Financial institutions must prioritize compliance with the Cybersecurity Posture Supervisory Letter to ensure operational resilience. This regulatory guidance outlines essential standards for risk management, threat detection, and data protection protocols. Strengthening your security framework is critical for maintaining trust and meeting examiner expectations. To assist your implementation, below are some ready to use template.

Image cover: Effective Cybersecurity Posture Supervisory Letter Templates and Samples

Letter Samples List

- Initial Cybersecurity Posture Supervisory Letter

- Incident Response Preparedness Supervisory Letter

- Third-Party Vendor Risk Management Supervisory Letter

- Cybersecurity Vulnerability Remediation Supervisory Letter

- Board Oversight and Cybersecurity Governance Letter

- Ransomware Threat Mitigation Supervisory Letter

- Annual Penetration Testing Posture Supervisory Letter

- Identity and Access Management Control Supervisory Letter

- Customer Data Protection and Privacy Supervisory Letter

- Cloud Infrastructure Security Posture Supervisory Letter

- Regulatory Compliance and Cybersecurity Posture Letter

- Business Continuity and Cyber Resilience Supervisory Letter

- Endpoint Detection and Network Security Supervisory Letter

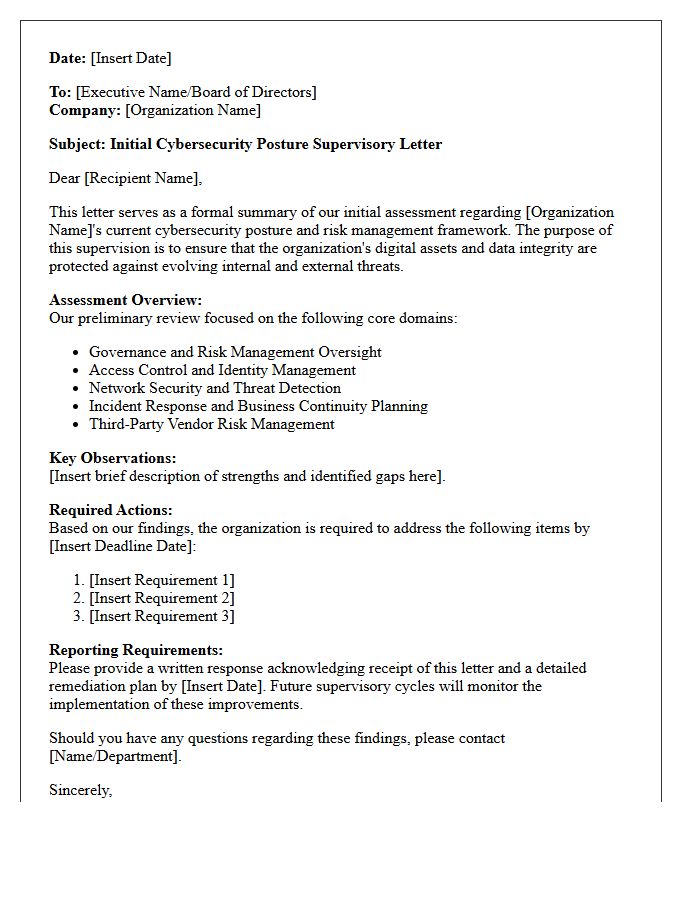

Initial Cybersecurity Posture Supervisory Letter

The Initial Cybersecurity Posture Supervisory Letter is a formal regulatory communication used by examiners to assess a firm's baseline security maturity. It outlines critical expectations regarding risk management, threat governance, and technical controls. Financial institutions must treat this document as a compliance roadmap, as it identifies gaps that require immediate remediation. Understanding these mandates is essential for maintaining operational resilience and ensuring alignment with supervisory standards during the examination process. Proactive response to these findings helps mitigate legal risks and strengthens overall data protection protocols.

