A Collection Agency Demand for Dishonored Check is a formal legal notification sent to a debtor after a payment fails due to insufficient funds. This demand outlines the legal consequences, including potential statutory damages and service fees, to compel immediate repayment. To help you draft a professional notice, below are some ready to use template.

Image cover: Professional Debt Recovery: Demand Letters and Templates for Dishonored Checks

Letter Samples List

- Initial Demand Letter for Dishonored Check

- Second Notice Letter for Bounced Check Collection

- Final Warning Letter for Returned Check Payment

- Statutory Notice Letter for Dishonored Check

- Insufficient Funds Notification Letter for Dishonored Check

- Pre-Legal Action Letter for Dishonored Check

- Penalty Fee Assessment Letter for Bounced Check

- Settlement Offer Letter for Returned Check Debt

- Payment Plan Approval Letter for Dishonored Check

- Intent to Sue Letter for Unpaid Dishonored Check

- Bank Rejection Notice Letter for Dishonored Check

- Last Attempt Collection Letter for NSF Check

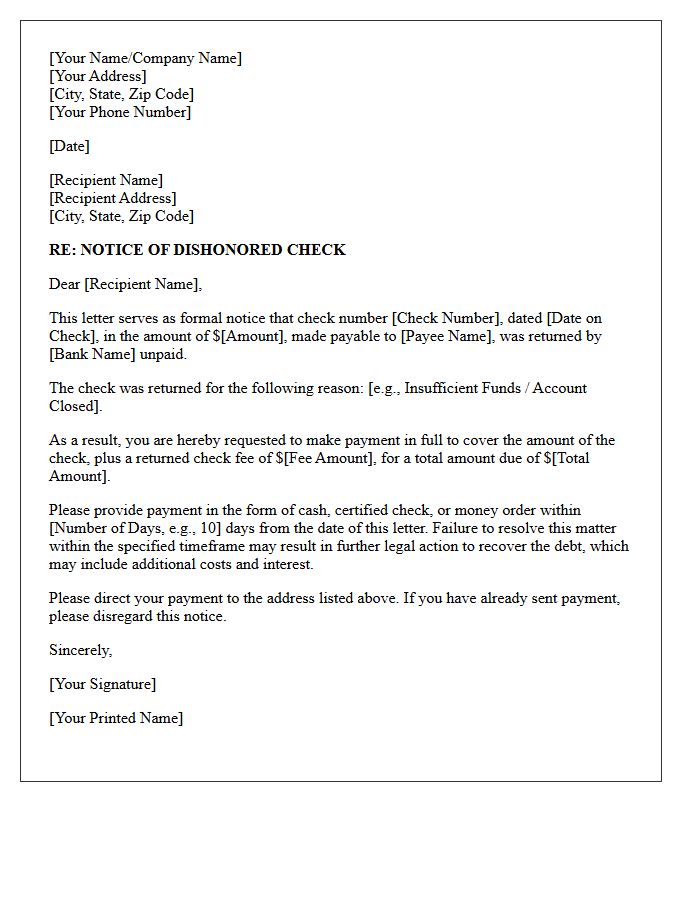

Initial Demand Letter for Dishonored Check

An Initial Demand Letter is a formal legal notice sent to a drawer whose payment was rejected. It serves as a statutory requirement before pursuing criminal charges or civil lawsuits. To recover funds, the letter must clearly state the check amount, any applicable service fees, and a specific deadline for repayment-typically 15 to 30 days. Sending this via certified mail provides crucial evidence that the debtor was notified. Failure to settle the debt after receiving this notice can result in treble damages or additional penalties under state laws.

