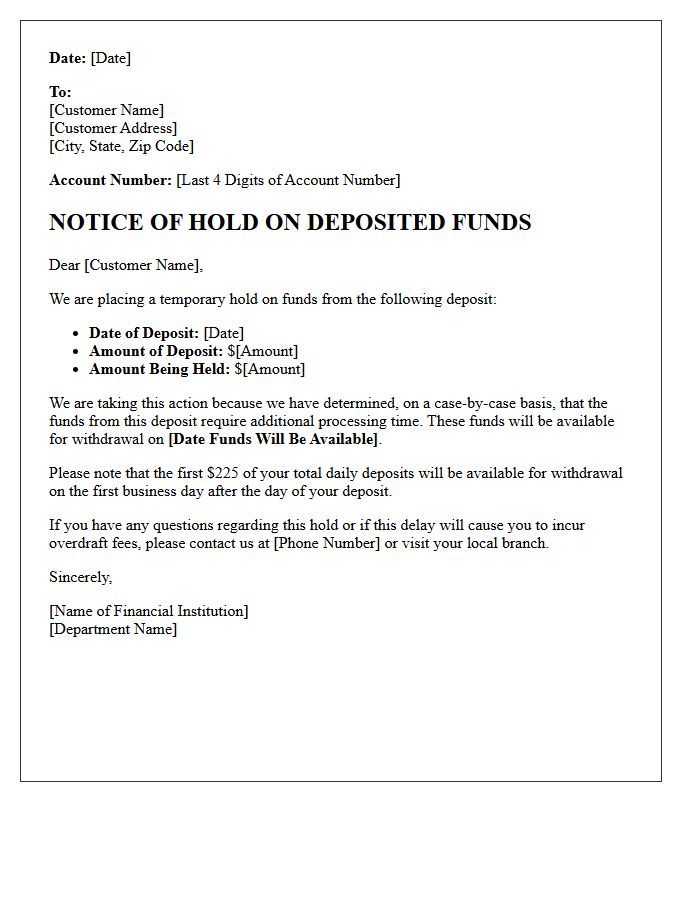

Banks often issue a Notification of Hold on Deposited Funds to delay access to large or suspicious deposits under Regulation CC. This process ensures check clearance while protecting financial institutions from potential fraud. Understanding these hold periods helps you manage your cash flow effectively and avoid overdraft fees. To help you communicate with clients, below are some ready to use template.

Image cover: Notice of Funds Availability: Templates and Hold Notification Samples

