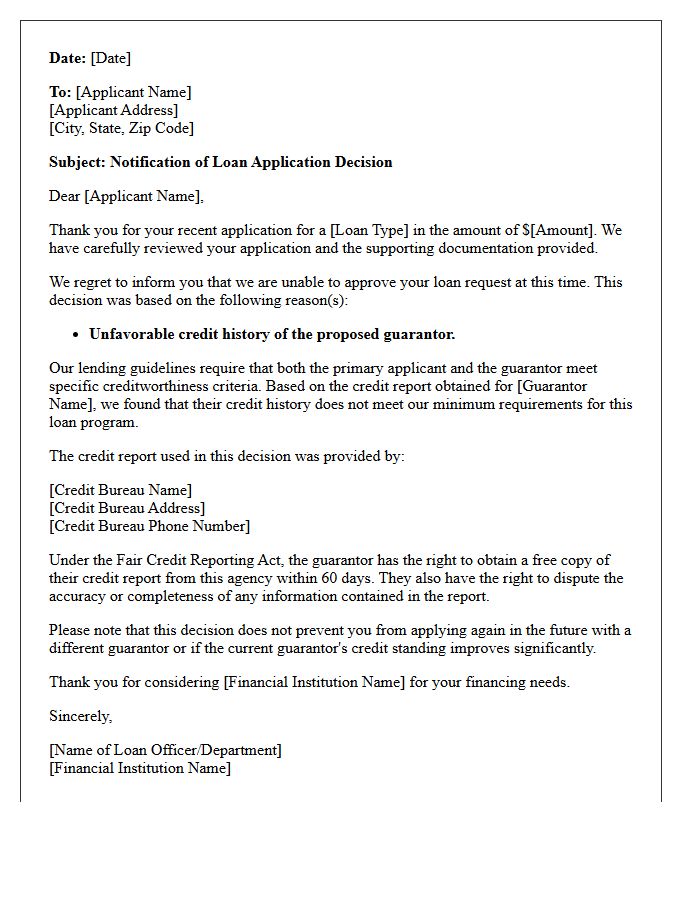

Primary Guarantor Credit Failure Loan Rejection Letter

A Primary Guarantor Credit Failure Loan Rejection Letter notifies an applicant that their request was denied due to the guarantor's poor credit history. Even if the borrower meets all requirements, the financial institution views the co-signer's fiscal instability as an unacceptable risk. This formal document outlines the specific credit reporting agency used and provides instructions on how to dispute inaccuracies. Understanding this rejection is vital, as it indicates the need for a stronger financial backup or a different security arrangement to successfully secure future funding or credit lines.

Guarantor Credit Check Failure Loan Denial Letter

Receiving a Guarantor Credit Check Failure Loan Denial Letter indicates that the lender rejected your application due to the co-signer's poor financial history. This notice is a legal requirement under the Fair Credit Reporting Act. It must specify which credit bureau provided the data and explain that the guarantor's low credit score or negative payment history failed to meet risk standards. To move forward, you should review the adverse action details, request a free credit report for the guarantor to dispute errors, or find a different person with stronger credit.

Business Loan Rejection Due to Guarantor Credit Letter

A business loan rejection due to a guarantor credit letter often occurs when a co-signer's financial history reveals negative credit marks or high debt ratios. Lenders require personal guarantees to mitigate risk; therefore, poor personal scores can disqualify the entire application regardless of business performance. It is vital to review credit reports for errors before applying. To improve approval odds, ensure your guarantor maintains a strong credit profile or consider offering additional collateral to offset concerns regarding personal financial stability and repayment reliability during the underwriting process.

Inadequate Guarantor Credit Profile Loan Rejection Letter

An Inadequate Guarantor Credit Profile Loan Rejection Letter informs an applicant that their loan was denied specifically due to the co-signer's financial history. This adverse action notice is mandatory under the Equal Credit Opportunity Act (ECOA). It typically identifies issues such as a low credit score, excessive debt, or derogatory marks on the guarantor's report. Lenders must provide specific reasons for the denial and offer information on how the guarantor can obtain a free copy of their credit report to dispute any potential inaccuracies or improve their future eligibility.

What is a guarantor credit unworthiness loan rejection letter?

A guarantor credit unworthiness loan rejection letter is a formal notice sent by a lender informing a loan applicant that their request was denied specifically because the proposed guarantor failed to meet the required credit standards or financial criteria.

Why was my loan denied due to my guarantor's credit score?

Your loan was denied because the lender's risk assessment determined that the guarantor's credit history, debt-to-income ratio, or repayment track record was insufficient to secure the debt in the event that you are unable to make payments.

Does a rejection based on a guarantor's credit affect the applicant's credit score?

The rejection itself is not recorded on your credit report; however, the hard inquiry performed by the lender during the application process may cause a temporary, minor decrease in your credit score.

Can I reapply for the loan if I find a different guarantor?

Yes, most lenders allow you to submit a new application or update your current one with a different guarantor who possesses a stronger credit profile and meets the lender's eligibility requirements.

What should a guarantor do if they receive a notice of credit unworthiness?

The guarantor should request a copy of the credit report used in the decision to check for errors, dispute any inaccuracies with the credit bureaus, and take steps to improve their credit utilization and payment history before attempting to guarantee a loan again.

Comments