Financial institutions must rectify compliance errors promptly to mitigate legal risks. A Truth in Lending Act Violation Self-Disclosure Letter serves as a formal notification to regulators or consumers regarding unintentional disclosure inaccuracies. Proactively addressing these oversights demonstrates transparency and can reduce potential penalties. To assist your compliance efforts, below are some ready to use template.

Image cover: Official TILA Violation Self-Disclosure Templates and Compliance Letter Guide

Letter Samples List

- Truth In Lending Act Annual Percentage Rate Calculation Error Self-Disclosure Letter

- Regulation Z Finance Charge Understatement Violation Self-Disclosure Letter

- Truth In Lending Act Right Of Rescission Notice Omission Self-Disclosure Letter

- Mortgage Disclosure Timing Violation Remediation And Self-Disclosure Letter

- Truth In Lending Act Periodic Statement Inaccuracy Self-Disclosure Letter

- Consumer Credit Advertising Violation Regulatory Self-Disclosure Letter

- Truth In Lending Act Customer Overcharge Restitution Self-Disclosure Letter

- Adjustable Rate Mortgage Adjustment Notice Failure Self-Disclosure Letter

- Truth In Lending Act Early Disclosure Delivery Violation Self-Disclosure Letter

- Credit Card Penalty Fee Limitation Violation Self-Disclosure Letter

- Truth In Lending Act Open-End Credit Terms Change Self-Disclosure Letter

- Systemic Loan Origination Software Calculation Error Self-Disclosure Letter

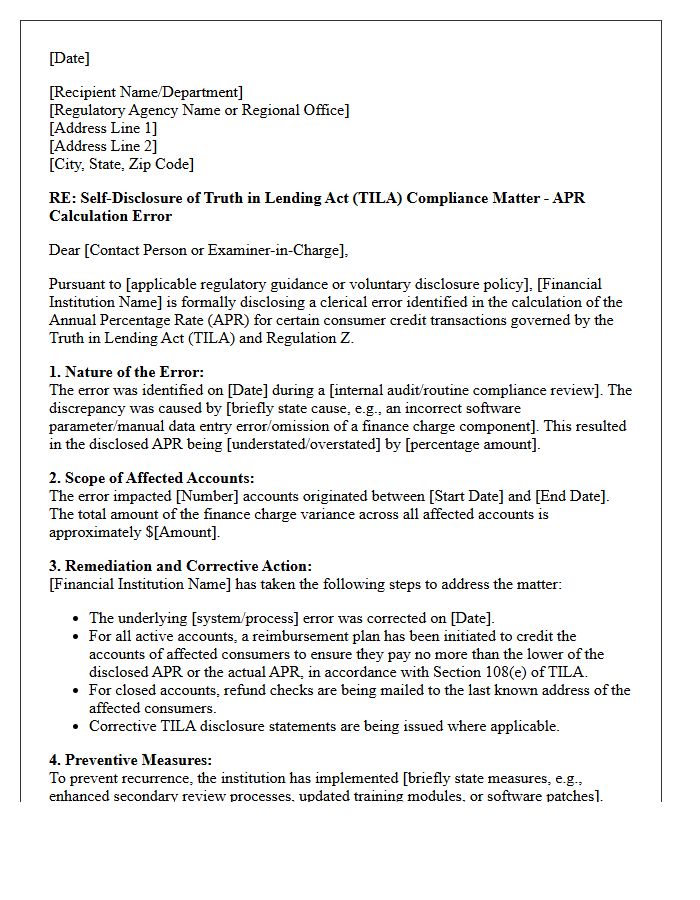

Truth In Lending Act Annual Percentage Rate Calculation Error Self-Disclosure Letter

A Truth In Lending Act (TILA) Self-Disclosure Letter is a formal notification sent by creditors to regulatory agencies when an Annual Percentage Rate (APR) calculation error is discovered. Promptly self-disclosing these inaccuracies is critical for legal compliance and mitigating potential statutory penalties. The letter must detail the scope of the error, the number of impacted consumers, and the remediation plan to refund overcharges. Timely reporting demonstrates proactive regulatory oversight and can significantly reduce the risk of administrative enforcement actions or private class-action litigation arising from disclosure violations.

