A Fair Lending Compliance Warning Letter is a formal notification sent to financial institutions regarding potential discriminatory practices or regulatory violations. It serves as a critical alert to rectify disparities in credit distribution before formal enforcement actions occur. Understanding these notices is essential for maintaining legal standards and institutional integrity. Below are some ready to use template.

Image cover: Compliance Alert: Standardized Fair Lending Warning Letter Templates and Samples

Letter Samples List

- Disparate Impact Loan Pricing Warning Letter

- Geographic Redlining Compliance Warning Letter

- Underwriting Disparities Fair Lending Warning Letter

- Equal Credit Opportunity Act Violation Warning Letter

- Fair Housing Act Non-Compliance Warning Letter

- Discriminatory Steering Practices Warning Letter

- Targeted Marketing Exclusion Warning Letter

- Home Mortgage Disclosure Act Anomaly Warning Letter

- Discretionary Pricing Markup Warning Letter

- Property Appraisal Bias Warning Letter

- Automated Underwriting Bias Warning Letter

- Policy Exception Disparity Warning Letter

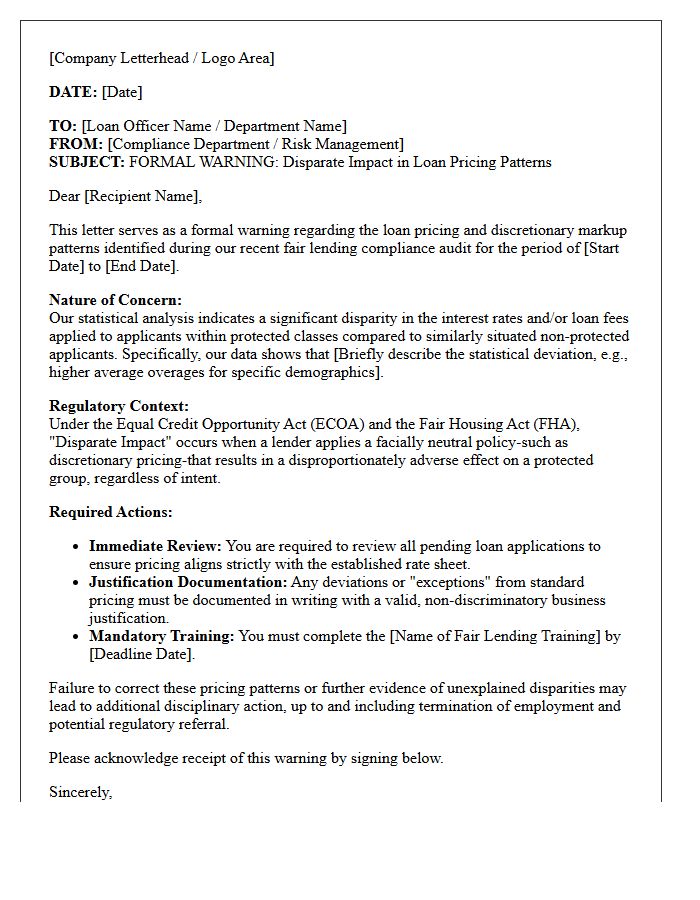

Disparate Impact Loan Pricing Warning Letter

A Disparate Impact Loan Pricing Warning Letter is a formal notification from regulators indicating that statistical analysis suggests lending discrimination. It warns that neutral pricing policies may have an unintended, disproportionate adverse effect on protected classes, such as minority borrowers. This letter serves as a compliance alert, requiring lenders to justify their pricing disparities through legitimate business necessity or face potential enforcement actions. To mitigate legal risks, financial institutions must prioritize regular fair lending audits and implement robust monitoring systems to ensure equitable treatment across all demographic groups.

