Receiving a Bank Secrecy Act Non-Compliance Letter indicates that your financial institution has identified deficiencies in your anti-money laundering protocols. Addressing these regulatory gaps promptly is essential to avoid severe legal penalties and reputational damage. This guide outlines how to respond effectively to enforcement actions and improve your compliance framework. To help you draft a professional response, below are some ready to use template.

Image cover: Formal Templates and Response Guide for Bank Secrecy Act Non-Compliance Notifications

Letter Samples List

- Unfiled Currency Transaction Report Non-Compliance Warning Letter

- Suspicious Activity Report Omission Penalty Letter

- Know Your Customer Deficiencies Audit Finding Letter

- Customer Identification Program Violation Notice Letter

- Anti-Money Laundering Program Inadequacy Warning Letter

- Beneficial Ownership Documentation Non-Compliance Letter

- Bank Secrecy Act Staff Training Deficiency Letter

- Independent Testing And Audit Failure Resolution Letter

- Enhanced Due Diligence Oversights Notification Letter

- Board Of Directors Bank Secrecy Act Escalation Letter

- Transaction Recordkeeping Requirement Violation Letter

- Financial Crimes Enforcement Network Civil Money Penalty Letter

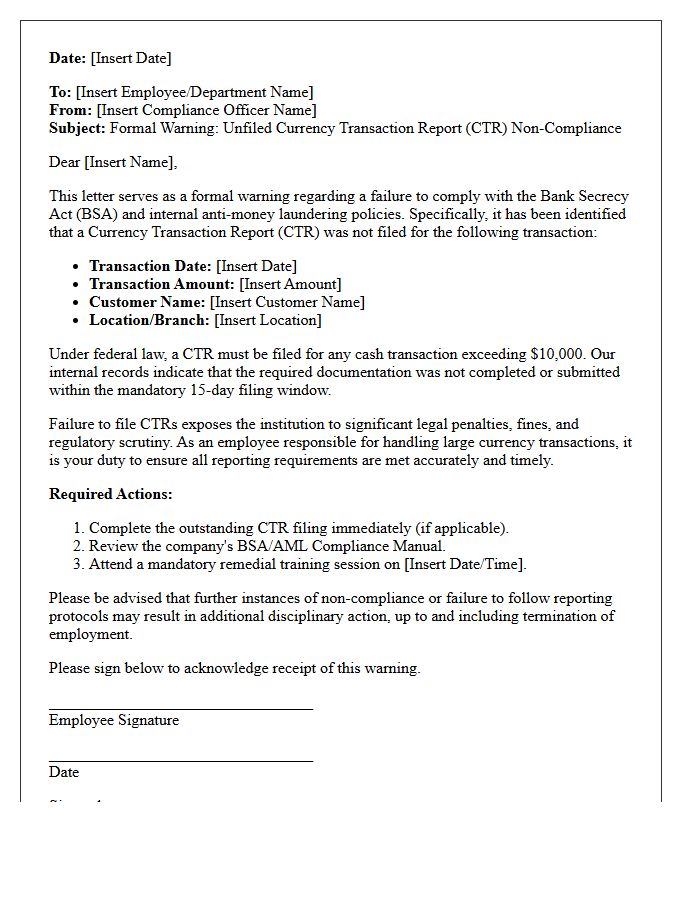

Unfiled Currency Transaction Report Non-Compliance Warning Letter

An Unfiled Currency Transaction Report Non-Compliance Warning Letter is a formal notification from FinCEN or the IRS regarding failures to report cash transactions exceeding $10,000. Receiving this notice indicates that your institution missed mandatory filings required by the Bank Secrecy Act. It serves as a final opportunity to rectify anti-money laundering (AML) deficiencies before the government imposes severe civil money penalties or legal sanctions. Immediate corrective action, including filing backlogged reports and enhancing internal audit controls, is essential to demonstrate compliance and avoid formal enforcement proceedings.