Letter Samples List

- Standard Deposited Funds Hold Notification Letter

- Large Deposit Exception Hold Notice Letter

- New Account Deposited Funds Hold Letter

- Repeated Overdrafts Account Hold Letter

- Redeposited Check Exception Hold Letter

- Reasonable Cause Collectibility Hold Letter

- Emergency Conditions Funds Hold Letter

- Extended Deposit Hold Notification Letter

- Uncollected Funds Administrative Hold Letter

- Suspected Fraud Deposit Freeze Letter

- Foreign Check Deposit Delay Notification Letter

- Case-By-Case Deposit Hold Notice Letter

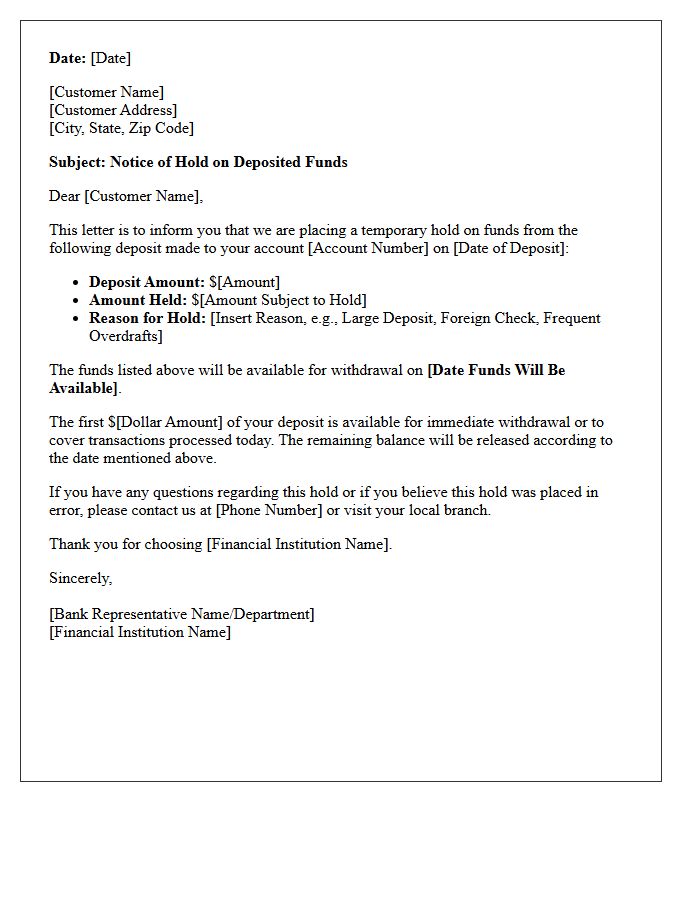

Standard Deposited Funds Hold Notification Letter

A Standard Deposited Funds Hold Notification Letter is a formal notice issued by a bank to inform customers that their recent deposit is being temporarily withheld. Governed by Regulation CC, this document specifies the exact date funds will become available for withdrawal. It must clearly state the reason for the delayed availability, such as a large deposit amount or frequent overdrafts. Receiving this letter ensures transparency, allowing account holders to manage their finances effectively while the financial institution verifies the transaction's validity to prevent potential fraud.

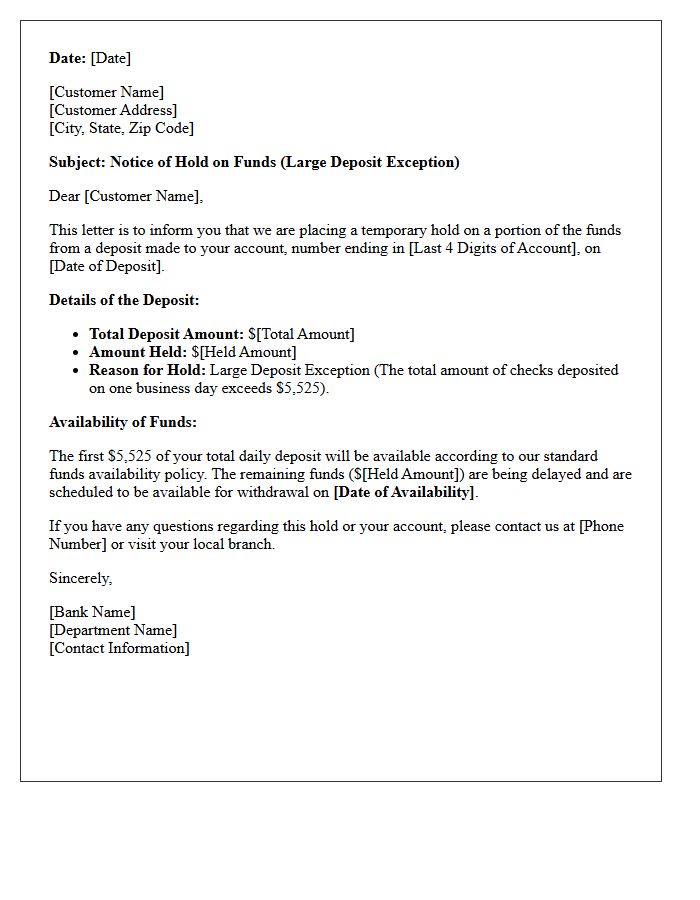

Large Deposit Exception Hold Notice Letter

A Large Deposit Exception Hold Notice Letter is a formal document issued by banks when a deposit exceeds $5,525. Under Regulation CC, financial institutions can delay fund availability beyond standard timeframes to mitigate risk. This notice must clearly state the extended hold period and the specific date funds will be accessible. Providing this written disclosure protects the bank's legal compliance while informing customers of potential delays in their available balance. Understanding these letters is essential for managing cash flow and avoiding overdraft fees during extended verification periods.

