If a payment has bounced, sending a formal Notice of Dishonored Check is a critical legal step to recover your money. This document officially notifies the issuer of the failed payment and issues a formal demand for certified funds to resolve the debt immediately. Protecting your financial interests requires clear communication. To help you get started, below are some ready to use templates.

Image cover: Professional Demand Templates for Dishonored Checks and Certified Funds Requests

Letter Samples List

- Notice of Dishonored Check and Demand for Certified Funds Letter

- First Notice of Bounced Check and Certified Payment Demand Letter

- Urgent Notice of Dishonored Check and Certified Funds Request Letter

- Second Demand for Certified Funds Following Dishonored Check Letter

- Final Notice of Dishonored Check and Mandatory Certified Funds Letter

- Returned Check Notification and Certified Funds Replacement Letter

- Notice of Insufficient Funds and Demand for Certified Payment Letter

- Dishonored Payment Notice and Certified Funds Requirement Letter

- Statutory Notice of Dishonored Check and Certified Funds Demand Letter

- Notice of Dishonored Item and Demand for Secured Funds Letter

- Debt Collection Notice of Bounced Check and Certified Funds Letter

- Pre-Litigation Notice of Dishonored Check and Certified Funds Letter

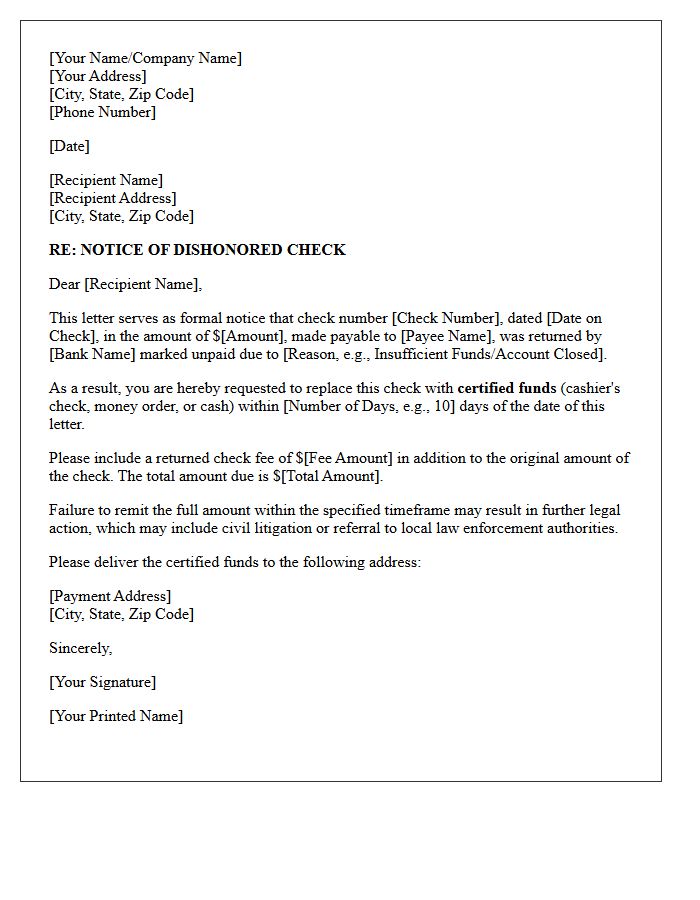

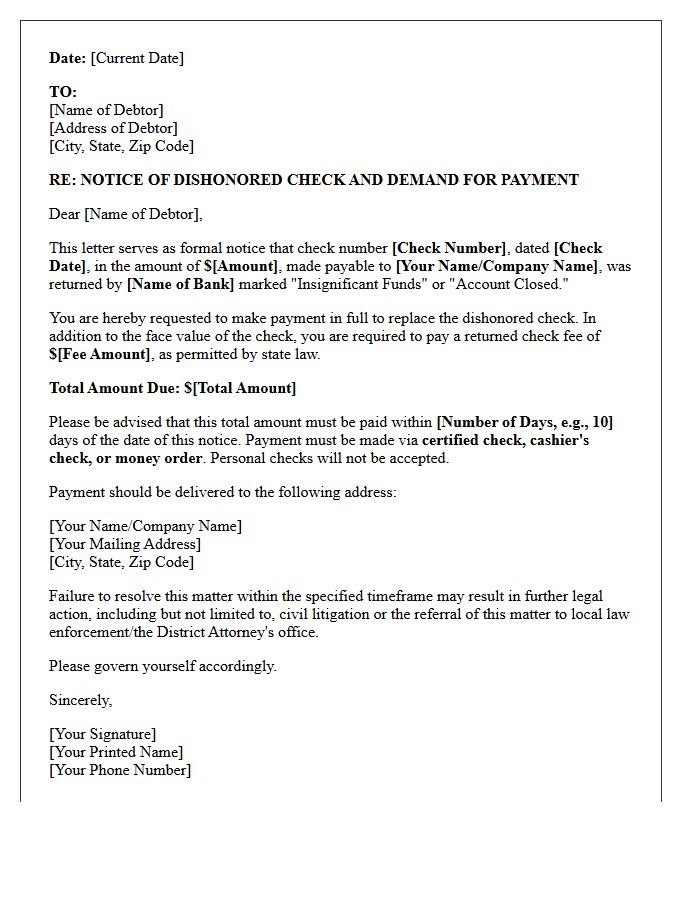

Notice of Dishonored Check and Demand for Certified Funds Letter

A Notice of Dishonored Check is a formal legal demand sent to a writer whose payment was returned for insufficient funds or closed accounts. It serves as an official warning that the recipient must provide certified funds, such as a cashier's check or money order, within a specific timeframe-often 15 to 30 days. Sending this notice is a critical prerequisite for pursuing civil penalties, liquidated damages, or criminal charges under state laws. It provides the debtor a final opportunity to rectify the debt before further litigation or collection actions are initiated.

First Notice of Bounced Check and Certified Payment Demand Letter

A First Notice of Bounced Check serves as a formal legal warning to a debtor that their payment failed due to insufficient funds. It initiates a statutory grace period, typically 15 to 30 days, for the issuer to rectify the debt. Sending this as a Certified Payment Demand Letter is crucial, as it provides verifiable proof of delivery required for potential legal action or criminal prosecution. This document must clearly state the check details, applicable service fees, and the deadline to pay before the matter escalates to court.