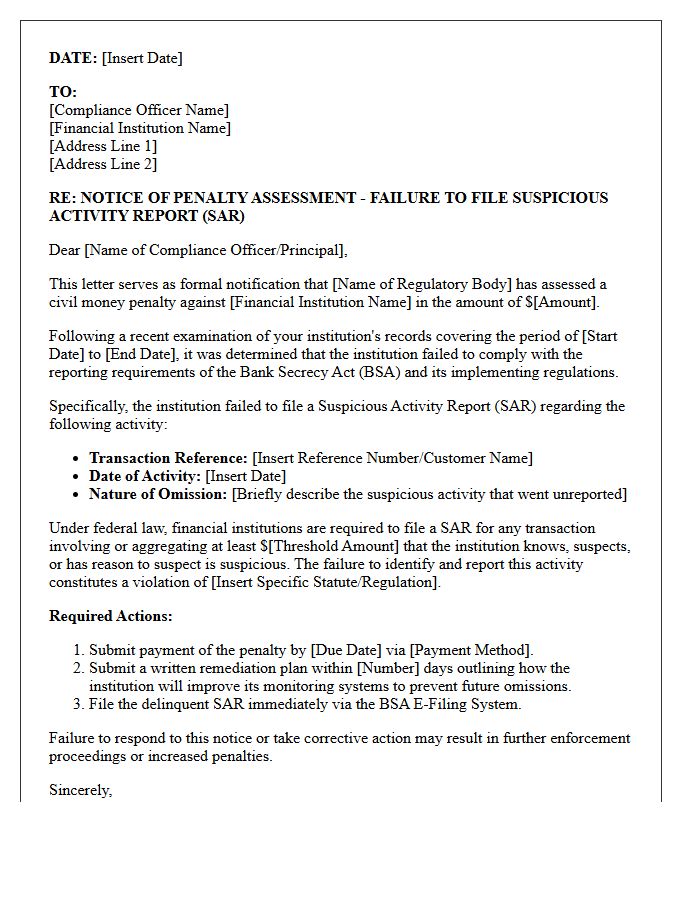

Suspicious Activity Report Omission Penalty Letter

Receiving a Suspicious Activity Report Omission Penalty Letter indicates that a financial institution failed to file mandatory SARs as required by the Bank Secrecy Act. This formal notice from regulators signifies serious compliance failures regarding anti-money laundering (AML) protocols. The most critical aspect is the potential for significant civil money penalties and heightened regulatory scrutiny. Organizations must respond immediately by addressing internal control weaknesses and demonstrating corrective actions to mitigate further legal liability and protect their professional reputation from severe regulatory enforcement actions.

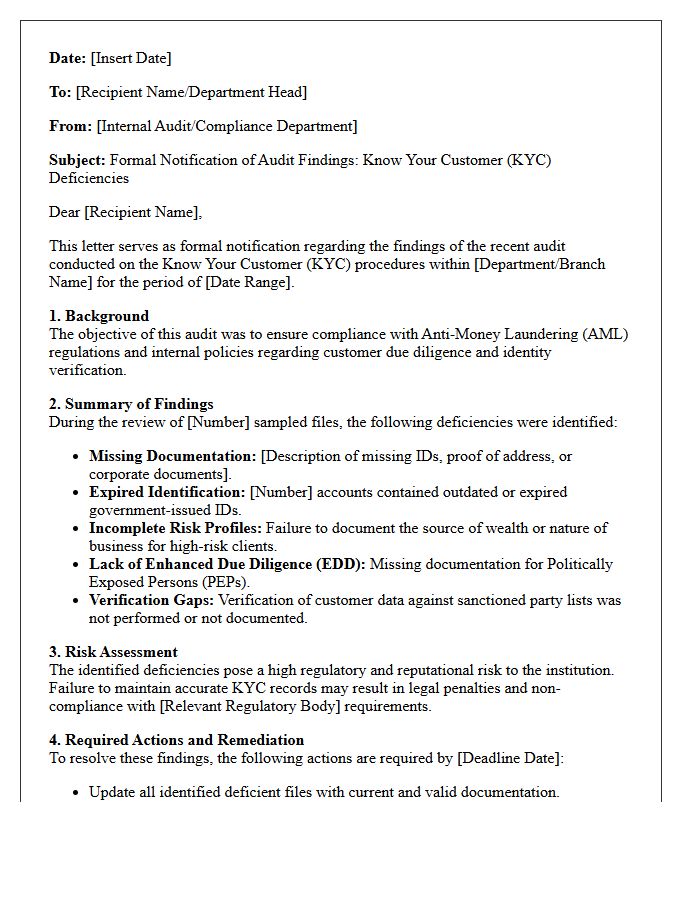

Know Your Customer Deficiencies Audit Finding Letter

A Know Your Customer Deficiencies Audit Finding Letter is a formal notification issued by regulators or internal auditors identifying gaps in your Anti-Money Laundering (AML) compliance program. This document highlights failures in identity verification, risk assessment, or due diligence procedures. Receiving this letter requires immediate corrective action to remediate missing documentation and improve monitoring systems. Addressing these findings promptly is critical to avoid severe regulatory penalties, legal sanctions, or the loss of banking licenses resulting from non-compliance with established financial security standards.