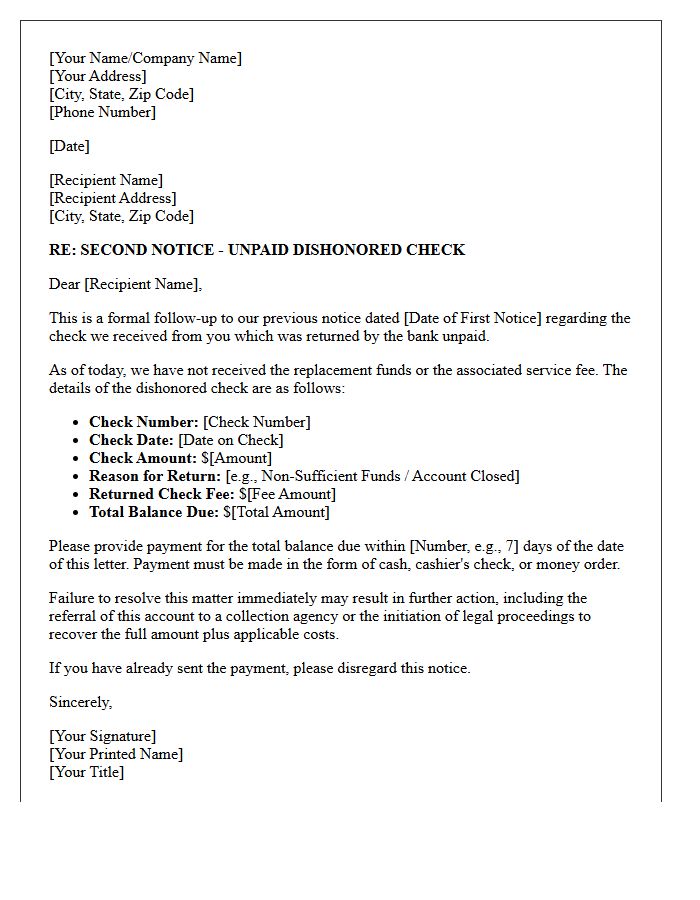

Second Notice Letter for Bounced Check Collection

A Second Notice Letter serves as a formal follow-up for a dishonored payment. It is crucial to include the original check number, the outstanding balance, and any applicable NSF fees permitted by state law. This document provides a final opportunity for the debtor to settle the debt voluntarily before you pursue legal action or involve a collection agency. Clearly state a firm deadline for payment and specify accepted methods, such as a cashier's check or money order, to ensure the collection process remains legally compliant and documented.

