Receiving a mortgage application denial due to insufficient income can be a significant setback in your home-buying journey. Lenders issue these notices when a borrower's debt-to-income ratio exceeds established risk thresholds. Understanding the specific reasons for rejection is essential for improving your financial profile and reapplying successfully. To assist your communication with lenders, below are some ready to use templates.

Image cover: Declined Mortgage Application: Income Insufficient Templates and Notice Samples

Letter Samples List

- Standard Mortgage Insufficient Income Denial Letter

- Adverse Action Mortgage Income Denial Letter

- High Debt-to-Income Ratio Mortgage Rejection Letter

- Unverifiable Employment Income Mortgage Denial Letter

- Self-Employment Insufficient Income Mortgage Rejection Letter

- Co-Borrower Income Shortfall Mortgage Denial Letter

- Inadequate Combined Household Income Mortgage Decline Letter

- Insufficient Projected Income Mortgage Application Denial Letter

- Secondary Income Disqualification Mortgage Denial Letter

- Minimum Income Requirement Unmet Mortgage Rejection Letter

- Variable Income Unpredictability Mortgage Denial Letter

- Notice of Action Taken Insufficient Income Letter

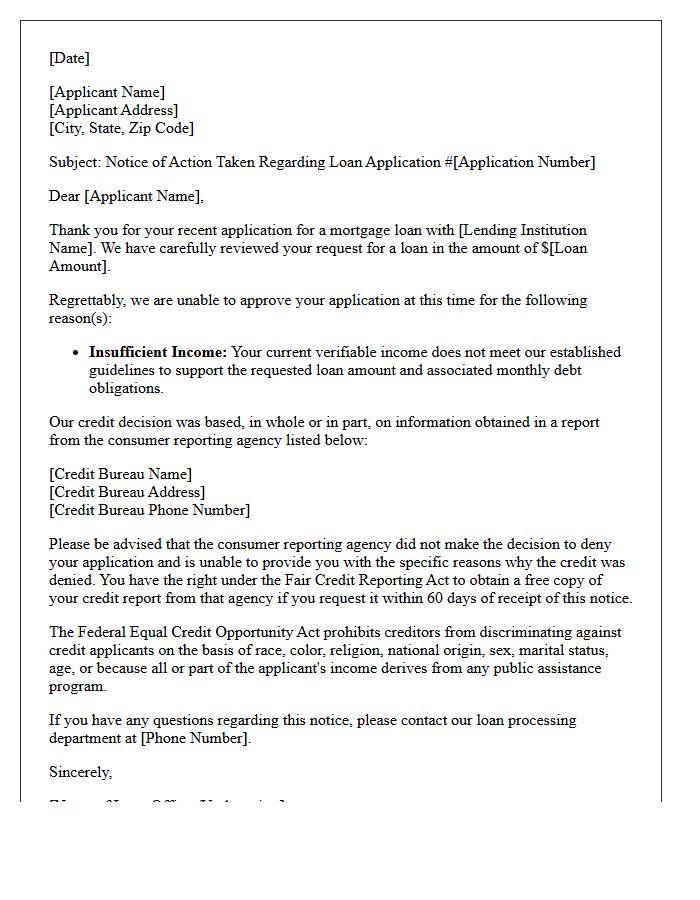

Standard Mortgage Insufficient Income Denial Letter

A Standard Mortgage Insufficient Income Denial Letter is a formal notice issued by lenders when a borrower's Debt-to-Income (DTI) ratio exceeds regulatory or internal guidelines. This document specifies that the applicant's verified gross monthly earnings are inadequate to cover the proposed housing payment alongside existing financial obligations. To address this rejection, borrowers should review the specific income sources analyzed, consider adding a co-signer, or focus on paying down current debts to improve their qualifying profile for a future mortgage application. Understanding these documented reasons is essential for financial restructuring.

Adverse Action Mortgage Income Denial Letter

An Adverse Action Notice is a formal document issued when a lender rejects your loan application. If the reason is an income denial, it signifies that your documented earnings failed to meet the debt-to-income (DTI) thresholds or stability requirements. Under the Equal Credit Opportunity Act, lenders must specify why you were declined. Reviewing this letter is essential to identify if the issue involves insufficient gross pay, unverified side income, or excessive existing debts, allowing you to improve your financial profile before reapplying.

