A Notice of Deficiency, or "90-day letter," is a critical legal document issued by the IRS proposing additional taxes. It serves as your formal opportunity to dispute the findings in Tax Court before paying the balance. Understanding your deadlines is essential to protecting your taxpayer rights. To help you respond effectively, below are some ready to use template.

Image cover: Official IRS Notice of Deficiency Templates and Response Samples

Letter Samples List

- Loan Application Documentation Deficiency Letter

- Know Your Customer Information Deficiency Letter

- Collateral Insurance Coverage Deficiency Letter

- Mortgage Underwriting Requirement Deficiency Letter

- Corporate Account Opening Deficiency Letter

- Regulatory Compliance Audit Deficiency Letter

- Escrow Account Balance Deficiency Letter

- Credit Card Application Income Deficiency Letter

- Commercial Loan Financial Statement Deficiency Letter

- Trust Account Documentation Deficiency Letter

- Margin Account Maintenance Deficiency Letter

- Loan Guarantor Signature Deficiency Letter

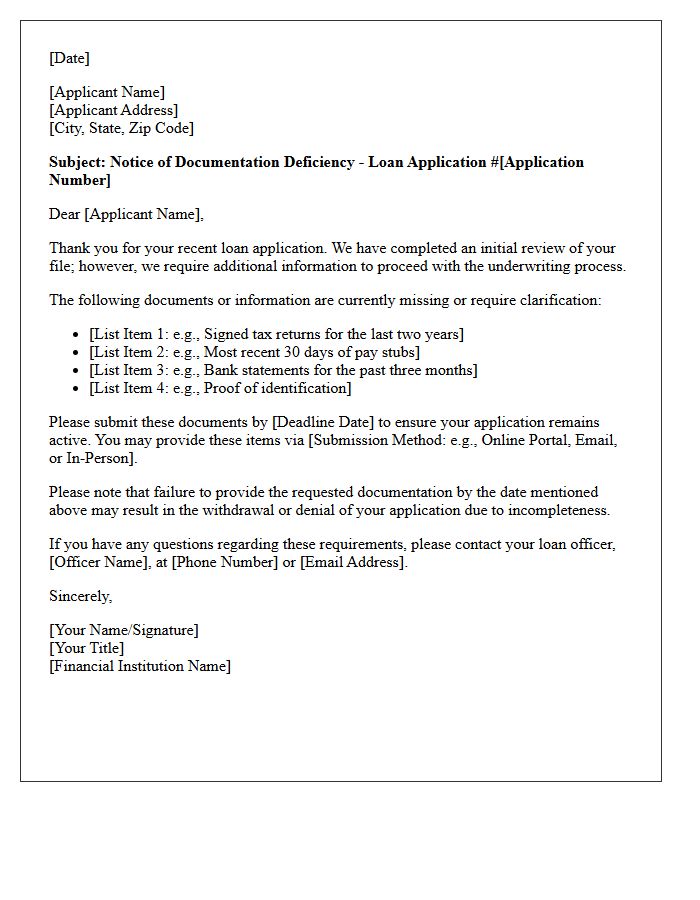

Loan Application Documentation Deficiency Letter

A Loan Application Documentation Deficiency Letter is a formal notice issued by lenders when a submission lacks required paperwork. This document identifies specific missing information, such as tax returns, bank statements, or identification, which prevents the underwriting process from moving forward. Timely resolution is critical, as failing to provide the requested items within the stated deadline may result in a denial or application cancellation. Efficiently addressing these gaps ensures the credit evaluation continues and improves your chances of securing timely financial approval.