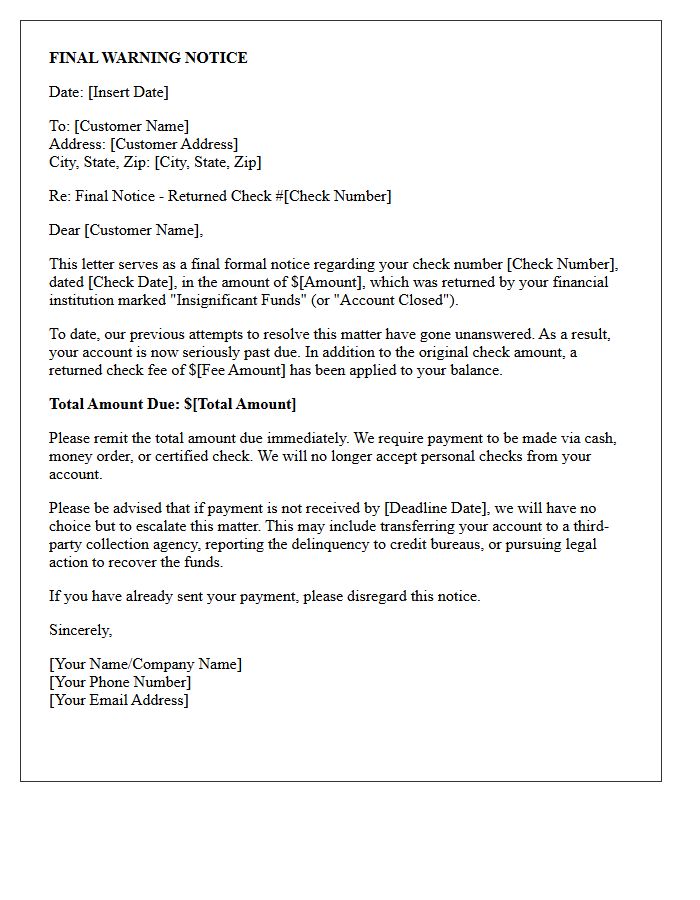

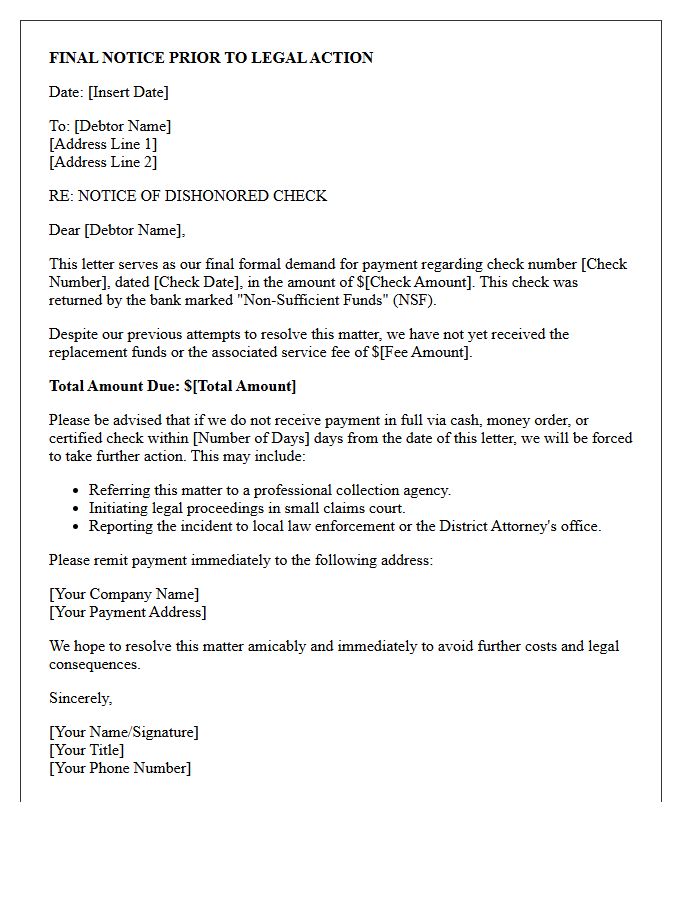

Final Warning Letter for Returned Check Payment

A final warning letter for a returned check is a formal notice demanding immediate settlement of a failed payment. It informs the recipient that their check was dishonored due to insufficient funds or closed accounts. This document typically includes a strict deadline and specifies additional late fees or administrative penalties. Failure to provide a replacement payment via certified funds may result in the suspension of services, reporting to credit bureaus, or legal action. It serves as the final opportunity to resolve the debt before the matter is escalated to a collection agency.

Statutory Notice Letter for Dishonored Check

A statutory notice letter for a dishonored check is a formal legal demand sent to a drawer whose payment was rejected by the bank. It serves as a mandatory prerequisite for filing a civil or criminal lawsuit. The notice informs the issuer that their check was returned for insufficient funds or a closed account, providing a strict deadline (usually 15 to 30 days) to make full restitution. Failing to settle the debt after receiving this formal notice can lead to penalties, court costs, and potential prosecution under state laws.

Insufficient Funds Notification Letter for Dishonored Check

An Insufficient Funds Notification Letter is a formal legal notice sent to a drawer when a check is dishonored by their bank. It serves as an official demand for repayment of the original amount plus any applicable administrative fees. Sending this written document is often a mandatory legal requirement before pursuing further collection actions or criminal charges. To protect your rights, ensure the letter includes the check date, number, and a specific deadline for the recipient to settle the debt and avoid potential litigation or penalties.

Pre-Legal Action Letter for Dishonored Check

A Pre-Legal Action Letter for a dishonored check is a formal demand for payment sent before initiating litigation. It serves as a final opportunity for the issuer to settle the debt, including the original amount and any applicable statutory penalties. Sending this notice is often a legal prerequisite under state laws to qualify for triple damages or attorney fees in court. The letter must clearly state the check details, the reason for return, and a specific deadline for restitution to ensure the sender's right to pursue further civil or criminal action.

Penalty Fee Assessment Letter for Bounced Check

A penalty fee assessment letter notifies an issuer that their payment was returned due to insufficient funds. This formal notice outlines the specific NSF fee imposed by the institution to cover processing costs. It serves as a legal record demanding immediate restitution of the original amount plus the penalty. Failure to resolve this debt promptly can negatively impact your credit score and may lead to legal action or the closure of your account. Always ensure your balance covers outstanding checks to avoid these costly administrative penalties.

