A Notice of Dishonored Check is a formal communication sent when a bank refuses payment because the drawer failed to sign the document. This administrative error invalidates the instrument, requiring immediate correction to settle the outstanding debt and avoid legal complications. To help you resolve this issue professionally, below are some ready to use templates.

Image cover: Notice of Dishonored Check: Missing Signature Guide and Formal Templates

Letter Samples List

- Notice of Dishonored Check Due to Missing Signature Letter

- First Demand Letter for Outstanding Balance

- Second Notice Demand Letter for Past Due Account

- Final Warning Letter Before Legal Action

- Notice of Dishonored Check Due to Insufficient Funds Letter

- Debt Validation Notice Letter

- Settlement Offer Agreement Letter

- Notice of Account Placement for Collection Letter

- Cease and Desist Acknowledgment Letter

- Payment Plan Confirmation Letter

- Notice of Returned Payment Fee Letter

- Notice of Default on Payment Arrangement Letter

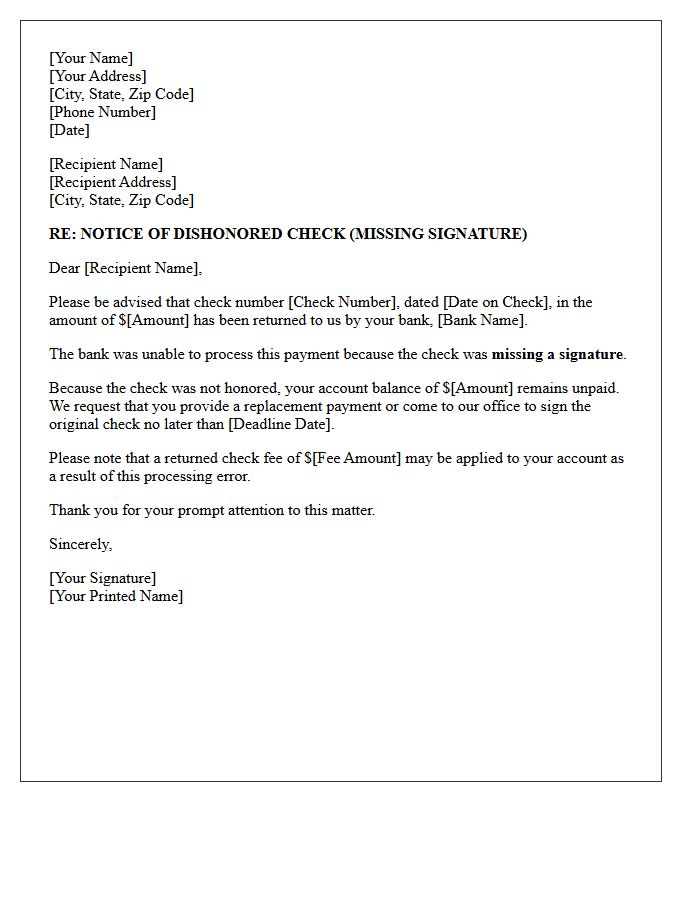

Notice of Dishonored Check Due to Missing Signature Letter

A Notice of Dishonored Check Due to Missing Signature is a formal legal document sent when a bank refuses to process a payment because the drawer failed to sign the check. The most critical step is providing immediate notification to the issuer to resolve the oversight. This letter serves as an official demand for a replacement check or alternative payment method to avoid late fees or legal action. Ensuring a valid signature is essential for a check to be considered a legally binding instrument for financial transactions.