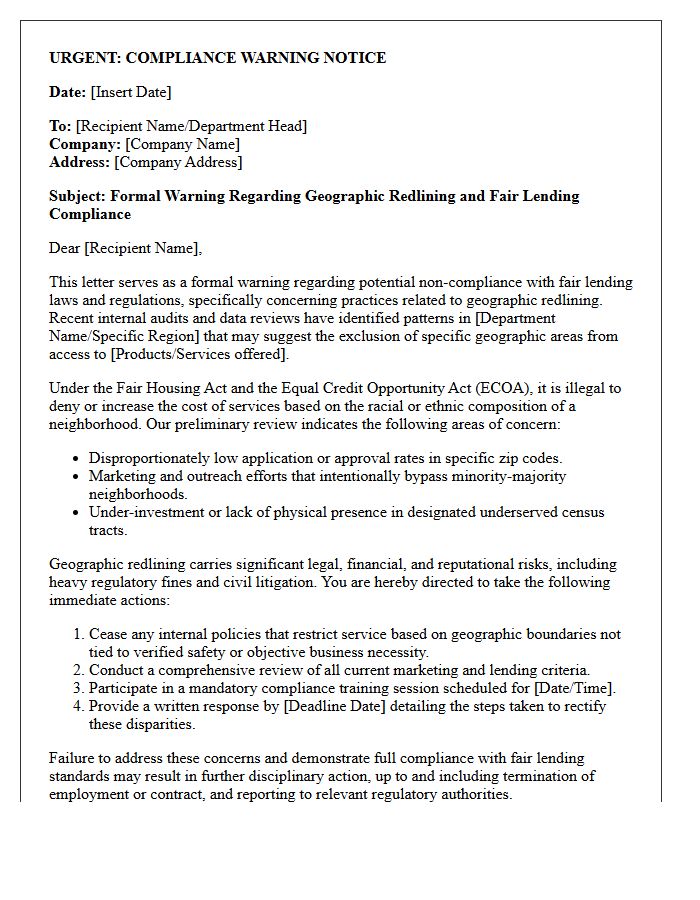

Geographic Redlining Compliance Warning Letter

A Geographic Redlining Compliance Warning Letter is a formal notification issued by regulators regarding potential violations of Fair Lending laws. This document alerts financial institutions that their lending patterns show discriminatory exclusion of specific neighborhoods based on racial or ethnic demographics. Recipient firms must immediately conduct a risk assessment and implement corrective actions to ensure equitable credit access. Failure to address these disparities often leads to severe legal penalties, public enforcement actions, and significant reputational damage. Proactive monitoring of market penetration and loan distribution is essential for maintaining regulatory compliance.

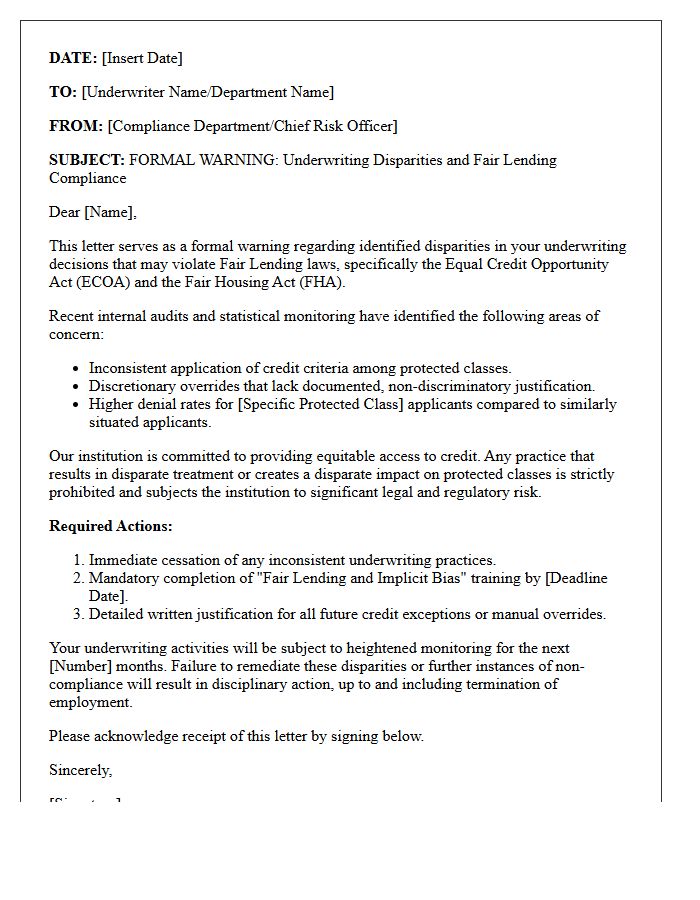

Underwriting Disparities Fair Lending Warning Letter

An Underwriting Disparities Fair Lending Warning Letter is a formal notification from regulators identifying potential discriminatory patterns in a creditor's loan approval process. These letters typically alert institutions that statistical anomalies suggest minority applicants are being denied at significantly higher rates than similarly situated non-minority peers. Receiving this warning indicates a high risk of violating the Equal Credit Opportunity Act. Lenders must immediately conduct a root-cause analysis, refine their underwriting models, and implement corrective actions to ensure fair access to credit and avoid formal enforcement penalties.

