A Return to Original Creditor Closure Notice is a formal document sent to a debt collection agency when they no longer have the authority to collect a debt. This notice confirms the account has been returned to the primary lender, effectively stopping third-party collection efforts. Understanding this process protects your consumer rights and ensures accurate financial records. Below are some ready to use templates.

Image cover: Formal Closure Notice Templates for Debts Returned to Original Creditors

Letter Samples List

- Standard Account Closure And Return To Original Creditor Letter

- Bankruptcy Notice And Return To Original Creditor Closure Letter

- Cease And Desist Return To Original Creditor Closure Letter

- Deceased Debtor Return To Original Creditor Closure Letter

- Identity Theft And Fraud Return To Original Creditor Closure Letter

- Expired Statute Of Limitations Return To Original Creditor Letter

- Voluntary Creditor Recall And Account Closure Letter

- Direct Creditor Payment Account Closure And Return Letter

- Unverified Dispute Return To Original Creditor Closure Letter

- Exhausted Collection Efforts Return To Original Creditor Letter

- Pending Litigation Return To Original Creditor Closure Letter

- Direct Creditor Settlement Account Closure Letter

- Unable To Locate Return To Original Creditor Closure Letter

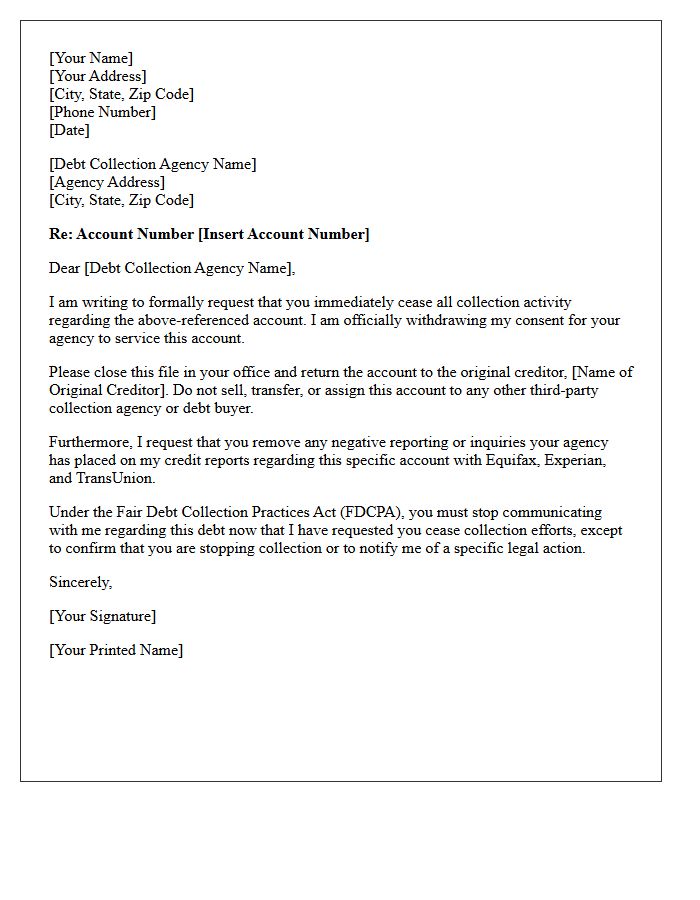

Standard Account Closure And Return To Original Creditor Letter

A Standard Account Closure And Return To Original Creditor Letter is a formal request sent to a collection agency. It demands they stop collection efforts and return the debt file to the original creditor. This strategy is essential for debt validation and regaining the ability to negotiate directly with the primary lender. By revoking the agency's authority, you can often secure better settlement terms or prevent further credit damage. Sending this letter via certified mail ensures a legal record of your request to terminate the third-party collection process effectively.