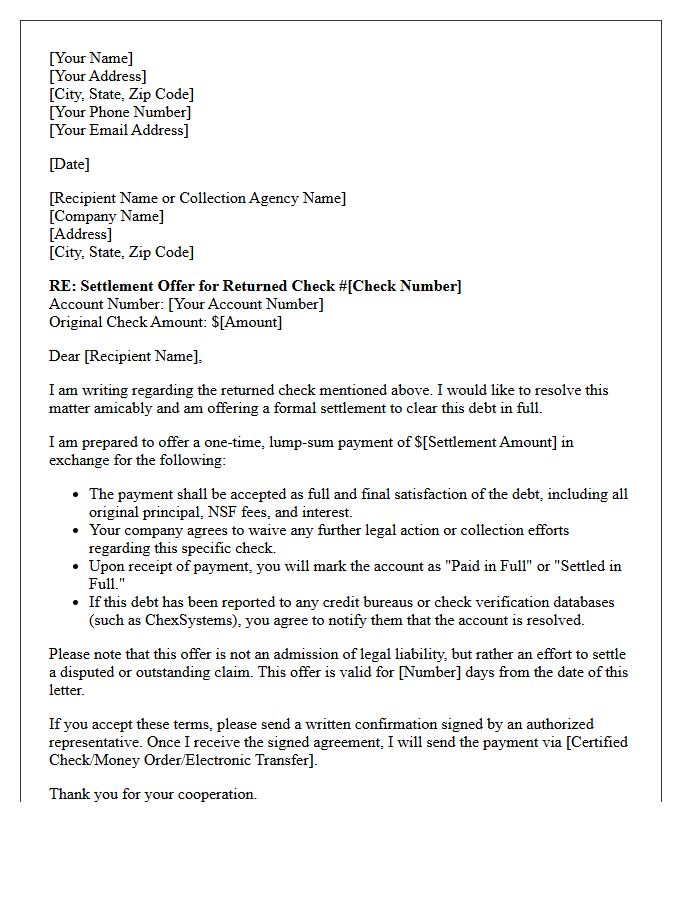

Settlement Offer Letter for Returned Check Debt

A settlement offer letter for a returned check debt is a formal proposal to resolve an outstanding balance for less than the original amount. To ensure legal protection, the document must include the account number, the specific settlement sum, and a request for a written agreement. It is crucial to specify that the payment constitutes a full satisfaction of the debt to prevent further collection actions. Once the creditor accepts, ensure you receive a confirmation letter before sending funds to effectively clear your financial liability and protect your credit standing.