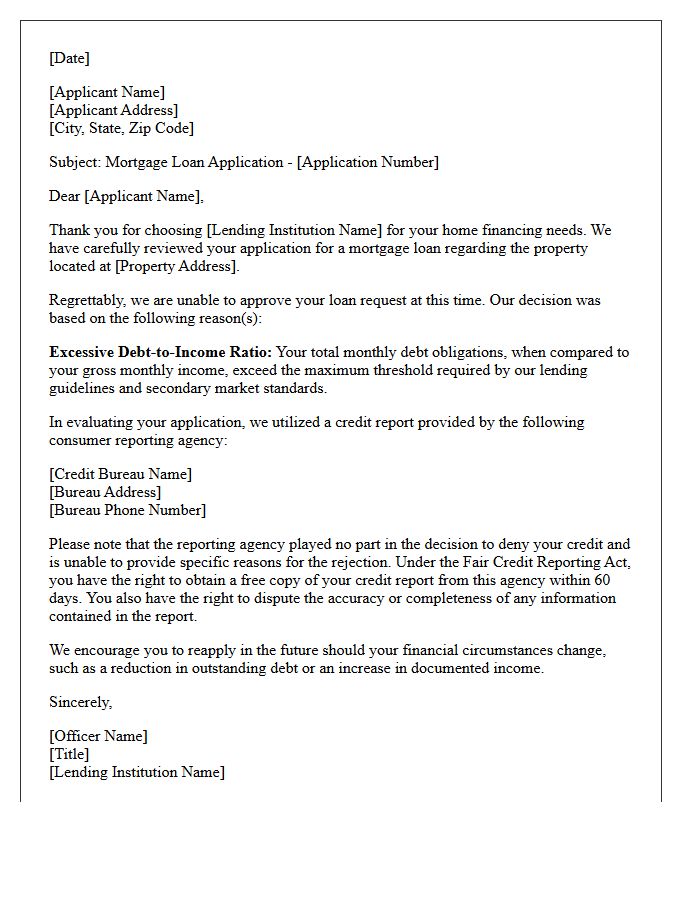

High Debt-to-Income Ratio Mortgage Rejection Letter

Receiving a mortgage rejection letter due to a high Debt-to-Income (DTI) ratio indicates that your monthly debt obligations are too high relative to your gross income. Lenders perceive this as a financial risk, fearing you cannot manage additional loan payments. To improve future approval chances, focus on paying down balances or increasing your total earnings. Review the letter carefully to identify the specific threshold you exceeded, as most conventional loans require a DTI below 43% to meet standard qualifying guidelines and ensure long-term housing affordability.