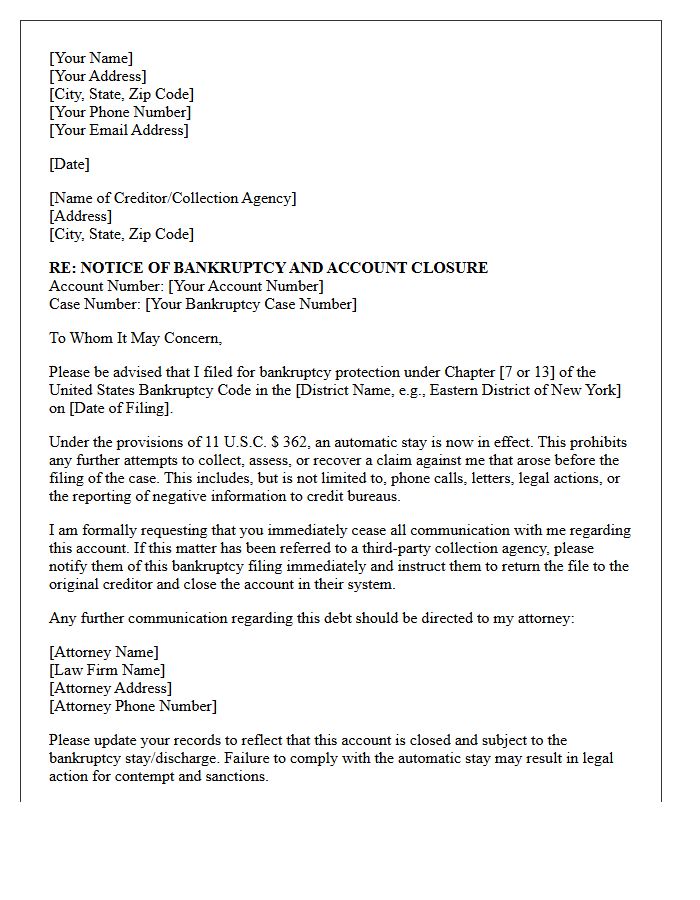

Bankruptcy Notice And Return To Original Creditor Closure Letter

A Bankruptcy Notice legally halts collection activities through an automatic stay. If you receive a Return to Original Creditor Closure Letter, it signifies that a third-party agency has ceased collections and transferred the account balance back to the initial lender. This occurs because bankruptcy discharges the debt or voids the collection contract. Always verify your credit report to ensure the status reflects "included in bankruptcy" with a zero balance, preventing future zombie debt attempts by secondary collectors after the case closes.