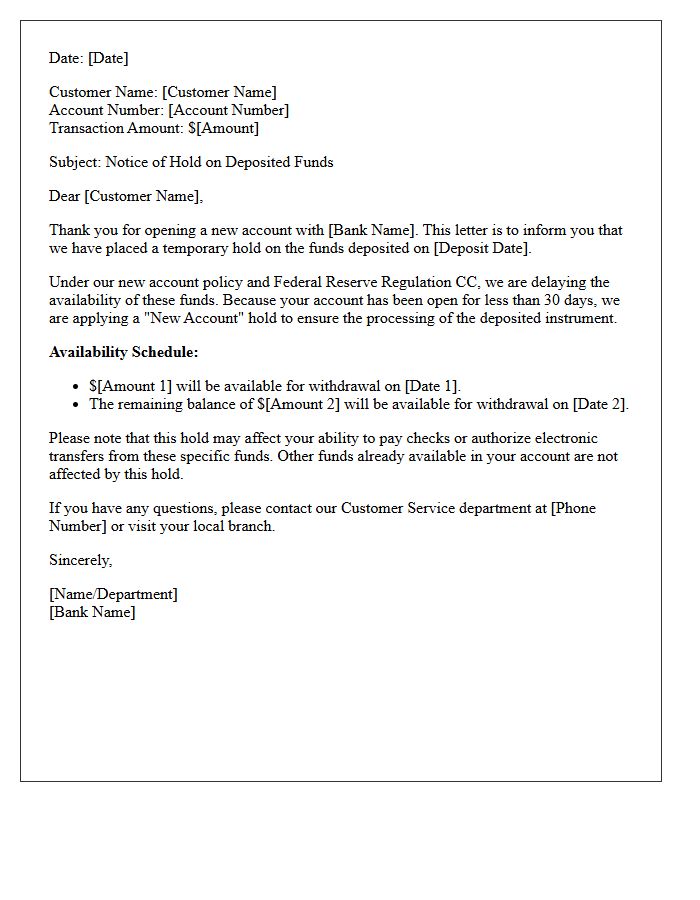

New Account Deposited Funds Hold Letter

A New Account Deposited Funds Hold Letter is a mandatory notice informing customers that their initial deposit is temporarily restricted. Under Regulation CC, financial institutions may delay access to funds to verify legitimacy and mitigate fraud risks. This document specifies the exact date when your money becomes available for withdrawal. Always review the letter for the hold duration and the specific reason for the delay, such as account age or large check amounts, to manage your cash flow effectively during the onboarding process.

