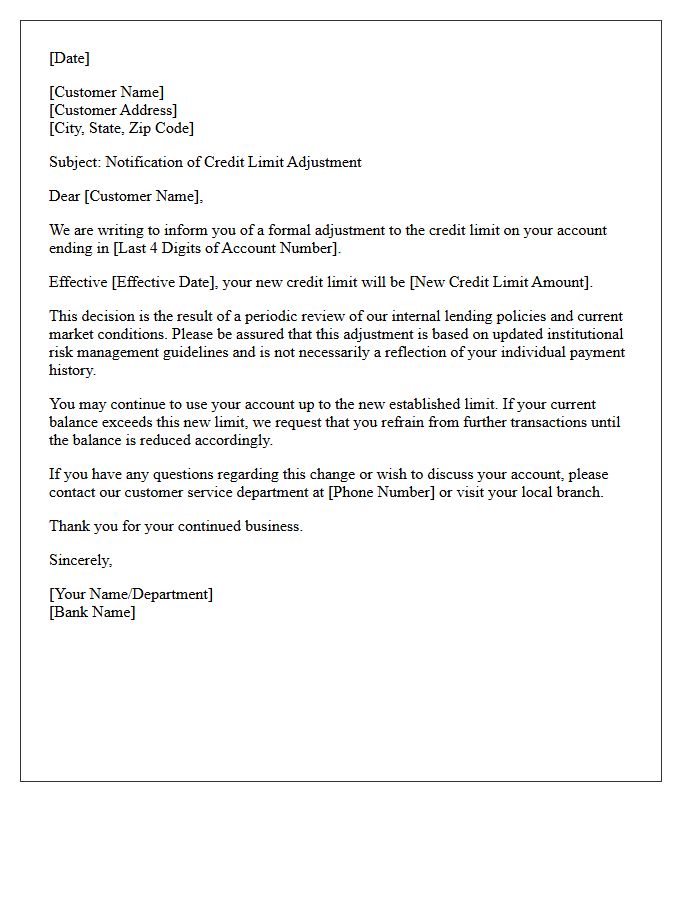

A Notification of Credit Limit Decrease informs customers when their borrowing capacity is reduced due to economic shifts or risk assessments. This guide explains why limits change, legal requirements for lenders, and how to manage the impact on your credit score. To simplify your communication process, below are some ready to use templates.

Image cover: Your Guide to Notifying Customers of Credit Limit Reductions: Samples and Templates