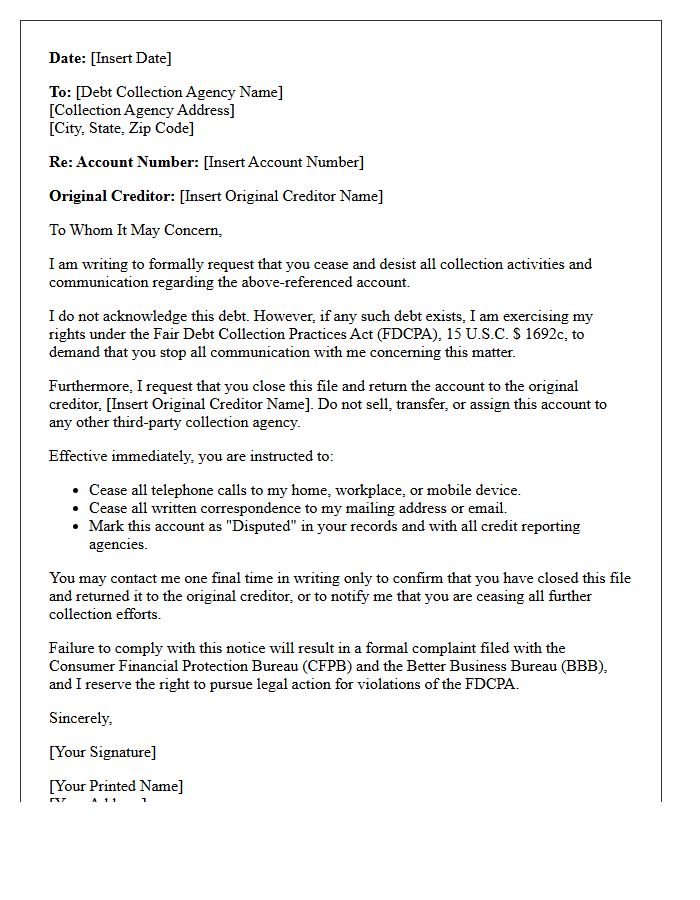

Cease And Desist Return To Original Creditor Closure Letter

A Cease and Desist letter sent to a third-party debt collector effectively revokes their right to contact you. When combined with a Return to Original Creditor request, it demands the agency stop collection activities and return the account to the entity you originally owed. This strategy is vital for account closure with agencies, forcing the debt back to the source. This allows you to negotiate directly with the original creditor or address reporting errors, potentially preventing further harassment while maintaining a clear paper trail for legal protection.

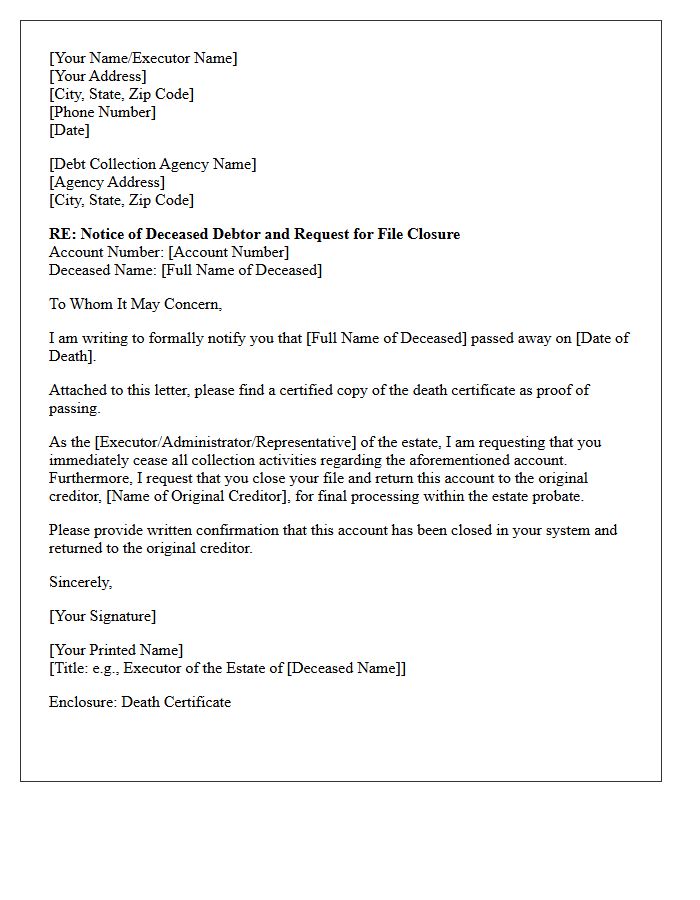

Deceased Debtor Return To Original Creditor Closure Letter

A Deceased Debtor Return To Original Creditor Closure Letter is a formal notification sent by an executor or estate representative to a third-party collection agency. This document informs the agency that the debtor has passed away and demands the account be returned to the original creditor for final probate settlement. Providing a certified death certificate is essential to ensure the closure of collection activities. This process prevents further harassment of grieving relatives and ensures the estate manages all remaining liabilities according to legal priority and state inheritance laws.