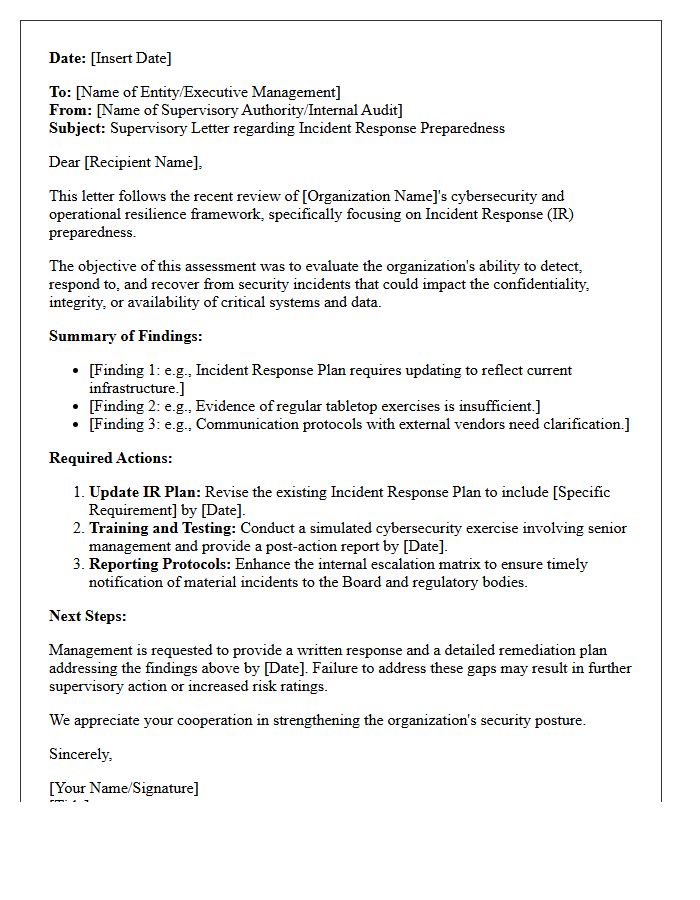

Incident Response Preparedness Supervisory Letter

The Incident Response Preparedness Supervisory Letter provides critical guidance for financial institutions to enhance their cyber resilience. Issued by regulators, it emphasizes the importance of a robust framework to detect, contain, and recover from security breaches. Banks must maintain updated response plans, conduct regular tabletop exercises, and ensure clear communication protocols with stakeholders. Effective implementation ensures compliance with safety and soundness standards while minimizing operational disruptions. Management is expected to oversee these strategies to mitigate evolving cybersecurity risks and protect sensitive consumer data from sophisticated threats.

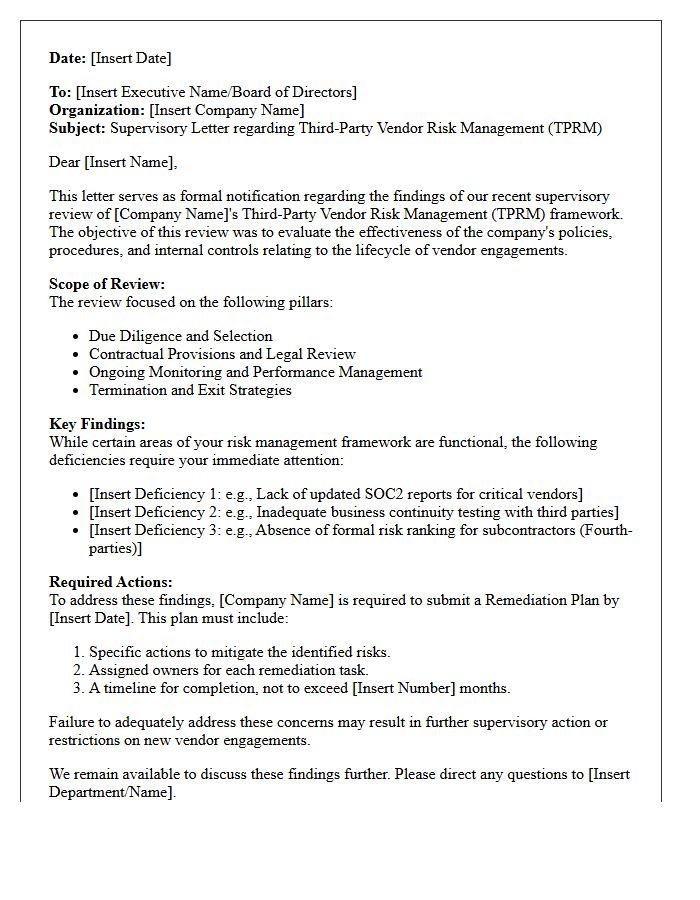

Third-Party Vendor Risk Management Supervisory Letter

The Third-Party Vendor Risk Management Supervisory Letter outlines critical expectations for financial institutions to manage external partnerships. This guidance emphasizes that outsourcing services does not diminish a board's responsibility to maintain safety and soundness. Key requirements include conducting due diligence, continuous monitoring, and establishing robust contingency plans. Regulators focus on identifying and mitigating operational, compliance, and strategic risks associated with vendors. Effective oversight ensures that third-party relationships remain resilient, protecting the institution from financial loss and reputational damage while maintaining regulatory compliance throughout the entire lifecycle of the contract.