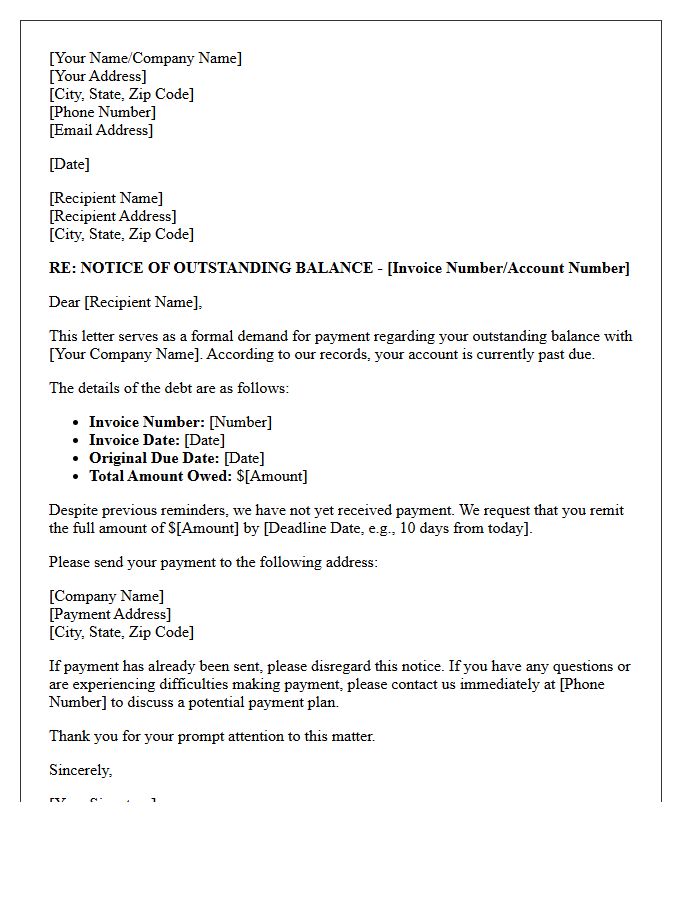

First Demand Letter for Outstanding Balance

A first demand letter is a formal written notice sent to a debtor to request the payment of an outstanding balance. It serves as a professional pre-legal notification, clearly outlining the total amount owed, the original due date, and the expected timeframe for resolution. Sending this document is a critical step in debt collection as it establishes a paper trail for potential litigation while offering the recipient a final opportunity to settle the debt amicably. Most businesses include specific payment instructions and a deadline to encourage an immediate settlement of the arrears.