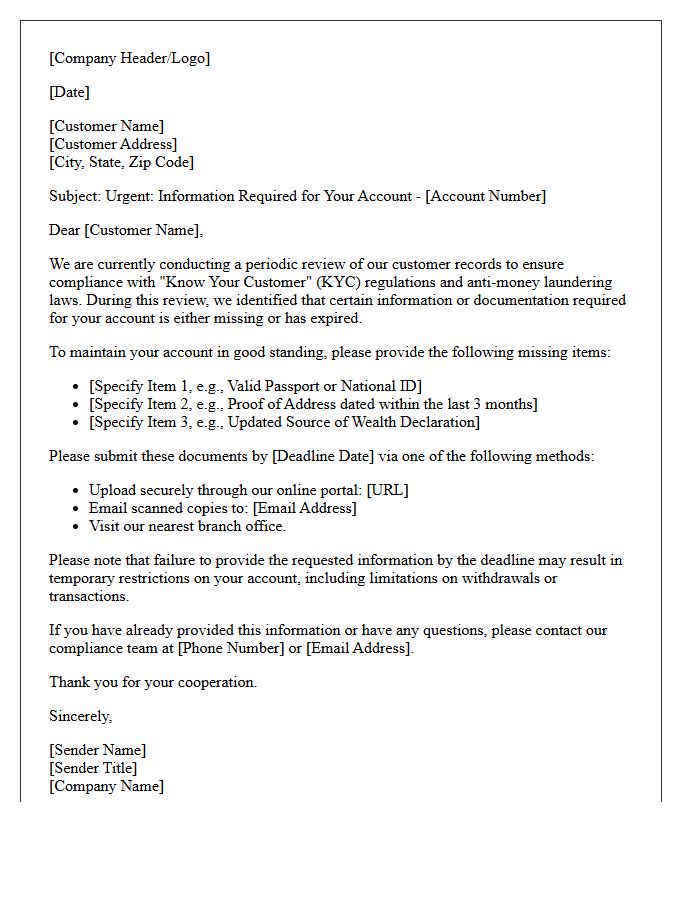

Know Your Customer Information Deficiency Letter

A Know Your Customer Information Deficiency Letter is a formal notice issued by financial institutions when submitted identity verification documents are incomplete, expired, or inconsistent. This critical compliance request identifies specific gaps in Anti-Money Laundering (AML) documentation required to verify a client's profile. Failure to resolve these discrepancies promptly can lead to account restrictions, transaction freezes, or service termination. It is essential to provide the requested verified data immediately to maintain regulatory standing and ensure uninterrupted access to financial services while preventing potential identity fraud risks.