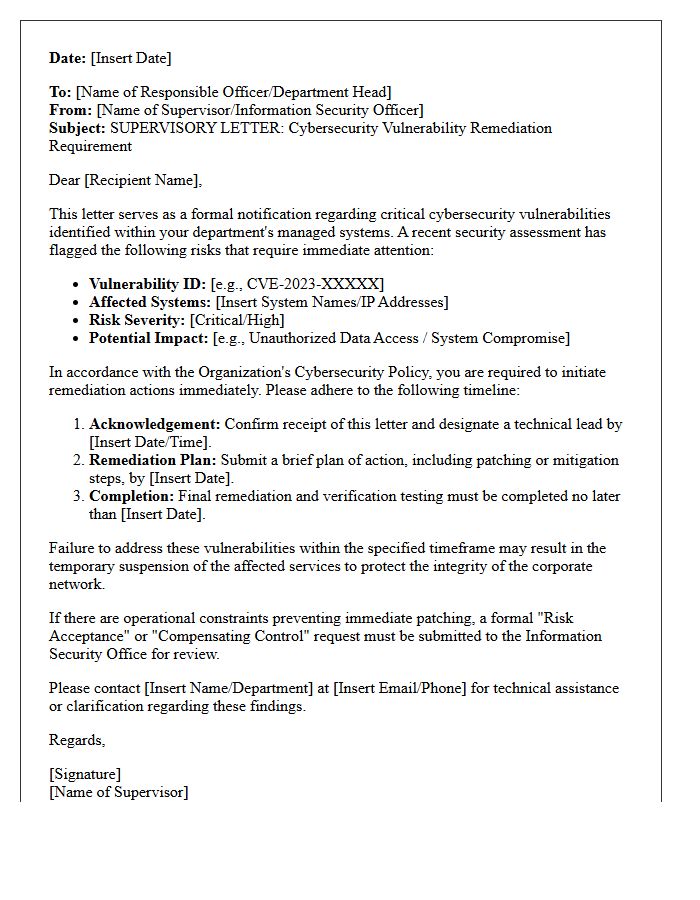

Cybersecurity Vulnerability Remediation Supervisory Letter

The Cybersecurity Vulnerability Remediation Supervisory Letter, issued by the Federal Reserve, establishes rigorous expectations for financial institutions. It emphasizes that risk-based prioritization is essential for managing security flaws. Banks must implement formal processes to identify, assess, and patch vulnerabilities within specific timeframes. The letter highlights that remediation delays must be documented and approved by management. Failure to address these gaps can lead to significant operational risks and regulatory enforcement actions. Compliance ensures that critical systems remain resilient against evolving cyber threats and unauthorized access attempts.

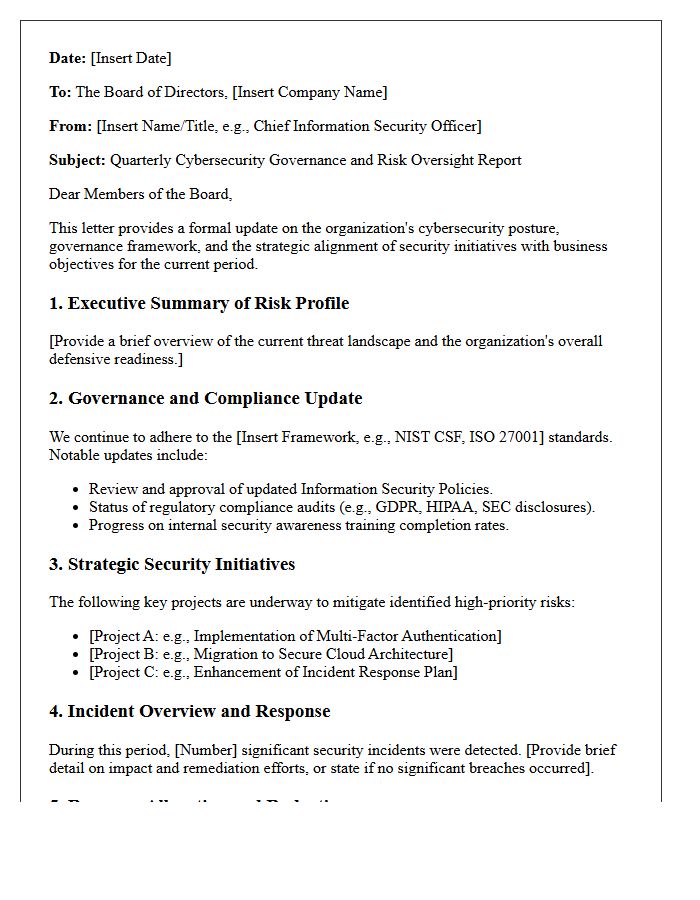

Board Oversight and Cybersecurity Governance Letter

A Board Oversight and Cybersecurity Governance Letter is a critical document that outlines how a company's directors manage digital risk. It demonstrates accountability by defining roles, reporting structures, and strategic alignment with security goals. This letter assures stakeholders that the board actively monitors threats, resource allocation, and regulatory compliance. Effective governance ensures that cybersecurity is treated as a core business priority rather than just a technical issue, fostering resilience and protecting long-term corporate value against evolving cyber threats and potential data breaches.

