Managing account balances is crucial to avoid costly penalties. This guide explains the implications of a Non-Sufficient Funds (NSF) check return and how to handle an overdraft notice effectively. Learn how to communicate with your bank and resolve payment failures to maintain a healthy credit standing. To help you professionalize your correspondence, below are some ready to use template.

Image cover: Professional Templates for NSF Return and Overdraft Notifications

Letter Samples List

- First Offense Non-Sufficient Funds Letter

- Standard Check Return and Penalty Letter

- Checking Account Overdraft Notice Letter

- Continuous Negative Balance Warning Letter

- Unpaid Item and Fee Assessment Letter

- Overdraft Protection Transfer Confirmation Letter

- Returned Deposited Item Notification Letter

- Commercial Account Non-Sufficient Funds Letter

- Final Demand for Overdraft Repayment Letter

- Bounced Check Account Restriction Letter

- Overdraft Line of Credit Draw Letter

- Account Closure Due to Insufficient Funds Letter

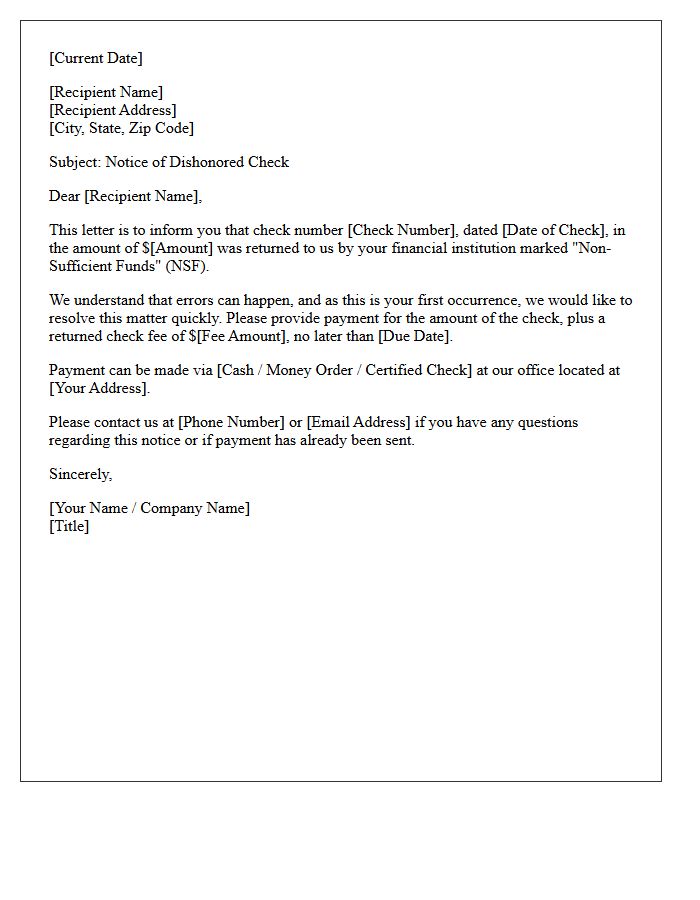

First Offense Non-Sufficient Funds Letter

A First Offense Non-Sufficient Funds Letter serves as a formal notification to a customer regarding a failed payment due to inadequate account balance. It outlines the specific transaction details, including the date and amount owed. The primary goal is to request a prompt replacement payment while often offering a one-time courtesy waiver of penalties or late fees. This professional correspondence helps maintain positive business relationships while ensuring debt recovery and providing clear instructions for resolving the financial discrepancy immediately to avoid further collection actions or account restrictions.