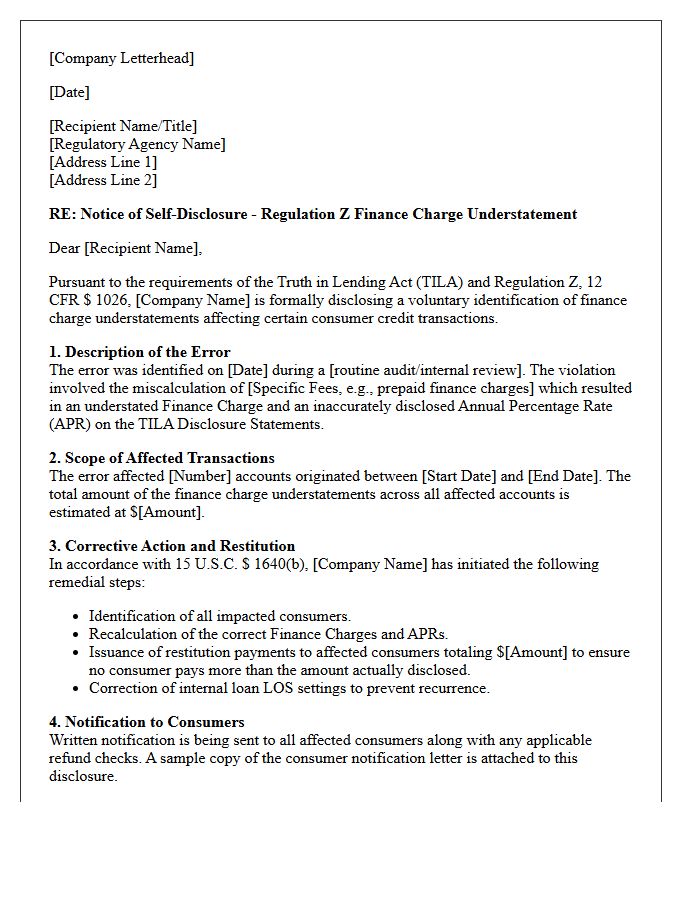

Regulation Z Finance Charge Understatement Violation Self-Disclosure Letter

A Regulation Z Finance Charge Understatement Violation Self-Disclosure Letter is a formal notification sent by lenders to the Consumer Financial Protection Bureau or relevant regulators. This document proactively identifies errors where the disclosed finance charge was understated beyond allowable tolerances. Timely self-disclosure is critical for mitigating civil liability and avoiding statutory penalties under the Truth in Lending Act. The letter must detail the root cause, the scope of affected loans, and the restitution plan to reimburse overcharged consumers, demonstrating a commitment to regulatory compliance and internal corrective actions.

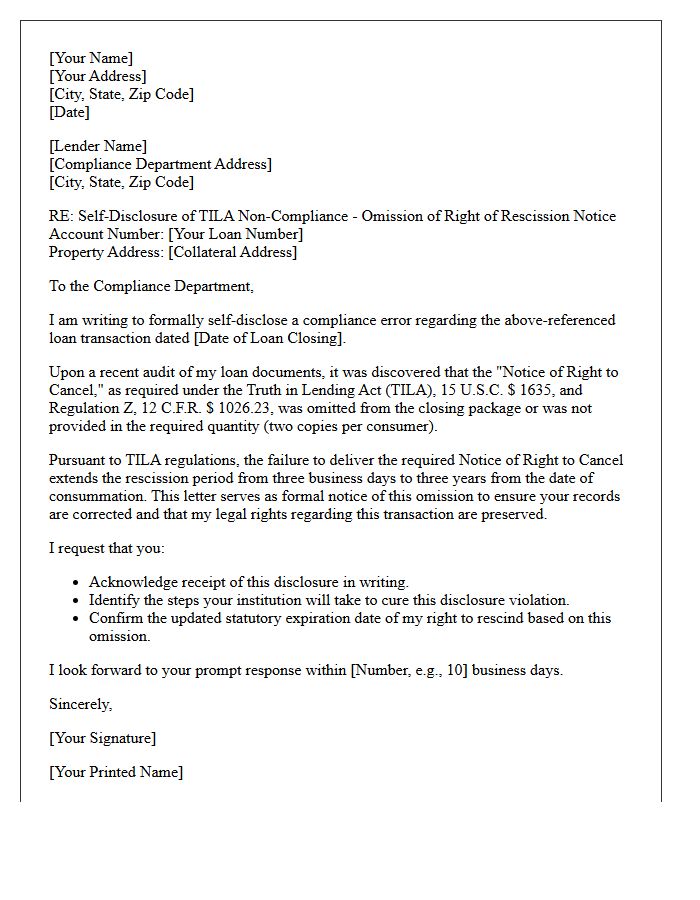

Truth In Lending Act Right Of Rescission Notice Omission Self-Disclosure Letter

The Truth in Lending Act grants borrowers a three-day window to cancel certain home equity loans. If a lender fails to provide the required Right of Rescission notice, the cancellation period may extend up to three years. A Self-Disclosure Letter is a formal document sent by a lender to acknowledge this omission and attempt to mitigate legal liability. For consumers, receiving this letter is critical, as it confirms their extended right to rescind the loan and potentially recover all interest and fees paid due to the compliance error.