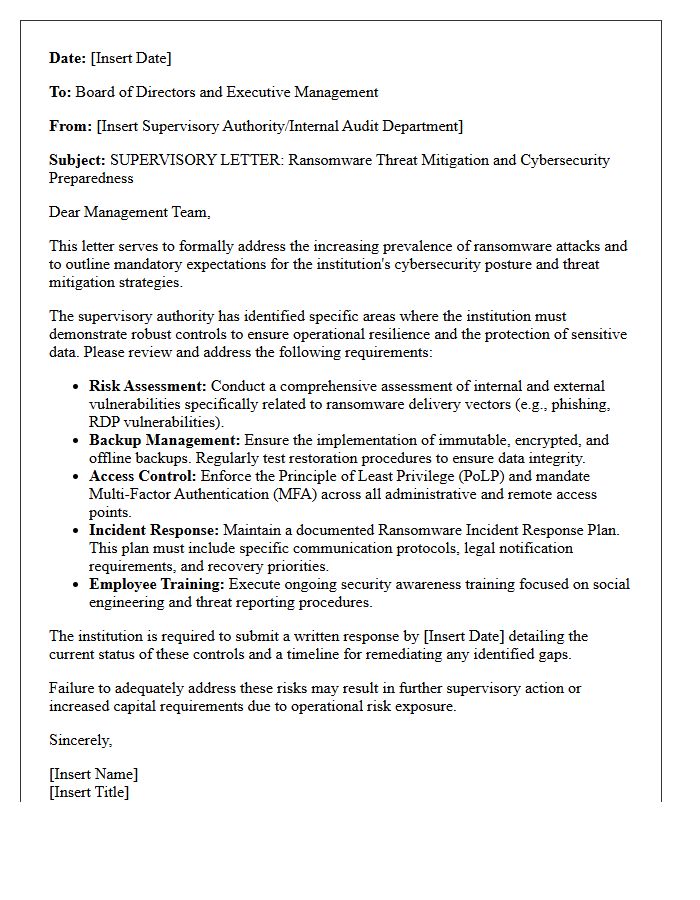

Ransomware Threat Mitigation Supervisory Letter

The Ransomware Threat Mitigation Supervisory Letter outlines critical expectations for credit unions to enhance cyber resilience. It emphasizes the necessity of robust incident response plans, regular data backups, and employee training to combat evolving digital threats. National Credit Union Administration (NCUA) examiners use this guidance to evaluate internal controls and security protocols. Financial institutions must prioritize proactive defense strategies and vulnerability management to protect sensitive member information and ensure operational continuity against sophisticated extortion attacks. Compliance ensures adherence to federal safety and soundness standards in an increasingly hostile cybersecurity landscape.

