Closing a financial account requires a formal Voluntary Surrender Account Closure Notice to ensure all legal and contractual obligations are officially terminated. This document serves as your written request to end a service agreement and settle outstanding balances. Properly notifying your provider prevents future fees and credit complications. To simplify this process, below are some ready to use templates.

Image cover: Formal Notices and Templates for Voluntary Account Closure

Letter Samples List

- Voluntary Surrender Account Closure Letter

- Notice of Account Closure Following Voluntary Surrender Letter

- Voluntary Surrender Final Account Settlement Letter

- Debt Collection Account Closure and Surrender Letter

- Voluntary Collateral Surrender Resolution Letter

- Final Balance Waiver and Surrender Closure Letter

- Voluntary Repossession Account Termination Letter

- Surrendered Asset Account Closure Confirmation Letter

- Debt Forgiveness and Voluntary Surrender Letter

- Notice of Zero Balance Voluntary Surrender Letter

- Post-Surrender Deficiency Waiver and Closure Letter

- Voluntary Surrender Debt Satisfaction Letter

- Collateral Recovery and Account Closure Letter

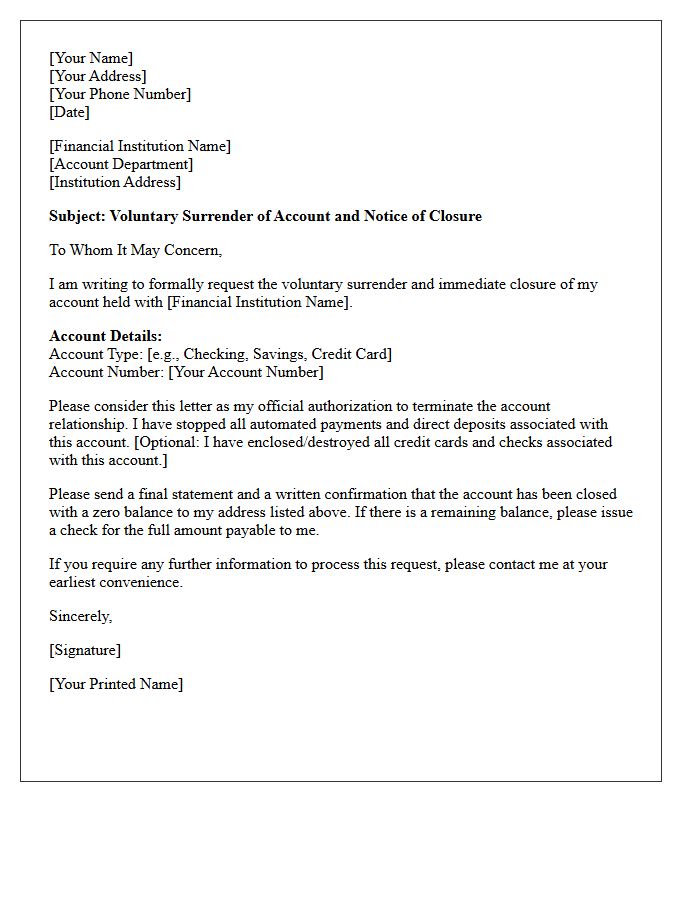

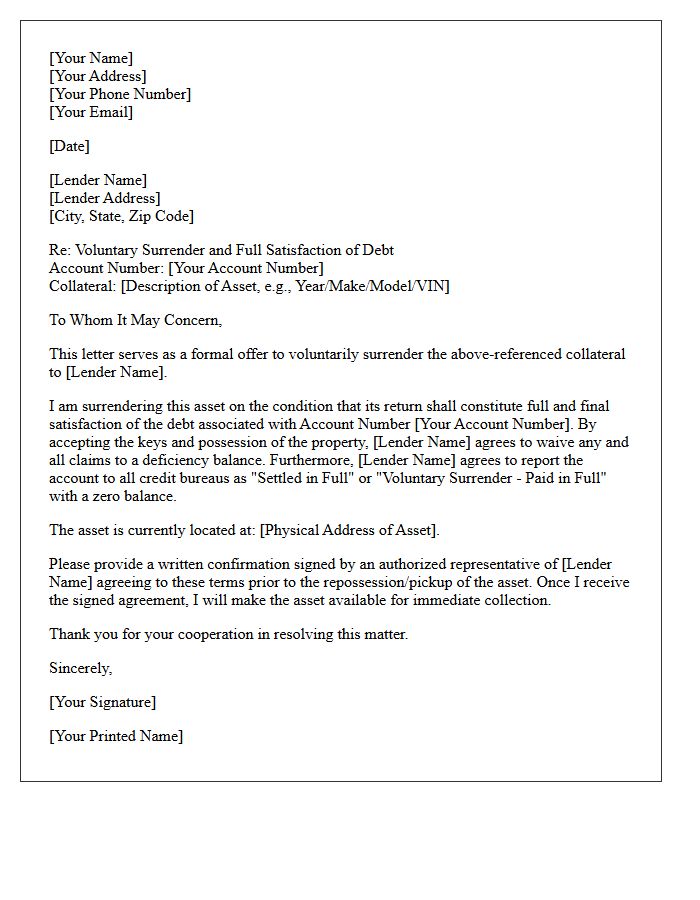