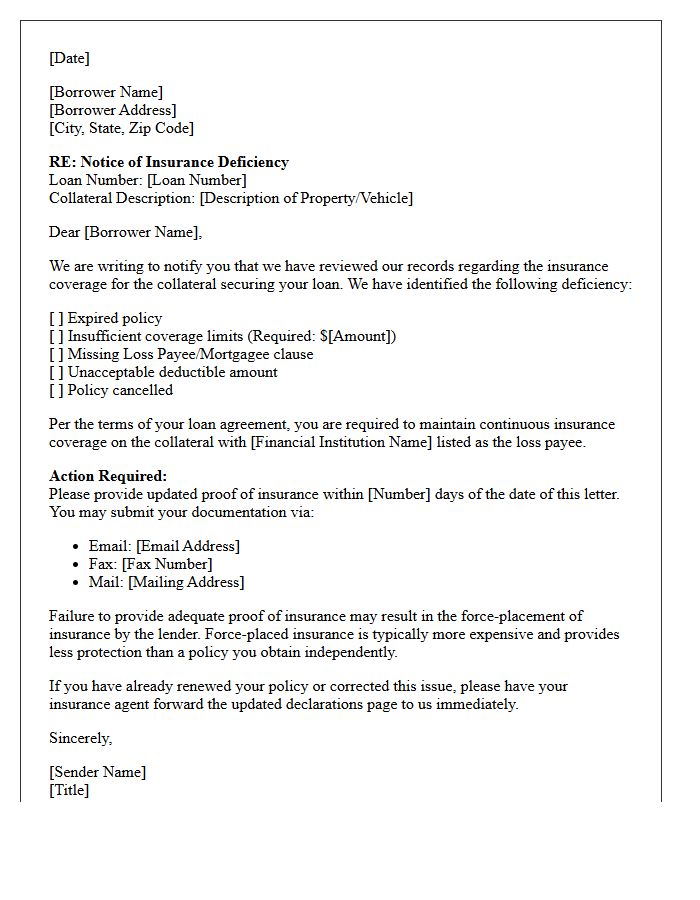

Collateral Insurance Coverage Deficiency Letter

A Collateral Insurance Coverage Deficiency Letter is a formal notice from a lender stating that your current insurance policy fails to meet the specific loan requirements. This typically occurs due to expired policies, inadequate coverage limits, or missing endorsements. If you receive this, you must provide updated proof of insurance immediately. Failure to rectify the deficiency may result in "force-placed insurance," where the lender purchases a policy at your expense, often at a much higher cost with fewer protections for your assets.

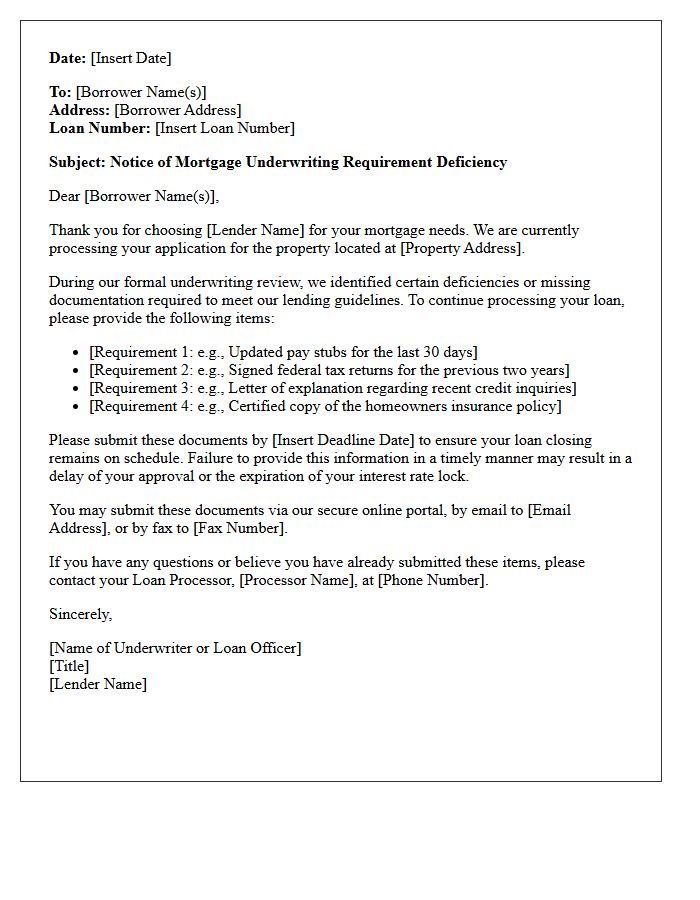

Mortgage Underwriting Requirement Deficiency Letter

A Mortgage Underwriting Requirement Deficiency Letter is a formal notification issued when a lender identifies missing documentation or eligibility issues during the loan evaluation. This document specifies stipulations that must be addressed before final approval. Common deficiencies include unverified income, credit discrepancies, or incomplete asset statements. Promptly providing the requested information is critical to prevent closing delays. Understanding these requirements helps borrowers resolve compliance gaps and ensures the mortgage meets strict secondary market standards for funding.