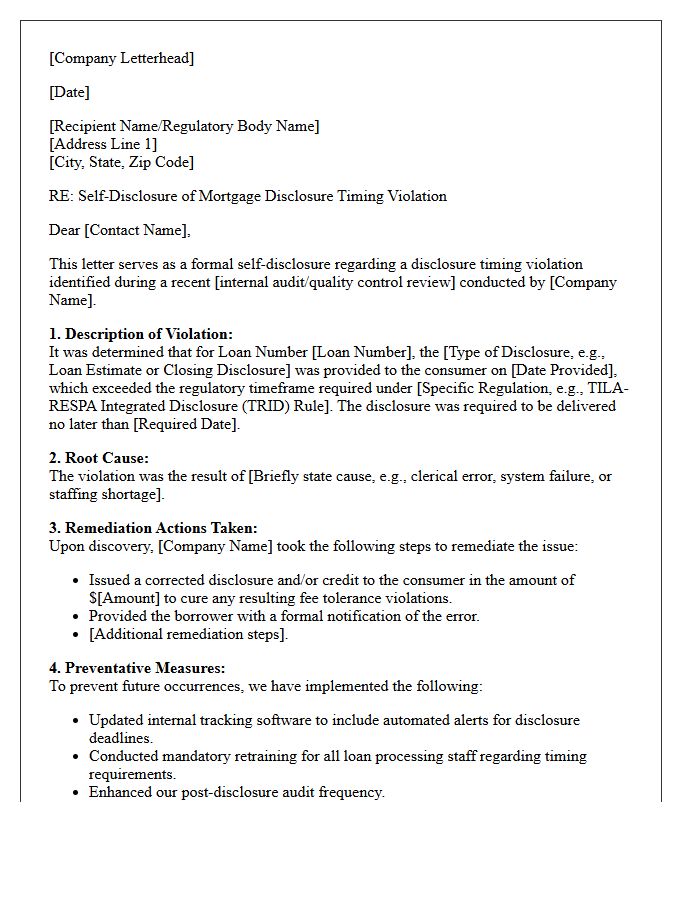

Mortgage Disclosure Timing Violation Remediation And Self-Disclosure Letter

Lenders must address a Mortgage Disclosure Timing Violation immediately to maintain regulatory compliance. When a Loan Estimate or Closing Disclosure is issued outside mandatory federal windows, the primary remediation involves issuing a Self-Disclosure Letter to the consumer. This formal notification acknowledges the error, outlines corrective actions, and may include restitution if the timing error resulted in overcharges. Documenting these breaches through a compliance management system is essential for mitigating penalties during audits and demonstrating a commitment to TILA-RESPA Integrated Disclosure accuracy and consumer protection standards.