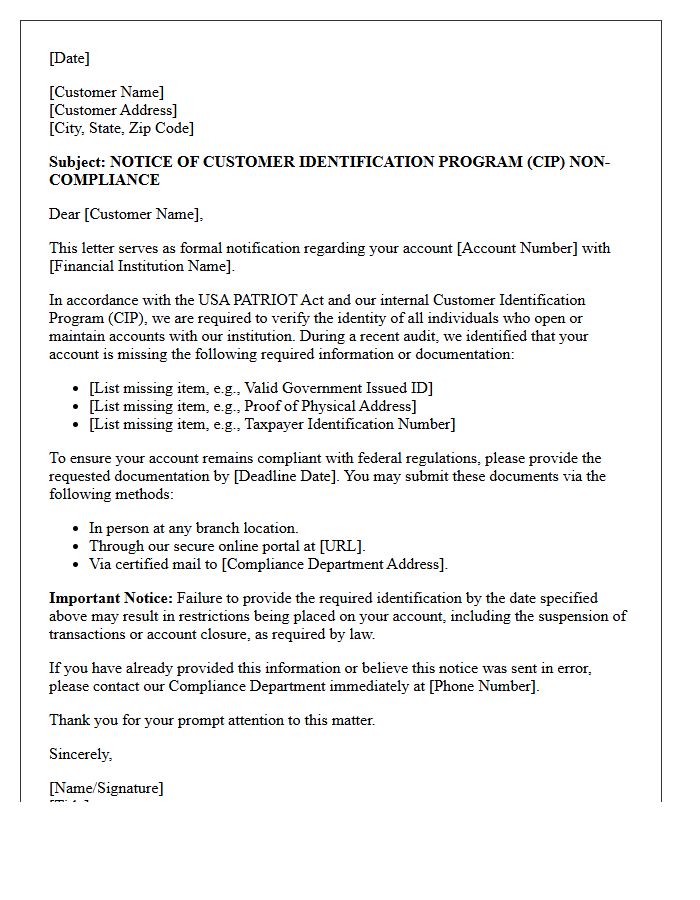

Customer Identification Program Violation Notice Letter

A Customer Identification Program (CIP) violation notice letter is a formal notification issued by a financial institution when an account fails to comply with AML regulations. It indicates that the identity verification process required by the USA PATRIOT Act was incomplete or unsuccessful. Recipient action is critical; you must provide valid government-issued identification or updated documentation immediately. Failure to resolve these compliance discrepancies within the specified timeframe typically results in account restrictions or permanent closure to mitigate risks of fraud and financial crimes.