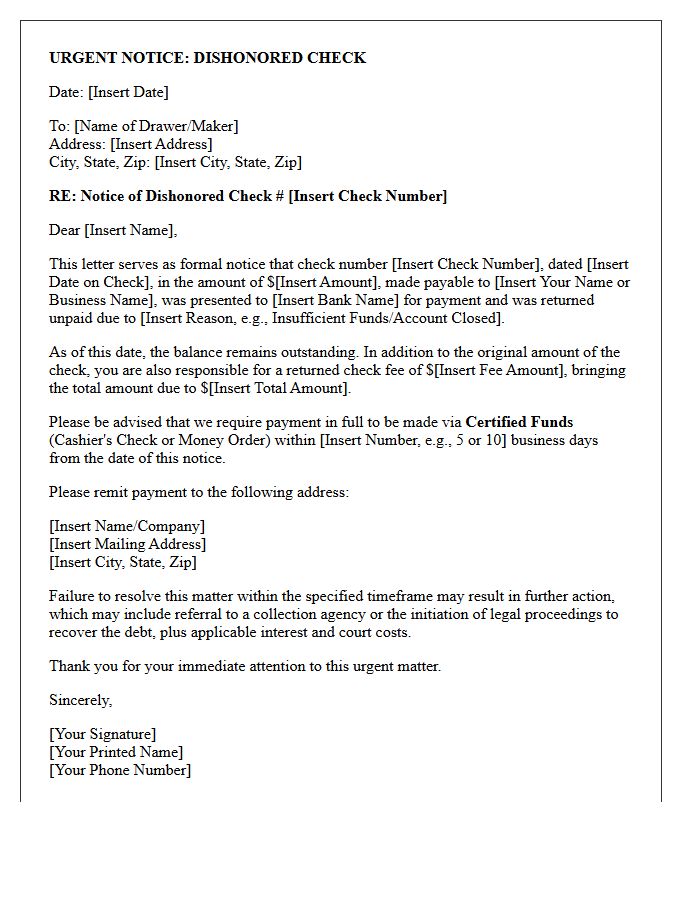

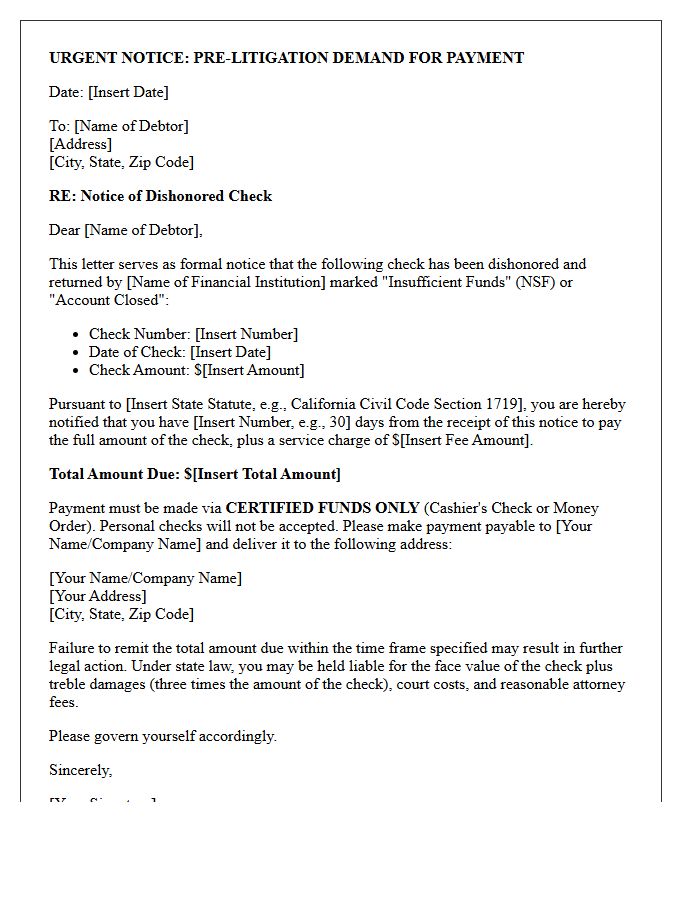

Urgent Notice of Dishonored Check and Certified Funds Request Letter

An Urgent Notice of Dishonored Check serves as a formal demand for payment following a returned check. It informs the recipient that their payment failed due to insufficient funds or a closed account. To resolve the debt and avoid potential legal action or penalties, the sender typically mandates a Certified Funds Request. This requires the recipient to provide guaranteed payment, such as a cashier's check or money order, within a specific timeframe. Promptly addressing this notice is essential to maintain financial credibility and prevent further collection efforts.

Second Demand for Certified Funds Following Dishonored Check Letter

A second demand for certified funds is a critical legal step issued after a debtor fails to resolve a previously dishonored check. This formal notice typically warns of impending litigation or criminal prosecution for fraud. To protect your rights, the letter must strictly comply with state statutes, often providing a final grace period (usually 10 to 30 days) to remit payment via cashier's check or money order. Failure to respond to this final notice frequently triggers statutory damages, court costs, and attorney fees beyond the original debt amount.

Final Notice of Dishonored Check and Mandatory Certified Funds Letter