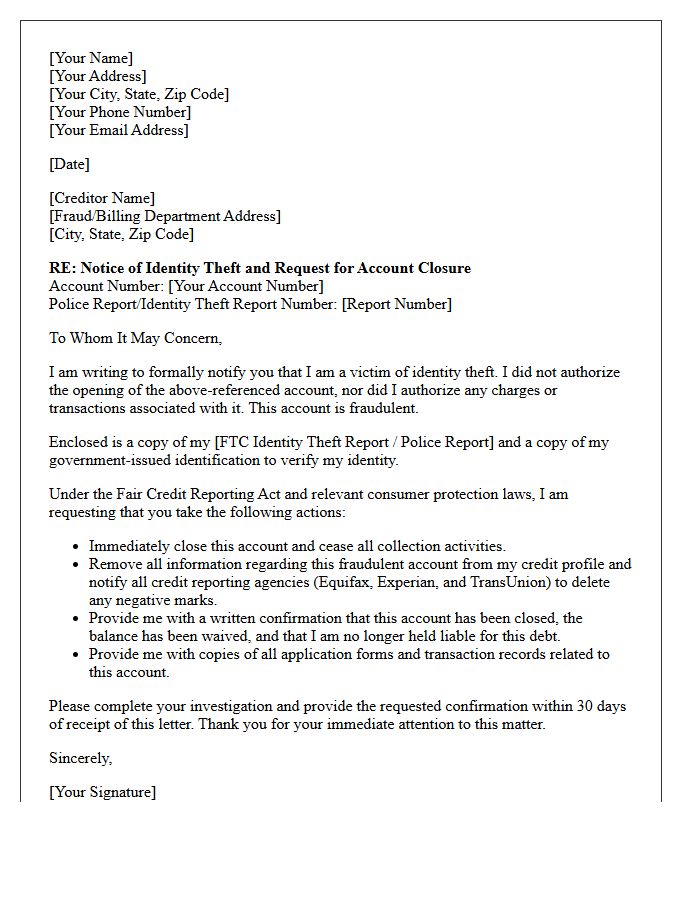

Identity Theft And Fraud Return To Original Creditor Closure Letter

An Identity Theft and Fraud Return to Original Creditor Closure Letter is a formal legal notice sent to businesses to dispute unauthorized accounts. This document informs the creditor that a debt resulted from fraudulent activity rather than your own spending. It demands an immediate account closure, a cessation of collection efforts, and the removal of negative marks from your credit report. Providing a police report or FTC affidavit alongside this letter ensures federal compliance under the Fair Credit Reporting Act, protecting your financial reputation from further damage.