Voluntary Surrender Account Closure Letter

A voluntary surrender account closure letter is a formal document sent to a financial institution to officially terminate a contractual relationship. It serves as written proof of your intent to close an account, ensuring that future liabilities or recurring fees are legally halted. To be effective, the letter must include your full name, account number, and a clear request for a balance confirmation. Maintaining a copy of this correspondence is essential for record-keeping and resolving any potential credit reporting discrepancies or outstanding disputes after the closure is finalized.

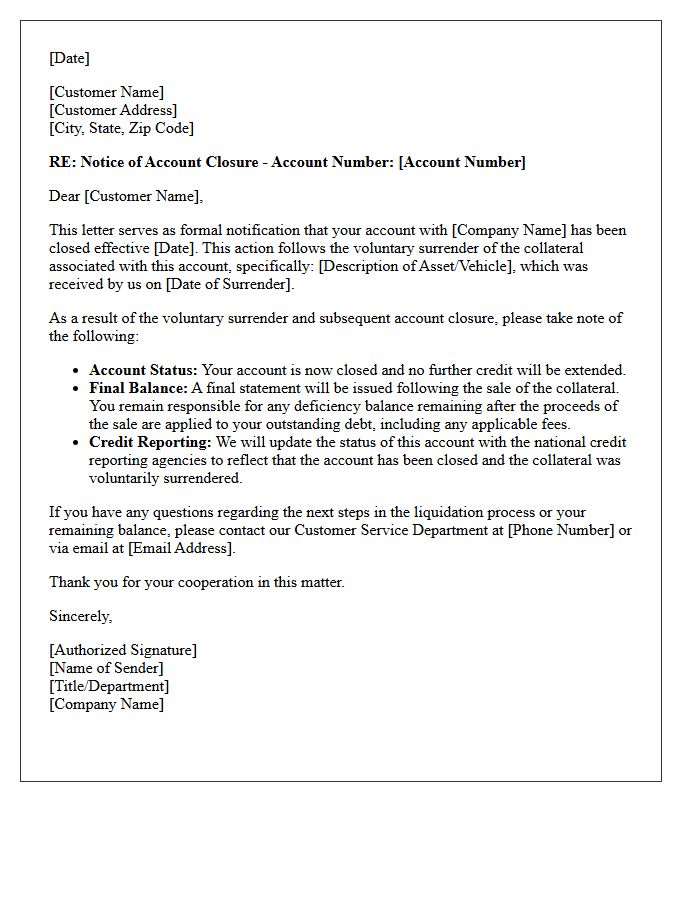

Notice of Account Closure Following Voluntary Surrender Letter

A Notice of Account Closure Following Voluntary Surrender confirms that a creditor has finalized the repossession process after you willingly returned collateral, such as a vehicle. This document is critical because it outlines the deficiency balance, which is the remaining debt if the asset sells for less than what you owe. Receiving this letter marks the formal termination of your contract and triggers credit reporting updates. It is essential to review the sale details for accuracy to ensure your legal rights are protected regarding any remaining financial liability.