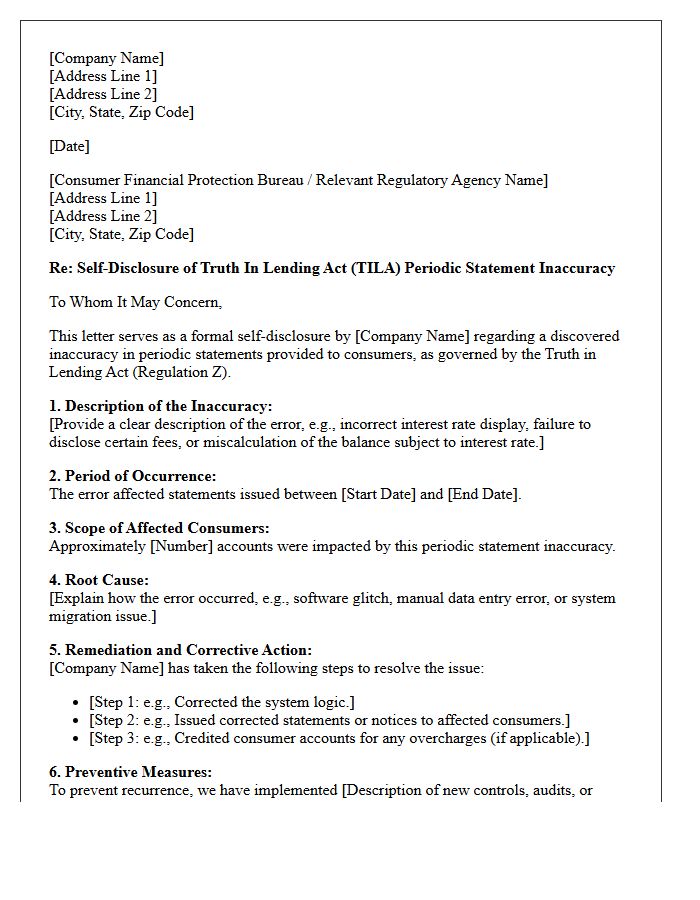

Truth In Lending Act Periodic Statement Inaccuracy Self-Disclosure Letter

Financial institutions use a Truth In Lending Act (TILA) Self-Disclosure Letter to proactively report periodic statement errors to regulators. This formal notification addresses billing inaccuracies, such as incorrect interest charges or missing transaction details, discovered during internal audits. By self-reporting these discrepancies under Regulation Z, creditors demonstrate compliance transparency and a commitment to remedial action. Timely disclosure helps mitigate legal penalties, ensures consumer protection, and confirms that corrective measures, such as customer refunds or statement adjustments, have been implemented to maintain regulatory integrity and trust.

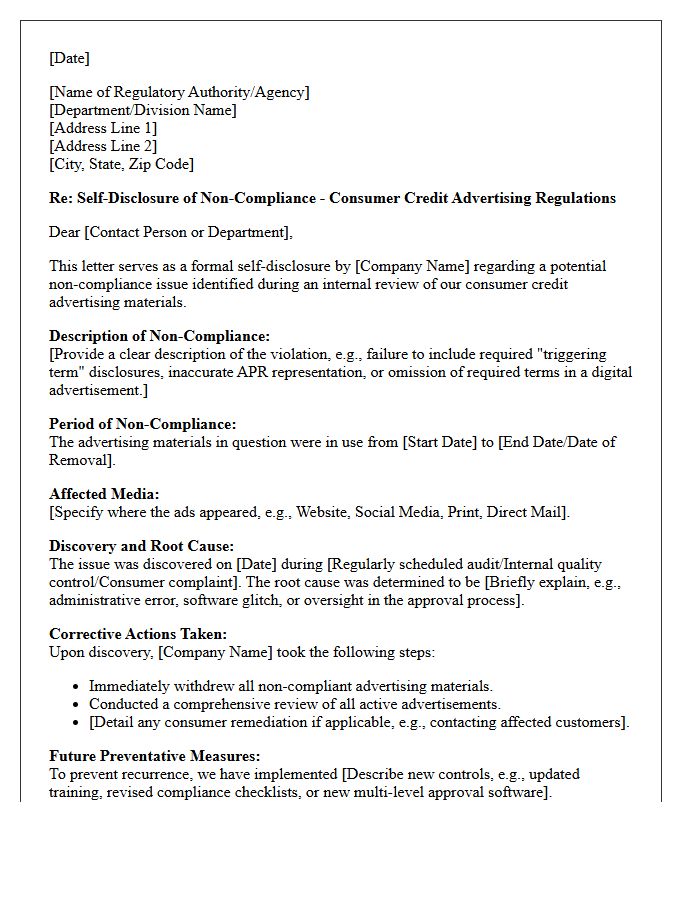

Consumer Credit Advertising Violation Regulatory Self-Disclosure Letter

A Consumer Credit Advertising Violation Regulatory Self-Disclosure Letter is a formal notification sent by a financial institution to regulators when non-compliance with lending disclosure laws is identified. Proactively submitting this voluntary disclosure can significantly mitigate potential administrative penalties and legal actions. The letter must detail the specific advertising error, the duration of the violation, and the remediation plan implemented to correct the issue. Promptly informing authorities demonstrates a commitment to regulatory transparency and consumer protection, often resulting in more lenient oversight during the resolution process.