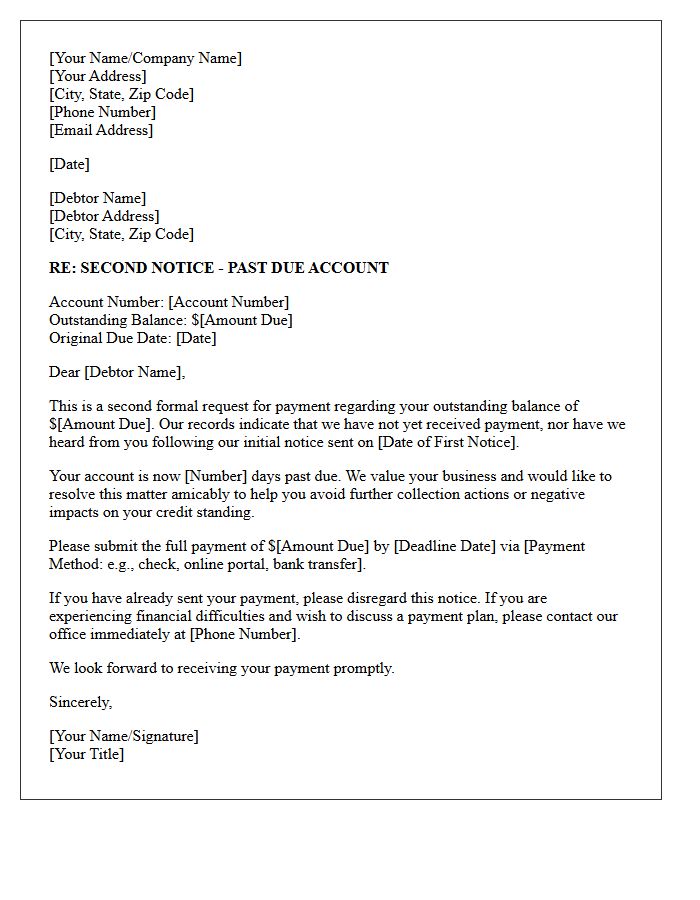

Second Notice Demand Letter for Past Due Account

A Second Notice Demand Letter serves as a final formal warning before escalating debt collection to legal action or credit reporting agencies. This document emphasizes the past due account status, re-stating the total balance, original due date, and any accumulated late fees. It is crucial to maintain professional documentation to prove non-payment in future litigation. Recipients should prioritize immediate communication or settlement to avoid litigation, negative credit impacts, or additional collection costs. Promptly addressing this notice is the last opportunity to resolve the delinquency through a standard payment plan.

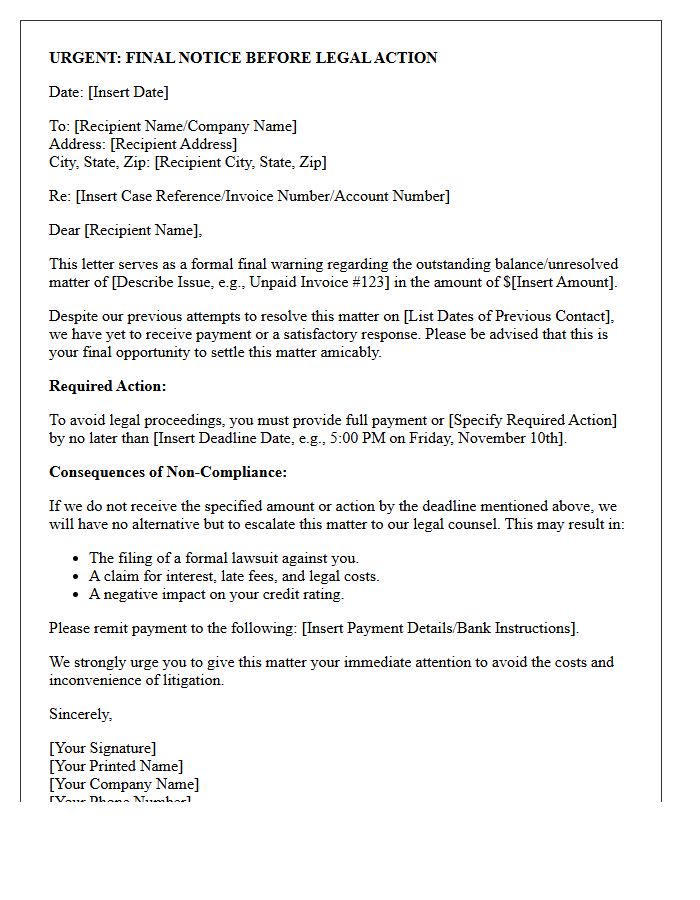

Final Warning Letter Before Legal Action

A Final Warning Letter Before Legal Action, or Letter Before Claim, is a formal notice sent to resolve a dispute before filing a lawsuit. It serves as a last opportunity for the recipient to settle a debt or fulfill an obligation. To be legally effective, it must clearly state the claim details, the specific amount owed, and a firm deadline for payment. Issuing this document is a critical procedural step that demonstrates to the court that you attempted to reach a fair settlement before initiating litigation.