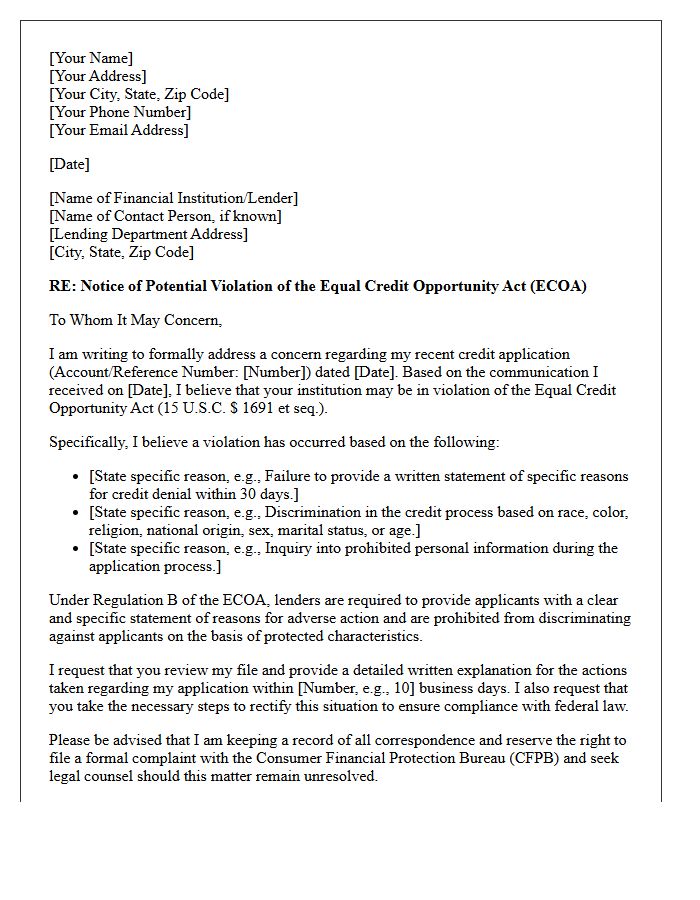

Equal Credit Opportunity Act Violation Warning Letter

An Equal Credit Opportunity Act Violation Warning Letter is a formal notice sent to creditors alleging discriminatory lending practices. This document identifies specific failures to comply with federal regulations that prohibit bias based on race, religion, or gender. Receiving this warning indicates a potential enforcement action or lawsuit. Financial institutions must respond by auditing their underwriting criteria to ensure fair treatment. Understanding these violations is crucial for maintaining legal compliance and avoiding significant civil penalties, as the act ensures all creditworthy applicants have equal access to financial opportunities without prejudice.

Fair Housing Act Non-Compliance Warning Letter

A Fair Housing Act Non-Compliance Warning Letter is a formal legal notice indicating potential discriminatory practices in residential real estate. Receiving this document signifies a violation of federal laws protecting against bias based on race, religion, sex, or disability. Property owners must provide an immediate corrective response to mitigate legal exposure and avoid costly litigation or federal investigations. Understanding these warnings is critical for maintaining fair housing standards and ensuring equal opportunity. Ignoring such notices can lead to severe financial penalties and permanent damage to a housing provider's professional reputation.

Discriminatory Steering Practices Warning Letter

A Discriminatory Steering Practices Warning Letter is a formal legal notice issued to real estate professionals suspected of housing discrimination. It serves as a serious caution against the illegal act of "steering," which involves directing prospective buyers toward or away from specific neighborhoods based on protected characteristics like race or religion. Receiving this letter indicates potential violations of the Fair Housing Act. Firms must immediately audit their compliance protocols and agent conduct to avoid severe litigation, license revocation, and substantial financial penalties resulting from systemic bias in the property market.