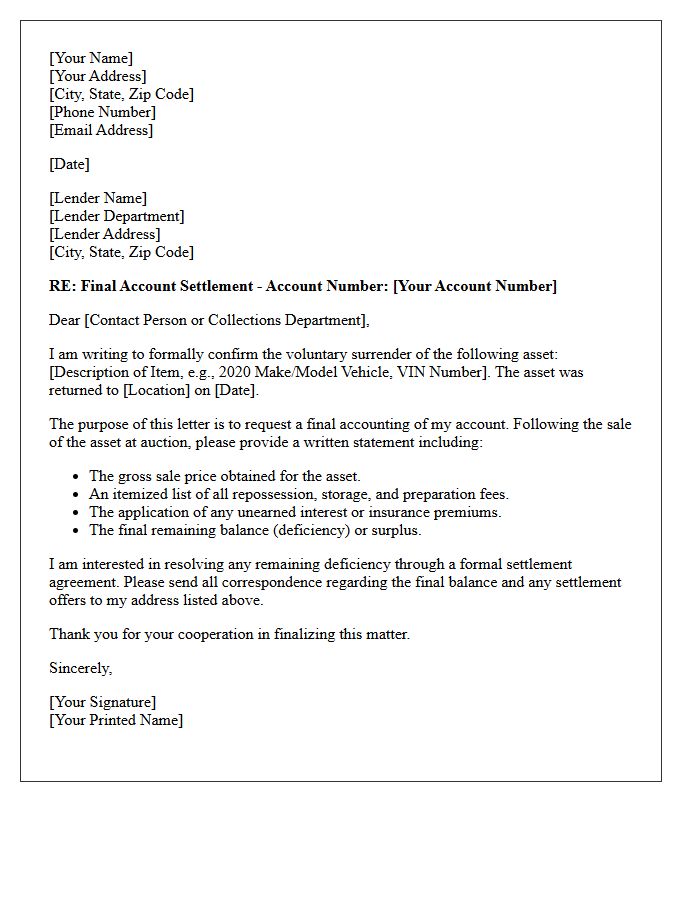

Voluntary Surrender Final Account Settlement Letter

A Voluntary Surrender Final Account Settlement Letter is a critical legal document confirming the formal closure of a credit agreement after returning collateral. It outlines the deficiency balance or surplus remaining after the asset's sale and specifies the final payment required to satisfy the debt. This letter serves as official proof that your obligations are fulfilled, protecting you from future collection actions. Always verify that the document explicitly states the account is settled in full to ensure your credit report accurately reflects the resolved status of the loan.

Debt Collection Account Closure and Surrender Letter

A debt collection closure letter serves as formal written confirmation that your account is fully resolved. It is essential to ensure the agency updates your credit report to show a zero balance, preventing future collection attempts. Always request a surrender letter if the debt was settled or paid in full, as this legal document protects you from "zombie debt" resurfacing. Maintaining these records is the most effective way to validate your financial rights and prove that you no longer have any outstanding legal obligations to the creditor.

Voluntary Collateral Surrender Resolution Letter

A Voluntary Collateral Surrender Resolution Letter is a formal document where a borrower agrees to voluntarily return secured assets to a lender to satisfy a debt. This process, often called a deed in lieu of foreclosure or voluntary repossession, helps avoid lengthy legal proceedings. It is essential to ensure the letter specifies whether the lender waives the right to pursue a deficiency balance. Documenting this mutual release of liability protects your financial future and may lessen the overall negative impact on your credit score compared to a forced recovery.