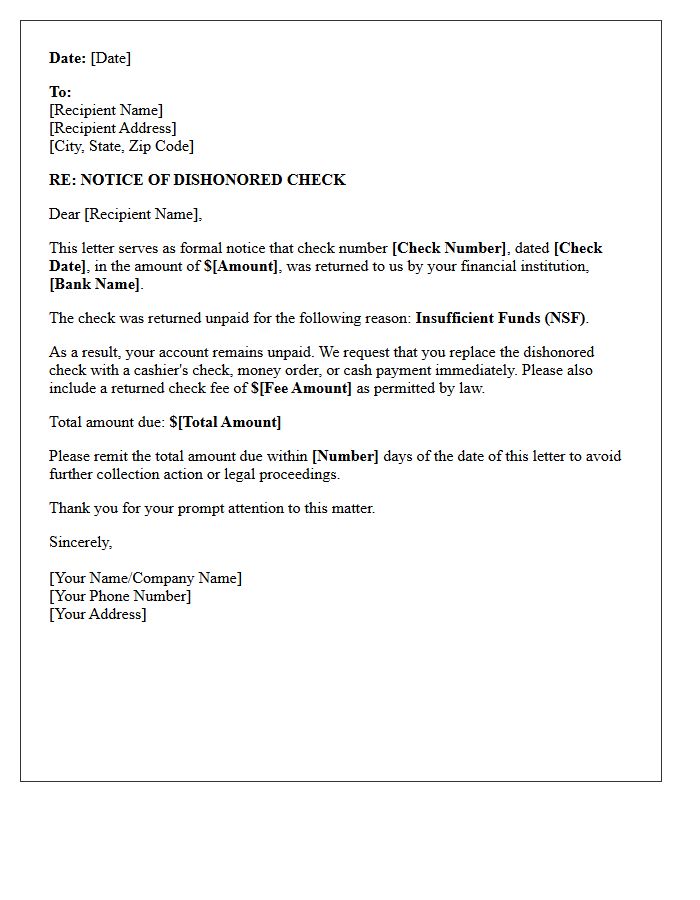

Notice of Dishonored Check Due to Insufficient Funds Letter

A Notice of Dishonored Check Due to Insufficient Funds is a formal demand for payment issued when a bank rejects a transaction. This letter serves as legal evidence that the payee notified the issuer of the bounced check. It typically requests the original amount plus applicable NSF fees within a specific timeframe. Sending this notice via certified mail is crucial for establishing a legal record, which is often required before pursuing civil penalties or criminal charges under state law to recover the debt owed.

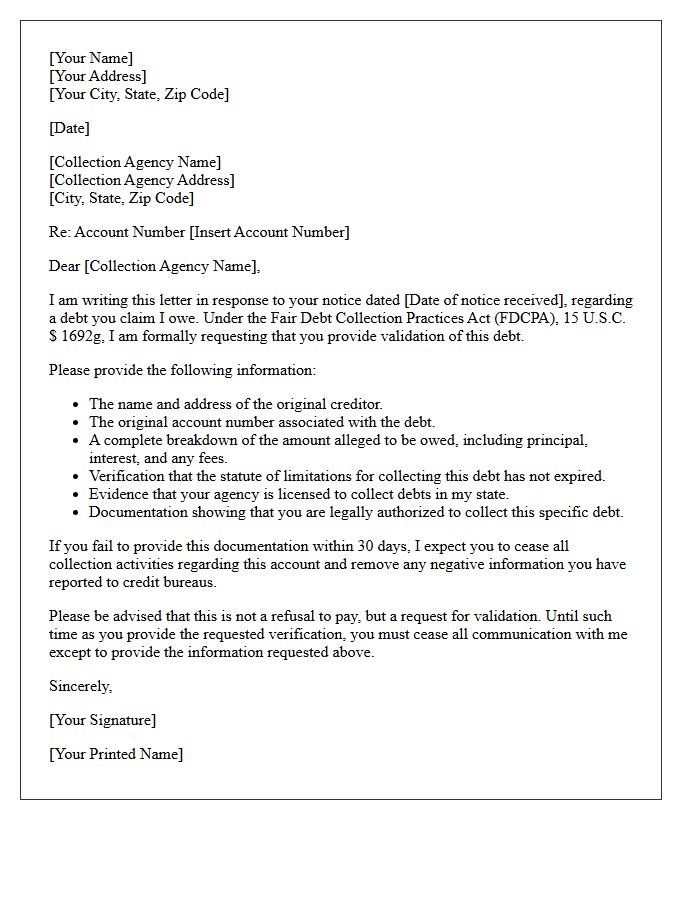

Debt Validation Notice Letter

A Debt Validation Notice is a federally mandated document sent by debt collectors to confirm a consumer's legal obligation. Under the Fair Debt Collection Practices Act (FDCPA), you have thirty days to dispute the claim in writing. This letter must include the total amount owed, the original creditor's name, and instructions on how to challenge the debt's accuracy. Requesting validation protects your rights, stops collection activities temporarily, and ensures you are not paying an expired or fraudulent debt. Always keep copies of this correspondence for your financial records.