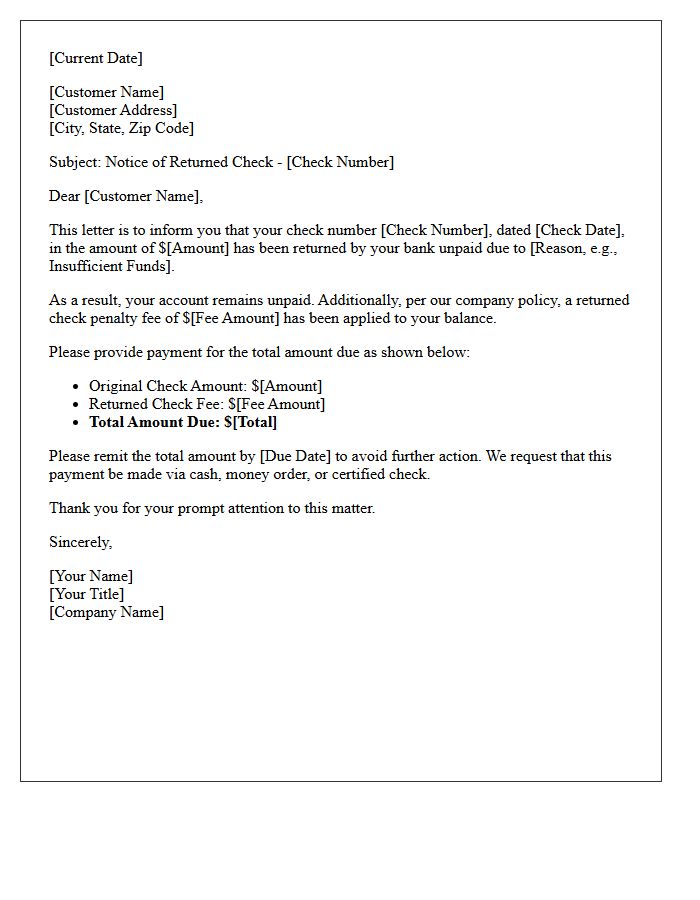

Standard Check Return and Penalty Letter

A Standard Check Return and Penalty Letter notifies a customer that their payment was declined due to insufficient funds or account issues. This formal notice confirms the payment failure and outlines the mandatory returned check fee applied to the balance. To avoid further legal action or credit damage, the recipient must provide an alternative payment method immediately. Timely resolution is essential to prevent additional late penalties and maintain a positive financial standing with the billing institution.

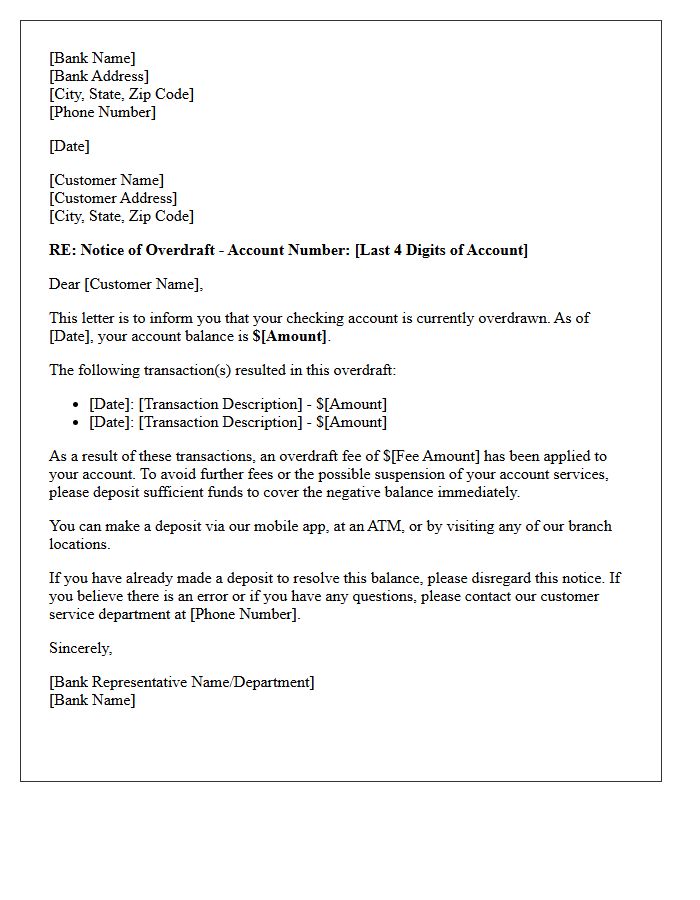

Checking Account Overdraft Notice Letter

A Checking Account Overdraft Notice Letter informs you that your balance has fallen below zero. This formal communication details specific overdraft fees, the negative balance amount, and the required deadline to deposit funds. It is essential to address this notice immediately to avoid account closure or negative reports to credit bureaus. Reviewing the letter helps identify potential unauthorized transactions or banking errors. To prevent future occurrences, consider linking a savings account for protection or opting out of overdraft coverage services provided by your financial institution.