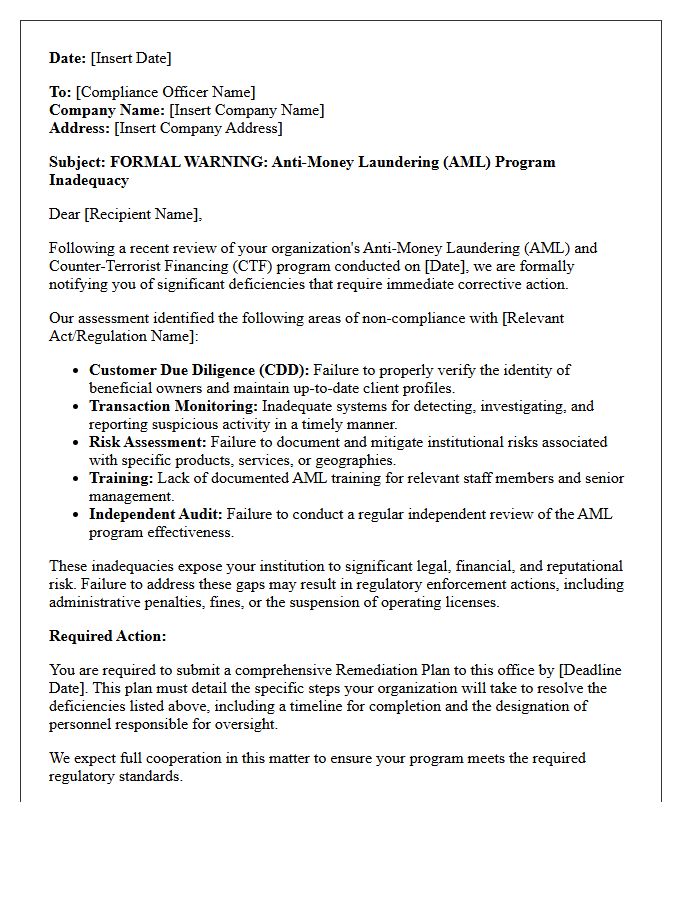

Anti-Money Laundering Program Inadequacy Warning Letter

An Anti-Money Laundering Program Inadequacy Warning Letter is a formal notice issued by regulators, such as FINRA or FinCEN, signaling critical deficiencies in a firm's compliance framework. This official notification serves as a final opportunity to rectify systemic gaps in monitoring, reporting, and due diligence protocols before severe enforcement actions occur. Receiving this letter indicates that current safeguards are insufficient to prevent financial crime, requiring immediate corrective measures to avoid heavy fines, regulatory sanctions, or the potential loss of operating licenses. Prompt remediation is essential to ensure institutional integrity.

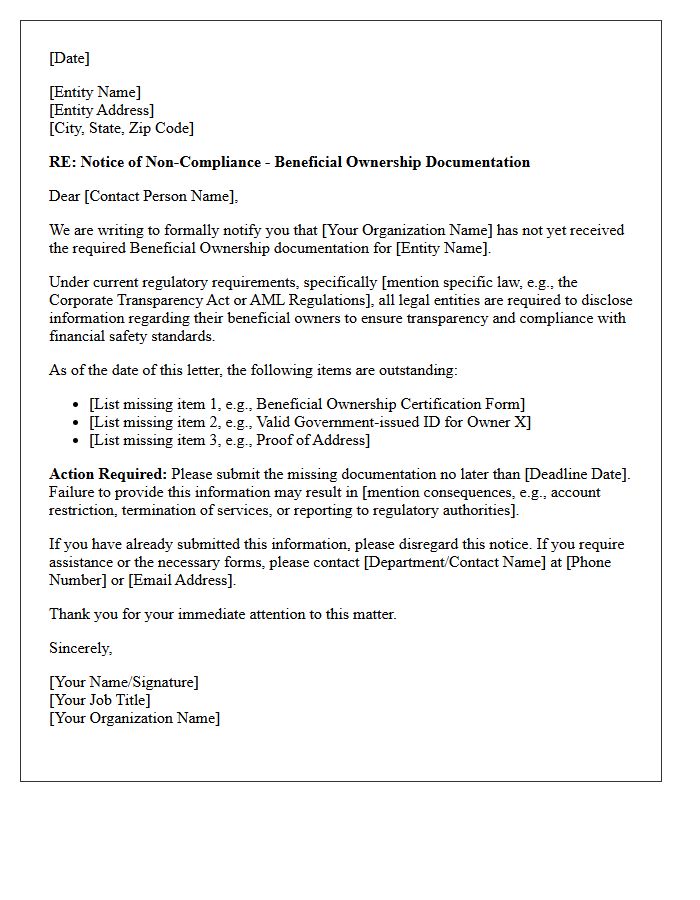

Beneficial Ownership Documentation Non-Compliance Letter

Receiving a Beneficial Ownership Documentation Non-Compliance Letter indicates that your entity has failed to meet transparency requirements regarding its controlling stakeholders. This formal notice often stems from missing or inaccurate filings with regulatory bodies like FinCEN. It is critical to address these reporting discrepancies immediately to avoid severe penalties, including significant daily fines or criminal charges. To achieve compliance, you must verify the identity of all individuals with substantial control and submit updated documentation through official channels to ensure legal corporate transparency.