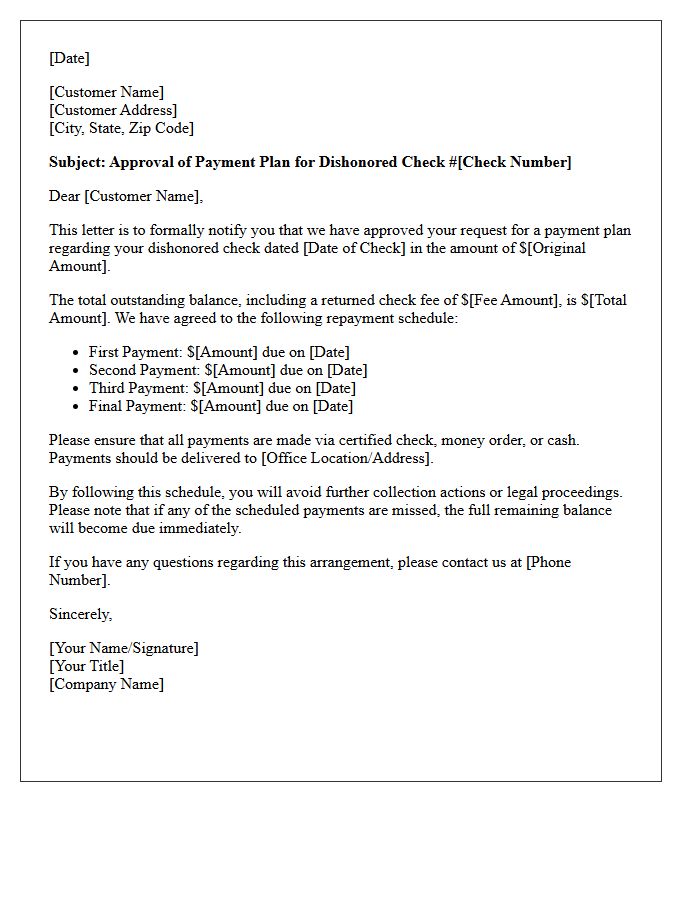

Payment Plan Approval Letter for Dishonored Check

A Payment Plan Approval Letter for a dishonored check formally confirms a structured agreement to resolve outstanding debt after a payment failure. This document is crucial because it provides legal evidence that the creditor has accepted your proposal to pay in installments rather than demanding an immediate lump sum. It outlines specific deadlines, interest rates, and penalties for future defaults. Receiving this written confirmation protects your credit score and helps avoid legal action or further collection efforts, provided you strictly adhere to the newly established repayment schedule.

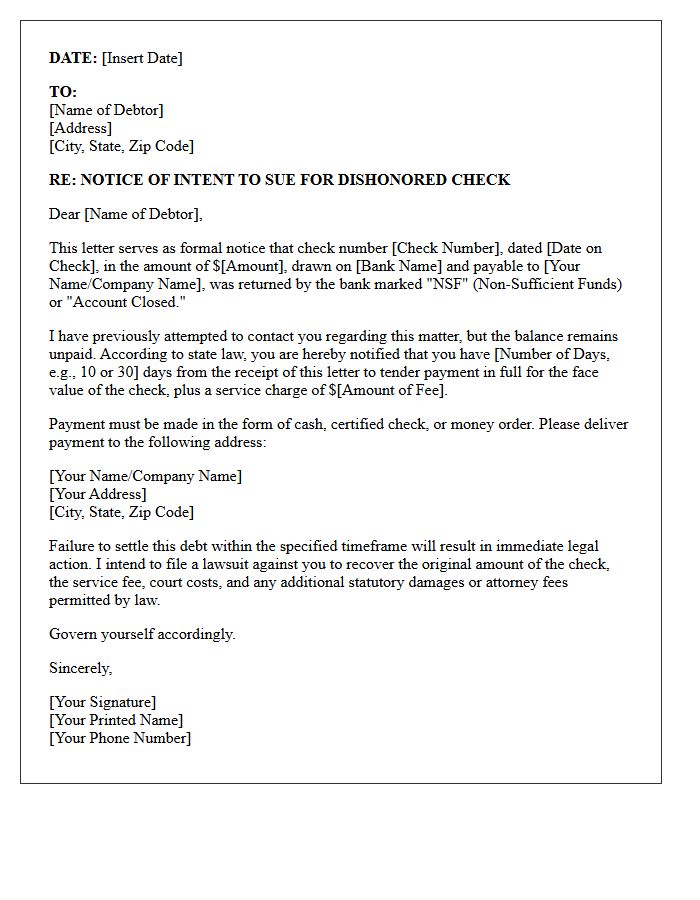

Intent to Sue Letter for Unpaid Dishonored Check

An Intent to Sue Letter serves as a formal legal demand notifying a debtor of pending litigation regarding an unpaid dishonored check. This notice provides a final opportunity to settle the debt, including the original amount plus applicable statutory damages or NSF fees, before a lawsuit is filed in small claims court. Sending this letter is often a mandatory legal requirement to prove a good-faith effort to collect. It underscores the legal consequences of check fraud or insufficient funds, compelling the recipient to resolve the balance immediately to avoid further legal action.