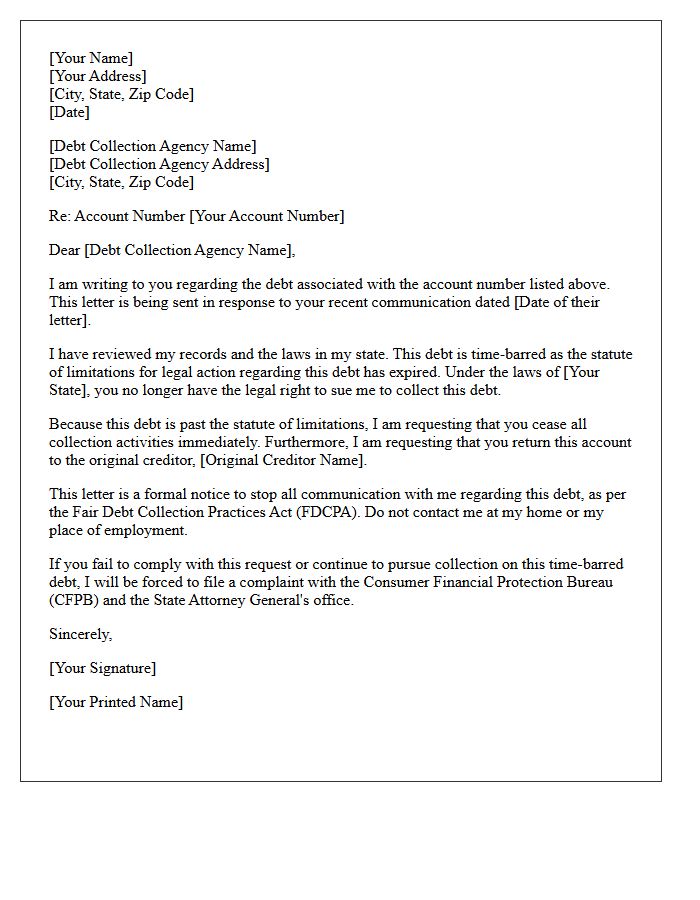

Expired Statute Of Limitations Return To Original Creditor Letter

An Expired Statute of Limitations letter notifies a debt collector that the legal timeframe to sue for a debt has passed. When you send this Return to Original Creditor notice, you effectively demand that the collection agency cease all contact and return the file to the original creditor. This action prevents further third-party harassment and asserts your consumer rights under the FDCPA. Always verify your state's specific statutory limits before mailing, as making a payment or acknowledging the debt could inadvertently restart the legal clock on an expired account.

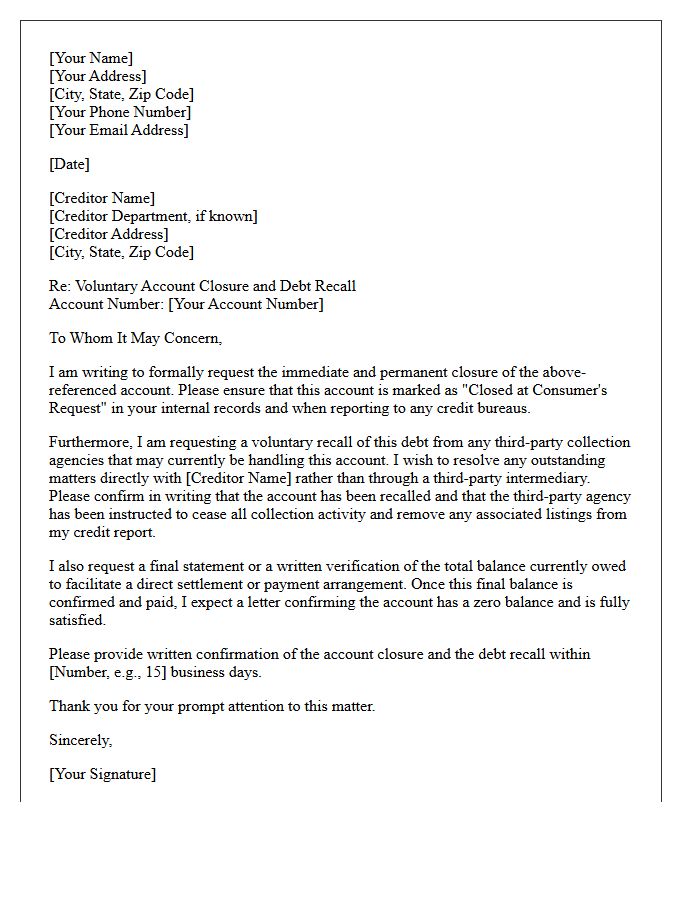

Voluntary Creditor Recall And Account Closure Letter

A Voluntary Creditor Recall and Account Closure Letter is a formal request sent by a consumer to terminate a credit agreement and cease further reporting. It is essential for individuals wishing to end their relationship with a lender while ensuring the account status is updated accurately on credit reports. This document serves as legal proof of your request, helping to prevent unauthorized charges and ensuring the final balance is settled. Using this letter protects your financial reputation by formally documenting the voluntary closure of the line of credit.

Direct Creditor Payment Account Closure And Return Letter

A Direct Creditor Payment Account Closure and Return Letter is a formal notification used to terminate a financial arrangement between a debtor and a creditor. This document officially confirms the account closure and requests the return of any surplus funds or security deposits held. It serves as essential legal evidence that the relationship has ended, preventing future unauthorized debits or incorrect credit reporting. Ensuring clear communication through this letter protects your consumer rights and provides a verified paper trail for your personal financial records.