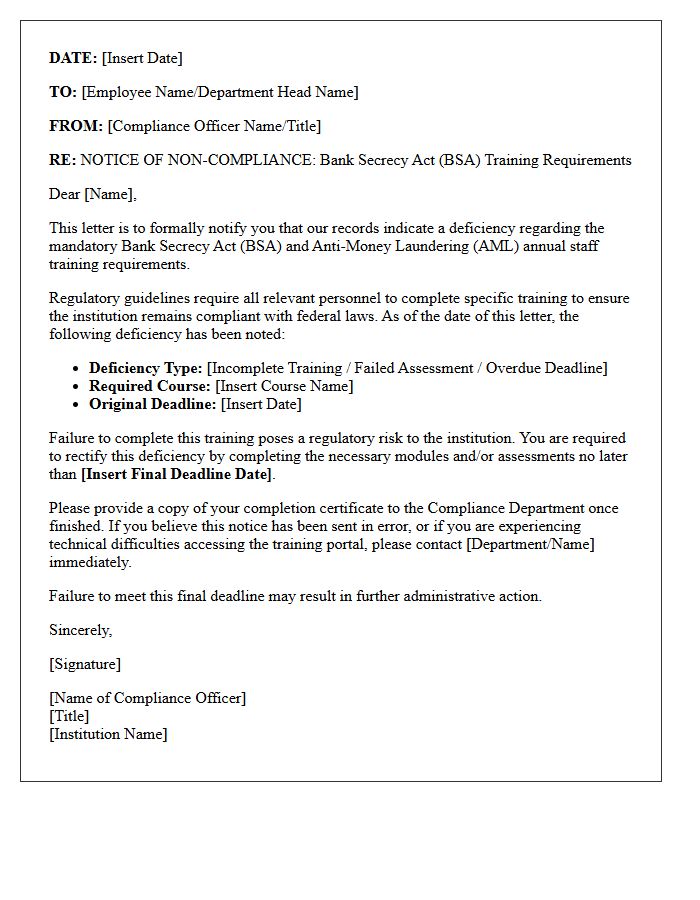

Bank Secrecy Act Staff Training Deficiency Letter

A Bank Secrecy Act Staff Training Deficiency Letter is a formal notification from regulators indicating that a financial institution's AML compliance program fails to meet educational standards. This document highlights a specific regulatory gap where employees lack the necessary knowledge to detect and report suspicious activities. Failure to address these findings through enhanced staff training can lead to severe enforcement actions, substantial fines, and increased institutional risk. Correcting these deficiencies requires implementing comprehensive, role-specific instruction and maintaining detailed records to prove ongoing compliance effectiveness to auditors and examiners.