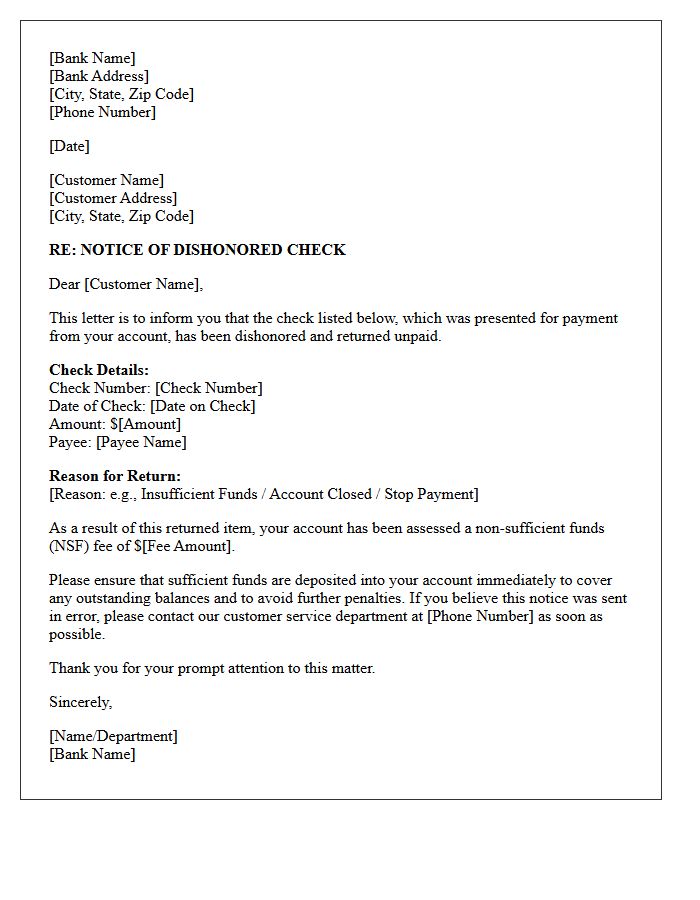

Bank Rejection Notice Letter for Dishonored Check

A Bank Rejection Notice Letter for a Dishonored Check is a formal notification sent when a payment cannot be processed due to insufficient funds. This document serves as legal evidence of a failed transaction, often resulting from account imbalances or closed accounts. It is crucial for the recipient to promptly resolve the debt to avoid additional late fees, administrative penalties, or potential legal action. For the issuer, receiving this notice signifies a payment default, necessitating immediate communication with the bank or merchant to rectify the outstanding balance and maintain financial credibility.

Last Attempt Collection Letter for NSF Check

A Last Attempt Collection Letter is the final formal notice issued before pursuing legal action or reporting a debt to credit bureaus. This document notifies the recipient that their NSF check (Non-Sufficient Funds) remains unpaid despite previous reminders. It typically includes the original check amount plus mandatory statutory fees. To avoid litigation or a criminal complaint for check fraud, the debtor must provide immediate payment within a specified deadline. This letter serves as critical evidence of a good-faith effort to resolve the debt out of court.

What is a collection agency demand for a dishonored check?

A collection agency demand for a dishonored check is a formal legal notice sent to a consumer or business who issued a check that failed to clear due to non-sufficient funds (NSF) or a closed account. This notice serves as a final demand for payment of the original check amount plus any state-mandated administrative and bank fees.

How long do I have to pay after receiving a demand letter for a bounced check?

Most state laws provide a specific grace period, typically between 10 and 30 days from the date the demand letter was mailed, to resolve the debt. Failure to pay within this statutory timeframe can result in the collection agency pursuing treble damages, which may be up to three times the value of the original check.

Can a collection agency charge extra fees for a dishonored check?

Yes, collection agencies are legally permitted to charge a returned check fee (NSF fee) in addition to the face value of the check. These fees are regulated by state law and usually range from $25 to $40, or a percentage of the check amount, whichever is greater.

What are the legal consequences of ignoring a dishonored check demand?

Ignoring a formal demand for a dishonored check can lead to civil litigation, where the court may award the creditor the original check amount, service fees, legal costs, and punitive damages. Furthermore, unpaid dishonored checks can be reported to specialized consumer reporting agencies like ChexSystems, which may impact your ability to open future bank accounts.

What should I do if I receive a demand for a check I didn't write?

If you receive a demand for a dishonored check that you believe is fraudulent or the result of identity theft, you should immediately send a written dispute to the collection agency. Provide documentation such as a police report or an affidavit of forgery to challenge the claim and request a validation of the debt under the Fair Debt Collection Practices Act (FDCPA).

Comments