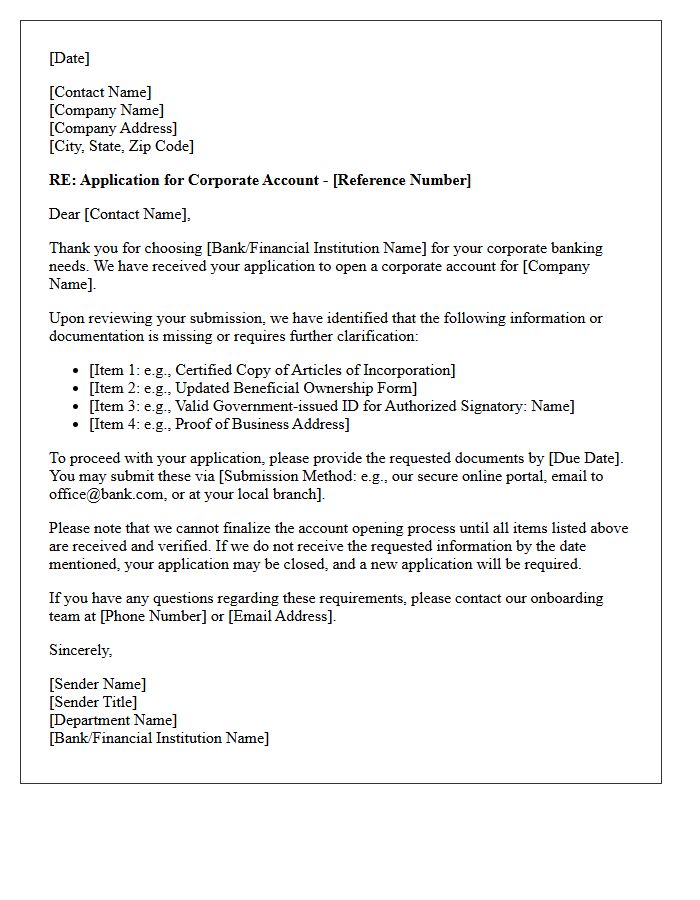

Corporate Account Opening Deficiency Letter

A Corporate Account Opening Deficiency Letter is a formal notification issued by a financial institution when an application is incomplete or non-compliant. This document identifies specific missing documentation or regulatory discrepancies that prevent account activation. Common issues include expired identification, unclear ultimate beneficial ownership (UBO) details, or incorrect corporate resolutions. Applicants must address these gaps promptly to ensure compliance with Know Your Customer (KYC) and Anti-Money Laundering (AML) standards. Failing to resolve these deficiencies will result in the application being rejected or significantly delayed.