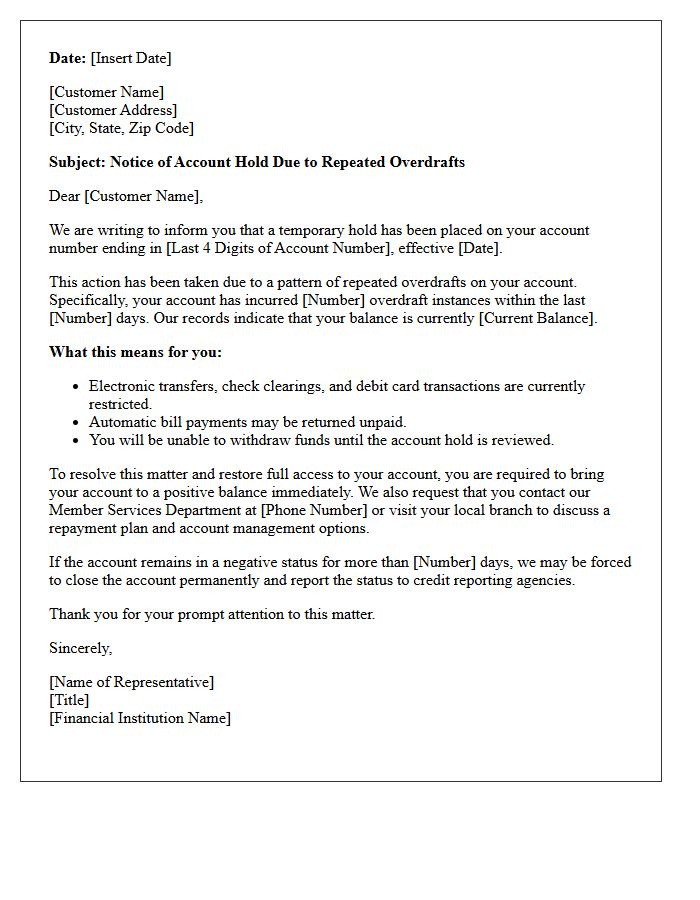

Repeated Overdrafts Account Hold Letter

Receiving a Repeated Overdrafts Account Hold Letter indicates that your financial institution has restricted access to your funds due to frequent negative balances. This formal notice serves as a warning that excessive transaction failures violate banking terms. To resolve the hold, you must immediately deposit funds to cover the deficit and demonstrate stable financial activity. Failure to address these consecutive overdrafts can lead to permanent account closure and negative reporting to credit agencies, severely impacting your future banking eligibility and financial reputation.

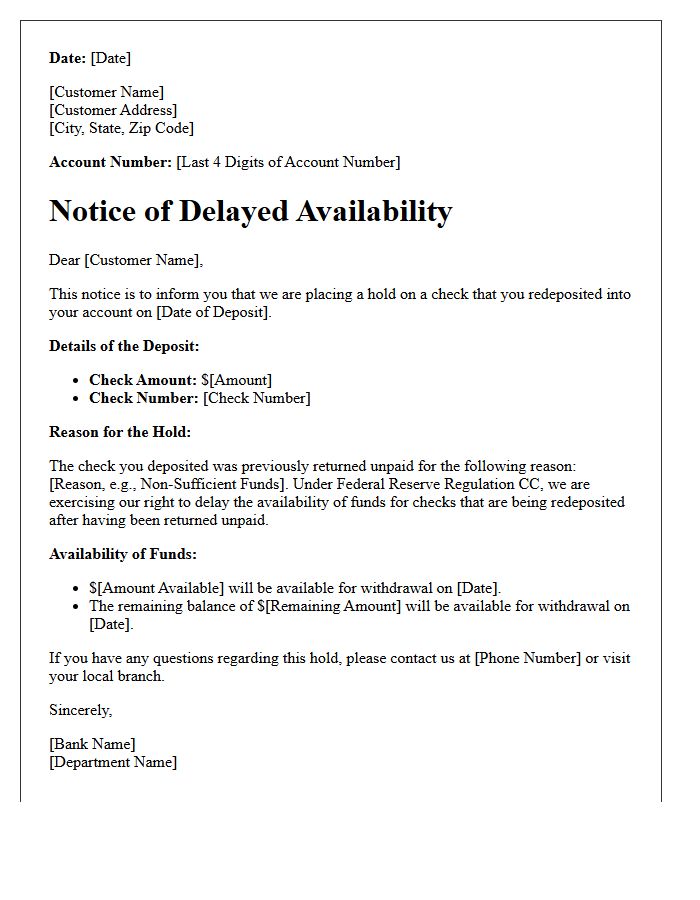

Redeposited Check Exception Hold Letter

A Redeposited Check Exception Hold Letter notifies customers that a bank is delaying funds availability because a previously returned check is being presented again. Under Regulation CC, financial institutions use this exception to mitigate risk, as redeposited items have a higher likelihood of being dishonored by the paying bank. The notice must specify the hold period and when funds will be accessible. Unlike standard deposits, these holds often extend beyond the typical two-day timeframe, protecting the bank from potential losses related to unpaid instruments and insufficient funds.