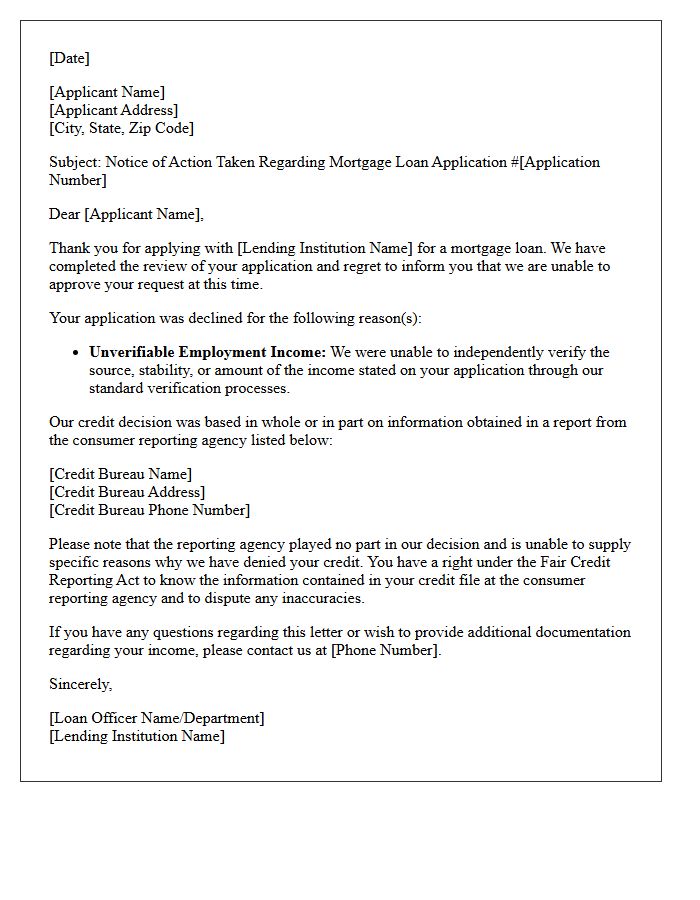

Unverifiable Employment Income Mortgage Denial Letter

An Unverifiable Employment Income Mortgage Denial Letter is a formal notice stating your loan was rejected because the lender could not confirm your earnings. This often occurs due to non-traditional income, gaps in work history, or insufficient documentation for self-employment. Lenders require stable, documented proof to ensure repayment ability. To resolve this, you must provide secondary evidence like tax returns, 1099s, or bank statements. Reviewing the letter helps identify specific underwriting gaps so you can improve your financial profile or seek specialized mortgage products for your next application.

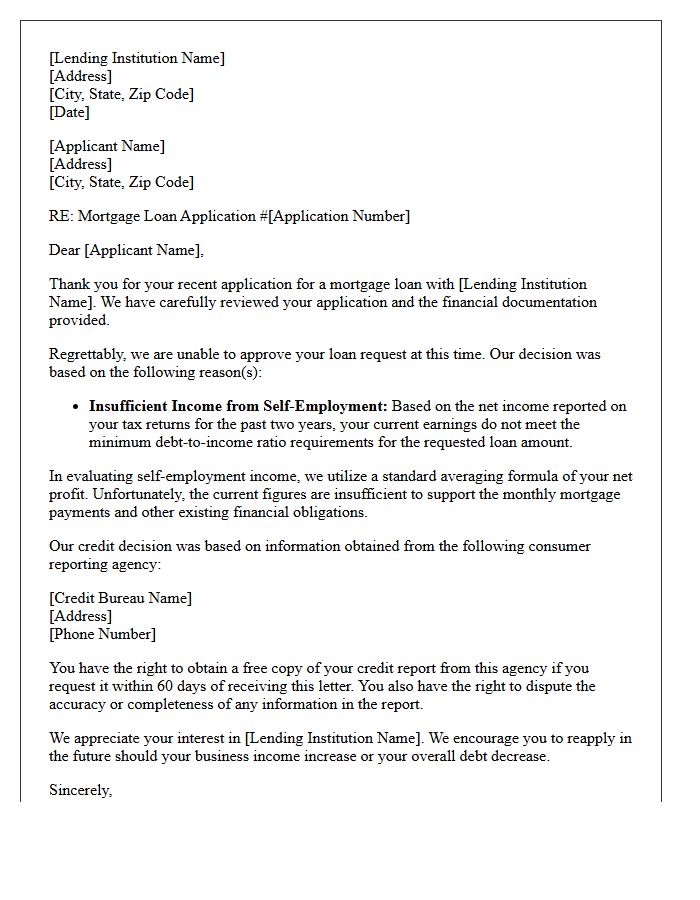

Self-Employment Insufficient Income Mortgage Rejection Letter

A self-employment mortgage rejection letter typically cites insufficient income when net profits, after tax deductions, fail to meet debt-to-income requirements. Lenders prioritize historical stability, often averaging the last two years of tax returns. If recent earnings fluctuate or significant expenses lower your taxable total, you may face a denial. To overturn this, provide audited financial statements or explore bank statement loans that focus on gross cash flow rather than net profit. Understanding these underwriting criteria is essential for self-employed borrowers to secure future financing approval.