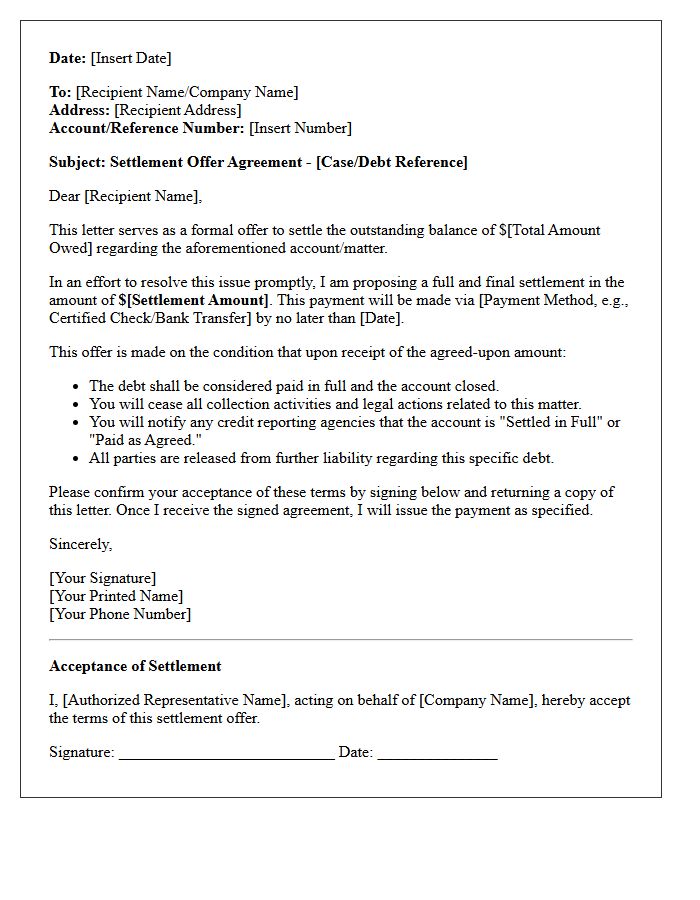

Settlement Offer Agreement Letter

A Settlement Offer Agreement Letter is a formal legal document used to resolve financial disputes or outstanding debts. It outlines a binding proposal where the creditor agrees to accept a reduced sum in exchange for releasing the debtor from further liability. This written proof is essential for legal protection and ensuring the account is marked as satisfied. Always verify that the agreement explicitly states the debt is considered paid in full to prevent future collection actions and protect your credit score from additional negative reporting.