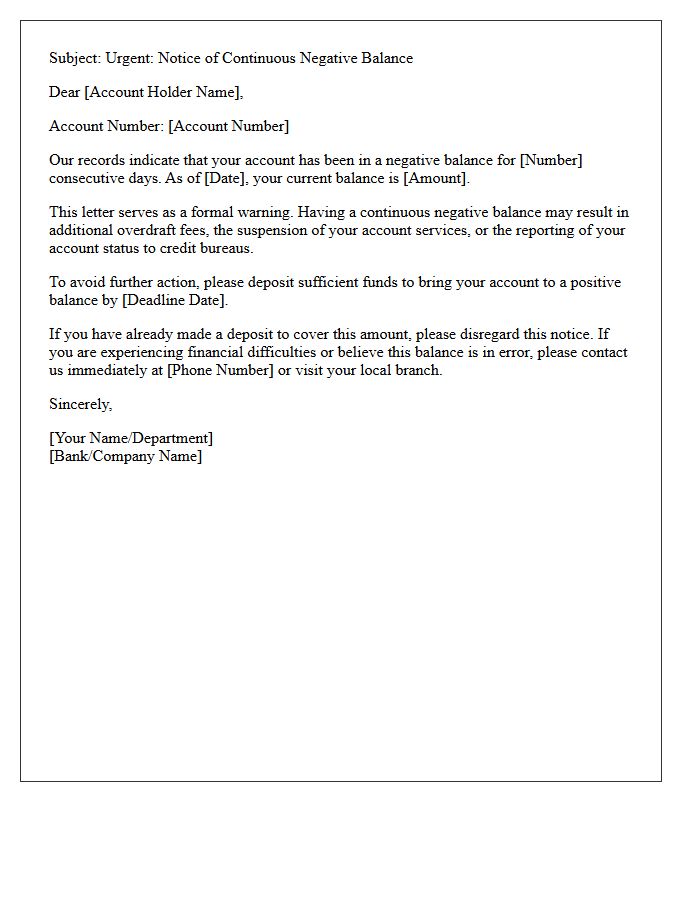

Continuous Negative Balance Warning Letter

A Continuous Negative Balance Warning Letter is a formal notification from a financial institution indicating your account has remained overdrawn for an extended period. It is crucial to address this immediately to avoid permanent account closure and negative reports to credit bureaus. This letter serves as a final opportunity to deposit funds and restore a positive balance. Failure to comply can result in debt collection actions and restricted access to future banking services. Always review the specified deadline to prevent additional overdraft fees or legal consequences associated with prolonged unsettled balances.