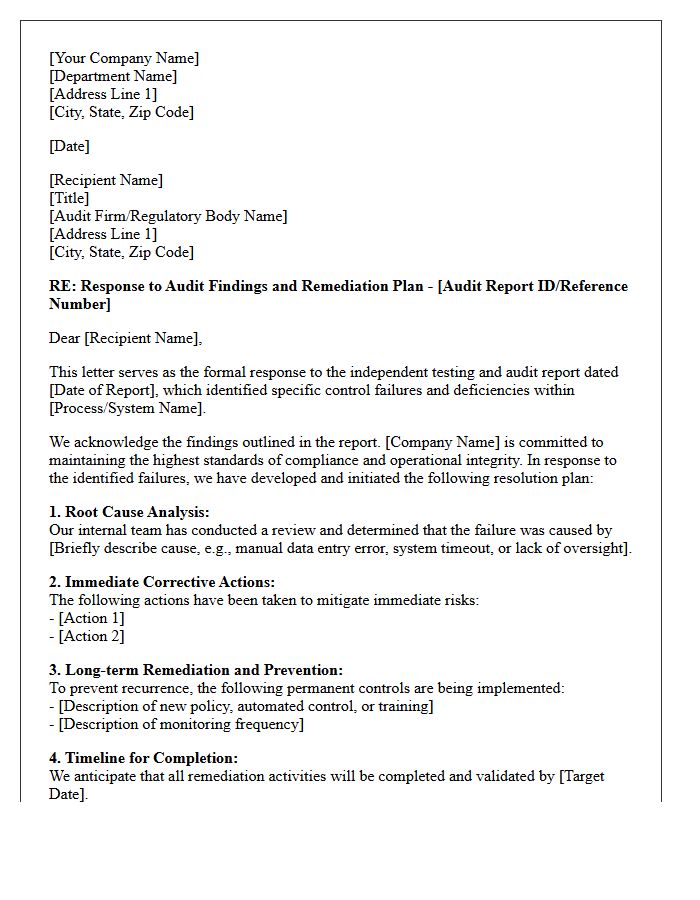

Independent Testing And Audit Failure Resolution Letter

An Independent Testing and Audit Failure Resolution Letter is a formal document addressing compliance deficiencies identified during financial or operational reviews. It outlines specific remediation actions, timelines, and responsible parties to rectify internal control gaps. This letter serves as critical evidence for regulators and stakeholders that a firm is actively mitigating risks and restoring governance standards. Effectively drafting this response ensures that systemic vulnerabilities are resolved, preventing future legal penalties or operational disruptions while demonstrating a commitment to regulatory integrity and continuous process improvement.

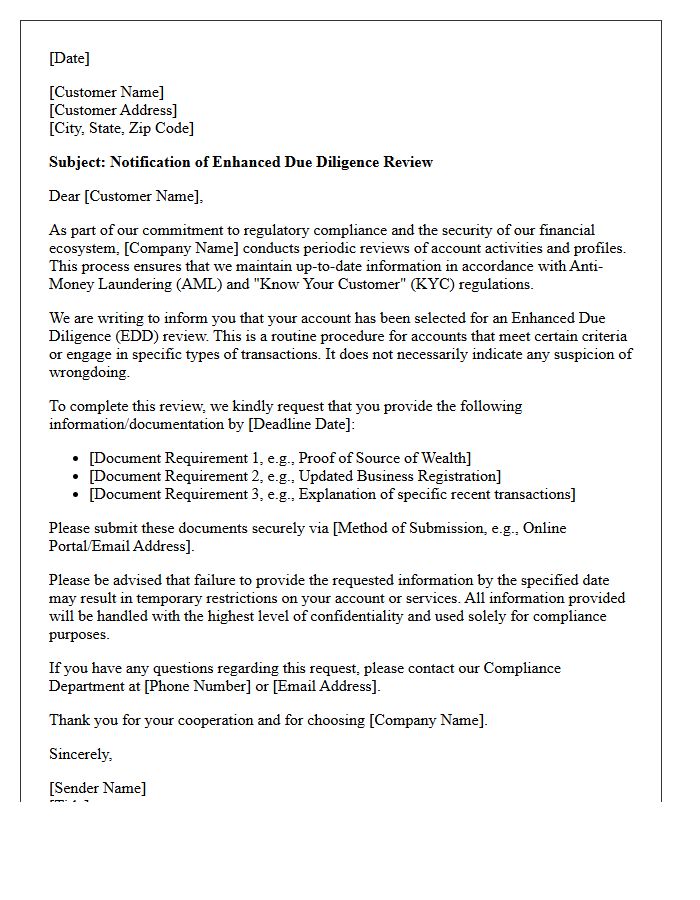

Enhanced Due Diligence Oversights Notification Letter

An Enhanced Due Diligence (EDD) Oversights Notification Letter is a formal communication from a financial institution to a high-risk client. It specifies that additional scrutiny is required to verify the source of wealth and transaction legitimacy. This process ensures compliance with Anti-Money Laundering (AML) regulations. Receiving this letter indicates that the bank must mitigate potential risks through rigorous documentation and continuous monitoring. Failure to provide requested information can lead to account restrictions or termination, as institutions must fulfill strict regulatory obligations to prevent financial crime and maintain systemic integrity.