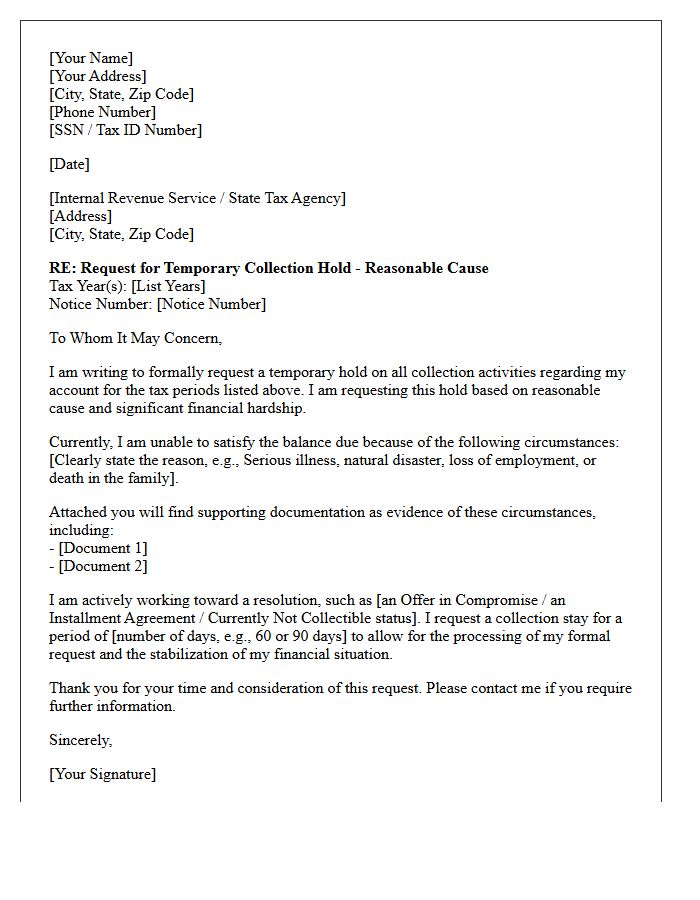

Reasonable Cause Collectibility Hold Letter

A Reasonable Cause Collectibility Hold Letter is a formal request sent to tax authorities to temporarily pause enforcement actions. It is used when a taxpayer faces financial hardship or specific extenuating circumstances that prevent immediate payment. By providing documented proof of "reasonable cause," such as serious illness or natural disasters, you can prevent levies or liens while your case is reviewed. This collection stay offers critical time to arrange a sustainable payment plan or settlement, ensuring your basic living expenses are protected during the resolution process.

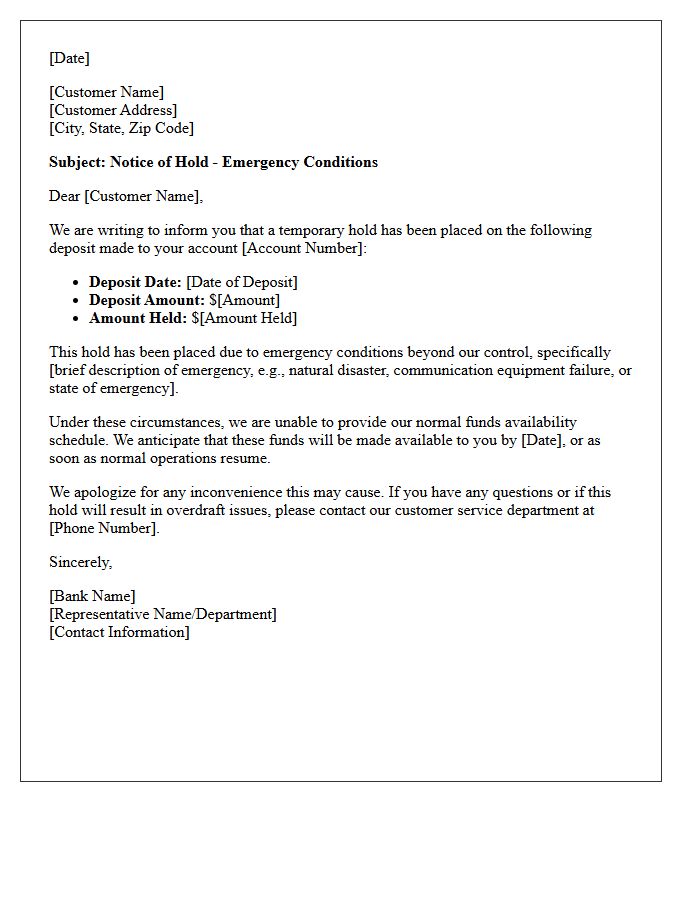

Emergency Conditions Funds Hold Letter

An Emergency Conditions Funds Hold Letter is a formal notice from a financial institution informing you of a delay in check availability. Under Regulation CC, banks can extend standard holding periods during emergency conditions, such as natural disasters, communication equipment failures, or state of emergency declarations. This document must specify the reason for the delay and the date your funds will be accessible. Understanding this letter helps you manage liquidity and anticipate extended processing times beyond typical banking schedules during unpredictable, large-scale disruptions.