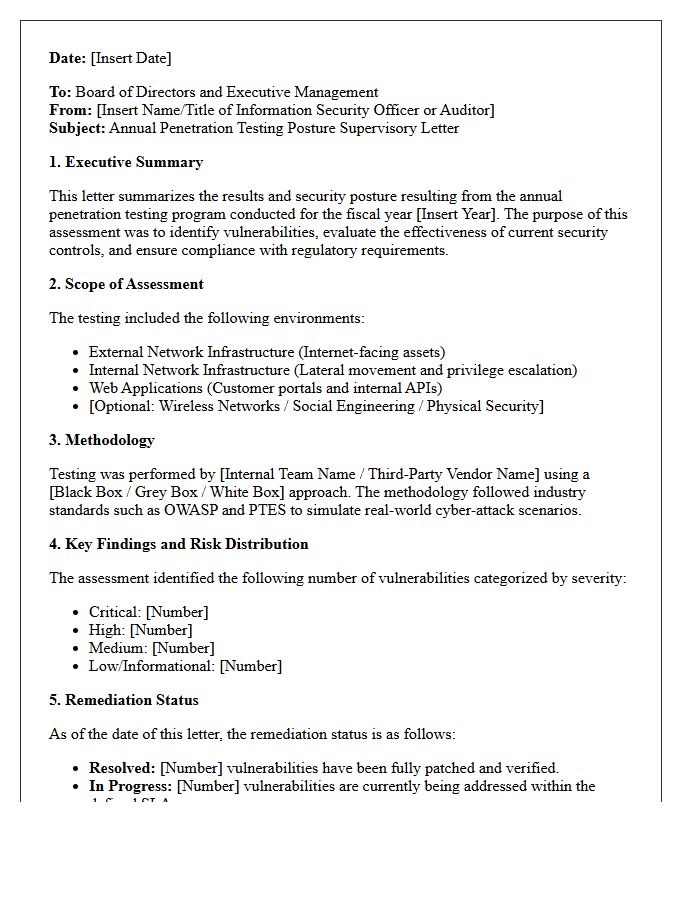

Annual Penetration Testing Posture Supervisory Letter

The Annual Penetration Testing Posture Supervisory Letter is a critical regulatory communication used by financial examiners to assess a firm's cybersecurity resilience. It summarizes findings from security assessments, highlighting vulnerabilities and risk management gaps. Financial institutions must review this letter to ensure compliance with regulatory standards and prioritize the remediation of identified threats. This document serves as a benchmark for your security posture, guiding strategic investments to protect sensitive data and maintain systemic stability against evolving cyber attacks.

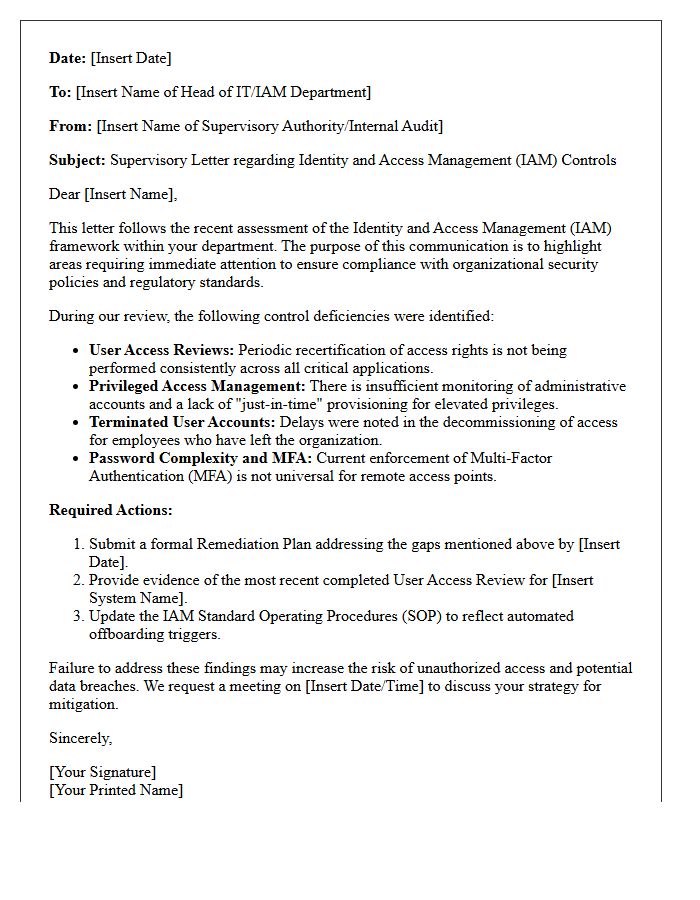

Identity and Access Management Control Supervisory Letter

The Identity and Access Management Control Supervisory Letter outlines critical regulatory expectations for financial institutions regarding user authentication and data protection. It emphasizes that robust identity governance is essential for mitigating cybersecurity risks, such as unauthorized access and insider threats. Examiners focus on the implementation of Multi-Factor Authentication, the principle of least privilege, and regular access reviews. Organizations must maintain comprehensive audit trails and enforce strict lifecycle management for all user credentials to ensure compliance with federal safety and soundness standards while preventing potential data breaches.