Letter Samples List

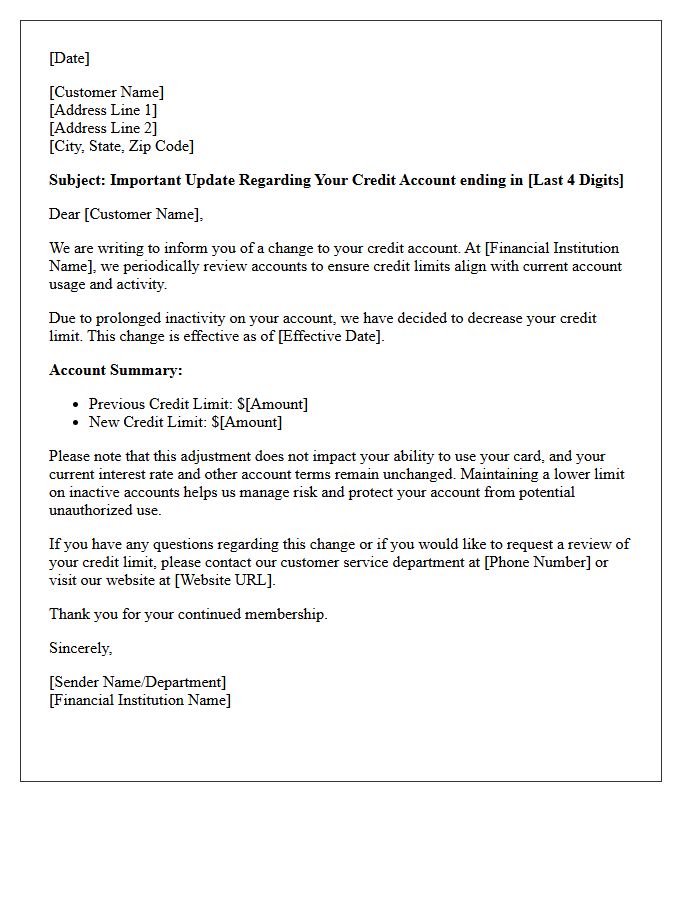

- Letter of Notification for Credit Limit Decrease Due to Account Inactivity

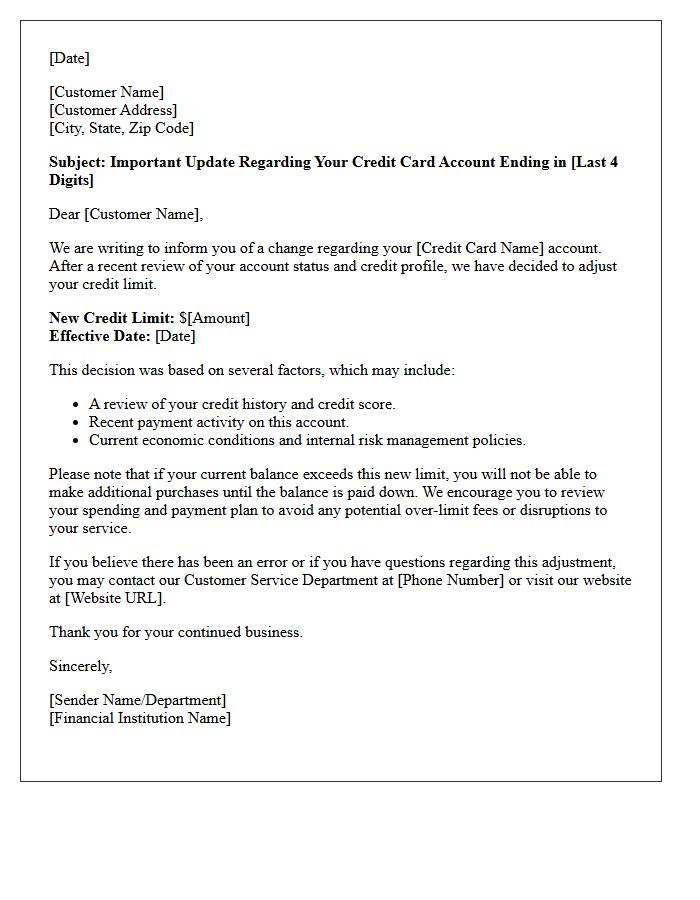

- Official Letter Regarding the Decrease of Your Credit Card Limit

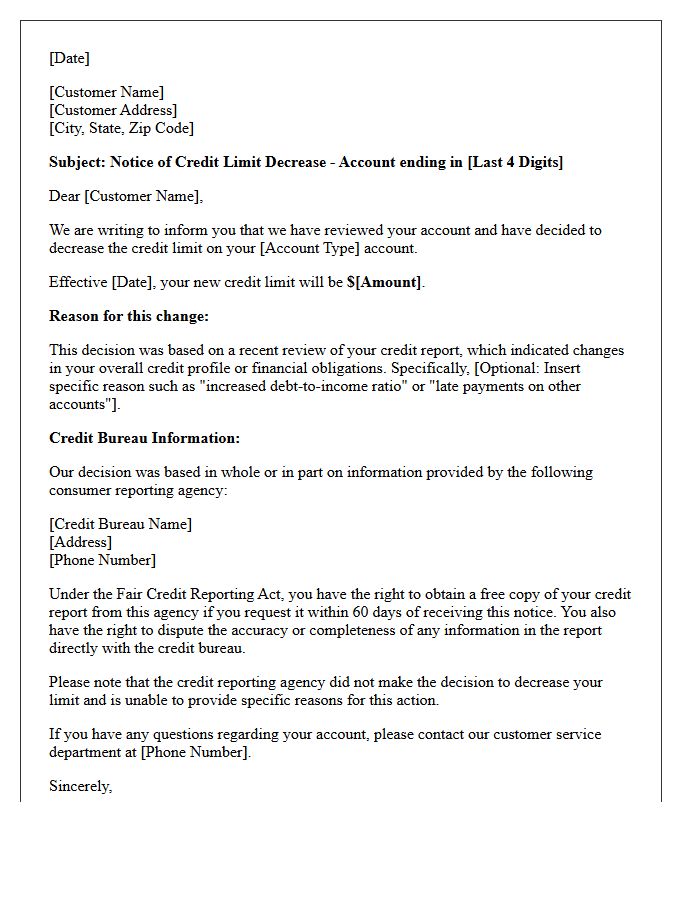

- Letter of Credit Limit Decrease Based on Recent Credit Report Changes

- Important Letter Concerning the Reduction of Your Business Credit Limit

- Letter Outlining the Decrease in Your Revolving Credit Line Limit

- Notification Letter for Credit Limit Decrease Due to Missed Payments

- Formal Letter of Decrease in Approved Overdraft Credit Limit

- Letter of Notification Regarding Corporate Account Credit Limit Decrease

- Standard Letter for Credit Limit Decrease Following Annual Financial Review

- Letter Advising of Credit Limit Decrease Due to High Debt-to-Income Ratio

- Customer Notification Letter for Proactive Credit Limit Decrease

- Letter of Credit Limit Decrease Based on Updated Bank Lending Policies

Letter of Notification for Credit Limit Decrease Due to Account Inactivity

A Letter of Notification for Credit Limit Decrease is a formal notice sent by lenders when they reduce your borrowing capacity. This action often occurs because of account inactivity, as banks minimize their financial exposure on dormant lines. While a lower limit helps prevent fraud, it may negatively impact your credit utilization ratio and lower your overall credit score. To prevent this, ensure you make small, periodic purchases to keep the account active. If you receive this notice, contact the issuer immediately to request a reinstatement of your original limit.

Official Letter Regarding the Decrease of Your Credit Card Limit

An official letter regarding a credit card limit decrease is a formal notice from your bank detailing a reduction in your available purchasing power. This action often results from changes in your credit score, payment history, or internal banking policies. It is crucial to review the stated reason to understand how it affects your debt-to-credit ratio, which can impact your overall credit rating. If you disagree with the adjustment, you should contact the issuer immediately to discuss your financial standing or request a manual account review.

Letter of Credit Limit Decrease Based on Recent Credit Report Changes