Final Balance Waiver and Surrender Closure Letter

A Final Balance Waiver occurs when a creditor agrees to cancel the remaining debt on an account, often following a settlement or vehicle repossession. Once the deficiency is forgiven, the lender issues a Surrender Closure Letter to confirm the account is officially closed with a zero balance. This document is essential for your records to prevent future collection actions. It serves as legal proof that you are no longer liable for the debt, although the forgiven amount may be reported as taxable income to the IRS.

Voluntary Repossession Account Termination Letter

A Voluntary Repossession Account Termination Letter is a formal document notifying a creditor of your intent to surrender a vehicle you can no longer afford. Submitting this written notice initiates the voluntary surrender process, which may reduce certain legal fees compared to forced seizure. However, it does not eliminate your liability for the deficiency balance-the remaining debt if the car sells for less than the loan amount. Using this letter creates a clear paper trail for your financial records and helps clarify your final obligations to the lender.

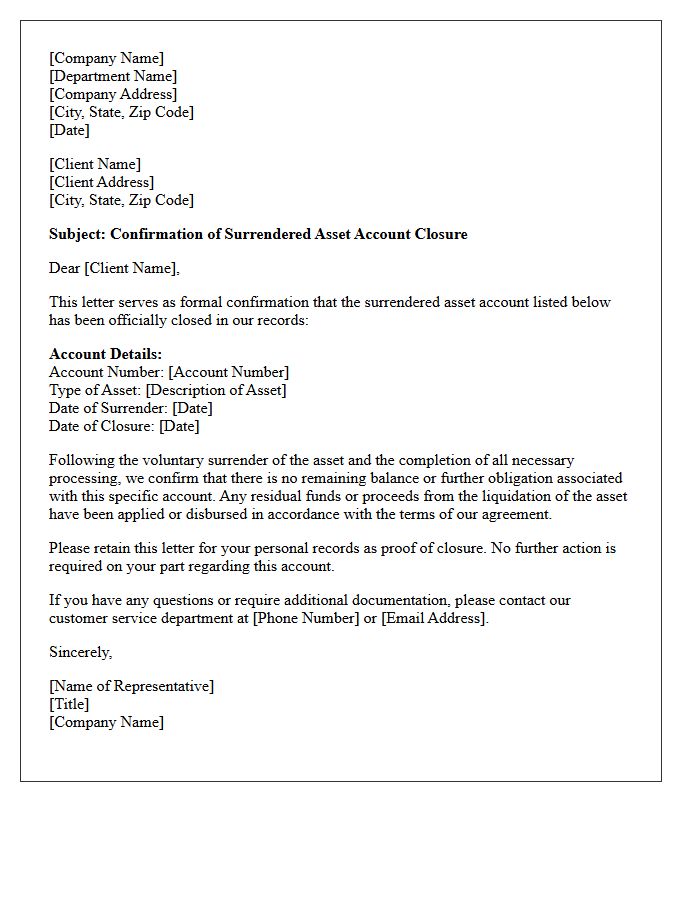

Surrendered Asset Account Closure Confirmation Letter

A Surrendered Asset Account Closure Confirmation Letter is a legal document verifying that an insurance policy or financial account has been officially terminated. This formal notification serves as definitive proof that the asset was liquidated and the contract ended. It is essential for tax reporting and financial record-keeping, confirming the final disbursement of funds to the owner. Retaining this letter is crucial for audit trails, ensuring no future liabilities or recurring fees remain associated with the closed account. Always review the stated final balance for accuracy upon receipt.