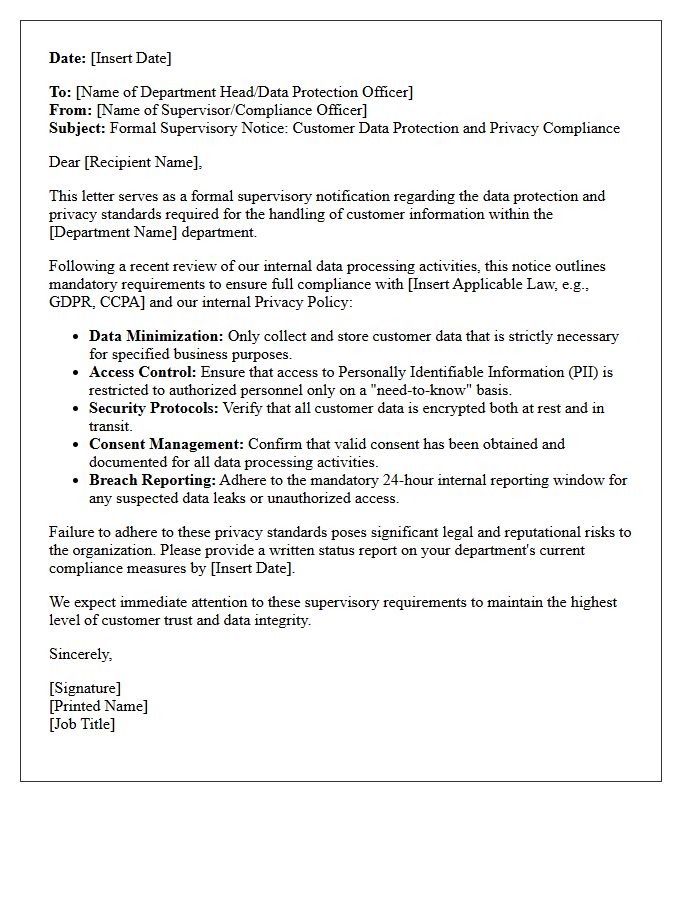

Customer Data Protection and Privacy Supervisory Letter

The Customer Data Protection and Privacy Supervisory Letter outlines critical regulatory expectations for financial institutions regarding sensitive information. It emphasizes that compliance requires robust governance frameworks to prevent unauthorized access and data breaches. Organizations must implement strict internal controls, regular risk assessments, and comprehensive employee training. Failure to adhere to these privacy standards can lead to severe legal penalties and reputational damage. Prioritizing data security ensures that consumer trust is maintained while meeting the evolving legal requirements set by supervisory authorities in an increasingly digital financial landscape.

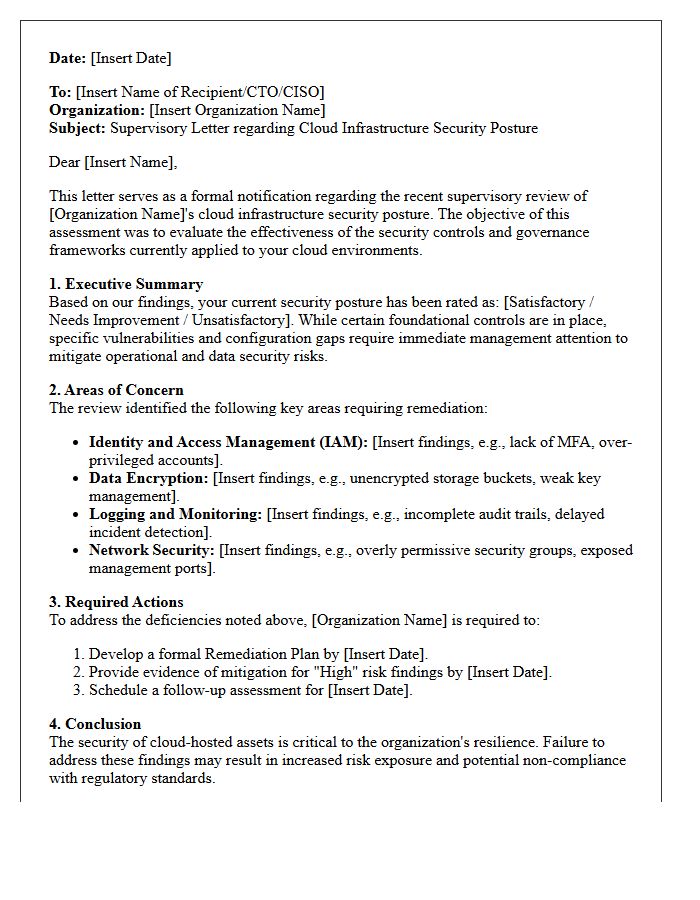

Cloud Infrastructure Security Posture Supervisory Letter

The Cloud Infrastructure Security Posture Supervisory Letter is a regulatory guidance issued by the Federal Reserve to address risks in banking cloud environments. It emphasizes that financial institutions must maintain robust governance and oversight when using third-party services. Key focus areas include misconfiguration management, identity access controls, and continuous monitoring. This letter underscores that while infrastructure is outsourced, accountability for data security and operational resilience remains with the organization. Proactive compliance ensures banks mitigate vulnerabilities within complex, scalable cloud architectures while meeting federal safety and soundness standards.