Targeted Marketing Exclusion Warning Letter

A Targeted Marketing Exclusion Warning Letter is a formal notice sent by regulators to businesses suspected of using discriminatory advertising practices. This document warns that their algorithms or audience filters may be illegally excluding protected groups from seeing essential offers, such as housing, employment, or credit opportunities. Receiving this letter indicates a potential violation of fair lending or civil rights laws. Companies must immediately audit their ad delivery systems and data parameters to ensure compliance and prevent significant legal penalties or formal enforcement actions.

Home Mortgage Disclosure Act Anomaly Warning Letter

A Home Mortgage Disclosure Act (HMDA) Anomaly Warning Letter is a formal notification from regulators identifying data inconsistencies or statistical outliers in a financial institution's loan application register. Receiving this letter indicates that your submitted information deviates significantly from historical patterns or peer benchmarks. It is crucial to verify data accuracy immediately to ensure compliance. Financial institutions must investigate these discrepancies promptly to determine if they result from reporting errors or actual shifts in lending practices, as unresolved anomalies can trigger regulatory audits or fair lending examinations.

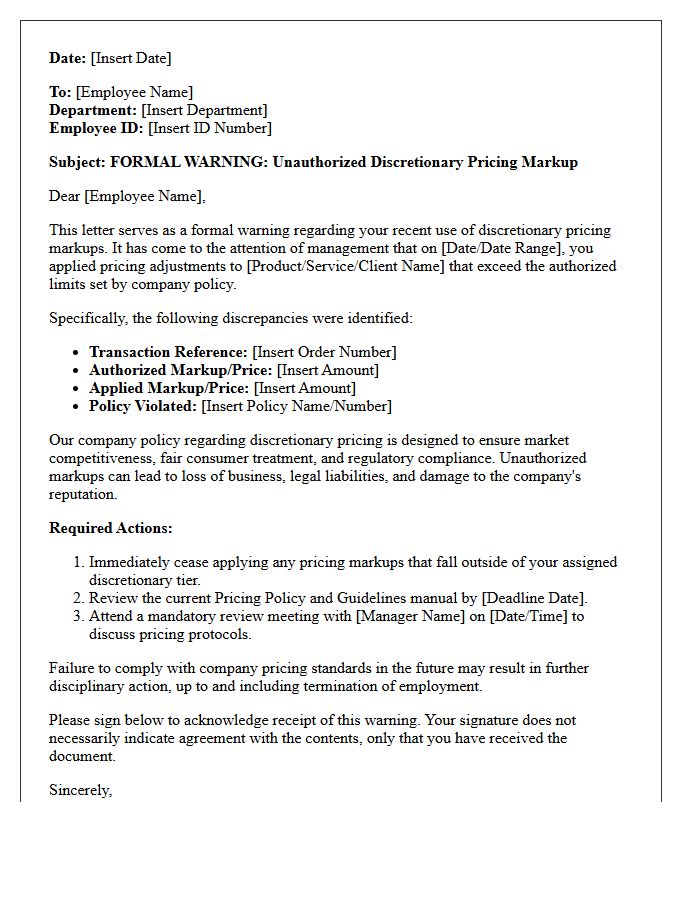

Discretionary Pricing Markup Warning Letter

A Discretionary Pricing Markup Warning Letter is a formal notification from regulators or lenders indicating potential fair lending violations. It flags concerns that loan officers may be applying inconsistent interest rate markups, often resulting in disparate impact against protected classes. To mitigate legal risk, institutions must monitor pricing variations and implement strict compliance controls. Receiving this letter requires immediate internal auditing of discretionary adjustments to ensure non-discriminatory practices and to avoid severe regulatory penalties or lawsuits.