Unverified Dispute Return To Original Creditor Closure Letter

An Unverified Dispute Return To Original Creditor Closure Letter signifies that a collection agency failed to validate a debt and returned the file to the original creditor. This legal notification confirms the agency has ceased collection efforts and must remove their entry from your credit report. It is critical to keep this document as proof of closure to prevent future double-reporting. While the agency is finished, the original creditor may still attempt collection or sell the debt again, necessitating a fresh verification request for any new third-party collectors.

Exhausted Collection Efforts Return To Original Creditor Letter

An Exhausted Collection Efforts Return To Original Creditor Letter formally notifies a debtor that a third-party agency has ceased recovery attempts and transferred the account back to the original creditor. This document is critical because it signals a change in who holds the legal right to collect. Once returned, the original creditor may choose to pursue litigation, sell the debt to a new buyer, or offer direct settlement options. Understanding this shift is essential for managing your credit reporting and resolving outstanding liabilities effectively through direct negotiation with the primary lender.

Pending Litigation Return To Original Creditor Closure Letter

A Pending Litigation Return To Original Creditor Closure Letter is a formal notice confirming that a debt collector has ceased legal action and transferred the account back to the original creditor. This document is crucial because it serves as evidence that the third-party agency no longer has the authority to collect the debt or pursue a lawsuit. Always verify your account status with the primary lender to ensure the balance is accurate and to prevent duplicate reporting on your credit profile during this transition period.

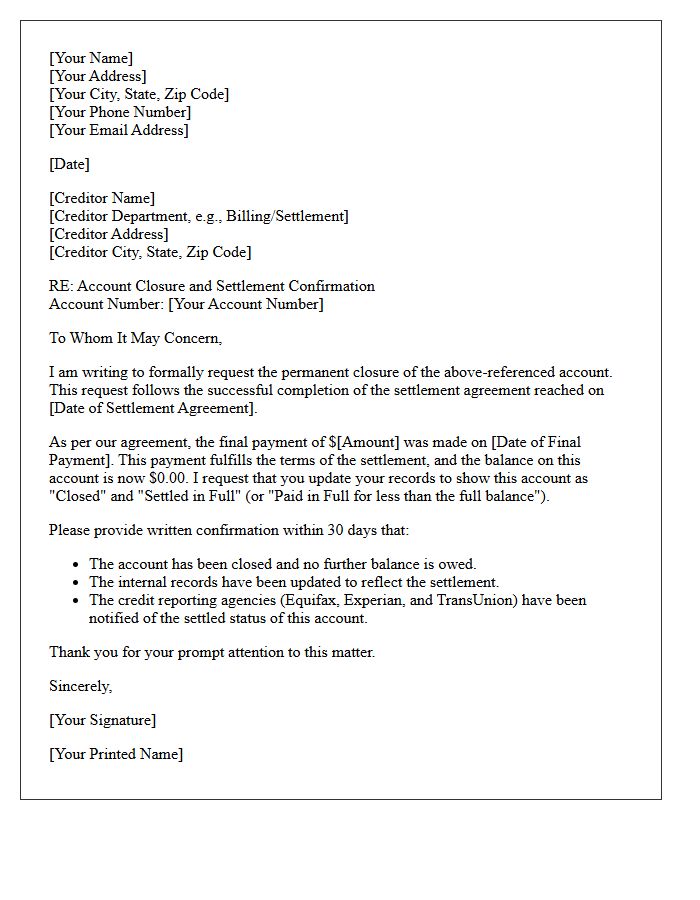

Direct Creditor Settlement Account Closure Letter

A Direct Creditor Settlement Account Closure Letter is a formal notification sent to creditors confirming that a debt settlement agreement has been fulfilled and the account should be permanently closed. This document serves as legal proof that you no longer owe a balance. It is essential to request that the creditor updates your credit report to reflect a zero balance. Always retain a copy of this correspondence and a delivery receipt to protect your financial history from future disputes or collection attempts regarding settled debts.