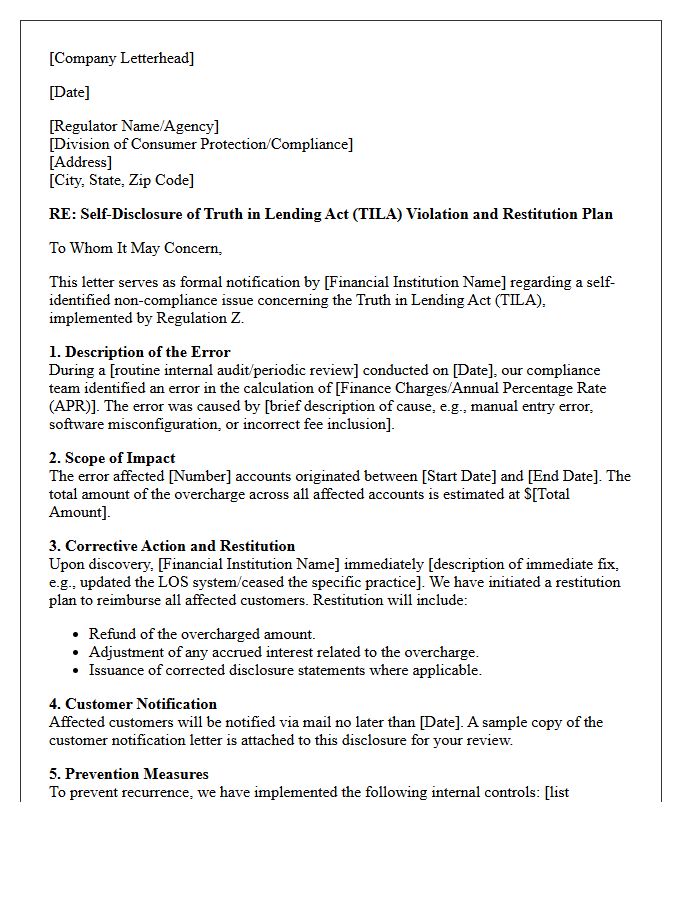

Truth In Lending Act Customer Overcharge Restitution Self-Disclosure Letter

Financial institutions use a Truth In Lending Act Self-Disclosure Letter to proactively report consumer credit violations to regulatory agencies. When a bank discovers an overcharge resulting from incorrect annual percentage rate (APR) calculations or finance charge errors, they must initiate restitution. This formal notification demonstrates compliance efforts and may mitigate potential penalties. The letter details the specific reimbursement plan to return excess funds to affected borrowers, ensuring transparency and adherence to federal Regulation Z requirements regarding fair lending practices and consumer protection standards.

Adjustable Rate Mortgage Adjustment Notice Failure Self-Disclosure Letter

An Adjustable Rate Mortgage Adjustment Notice Failure Self-Disclosure Letter is a formal report sent by lenders to regulators when they fail to provide timely ARM payment change notices. Under Regulation Z, lenders must notify borrowers of interest rate adjustments 60 to 120 days in advance. Self-disclosing these compliance violations demonstrates proactive risk management and may mitigate penalties. The letter typically outlines the error, the number of affected loans, and the remediation plan to refund overcharges or correct payment schedules, ensuring alignment with consumer protection standards.

Truth In Lending Act Early Disclosure Delivery Violation Self-Disclosure Letter

Lenders use a Truth In Lending Act (TILA) Self-Disclosure Letter to proactively report an Early Disclosure Delivery Violation. This formal notice acknowledges a failure to provide required initial disclosures within the three-business-day regulatory window. By voluntarily notifying the borrower and documenting the error, institutions aim to mitigate legal liability and demonstrate compliance oversight. It is essential to include the specific breach details and any corrective actions taken to ensure transparency and maintain regulatory standing with federal authorities while protecting consumer rights under the original statute.

Credit Card Penalty Fee Limitation Violation Self-Disclosure Letter

A Credit Card Penalty Fee Limitation Violation Self-Disclosure Letter is a formal notification sent by financial institutions to regulators, such as the CFPB, acknowledging a breach of Regulation Z. This document outlines instances where late fees or penalties exceeded legal caps. Proactive self-disclosure is essential for mitigating potential fines and demonstrating a commitment to compliance. The letter must detail the root cause, the specific period of non-compliance, and the corrective actions taken to provide restitution to affected consumers while preventing future regulatory violations.