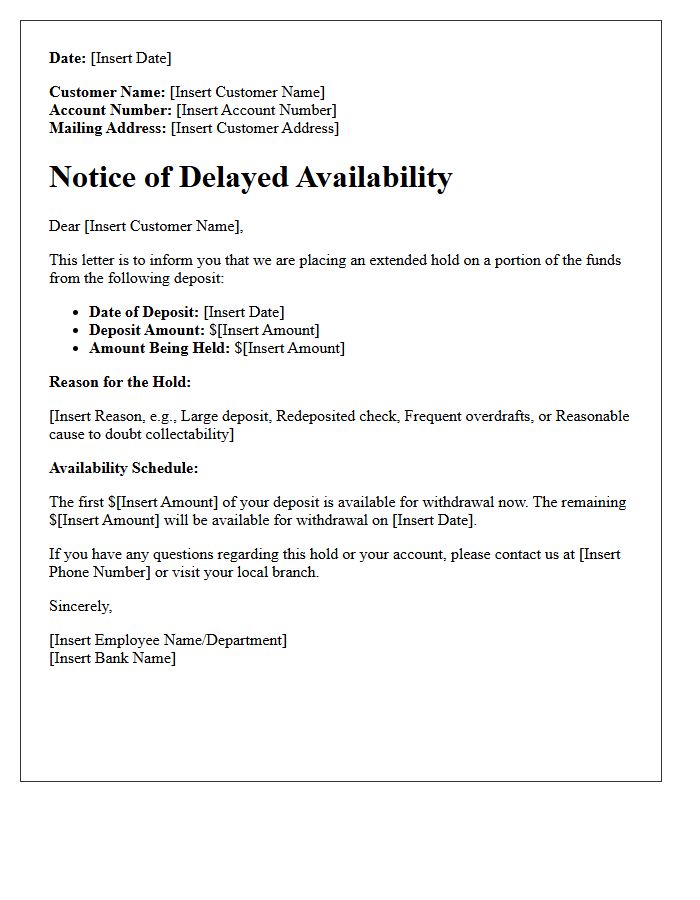

Extended Deposit Hold Notification Letter

An Extended Deposit Hold Notification Letter is a formal notice sent by banks when they delay access to deposited funds beyond standard timeframes. Under Regulation CC, institutions must provide this written disclosure explaining the specific reason for the exception, such as large deposits, frequent overdrafts, or doubtful collectability. The letter must state the date the deposit was made and exactly when the funds will become available for withdrawal. Reviewing these notifications helps account holders manage cash flow and avoid potential returned item fees during the extended holding period.