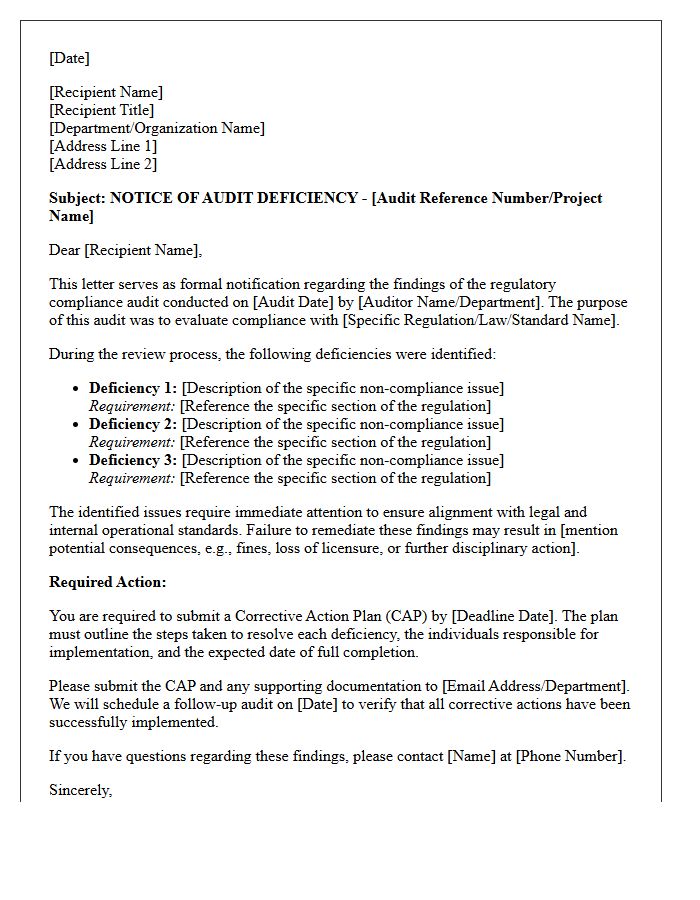

Regulatory Compliance Audit Deficiency Letter

A Regulatory Compliance Audit Deficiency Letter is an official notification issued by a governing body identifying failures to meet legal standards. Receiving this document signifies that your organization's internal controls or operational processes have been found lacking during an inspection. It is a critical warning that requires immediate attention and a formal corrective action plan. Addressing a Compliance Audit Deficiency promptly is essential to avoid severe consequences, including hefty fines, legal sanctions, or the loss of operating licenses. Transparency and rapid remediation are vital to restoring regulatory trust and ensuring long-term business continuity.

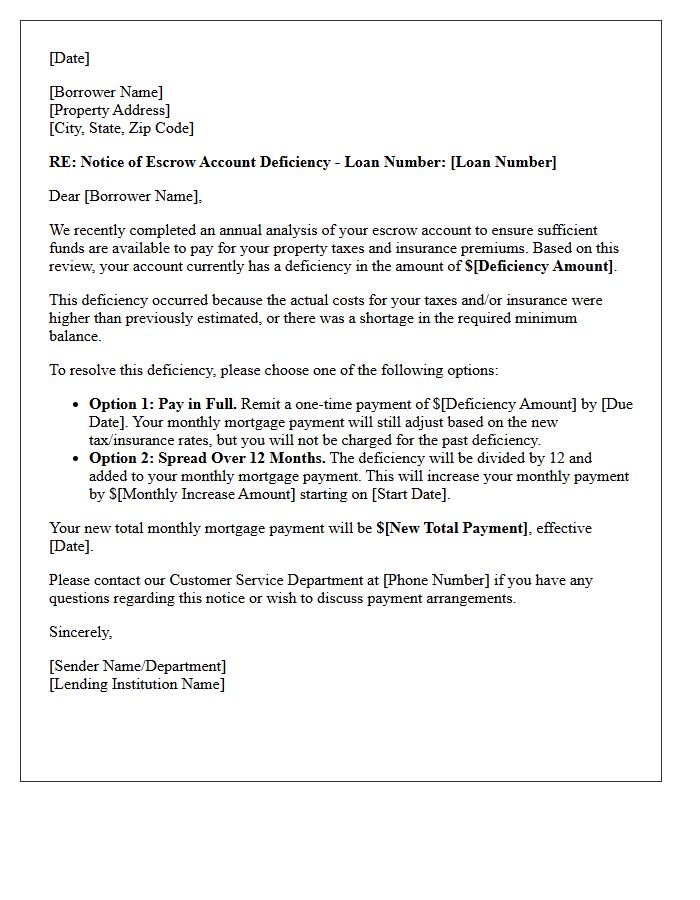

Escrow Account Balance Deficiency Letter

An Escrow Account Balance Deficiency Letter notifies homeowners that their property tax or insurance payments exceeded the funds available in their escrow account. This shortfall typically occurs due to rising tax assessments or insurance premiums. The notice outlines the total shortage amount and provides options for resolution. Borrowers can usually pay the full balance immediately or increase their monthly mortgage payment to spread the cost over the coming year. Timely action is essential to avoid significant monthly payment increases and ensure your loan remains in good standing.