A Final Notice of Dishonored Check is a formal legal warning issued when a payment fails due to insufficient funds. It informs the recipient that they have a strict deadline, typically 10 to 30 days, to settle the debt before legal action or criminal prosecution begins. To ensure payment validity, the notice often includes a Mandatory Certified Funds requirement, meaning the balance must be paid via cashier's check or money order. Failure to comply can result in additional statutory penalties, court costs, and negative impacts on your credit standing.

Returned Check Notification and Certified Funds Replacement Letter

A Returned Check Notification informs a payer that their payment was declined due to insufficient funds. This formal notice requires an immediate Certified Funds Replacement Letter to resolve the debt securely. Payers must replace the bounced check with guaranteed payment, such as a cashier's check or money order, to avoid additional NSF fees or legal action. Providing prompt certified funds ensures the account is settled and restores financial credibility between both parties while preventing further collection procedures.

Notice of Insufficient Funds and Demand for Certified Payment Letter

A Notice of Insufficient Funds and Demand for Certified Payment is a formal legal document sent when a bounced check fails to clear. This letter serves as official notification that a transaction was rejected due to lack of capital. To avoid potential criminal prosecution or civil penalties, the recipient must provide a certified payment-such as a money order or cashier's check-within a specific statutory timeframe. Promptly resolving the debt is essential to mitigate additional bank fees and protect your legal standing regarding the outstanding balance.