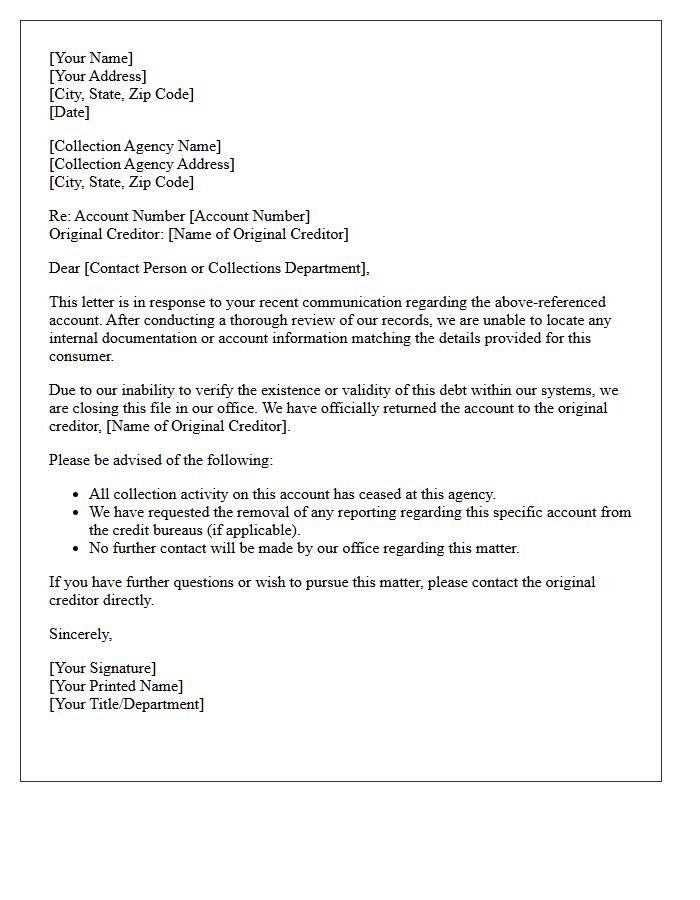

Unable To Locate Return To Original Creditor Closure Letter

When a collection agency reports a status of Unable to Locate, it typically means the account was returned to the Original Creditor after the agency failed to collect. This Closure Letter is vital for credit repair as it serves as proof that the third-party debt collector no longer has the legal authority to report or collect on the debt. If the collection remains on your credit report after the return, you must use this documentation to dispute and remove the inaccurate entry to protect your financial standing.

What is a Return to Original Creditor Closure Notice?

A Return to Original Creditor Closure Notice is a formal notification from a third-party debt collection agency stating they have ceased collection efforts and transferred the account back to the entity that originally issued the debt.

Does a Return to Original Creditor notice mean my debt is canceled?

No, this notice does not mean the debt is forgiven or canceled. It simply indicates that the specific collection agency is no longer authorized to collect the balance and the legal right to pursue the debt has reverted to the original creditor.

How does a Return to Original Creditor status affect my credit score?

When an account is returned to the original creditor, the collection agency's entry should be removed or marked as closed on your credit report. While this may remove a collection tradeline, the original delinquency or charge-off from the primary creditor may still impact your score.

Can I still negotiate a settlement after receiving this notice?

Yes, once the account is returned, you must direct all payment negotiations and settlement offers to the original creditor. They regained full control over the account and can decide whether to accept a settlement or assign it to a new collection firm.

Why was my account returned to the original creditor?

Accounts are typically returned if the collection contract expired, the agency was unsuccessful in its recovery efforts, or if you disputed the debt and the agency chose to return the file rather than provide further verification.

Comments