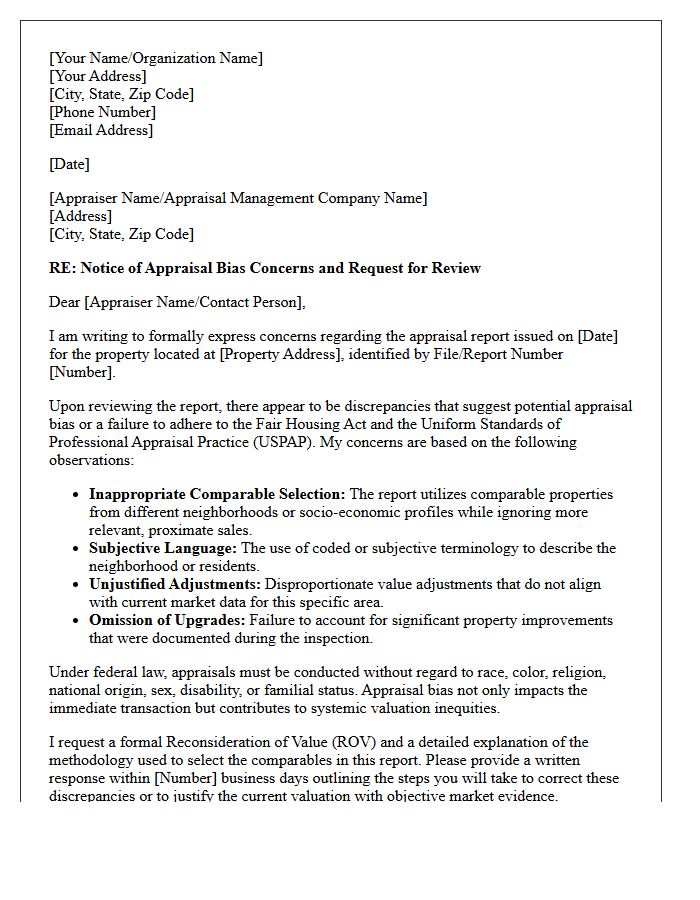

Property Appraisal Bias Warning Letter

A Property Appraisal Bias Warning Letter is a formal notification issued when valuation discrimination is suspected during the home appraisal process. This document alerts lenders and regulators that a property's value may have been unfairly influenced by the owner's race, religion, or neighborhood demographics. It is a critical tool for homeownership equity, allowing consumers to dispute undervalued assessments and request a reconsideration of value. Understanding this letter helps protect your fair housing rights and ensures that property appraisals remain objective, accurate, and free from illegal systemic prejudice.

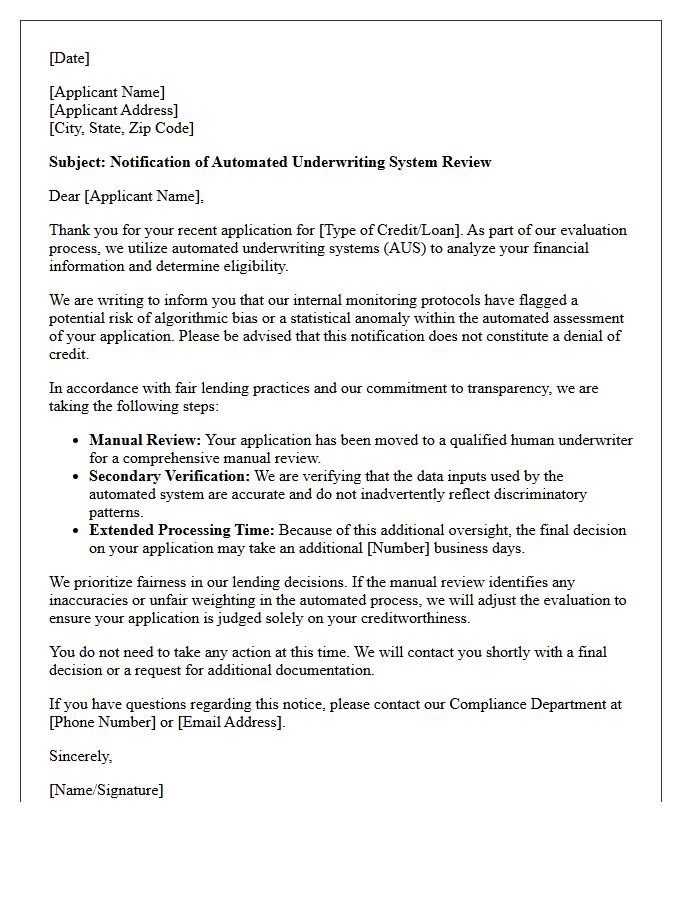

Automated Underwriting Bias Warning Letter

An Automated Underwriting Bias Warning Letter is a formal notification issued by regulators to financial institutions regarding discriminatory patterns in algorithmic loan processing. These letters highlight risks where artificial intelligence inadvertently favors specific demographics, leading to potential violations of fair lending laws. Lenders must act quickly to audit their automated systems and ensure mathematical models do not perpetuate systemic exclusion. Failure to address these warnings can result in severe legal penalties and reputational damage. Continuous compliance monitoring is essential to mitigate unintended algorithmic bias and maintain equitable access to credit for all applicants.