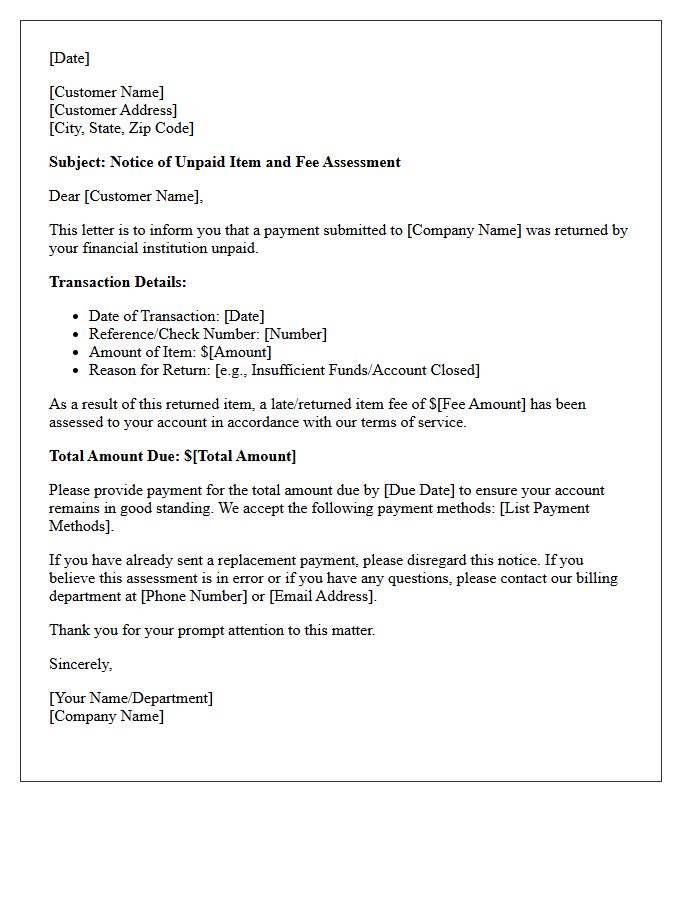

Unpaid Item and Fee Assessment Letter

An Unpaid Item and Fee Assessment Letter is a formal notice issued when a payment fails due to insufficient funds or account issues. It details the specific transaction that was returned and outlines the resulting penalties or administrative charges applied to your balance. To avoid further debt or service interruption, you must settle the outstanding amount and fees promptly. Monitoring your account balance ensures you bypass these costly restitution requirements and maintain a positive credit standing with the service provider or financial institution.

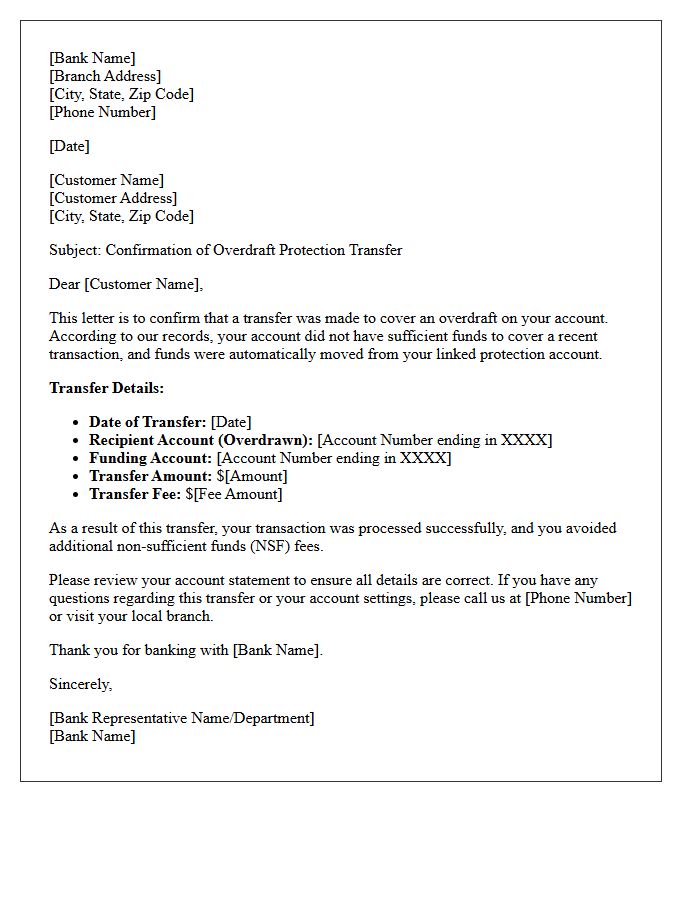

Overdraft Protection Transfer Confirmation Letter

An Overdraft Protection Transfer Confirmation Letter serves as official documentation that funds were moved from a linked account to prevent a transaction decline or penalty. This notification details the specific amount transferred, the source account used, and any applicable service fees. It is essential for accurate financial record-keeping and helps account holders monitor their balances to prevent future deficits. Always review these letters promptly to ensure all automated automated transfers were authorized and to maintain better control over your personal banking activity and overall credit health.