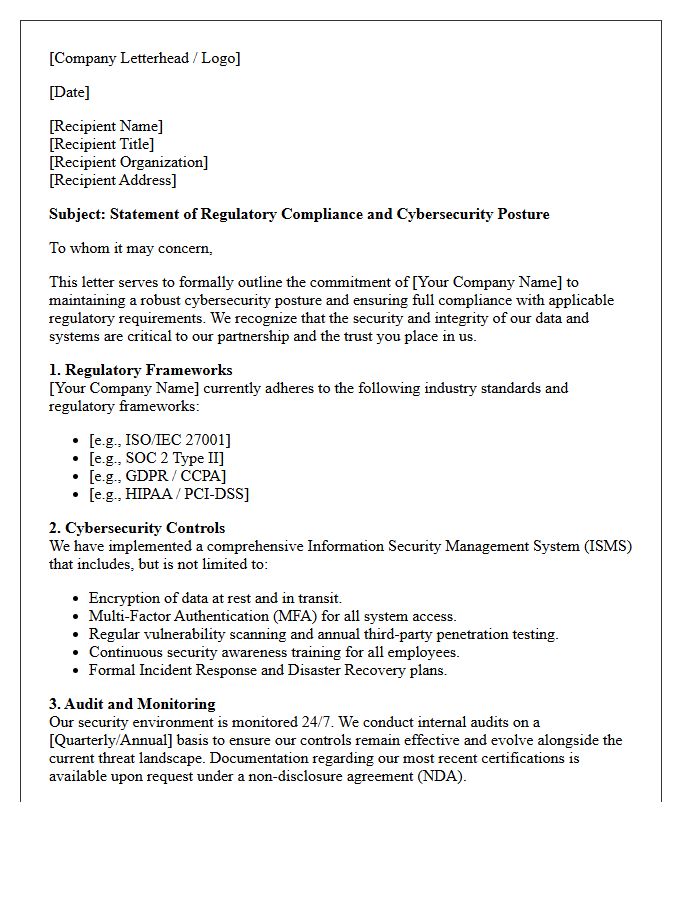

Regulatory Compliance and Cybersecurity Posture Letter

A Regulatory Compliance and Cybersecurity Posture Letter is a formal document verifying that an organization adheres to specific security standards and legal mandates. It provides stakeholders with assurance regarding the effectiveness of internal controls and risk management strategies. This letter acts as a bridge of trust, summarizing complex audit results to demonstrate a proactive cybersecurity posture. By validating compliance with frameworks like GDPR or HIPAA, it helps mitigate liability and simplifies the due diligence process during business partnerships or vendor assessments.

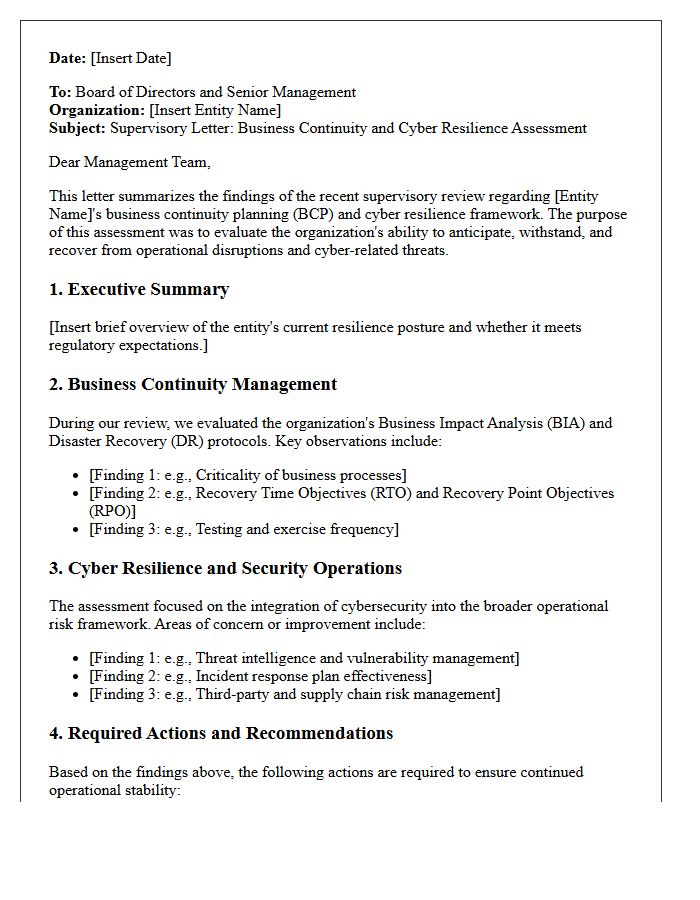

Business Continuity and Cyber Resilience Supervisory Letter

The Business Continuity and Cyber Resilience Supervisory Letter establishes critical regulatory expectations for financial institutions. It emphasizes operational resilience by requiring firms to maintain robust strategies against systemic disruptions. Boards must ensure comprehensive risk management frameworks that address data integrity, cybersecurity threats, and third-party dependencies. This guidance mandates rigorous testing of recovery capabilities to safeguard essential services. Compliance ensures that organizations can anticipate, withstand, and rapidly recover from significant cyber incidents, maintaining stability within the broader financial ecosystem through proactive governance and mitigation protocols.