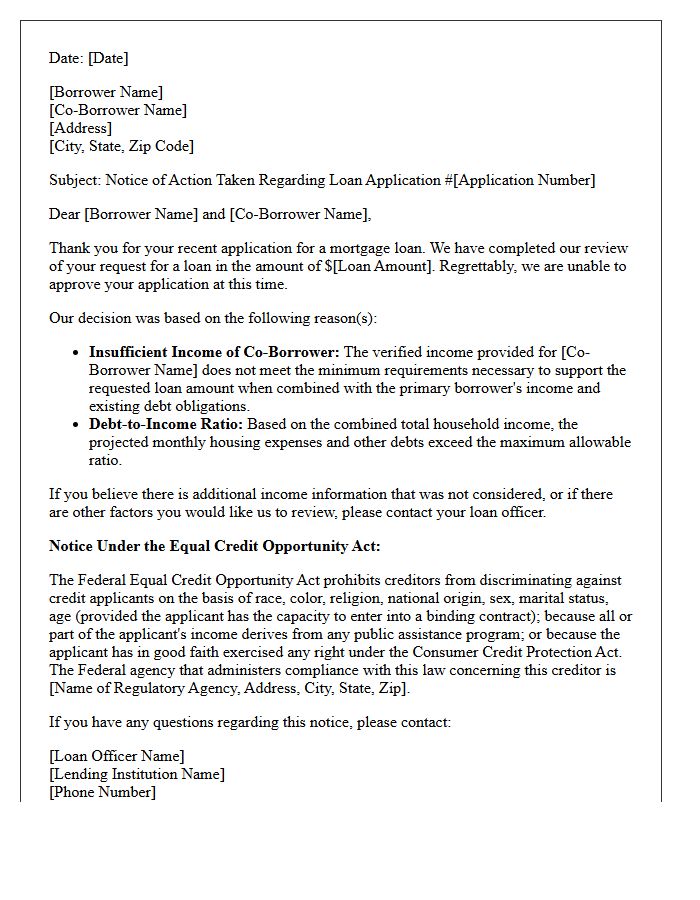

Co-Borrower Income Shortfall Mortgage Denial Letter

A Co-Borrower Income Shortfall Mortgage Denial Letter is a formal notice issued when a lender rejects a loan application because the combined debt-to-income ratio fails to meet underwriting standards. This document specifies that the secondary applicant's earnings, or the joint total, are insufficient to cover the requested monthly payments and existing liabilities. Understanding this letter is crucial for identifying financial gaps, allowing applicants to improve their credit profile, pay down debts, or seek a lower loan amount before reapplying for a mortgage.

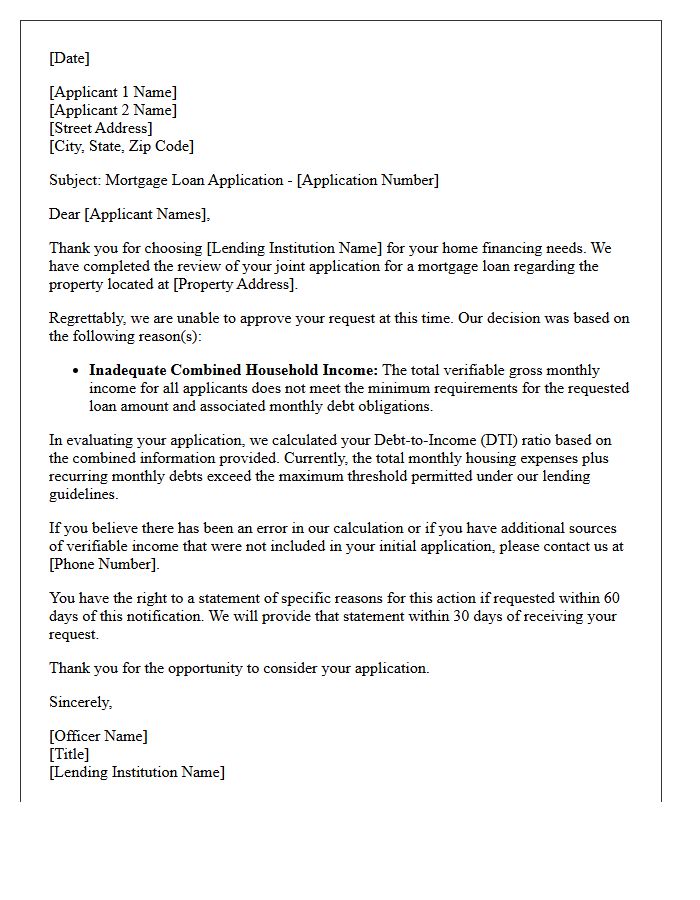

Inadequate Combined Household Income Mortgage Decline Letter

An Inadequate Combined Household Income decline letter is a formal notification from a lender stating your total earnings fail to meet the debt-to-income ratio requirements. This occurs when the pooled gross income of all co-borrowers is insufficient to cover the proposed mortgage payment plus existing monthly liabilities. To resolve this, you may need to reduce current debts, provide proof of additional supplementary earnings, or increase your down payment to lower the loan amount. Reviewing the specific figures in the letter helps identify the exact financial gap needed for a future approval.