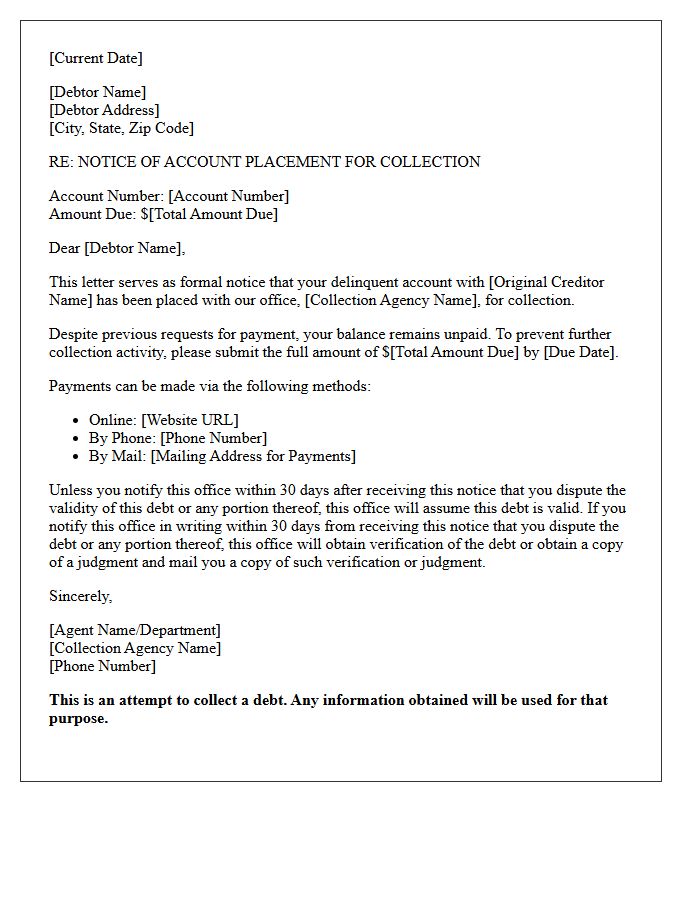

Notice of Account Placement for Collection Letter

A Notice of Account Placement is a formal notification that your delinquent debt has been transferred to a collection agency. Receiving this letter means the original creditor is no longer managing the account, and you must now communicate with the third-party collector. It is crucial to validate the debt in writing within thirty days to ensure accuracy. Ignoring this notice can lead to credit score damage or legal action. Promptly addressing the letter allows you to negotiate a settlement or dispute incorrect information before further recovery efforts occur.

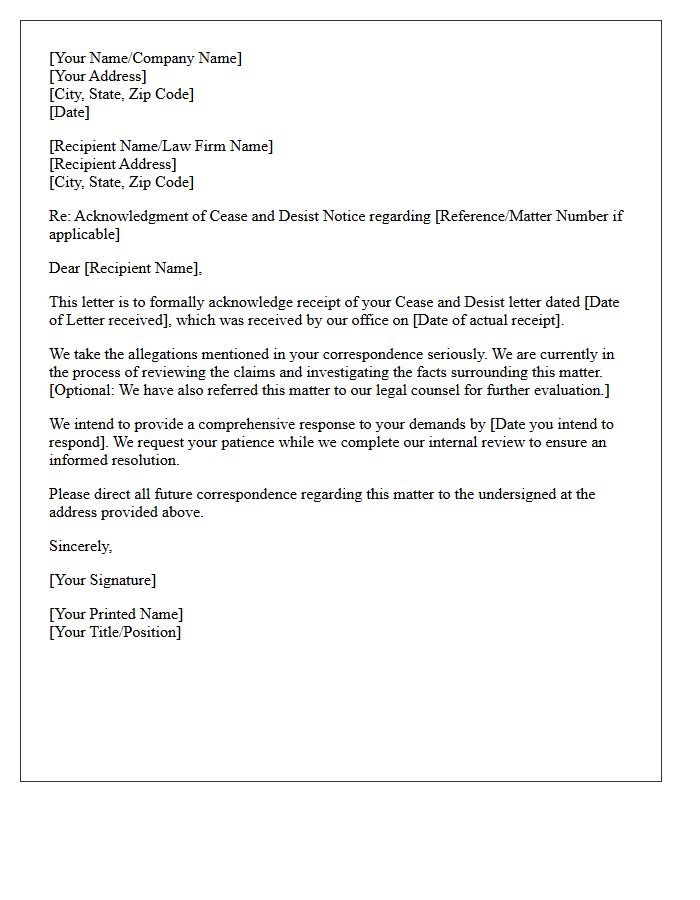

Cease and Desist Acknowledgment Letter

A Cease and Desist Acknowledgment Letter is a formal written response confirming that you have received a demand to stop specific activities. This document is crucial for legal documentation and serves to notify the sender that their request is under review. It does not necessarily imply an admission of guilt but helps establish a professional paper trail. Promptly acknowledging the notice can prevent immediate escalation to litigation while providing time to consult with counsel to evaluate the claims and determine the next legal strategy.