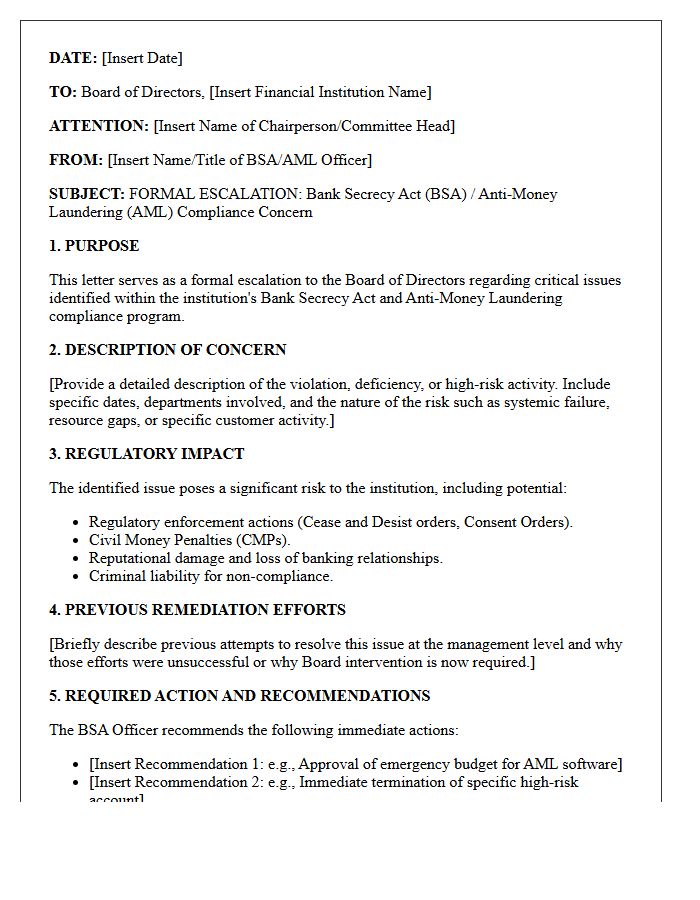

Board Of Directors Bank Secrecy Act Escalation Letter

A Board of Directors Bank Secrecy Act (BSA) Escalation Letter is a critical regulatory notification indicating systemic AML compliance failures. This formal document warns leadership that previous audit findings or regulatory deficiencies remain unresolved. Receiving this letter signifies that legal or financial penalties are imminent unless the board takes immediate oversight action. It serves as a final opportunity for senior management to allocate necessary resources and correct anti-money laundering violations before the institution faces severe enforcement actions, consent orders, or significant reputational damage.

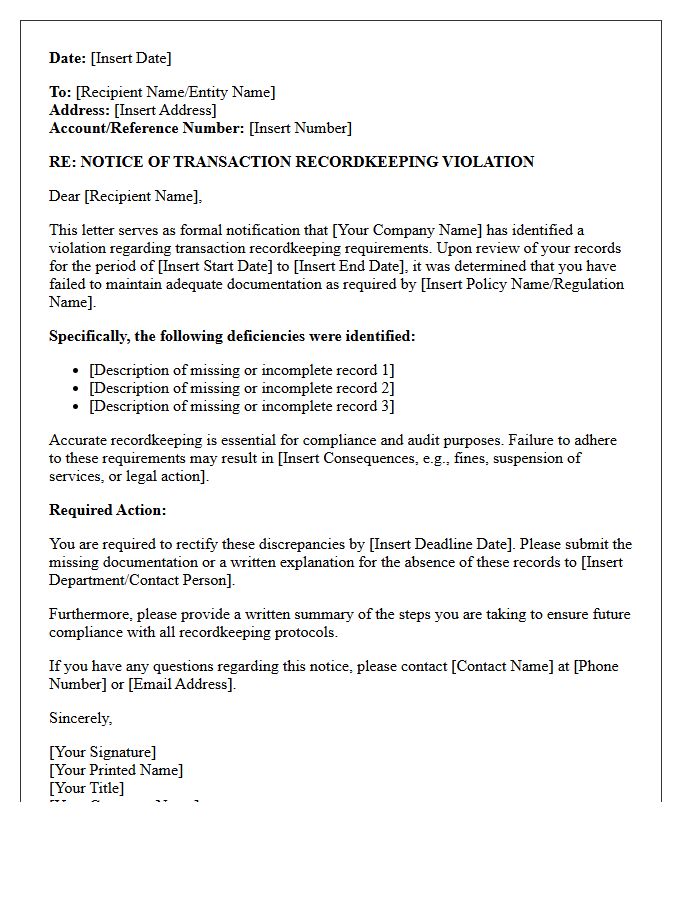

Transaction Recordkeeping Requirement Violation Letter

Receiving a Transaction Recordkeeping Requirement Violation Letter signifies a failure to maintain accurate financial documentation mandated by regulatory bodies like the IRS or FinCEN. This formal notice indicates that your compliance procedures are insufficient, often involving missing receipts, incomplete logs, or unreported transactions. Ignoring this warning can lead to severe penalties, audits, or legal action. It is essential to immediately rectify accounting gaps, preserve all future records, and potentially consult a professional to ensure your business meets all statutory reporting obligations to avoid further escalation.