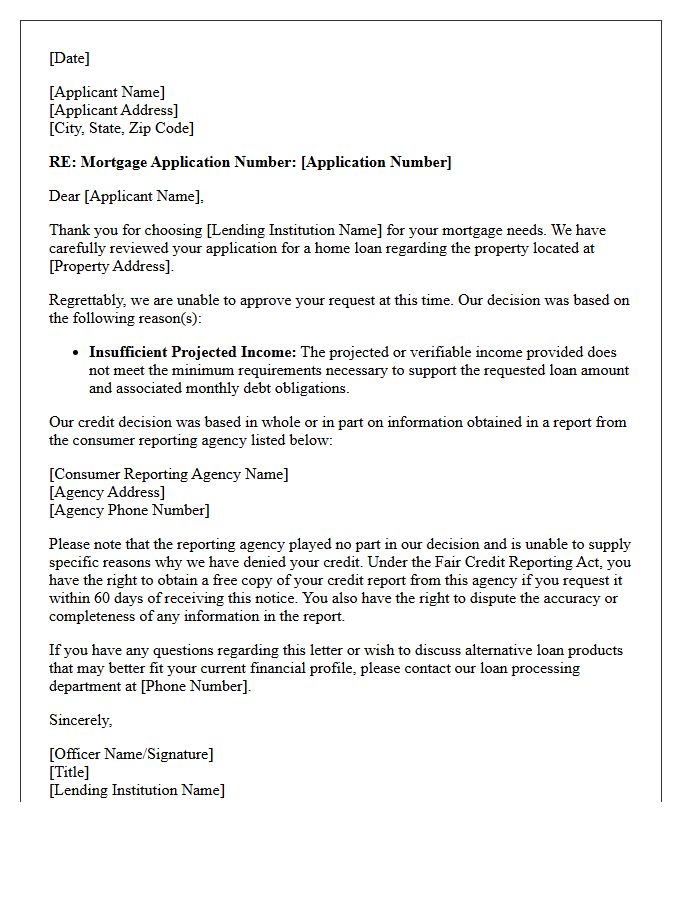

Insufficient Projected Income Mortgage Application Denial Letter

An Insufficient Projected Income letter is a formal notice that your mortgage application was denied because the lender's analysis suggests your future earnings won't cover monthly payments. This often occurs when your Debt-to-Income (DTI) ratio exceeds regulatory limits. Lenders evaluate variable components like bonuses, commissions, or self-employment history to determine reliability. To resolve this, you may need to provide additional financial documentation, increase your down payment, or settle existing debts to lower your monthly obligations and qualify for the desired loan amount.