A Letter of Credit limit decrease often occurs when an issuing bank identifies negative shifts in a borrower's financial stability. Following a recent credit report change-such as late payments, high debt utilization, or a lower credit score-banks may reduce available limits to mitigate potential default risk. This proactive adjustment protects the lender's exposure but can impact a business's liquidity and international purchasing power. Monitoring credit health is essential to maintaining favorable trade finance terms and preventing sudden reductions in revolving credit capacity.

Important Letter Concerning the Reduction of Your Business Credit Limit

Receiving an Important Letter Concerning the Reduction of Your Business Credit Limit requires immediate attention to protect your cash flow. Banks typically lower limits due to economic shifts, decreased credit scores, or account inactivity. Carefully review the notice to identify the specific reason for the change and the effective date. To mitigate the impact, contact your lender to negotiate a reinstatement or explore alternative financing options. Maintaining a strong credit profile is essential to ensure your business retains the necessary liquidity for daily operations and long-term growth.

Letter Outlining the Decrease in Your Revolving Credit Line Limit

A letter outlining a credit limit decrease informs you that a lender has reduced your available borrowing capacity. This action often results from changes in your credit score, missed payments, or prolonged inactivity. It is crucial to review the notice immediately because a lower limit can increase your credit utilization ratio, potentially harming your overall rating. If the reduction seems incorrect, contact the issuer to discuss restoration options or provide updated financial documentation to prove your creditworthiness and maintain your purchasing power.

Notification Letter for Credit Limit Decrease Due to Missed Payments

A notification letter regarding a credit limit decrease serves as a formal warning that your available borrowing capacity has been reduced. Lenders typically issue these notices when missed payments or frequent delinquencies signal increased financial risk. Under the Fair Credit Reporting Act, creditors must disclose the specific reasons for this adverse action. This reduction can negatively impact your credit utilization ratio, potentially lowering your overall credit score. To restore your previous limit, focus on consistent on-time payments and maintaining a lower balance to demonstrate improved creditworthiness over time.