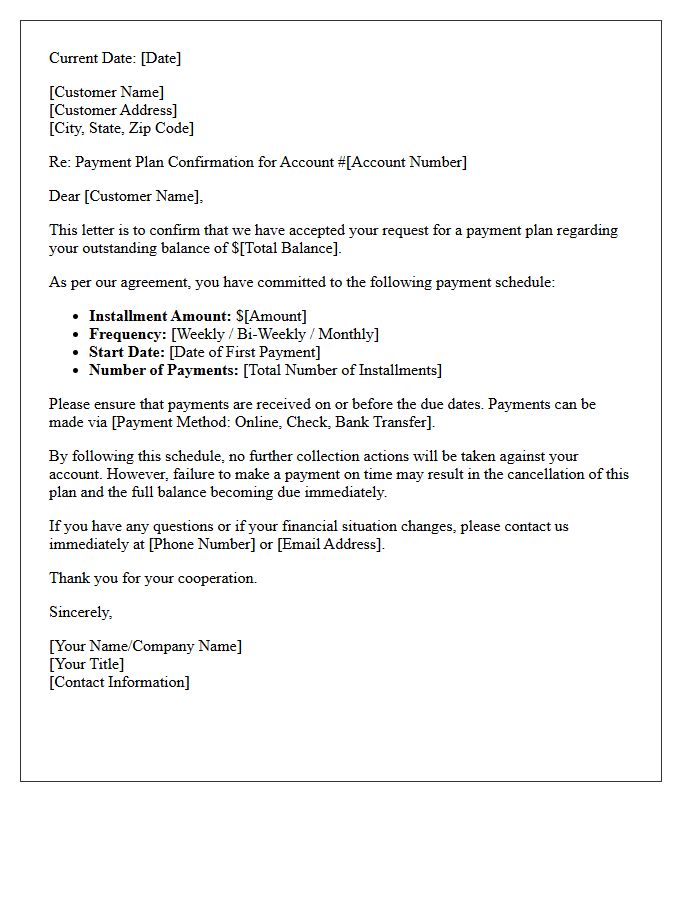

Payment Plan Confirmation Letter

A Payment Plan Confirmation Letter serves as a legally binding document that outlines a formal agreement between a debtor and a creditor. This essential record specifies the repayment schedule, including installment amounts, due dates, and applicable interest rates. It provides financial clarity for both parties, ensuring terms are transparent and documented to prevent future disputes. Always verify that the letter includes the total outstanding balance and specific methods of payment to maintain a professional record of your commitment to debt resolution and financial accountability.