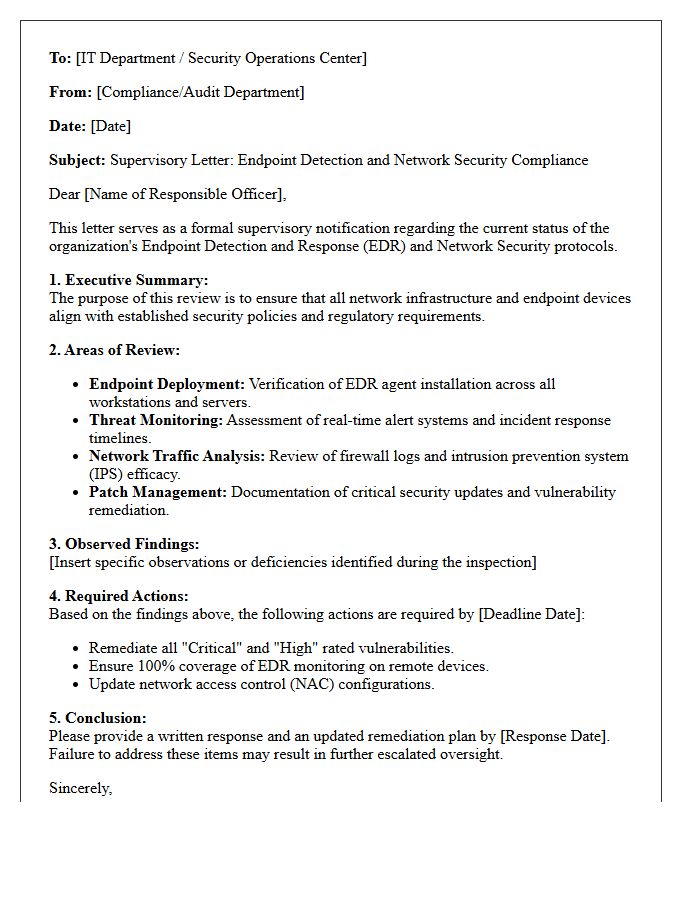

Endpoint Detection and Network Security Supervisory Letter

The Endpoint Detection and Network Security Supervisory Letter issued by the NCUA emphasizes that credit unions must implement robust monitoring to combat evolving cyber threats. It highlights the necessity of Endpoint Detection and Response (EDR) solutions to identify and mitigate malware at the device level. Additionally, credit unions are expected to maintain persistent network visibility and logging to ensure rapid incident detection. Compliance requires aligning security frameworks with established standards to protect sensitive member data and ensure operational resilience against sophisticated cybersecurity attacks within the financial sector.

What is a Cybersecurity Posture Supervisory Letter?

A Cybersecurity Posture Supervisory Letter is an official communication issued by regulatory bodies to financial institutions or supervised entities, detailing specific deficiencies, risks, or required improvements identified during a cybersecurity examination or assessment.

What are the primary objectives of a supervisory letter regarding cybersecurity?

The primary objectives are to ensure the entity maintains operational resilience, protects sensitive consumer data, complies with cybersecurity frameworks (such as NIST or FFIEC), and addresses identified vulnerabilities that could threaten the stability of the financial system.

How should an organization respond to a Cybersecurity Posture Supervisory Letter?

Organizations must provide a formal written response within a specific timeframe, typically including a detailed remediation plan, clear milestones, assigned accountability, and evidence of how they intend to mitigate the findings noted by the regulator.

What are the common findings addressed in cybersecurity supervisory communications?

Common findings include inadequate identity and access management (IAM), insufficient incident response planning, lack of board-level oversight of cyber risks, outdated patch management protocols, and ineffective third-party vendor risk management programs.

What are the consequences of failing to address a Cybersecurity Posture Supervisory Letter?

Failure to remediate the identified issues can lead to escalated regulatory actions, including formal enforcement orders, monetary fines, increased capital requirements, and restrictions on business activities or future acquisitions.

Comments