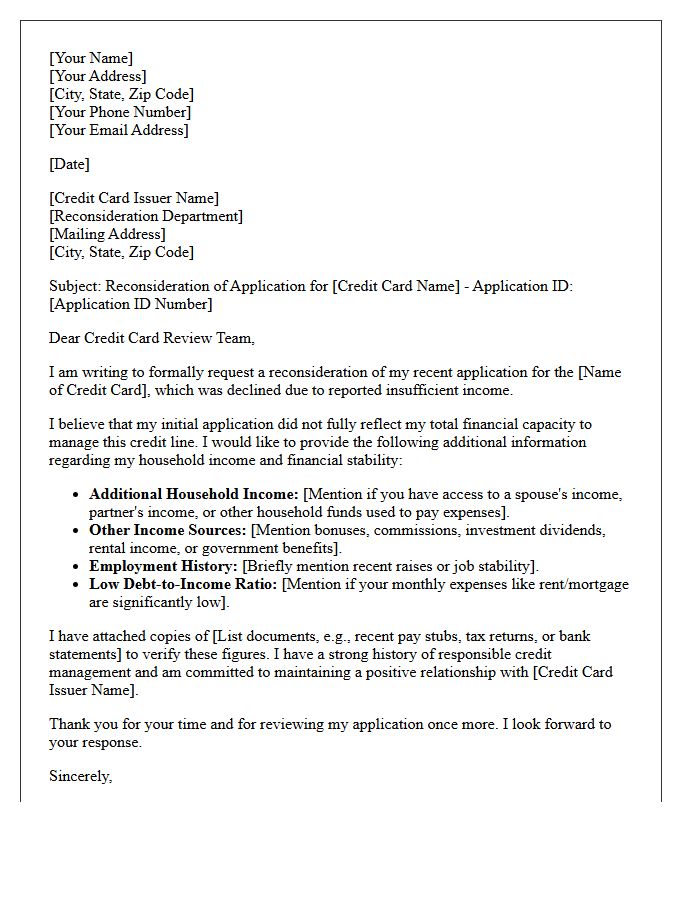

Credit Card Application Income Deficiency Letter

A Credit Card Application Income Deficiency Letter is a formal notice from a lender stating your reported earnings do not meet their specific underwriting requirements. Receiving this means your debt-to-income ratio or total salary was insufficient to guarantee repayment. To resolve this, you can provide supplemental proof of earnings, such as tax returns or side-hustle documentation. Alternatively, adding a co-signer or reducing existing debt can improve your eligibility. This letter is not a permanent ban but an invitation to clarify your financial capacity before a final decision is made.

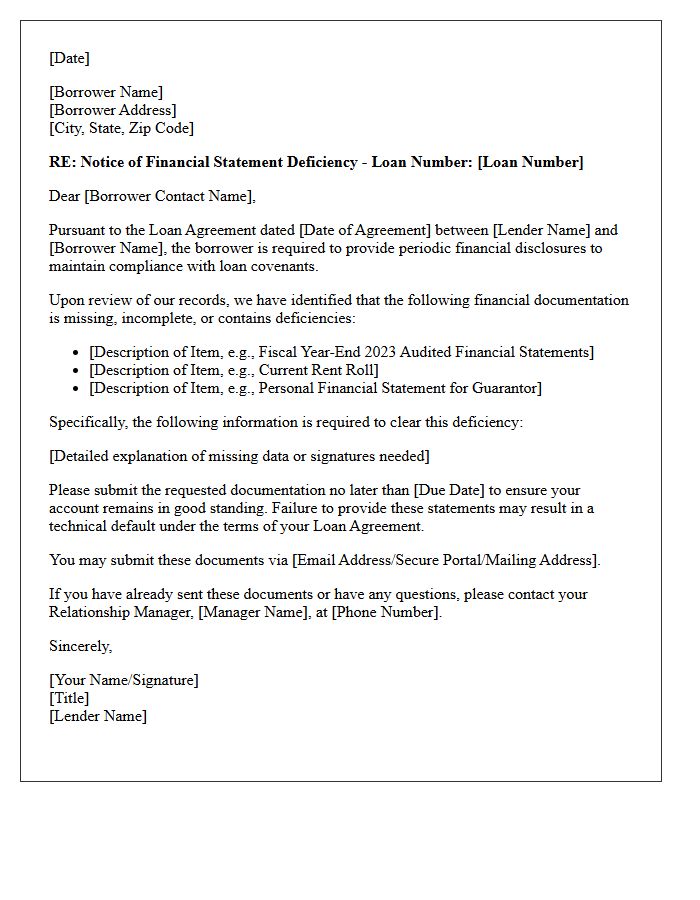

Commercial Loan Financial Statement Deficiency Letter

A Commercial Loan Financial Statement Deficiency Letter is a formal notice from a lender indicating that submitted documentation is incomplete or outdated. This letter highlights a financial reporting breach, which can technicaly trigger a loan default if not resolved. Borrowers must provide updated balance sheets, tax returns, or income statements within the specified cure period to maintain compliance. Promptly addressing these gaps is essential to preserve your credit relationship and ensure continued access to your commercial credit facility without facing penalties or accelerated repayment demands.