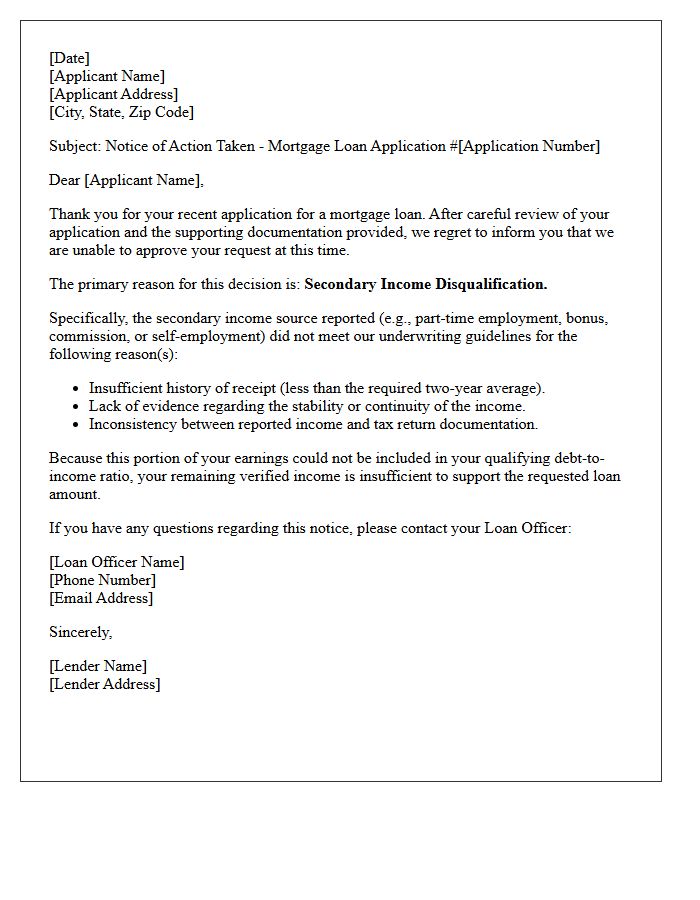

Secondary Income Disqualification Mortgage Denial Letter

A Secondary Income Disqualification occurs when a lender excludes additional earnings from your debt-to-income ratio. This often happens because the income lacks a consistent two-year history or is not expected to continue. Receiving a mortgage denial letter for this reason means your primary salary alone is insufficient to cover the loan. To resolve this, ensure all side earnings are documented via tax returns and meet the stability requirements set by underwriting guidelines to prove long-term financial reliability.

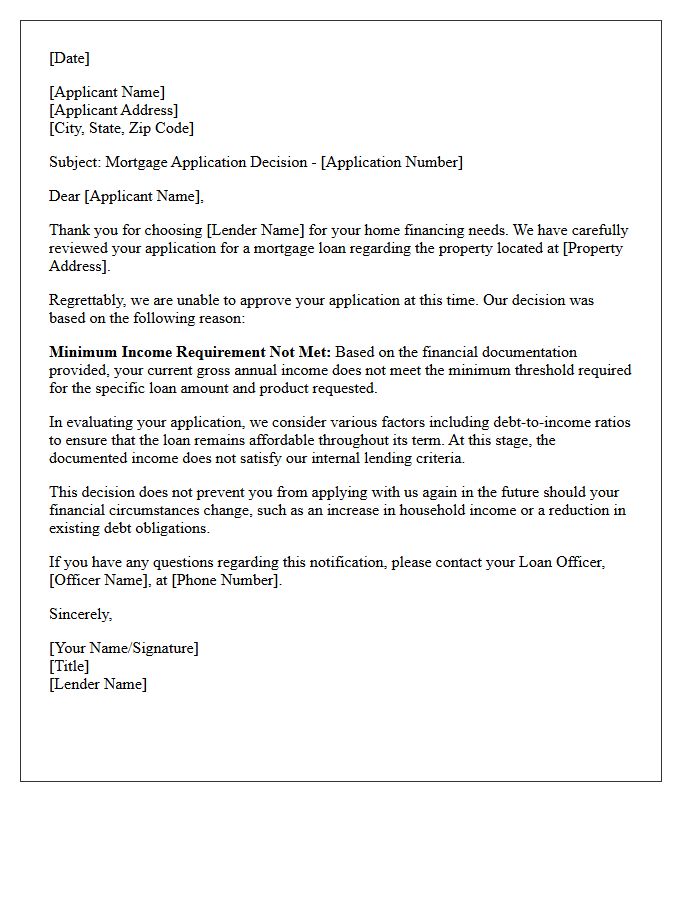

Minimum Income Requirement Unmet Mortgage Rejection Letter

Receiving a mortgage rejection letter due to an unmet minimum income requirement indicates your debt-to-income ratio is too high for the loan amount. Lenders use specific affordability benchmarks to ensure you can manage monthly repayments alongside existing debts. To improve your chances for future approval, consider increasing your down payment, paying down current liabilities, or adding a co-signer with stable earnings. Reviewing your application for overlooked income sources, like bonuses or rental dividends, can also help bridge the gap and satisfy strict lending criteria.