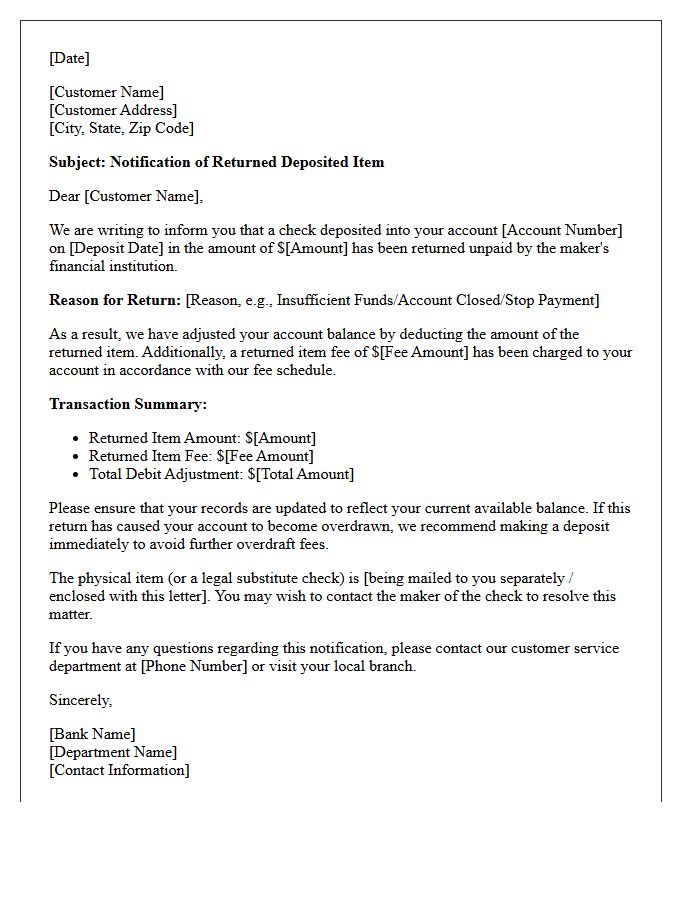

Returned Deposited Item Notification Letter

A Returned Deposited Item Notification Letter informs a payee that a check or electronic payment could not be processed. This typically occurs due to insufficient funds, a closed account, or stop-payment orders. When an item is returned, the bank reverses the initial credit to your balance and often assesses a service fee. It is crucial to contact the payor immediately to resolve the payment failure and recover the funds. Keep this formal record for your accounting files to track outstanding debts and associated banking penalties.

Commercial Account Non-Sufficient Funds Letter

A Commercial Account Non-Sufficient Funds Letter is a formal notification issued by a bank when a business transaction exceeds the available balance. This document serves as legal evidence of payment failure and often triggers immediate overdraft fees. It is crucial for businesses to rectify the deficit promptly to maintain a positive credit standing and avoid service interruptions. Professional communication regarding NSF notices helps preserve vendor relationships and ensures compliance with financial regulations, protecting the company from potential legal action or long-term reputational damage in commercial trade.

Final Demand for Overdraft Repayment Letter

A Final Demand for Overdraft Repayment Letter is a formal notice issued by a bank when a customer fails to clear a deficit. This document serves as a legal prerequisite before the institution initiates debt collection or legal proceedings. It typically specifies the total outstanding balance, a strict repayment deadline, and the consequences of non-compliance, such as credit score damage. If you receive this letter, immediate communication with the bank is essential to negotiate a payment plan and avoid further financial penalties or formal litigation.

Bounced Check Account Restriction Letter

A Bounced Check Account Restriction Letter is a formal notice from a financial institution informing a customer that their checking privileges have been limited. This occurs due to repeated non-sufficient funds (NSF) activity. The letter outlines specific penalties, such as the inability to write checks or the closure of the account. It often cites regulations from credit reporting agencies like ChexSystems, which can negatively impact your ability to open new bank accounts. To resolve this, you must immediately deposit funds to cover outstanding balances and prevent further legal or financial consequences.

Overdraft Line of Credit Draw Letter

An Overdraft Line of Credit Draw Letter is a formal request sent to a financial institution to activate a borrowing facility. This document ensures liquidity by covering temporary cash flow shortages or preventing bounced checks. It specifies the precise amount to be transferred from the credit line into a linked checking account. Business owners must maintain accurate records of these draws to track interest expenses and repayment schedules. Timely submission is crucial to maintain operational stability and avoid penalty fees associated with insufficient funds during critical payment cycles.