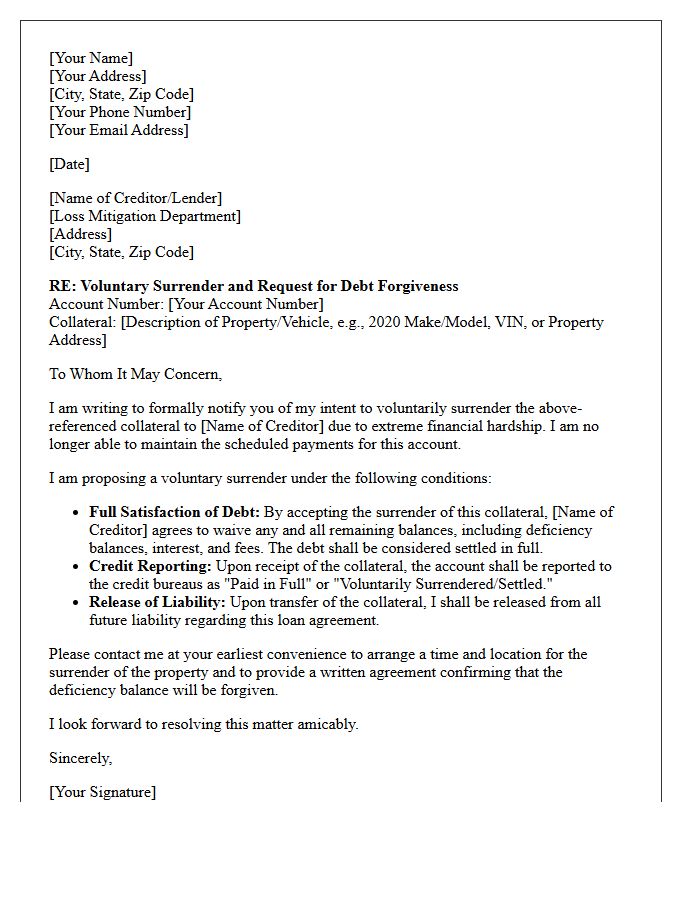

Debt Forgiveness and Voluntary Surrender Letter

A voluntary surrender letter is a formal notification to a lender expressing your intent to return collateral, such as a vehicle, when payments are no longer manageable. While this process is a voluntary repossession, it does not automatically erase your financial obligation. The lender will sell the asset, but you may still owe a deficiency balance if the sale proceeds are less than your total debt. You must specifically request debt forgiveness in writing to negotiate a waiver of this remaining balance and protect your long-term credit standing.