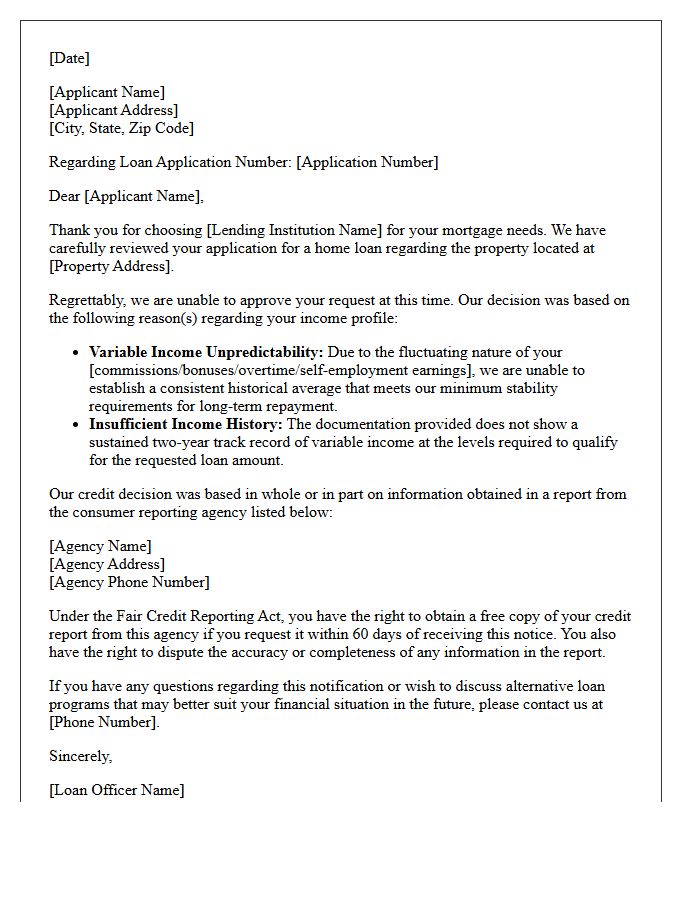

Variable Income Unpredictability Mortgage Denial Letter

Receiving a mortgage denial letter due to variable income unpredictability is common for freelancers or commission-based workers. Lenders require stable earnings to ensure future repayment capability. If your income fluctuates significantly, underwriters may exclude certain amounts, leading to a high debt-to-income ratio. To overcome this, provide two years of tax returns and 1099 forms to prove a consistent upward trend. Demonstrating financial stability through significant cash reserves or a larger down payment can often help mitigate the perceived risk of irregular pay cycles.