Dishonored Payment Notice and Certified Funds Requirement Letter

A Dishonored Payment Notice informs a debtor that their recent payment failed due to insufficient funds or account issues. This formal communication acts as a legal demand for immediate rectification. To prevent future risks, creditors often issue a Certified Funds Requirement Letter, mandates that all subsequent payments be made via guaranteed methods like cashier's checks or money orders. These documents protect businesses from financial loss and establish a clear paper trail for potential legal action or debt recovery processes if the balance remains unpaid.

Statutory Notice of Dishonored Check and Certified Funds Demand Letter

A Statutory Notice of Dishonored Check is a formal legal demand sent to a drawer whose payment failed due to insufficient funds or a closed account. This document serves as a mandatory prerequisite for pursuing civil penalties, which may include triple damages or legal fees. To avoid litigation, the recipient is typically required to provide a Certified Funds Demand Letter response, ensuring the debt is cleared via guaranteed payment methods like cashier's checks or money orders within a strict statutory timeframe, usually fifteen to thirty days depending on local jurisdiction.

Notice of Dishonored Item and Demand for Secured Funds Letter

A Notice of Dishonored Item and Demand for Secured Funds Letter is a formal legal notification sent when a payment, typically a check, is rejected due to insufficient funds. This document informs the payer of the failed transaction and serves as a statutory demand for immediate reimbursement. It often includes a deadline to provide secured funds, such as a cashier's check or money order, plus applicable returned check fees. Sending this letter is a critical prerequisite for pursuing further legal action or criminal charges under state bad check laws.

Debt Collection Notice of Bounced Check and Certified Funds Letter

Receiving a debt collection notice for a bounced check signifies a legal demand for payment due to non-sufficient funds. To resolve this, creditors typically issue a formal letter requiring certified funds, such as a cashier's check or money order, to guarantee the debt is cleared. This process often includes additional statutory penalties and administrative fees. Promptly responding with verified payment is essential to avoid further legal action, potential criminal charges, or negative reports to credit bureaus that can severely damage your financial standing.

Pre-Litigation Notice of Dishonored Check and Certified Funds Letter

A Pre-Litigation Notice of Dishonored Check serves as a formal legal demand for payment after a check is returned for insufficient funds. To comply with statutory requirements and preserve your right to claim treble damages or legal fees, the notice must be sent via certified mail with a return receipt. This letter provides the debtor a specific window, typically 15 to 30 days, to settle the debt using certified funds, such as a cashier's check or money order, before formal civil litigation or criminal charges are pursued.

What is a Notice of Dishonored Check and Demand for Certified Funds?

A Notice of Dishonored Check and Demand for Certified Funds is a formal legal letter sent to a person or business who issued a payment that was returned by the bank, typically due to non-sufficient funds (NSF) or a closed account. It officially demands that the debt be cleared using guaranteed payment methods like a cashier's check or money order.

What information must be included in a formal Demand for Certified Funds?

The notice should include the date the check was issued, the check number, the exact amount owed, the reason for dishonor (e.g., NSF), and a specific deadline for payment. It must also state that the replacement payment must be made via certified funds, such as a certified check, cashier's check, or cash, to ensure the funds are guaranteed.

How long does a recipient have to respond to a Dishonored Check Notice?

State laws vary, but most jurisdictions require the sender to provide a grace period of 15 to 30 days from the date the notice was received. If the recipient fails to provide certified funds within this statutory timeframe, the sender may be entitled to pursue additional damages, such as triple the check amount or attorney fees.

Why is it necessary to send this notice via Certified Mail?

Sending the notice via Certified Mail with a Return Receipt Requested provides legal proof that the recipient was officially notified of the dishonored check. This documentation is essential if the case proceeds to small claims court or if you intend to pursue criminal charges for a "bad check" under state statutes.

What legal actions can be taken if the Demand for Certified Funds is ignored?

If the debtor fails to pay after receiving the notice, the creditor can file a civil lawsuit in small claims court to recover the original amount plus bank fees and statutory penalties. In cases involving intentional fraud, the matter may also be referred to the local District Attorney's office for criminal prosecution under "bad check" laws.

Comments