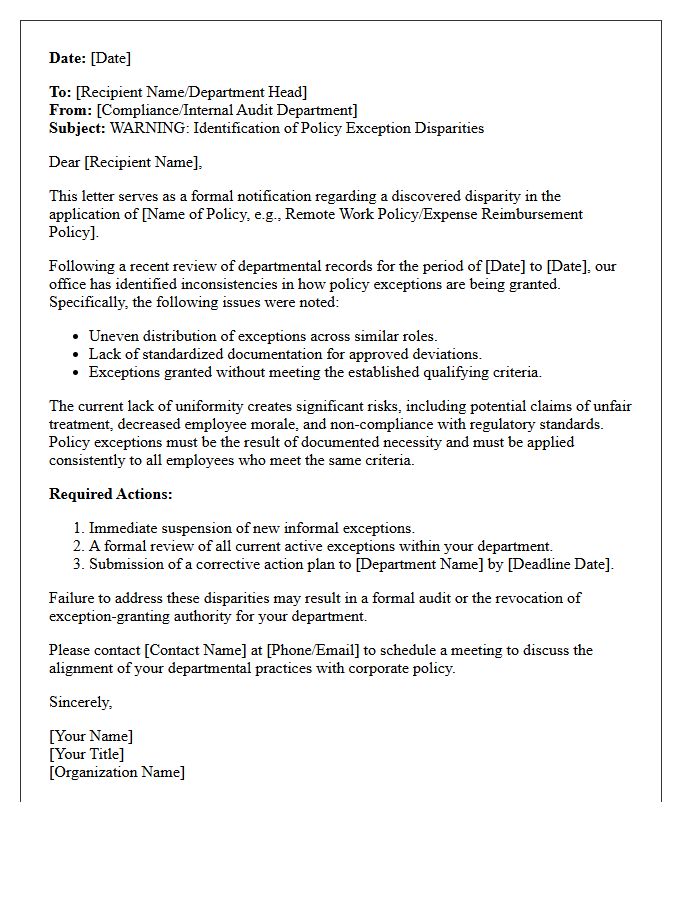

Policy Exception Disparity Warning Letter

A Policy Exception Disparity Warning Letter is a formal notification issued when internal audits reveal inconsistent application of corporate rules. It highlights a compliance gap where certain individuals or departments receive preferential treatment, creating operational risks. This document serves as a critical risk mitigation tool to prevent potential legal action or discrimination claims. Organizations use these warnings to enforce standardized procedural integrity and ensure that all policy deviations are documented, justified, and applied uniformly across the entire workforce to maintain institutional fairness and transparency.

What is a Fair Lending Compliance Warning Letter?

A Fair Lending Compliance Warning Letter is an official notification issued by regulatory bodies, such as the CFPB or DOJ, advising a financial institution that their lending data shows patterns of potential discrimination or significant deviations from fair lending standards. It serves as a formal alert for the institution to investigate and remediate issues before formal enforcement action or litigation occurs.

What triggers a fair lending warning letter from regulators?

Warning letters are typically triggered by statistical outliers found in HMDA data analysis, such as significant disparities in loan denial rates, pricing, or marketing reach across protected classes. Other triggers include whistleblower complaints, evidence of "redlining" in specific geographic areas, or discrepancies found during routine compliance examinations.

How should a financial institution respond to a fair lending warning?

Institutions should immediately conduct a privileged internal audit or comparative file review to identify the root cause of the flagged disparities. The response should involve legal counsel and include a detailed explanation of non-discriminatory business justifications, a plan for corrective action, and evidence of enhanced compliance monitoring systems.

What are the consequences of ignoring a fair lending compliance alert?

Ignoring a warning letter can lead to formal administrative enforcement actions, heavy civil money penalties, mandatory restitution to affected borrowers, and significant reputational damage. Furthermore, it may result in the denial of future merger and acquisition applications due to a poor Community Reinvestment Act (CRA) or compliance rating.

How can lenders prevent receiving fair lending violation notices?

Lenders can prevent violations by implementing a robust Fair Lending Management System (CMS) that includes regular statistical monitoring of loan portfolios, comprehensive staff training on ECOA and FHA regulations, and periodic "mystery shopping" or matched-pair testing to ensure consistent treatment of all applicants.

Comments