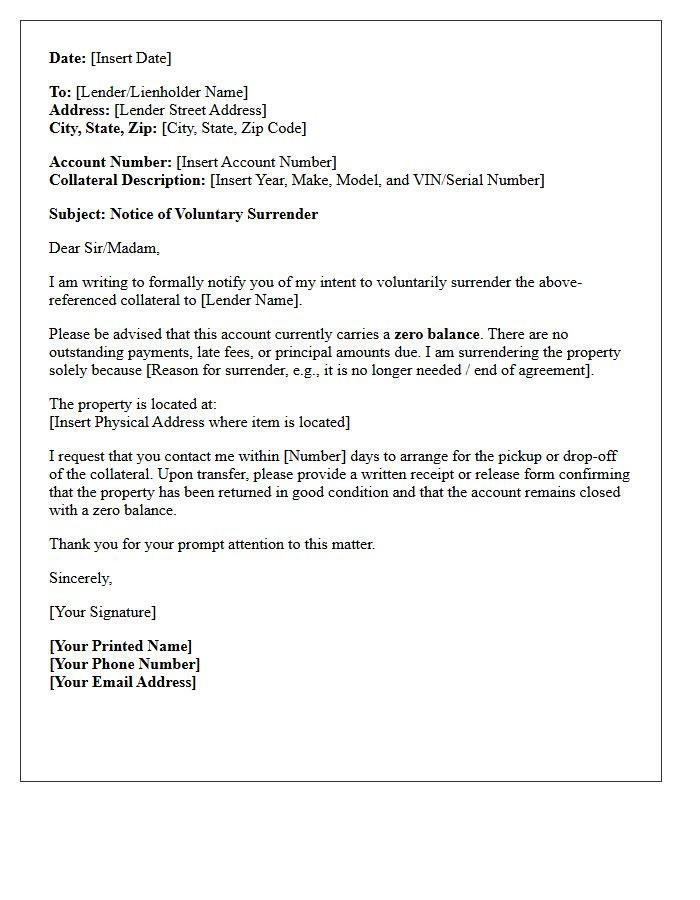

Notice of Zero Balance Voluntary Surrender Letter

A Notice of Zero Balance Voluntary Surrender Letter is a formal document used to return a vehicle to a lender when the loan is fully paid. This legal notification ensures the voluntary surrender is documented, protecting the consumer from future deficiency claims or collection efforts. It serves as proof that the collateral was returned in good faith with no remaining debt. Always keep a signed copy of this letter to verify the account status and prevent inaccurate credit reporting regarding the repossession or final balance of the agreement.

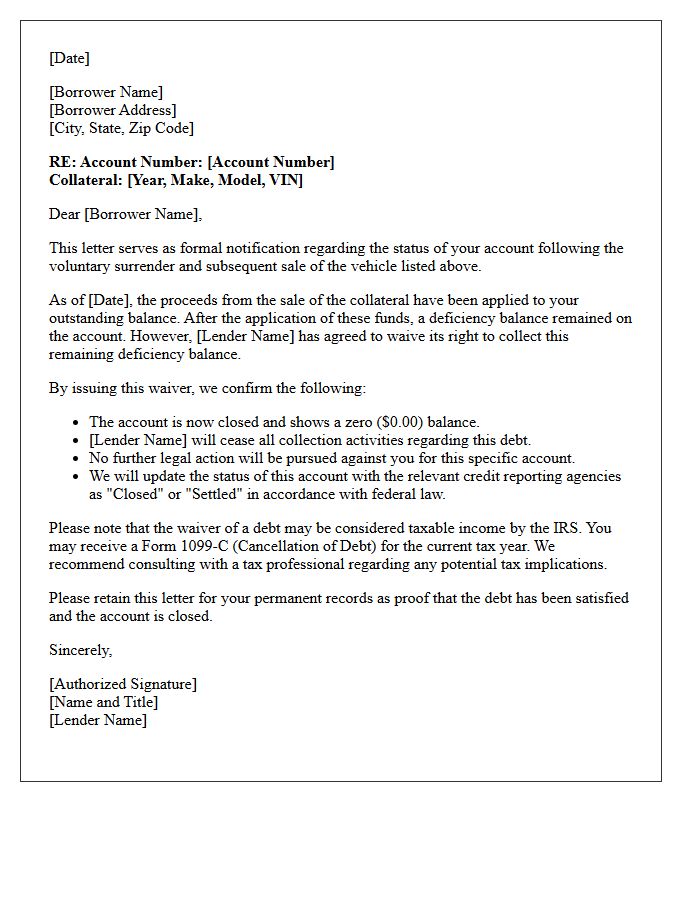

Post-Surrender Deficiency Waiver and Closure Letter

A Post-Surrender Deficiency Waiver is a formal agreement where a lender forgives the remaining balance after a repossessed asset is sold. This document ensures you are no longer personally liable for the "deficiency balance." Obtaining a Closure Letter is critical, as it serves as legal proof that the account is settled in full. Without these documents, creditors can pursue legal action or wage garnishment. Always verify that the letter explicitly states a zero balance and confirms the account is closed to protect your future credit and financial stability.

Voluntary Surrender Debt Satisfaction Letter

A Voluntary Surrender Debt Satisfaction Letter is a legal document confirming that a borrower has voluntarily returned collateral, such as a vehicle, to satisfy a debt. It serves as formal proof that the property was surrendered peacefully, potentially reducing legal fees or collection costs. While this action may result in a deficiency balance if the asset's resale value is less than the total loan, the letter ensures the creditor acknowledges the surrender of possession. Obtaining this written confirmation is vital for accurate credit reporting and future financial recovery.