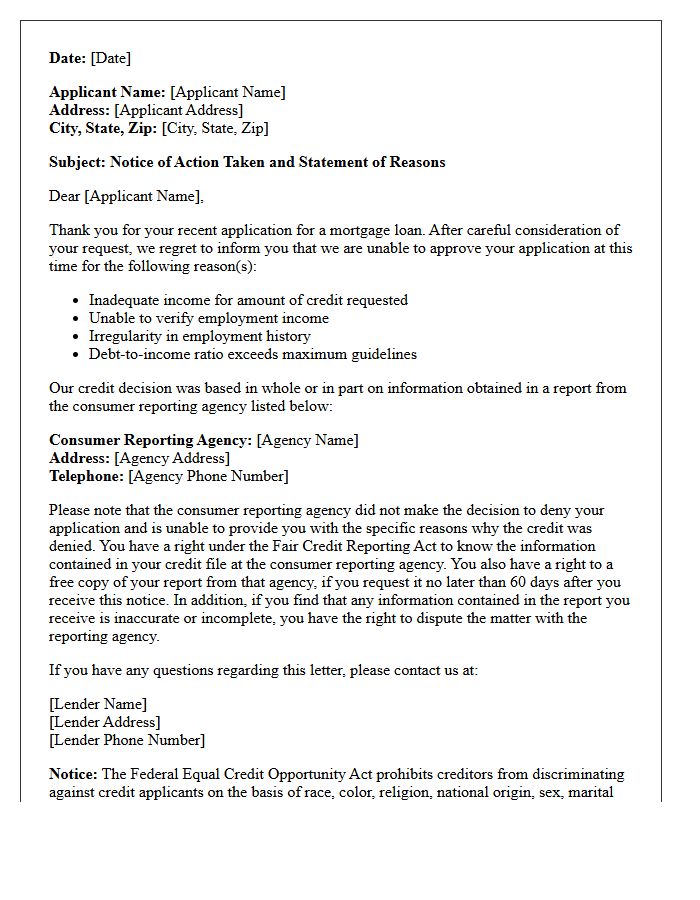

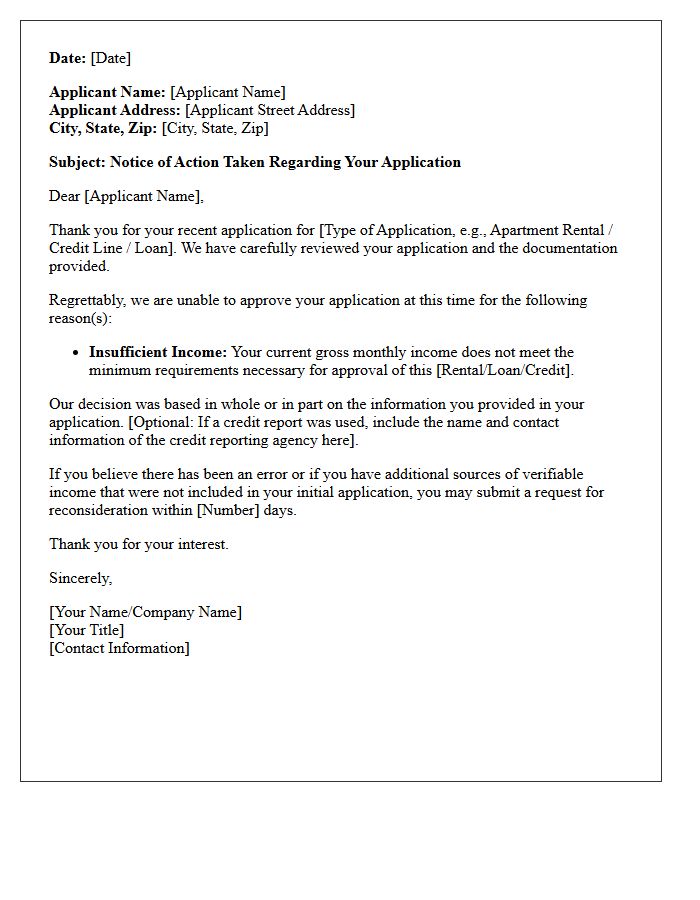

Notice of Action Taken Insufficient Income Letter

A Notice of Action Taken for insufficient income is a formal document issued by lenders when a loan or credit application is denied. This letter must comply with the Equal Credit Opportunity Act (ECOA) by providing a specific reason for the rejection. It indicates that your current debt-to-income ratio or documented earnings do not meet the minimum financial requirements for the requested credit amount. Reviewing this notice is essential for understanding how to improve your creditworthiness before reapplying for future financing or credit products.

Why was my mortgage application denied for insufficient income?

A mortgage denial for insufficient income typically occurs when your Debt-to-Income (DTI) ratio is too high, meaning your monthly gross income is not enough to cover the projected mortgage payments along with your existing debt obligations.

What does a Mortgage Application Insufficient Income Denial Letter include?

The letter, also known as an Adverse Action Notice, must legally state the specific reasons for the denial, the name of the credit reporting agency used, and your rights to request a free copy of your credit report within 60 days.

How can I improve my chances of approval after an income-based denial?

To address an income-based denial, you can apply for a smaller loan amount, pay off existing high-interest debts to lower your DTI ratio, or add a co-signer with a stable income to the application.

Can I use non-traditional income to appeal a mortgage denial?

Yes, if you have consistent secondary income such as bonuses, commissions, rental income, or child support that was not factored into the initial application, you can provide documentation to the lender for a reconsideration of your total qualifying income.

How long should I wait to reapply for a mortgage after being denied for income?

There is no mandatory waiting period; however, it is best to reapply only after you have significantly reduced your monthly debt, increased your household income, or saved a larger down payment to reduce the total loan-to-value ratio.

Comments