Formal Letter of Decrease in Approved Overdraft Credit Limit

A formal letter notifying a decrease in approved overdraft credit limit is a critical communication from a financial institution. This document outlines the reduction in your available borrowing capacity, often triggered by changes in risk assessment, credit scores, or account activity. It typically specifies the new limit, the effective date of the change, and the reasons for the adjustment. Reviewing this notice immediately is essential to avoid unauthorized overlimit fees and to ensure your cash flow management remains stable under the new contractual terms.

Letter of Notification Regarding Corporate Account Credit Limit Decrease

A Letter of Notification Regarding Corporate Account Credit Limit Decrease is a formal communication from a financial institution informing a business of a reduction in its available borrowing capacity. This reduction often stems from changes in the company's creditworthiness, updated risk assessments, or shifts in the lender's internal policies. Upon receipt, it is vital to review your cash flow management and existing payment obligations to ensure operational stability. Proactively contacting your account manager to discuss the underlying reasons can help in negotiating a potential restoration of your previous limits.

Standard Letter for Credit Limit Decrease Following Annual Financial Review

A Standard Letter for Credit Limit Decrease is a formal notification sent by lenders after an annual financial review. This document informs the borrower that their borrowing capacity has been reduced based on updated risk assessment metrics. Key triggers include changes in debt-to-income ratios, credit scores, or overall business liquidity. Understanding this adverse action notice is crucial, as it impacts your credit utilization ratio and total available capital. Always review the specific reasons cited to address financial weaknesses and request a limit reinstatement in the future.

Letter Advising of Credit Limit Decrease Due to High Debt-to-Income Ratio

Receiving a letter advising of a credit limit decrease indicates that the lender perceives increased financial risk. The primary reason cited is often a high debt-to-income (DTI) ratio, suggesting your current monthly obligations are too large relative to your gross earnings. This reduction protects the creditor from potential default but can negatively impact your credit utilization rate and overall credit score. To address this, focus on paying down existing balances or increasing documented income to improve your financial profile and request a future limit restoration.

Customer Notification Letter for Proactive Credit Limit Decrease

A customer notification letter for a proactive credit limit decrease is a formal communication informing borrowers of a reduction in their available credit line. Lenders often issue these updates based on risk assessment, changing market conditions, or account inactivity. It is essential to clearly explain the reasoning, the new limit, and the effective date to ensure transparency. Providing contact information for appeals helps maintain trust while managing financial exposure. Timely delivery of this notice is crucial for regulatory compliance and helps customers adjust their financial planning accordingly.

Letter of Credit Limit Decrease Based on Updated Bank Lending Policies

A Letter of Credit limit decrease typically occurs when updated bank lending policies reflect higher risk sensitivity or regulatory capital requirements. Financial institutions periodically review borrower creditworthiness and market conditions to adjust exposure. If a bank's internal risk appetite shifts, they may reduce your available credit facility to mitigate potential losses. It is essential for businesses to monitor these policy changes closely, as a lower limit can impact operational liquidity and international trade capabilities. Maintaining strong financial transparency and proactive communication with your lender can help navigate these restrictive policy updates.

Why was my credit limit decreased?

Credit limits are typically reduced due to changes in credit scores, a history of late payments, prolonged account inactivity, or shifts in the lender's internal risk assessment policies.

Will a credit limit decrease affect my credit score?

A lower credit limit can increase your credit utilization ratio-the amount of credit you use versus your total limit-which may negatively impact your credit score if your balances remain high.

Can I appeal the decision to lower my credit limit?

Yes, you can contact the issuer's customer service department to request a reconsideration. Providing updated income information or proof of improved financial stability may help your case.

Was I supposed to receive a notification before the limit was lowered?

Under the Credit CARD Act, lenders are generally required to provide a written notice if the limit is decreased due to an adverse action, though the reduction can often take effect immediately.

How can I restore my original credit limit?

To qualify for a limit increase in the future, maintain a consistent history of on-time payments, reduce your current debt-to-income ratio, and ensure your credit report shows positive financial behavior.

Comments