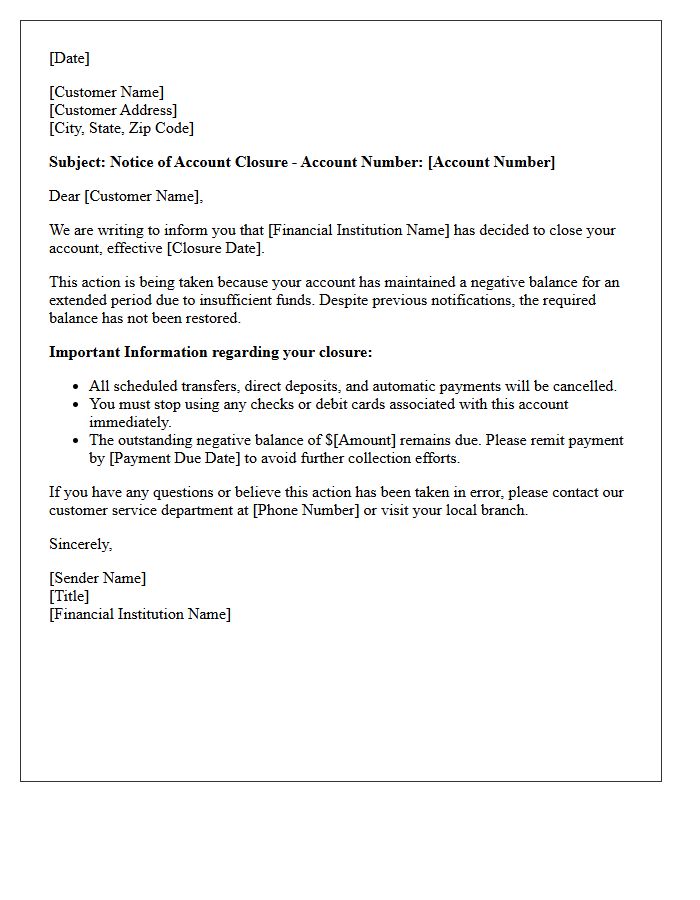

Account Closure Due to Insufficient Funds Letter

An Account Closure Due to Insufficient Funds Letter is a formal notification from a financial institution informing a customer that their bank account has been terminated. This action typically follows repeated instances of overdrafts or failed payments that remain unresolved. It is crucial to understand that such closures can negatively impact your ChexSystems report, making it difficult to open new accounts elsewhere. Upon receiving this notice, you should immediately settle any outstanding balances to prevent further legal action or debt collection efforts while seeking alternative banking solutions.

What is a Non-Sufficient Funds (NSF) check return?

A Non-Sufficient Funds (NSF) check return occurs when a bank refuses to honor a payment because the account holder does not have enough cleared funds to cover the transaction. The check is "bounced" back to the recipient's bank unpaid, and the account holder is typically charged a returned item fee.

What is the difference between an NSF fee and an overdraft fee?

An NSF fee is charged when the bank rejects a transaction and returns the check or ACH transfer unpaid due to a lack of funds. An overdraft fee is charged when the bank chooses to cover the transaction on your behalf, allowing the account balance to go negative while ensuring the payment is successfully processed.

What information is included in an Overdraft Notice?

An Overdraft Notice typically includes the date of the transaction, the specific amount that exceeded your balance, the current negative balance of the account, and the total amount of fees charged. It serves as a formal alert that you must deposit funds immediately to bring the account back to a positive standing.

How does a returned check affect my credit score?

A returned check does not directly appear on your credit report from major bureaus like Equifax or Experian. However, it is recorded in specialty databases like ChexSystems, which banks use to evaluate account applications. If the debt remains unpaid and is sent to a collection agency, it will then negatively impact your credit score.

How can I avoid NSF returns and overdraft charges?

You can avoid these fees by setting up low-balance mobile alerts, maintaining a financial buffer in your checking account, and linking a savings account for automatic overdraft protection transfers. Additionally, opting out of discretionary overdraft coverage ensures transactions are simply declined at the point of sale without incurring a fee.

Comments