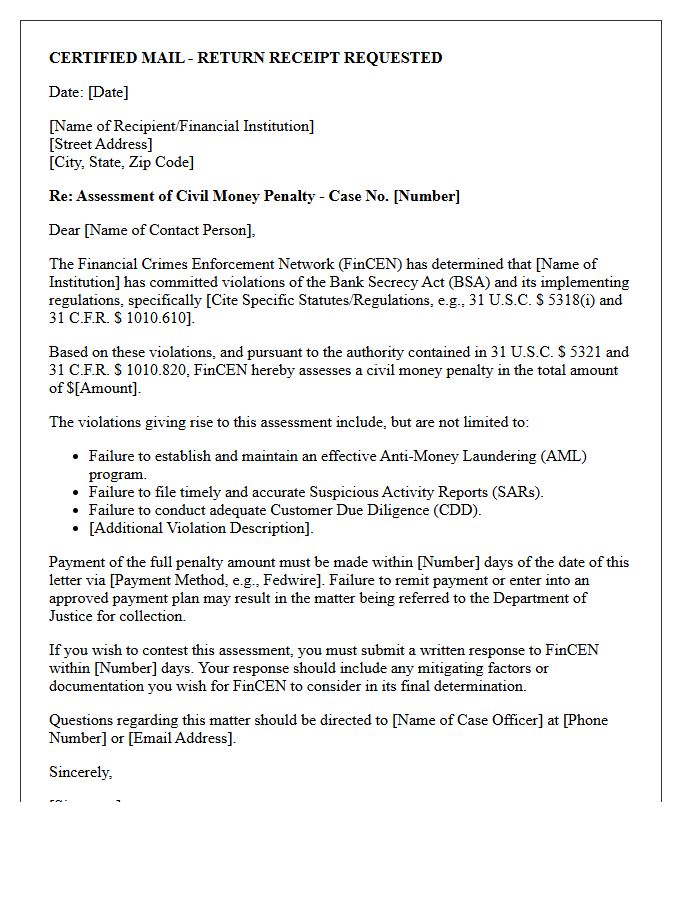

Financial Crimes Enforcement Network Civil Money Penalty Letter

A Financial Crimes Enforcement Network (FinCEN) Civil Money Penalty Letter is a formal notification of legal action for violations of the Bank Secrecy Act (BSA). These letters demand payment for compliance failures, such as inadequate anti-money laundering (AML) programs or failing to file suspicious activity reports. Receiving one indicates severe regulatory breaches that can result in significant monetary fines and public reputational damage. Financial institutions must respond urgently, as these penalties are legally enforceable measures designed to deter illicit financial activities and ensure global financial transparency and accountability.

What is a Bank Secrecy Act (BSA) non-compliance letter?

A Bank Secrecy Act non-compliance letter is an official notification sent by federal regulators, such as the FinCEN, OCC, or FDIC, informing a financial institution that they have failed to maintain adequate anti-money laundering (AML) controls or have violated specific record-keeping and reporting requirements.

What are the common reasons for receiving a BSA non-compliance notice?

Common triggers include failure to file Suspicious Activity Reports (SARs) or Currency Transaction Reports (CTRs), inadequate customer due diligence (CDD) processes, insufficient staff training, or failing to designate a qualified BSA compliance officer.

What are the potential penalties for failing to comply with BSA regulations?

Consequences for non-compliance range from formal written agreements and Cease and Desist orders to substantial civil money penalties (CMPs), increased regulatory oversight, and in severe cases, criminal charges against the institution or its executives.

How should a financial institution respond to a BSA non-compliance letter?

An institution must respond by acknowledging the deficiencies, providing a detailed remediation plan with specific timelines, and demonstrating a commitment to enhancing their AML/BSA compliance framework to prevent future violations.

Can a BSA non-compliance letter affect a bank's regulatory rating?

Yes, receiving a non-compliance letter typically leads to a downgrade in the institution's management or compliance ratings (such as the CAMELS rating), which can restrict the bank's ability to engage in mergers, acquisitions, or branch expansions.

Comments