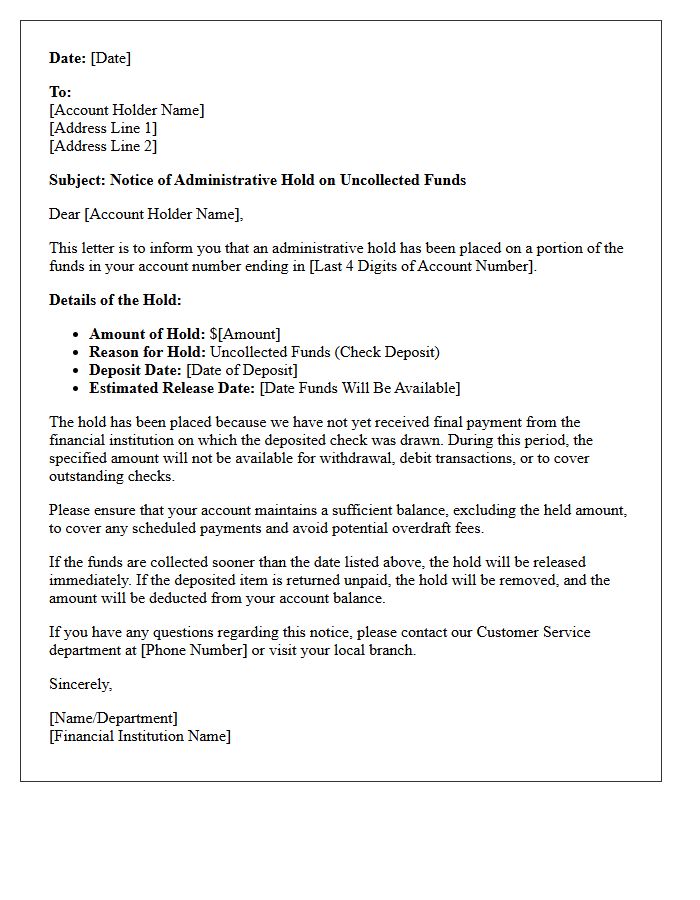

Uncollected Funds Administrative Hold Letter

An Uncollected Funds Administrative Hold Letter notifies account holders that deposited checks are under a temporary restrictive hold. This occurs because the bank has not yet received guaranteed payment from the issuing institution. To ensure account security and prevent overdrafts, these funds remain unavailable for withdrawal until the collection process completes. Understanding this notice is crucial for managing cash flow and avoiding returned payments. Always verify the specific release date mentioned in the letter before attempting to use the pending balance to cover outstanding financial obligations.

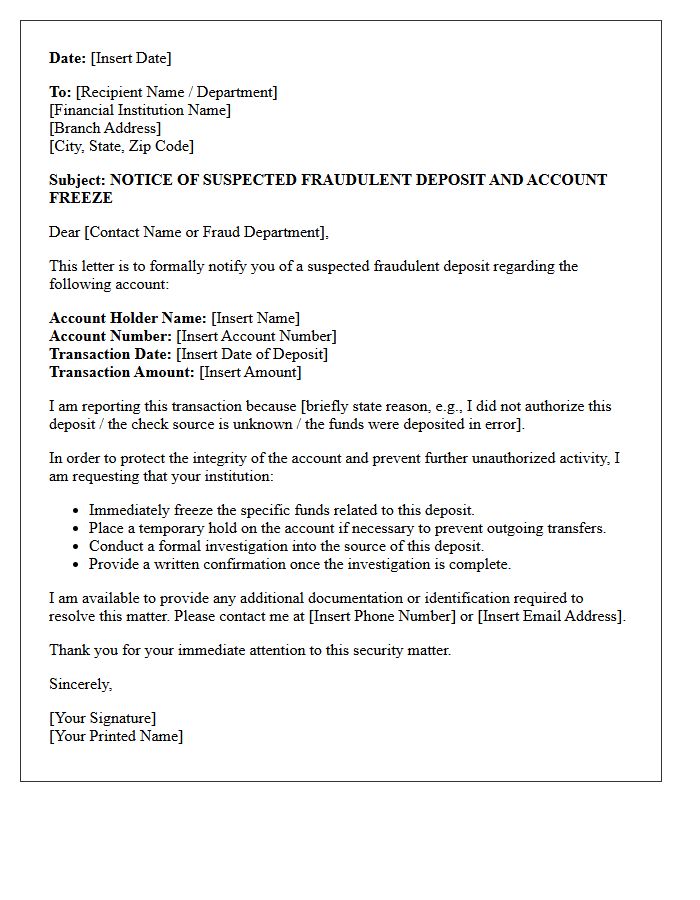

Suspected Fraud Deposit Freeze Letter

Receiving a Suspected Fraud Deposit Freeze Letter means your financial institution has detected unusual activity and temporarily restricted access to your funds. This administrative hold is a protective measure under banking regulations to investigate potential scams or unauthorized transactions. You must immediately contact the bank's fraud department using a verified number to confirm your identity and explain the deposit's origin. Timely cooperation is essential to resolve the investigation and restore account access, as failure to respond may lead to permanent closure or legal reporting.