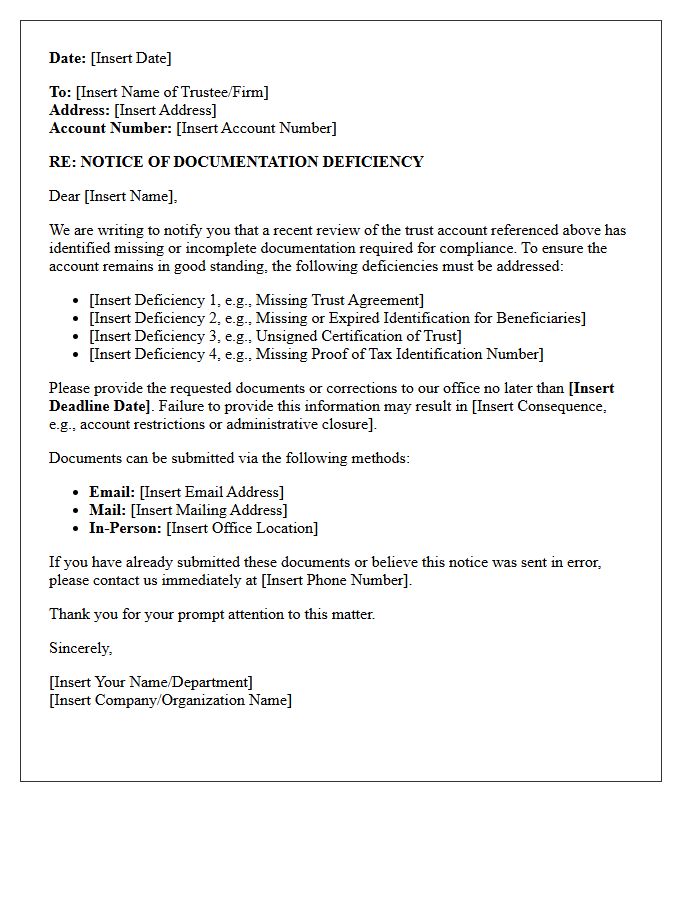

Trust Account Documentation Deficiency Letter

A Trust Account Documentation Deficiency Letter is a formal notice issued by regulatory bodies or auditors indicating that your fiduciary records fail to meet legal standards. Receiving this letter means your compliance documentation is incomplete, inaccurate, or missing essential reconciliation reports. It is critical to address these gaps immediately to prevent allegations of commingling or financial mismanagement. Rectifying the noted deficiencies through detailed ledgers and bank statements is mandatory to maintain your professional license and ensure the integrity of client funds held in trust.