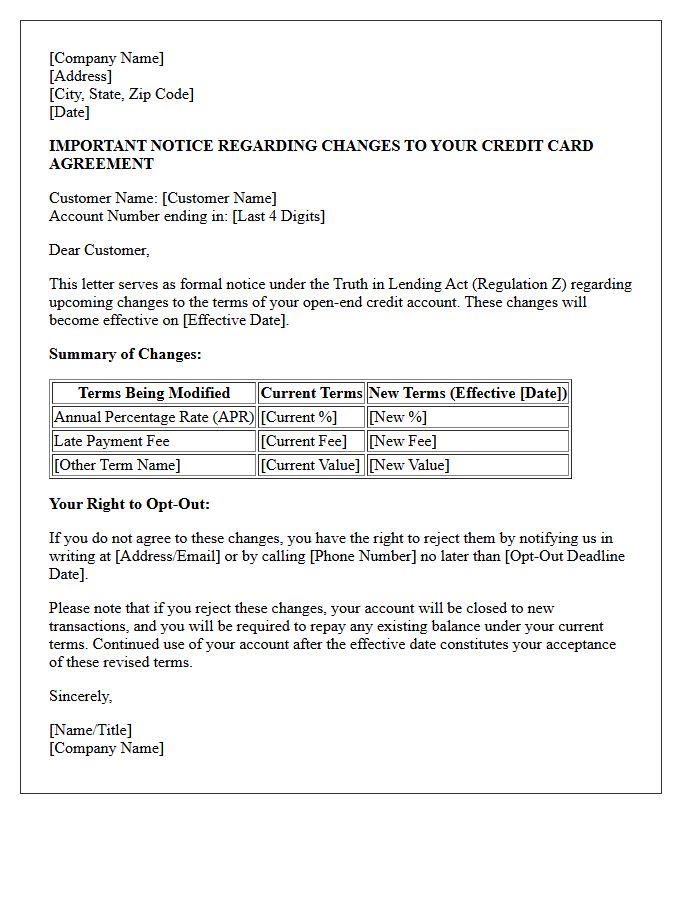

Truth In Lending Act Open-End Credit Terms Change Self-Disclosure Letter

A Truth In Lending Act (TILA) self-disclosure letter is a formal notification sent by creditors to consumers when modifying open-end credit agreements, such as credit cards. Under federal law, lenders must provide a clear written notice at least 45 days before significant changes take effect. This includes adjustments to interest rates, fees, or payment terms. This transparency ensures borrowers understand their financial obligations and maintain the right to opt-out or cancel the account before new, potentially costlier terms are legally applied to their outstanding balance.

Systemic Loan Origination Software Calculation Error Self-Disclosure Letter

A Systemic Loan Origination Software Calculation Error Self-Disclosure Letter is a formal notification sent to regulators when a technical glitch causes widespread compliance violations or inaccurate financial disclosures. Lenders use this document to proactively report errors in APR, fees, or interest calculations before an audit. To mitigate regulatory penalties, the letter must detail the root cause, the volume of affected loans, and a comprehensive remediation plan to reimburse consumers. Transparent self-disclosure demonstrates a commitment to consumer protection and can significantly reduce the severity of enforcement actions under federal banking laws.

What is a Truth in Lending Act (TILA) self-disclosure letter?

A TILA self-disclosure letter is a formal notification sent by a creditor to a consumer or regulatory body voluntarily identifying errors or violations of the Truth in Lending Act, such as incorrect Annual Percentage Rate (APR) disclosures or missing finance charges.

How does a self-disclosure letter affect statutory penalties under TILA?

Under 15 U.S.C. § 1640(b), a creditor may avoid liability for statutory penalties if they notify the consumer of the error within 60 days of discovery, provided the notification occurs before the consumer files a lawsuit or provides written notice of the error.

What information must be included in a TILA violation disclosure?

The letter must clearly state the specific disclosure error, provide the corrected financial information, and outline the adjustments made to the consumer's account to ensure they do not pay more than the lower of the disclosed or actual finance charge.

Can self-disclosure prevent a consumer from exercising their right of rescission?

Self-disclosure can mitigate damages, but if the violation involved a "material disclosure" on a principal residence loan, the consumer may still retain their three-year right of rescission unless the error is corrected and a new notice of right to cancel is provided.

What are the requirements for a TILA "Bona Fide Error" defense?

To use self-disclosure as a defense, the creditor must prove the violation was unintentional and resulted from a bona fide error, such as a clerical, calculation, or printing mistake, despite maintaining procedures reasonably adapted to avoid such errors.

Comments