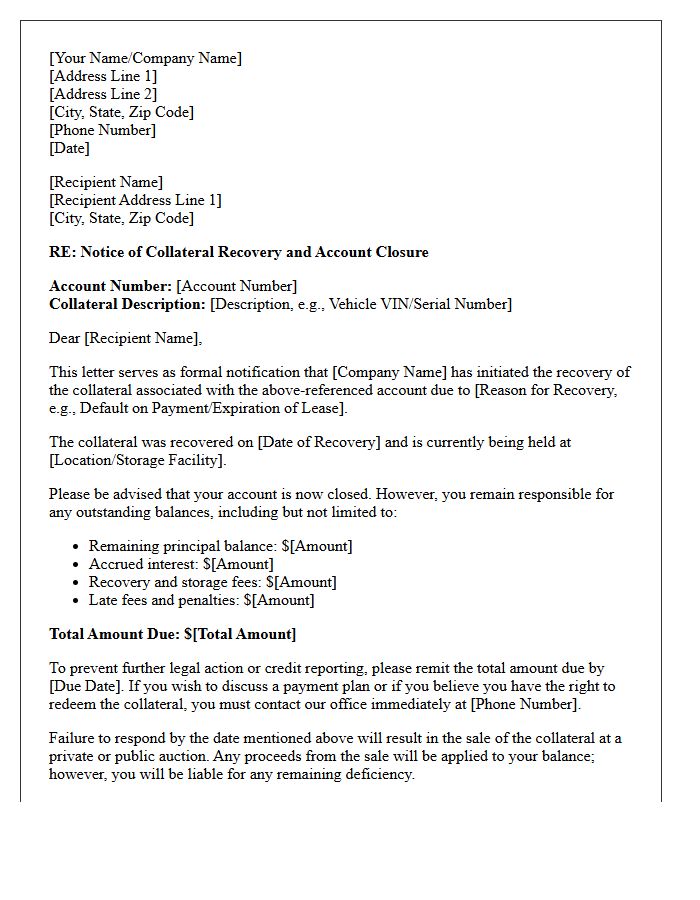

Collateral Recovery and Account Closure Letter

A Collateral Recovery and Account Closure Letter is a formal legal notification sent by a lender to a borrower following a default. It officially confirms the repossession of assets used as security and outlines the final steps to terminate the credit agreement. This document is legally binding, detailing any remaining deficiency balances, redemption rights, and the timeline for the final sale of property. Understanding your rights regarding the disposition of collateral is essential to managing your credit standing and ensuring compliance with financial regulations during the account settlement process.

What is a Voluntary Surrender Account Closure Notice?

A Voluntary Surrender Account Closure Notice is a formal written notification submitted by an account holder to a financial institution or service provider requesting the permanent closure of their account and the relinquishment of any associated assets or services.

How do I initiate a voluntary surrender of my account?

To initiate the process, you must submit a signed closure notice via the provider's authorized channels, typically through a secure online portal, certified mail, or in-person at a branch location, ensuring all outstanding balances are settled beforehand.

What information must be included in a formal account closure notice?

The notice should include your full legal name, account number, current contact information, the effective date of closure, and specific instructions regarding the disbursement of any remaining credit balances or funds.

Does voluntary account surrender impact my credit score?

While the act of surrendering an account is voluntary, it may impact your credit score by affecting your credit utilization ratio or the average age of your accounts; however, it is generally viewed more favorably than an involuntary closure initiated by the creditor.

Can a voluntary surrender notice be revoked once submitted?

Once a voluntary surrender notice is processed and the account is closed, it typically cannot be revoked. You would usually need to undergo a new application process to re-establish a relationship with the institution.

Comments