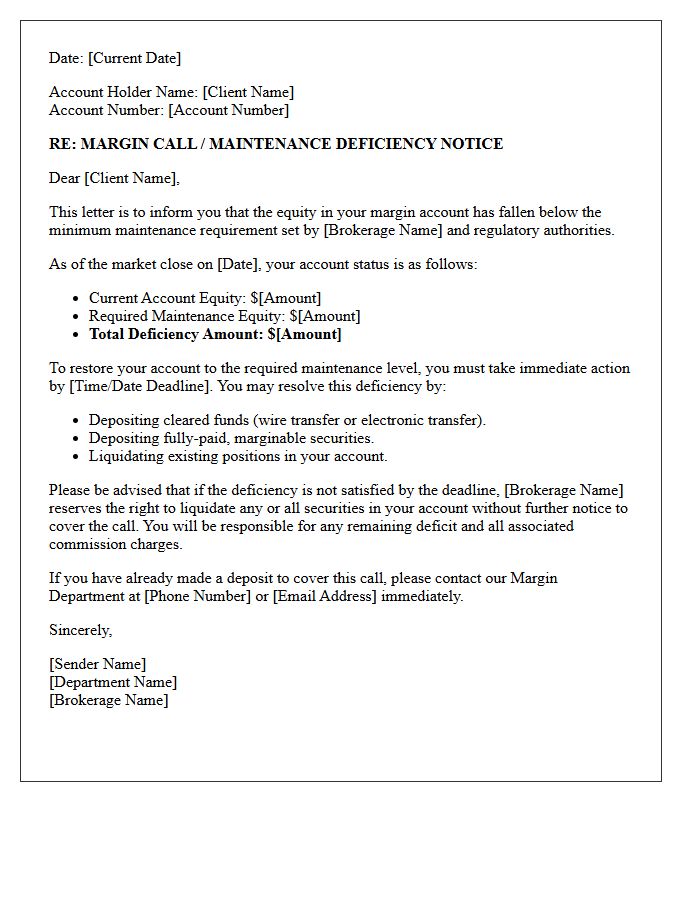

Margin Account Maintenance Deficiency Letter

A Margin Account Maintenance Deficiency Letter, commonly known as a margin call, is a formal notice issued by a brokerage when your account equity falls below the minimum regulatory or house requirement. This occurs due to market volatility or declining asset values. To resolve the deficiency, you must immediately deposit additional cash or marginable securities, or liquidate positions to increase your equity ratio. Failure to act promptly allows the broker to sell your assets without prior consent to cover the shortfall and mitigate financial risk.

Loan Guarantor Signature Deficiency Letter

A Loan Guarantor Signature Deficiency Letter is a formal notice issued by a lender when a legally binding signature is missing, incomplete, or incorrectly executed on guarantee documents. This document is critical because it identifies administrative errors that prevent the loan from being fully secured. To resolve the issue, the guarantor must promptly provide a valid signature to ensure the enforceability of the agreement. Ignoring this letter can delay funding or lead to a technical default, as the lender requires a complete guaranty agreement to mitigate financial risk.

What is an IRS Notice of Deficiency (90-Day Letter)?

An IRS Notice of Deficiency, also known as a 90-Day Letter or Statutory Notice of Deficiency, is a legal notification informing a taxpayer that the IRS has determined a tax shortfall. It outlines the proposed additional tax, penalties, and interest the agency believes you owe based on an audit or document matching.

What should I do if I receive a Notice of Deficiency?

Upon receiving the notice, you must either agree to the changes by signing and returning the enclosed form or challenge the findings by filing a petition with the U.S. Tax Court. You have exactly 90 days (150 days if addressed to a person outside the U.S.) from the date on the notice to file a petition if you disagree with the assessment.

Can I request an extension to file a petition with the Tax Court?

No, the 90-day deadline for filing a petition with the U.S. Tax Court is statutory and cannot be extended by the IRS. If you miss the deadline, you lose your right to challenge the deficiency in Tax Court without paying the tax first; your only remaining option would be to pay the full amount and file a refund suit in District Court or the Court of Federal Claims.

Does receiving a Notice of Deficiency mean I have to pay immediately?

No, the Notice of Deficiency is not a bill for immediate payment. It is a legal window that prevents the IRS from officially assessing the tax or initiating collection actions (like liens or levies) until the 90-day period expires or the Tax Court reaches a decision. However, interest will continue to accrue on any unpaid balance during this period.

What is the difference between a 30-Day Letter and a 90-Day Letter?

A 30-Day Letter is an initial notice sent after an audit offering you the chance to appeal within the IRS Office of Appeals. A 90-Day Letter (Notice of Deficiency) is the final legal notice sent if you do not respond to the 30-Day Letter or fail to reach an agreement with the appeals officer, providing your formal path to Tax Court.

Comments