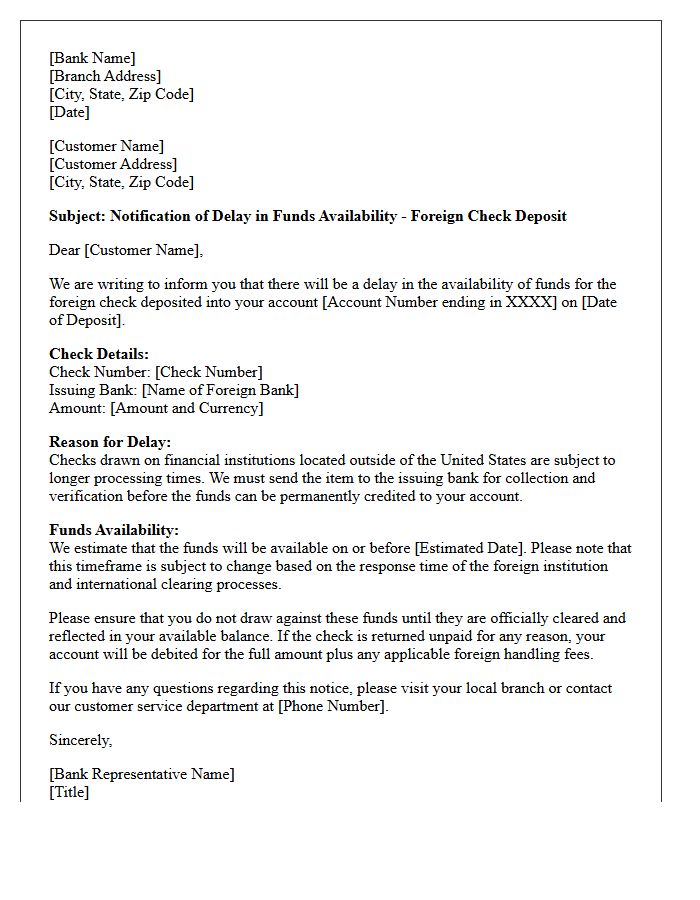

Foreign Check Deposit Delay Notification Letter

A Foreign Check Deposit Delay Notification Letter is a formal notice from your bank explaining that funds from an international check are being held. This delay occurs because international clearing processes take longer than domestic ones to verify authenticity and available funds. The most important thing to know is the extended hold period, which can last several weeks. Banks issue these letters to comply with banking regulations and mitigate the risk of fraudulent transactions or returned items. Always wait for final clearance before spending the funds to avoid potential overdraft fees.

Case-By-Case Deposit Hold Notice Letter

A Case-By-Case Deposit Hold Notice Letter is a critical document used by banks to inform customers of a delayed fund availability. Under Federal Reserve Regulation CC, institutions must provide this notice when they choose to extend the standard holding period for a specific check. The letter serves as a legal disclosure, specifying the exact date funds will be accessible and the reason for the exception. Receiving this notice helps account holders manage their cash flow and avoid potential overdraft fees caused by uncleared deposits during the additional processing time.

What is a notification of hold on deposited funds?

A notification of hold on deposited funds is a formal notice from a financial institution informing an account holder that recently deposited checks or items are not yet available for withdrawal. This delay ensures the bank can verify the validity of the funds before they are released to the account balance.

Why did the bank place a hold on my recent deposit?

Banks typically place holds on deposits to manage risk. Common reasons include depositing a large dollar amount, frequent overdrafts in the account, a history of returned checks, or information from the paying bank suggesting the check may not be honored.

How long will the hold on my deposited funds last?

Under Federal Reserve Regulation CC, most local checks are held for two business days, while longer holds-often up to seven business days-may apply to large deposits (over $5,525), new accounts, or checks from out-of-state or international institutions.

Can I access any portion of my money while a hold is active?

Yes, in many cases, federal regulations require banks to make the first $225 of a check deposit available by the next business day. The remaining balance will be released once the hold period expires, provided the check is successfully processed.

What should I do if I receive a hold notice?

If you receive a hold notice, review the "funds available" date listed to understand when you can access your money. To avoid potential overdraft fees, ensure you do not write checks or schedule electronic payments against those specific funds until the hold has been officially lifted.

Comments