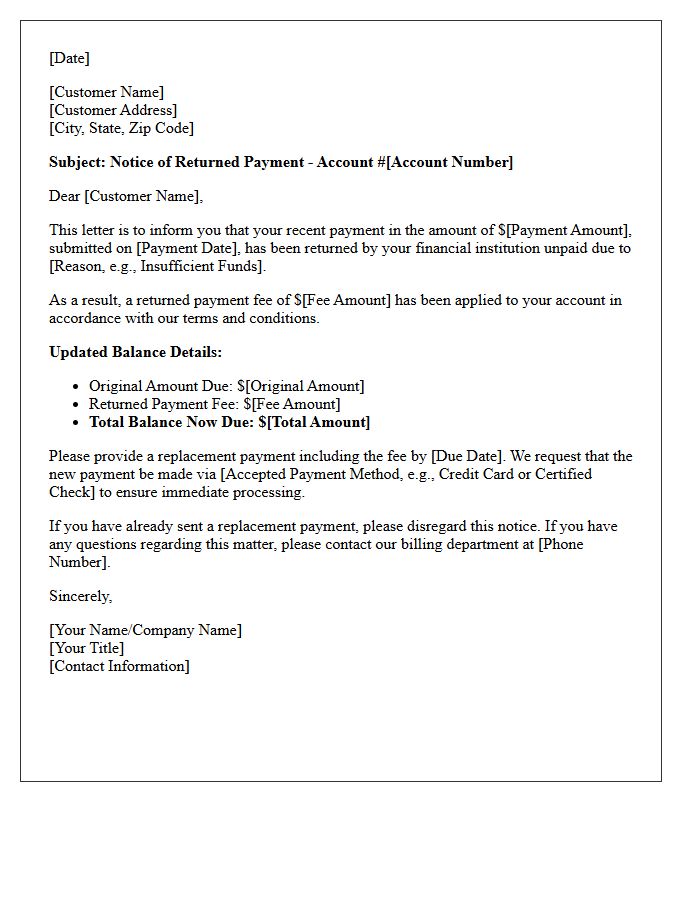

Notice of Returned Payment Fee Letter

A Notice of Returned Payment Fee Letter is a formal notification sent when a transaction is rejected due to insufficient funds or incorrect account details. This document serves as a legal record informing the payer that their payment failed and a penalty has been applied. It typically outlines the original amount owed, the additional service charge, and the new total balance. Timely action is required to settle the debt and avoid further late fees, service interruptions, or negative impacts on your credit score and financial standing with the creditor.

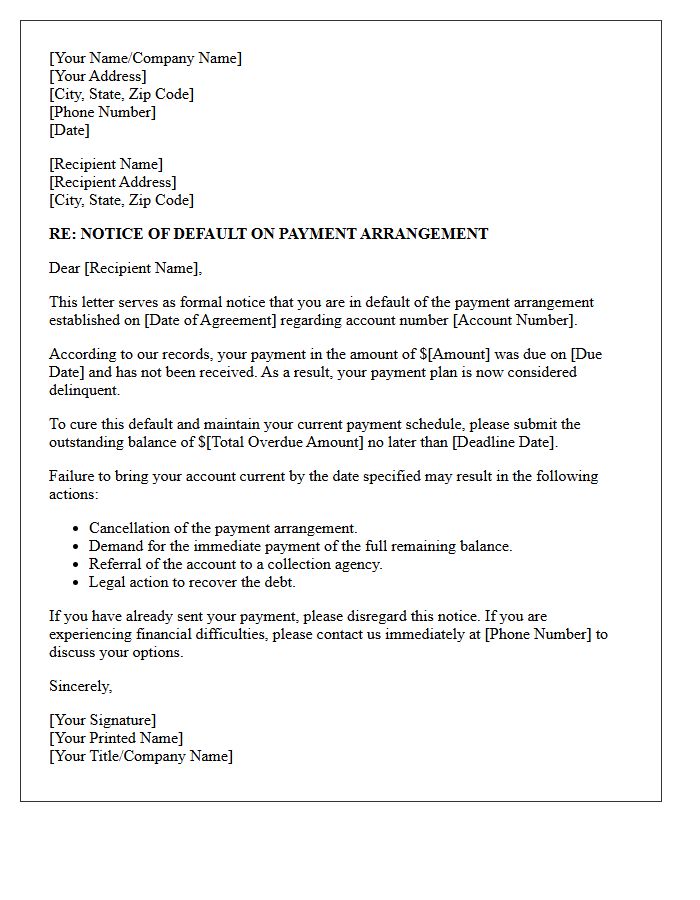

Notice of Default on Payment Arrangement Letter

A Notice of Default on Payment Arrangement Letter is a formal warning issued when a debtor fails to meet agreed installment terms. This document serves as legal evidence that the repayment contract has been breached. It typically outlines the missed amount, applicable late fees, and a final deadline to rectify the delinquency. Receiving this notice is critical because it often precedes aggressive debt collection, legal action, or the termination of services. Promptly addressing the default is essential to protect your credit score and avoid further financial penalties.

What is a Notice of Dishonored Check Due to Missing Signature?

A Notice of Dishonored Check Due to Missing Signature is a formal notification sent by a payee to a drawer stating that their bank refused to process a check because it was not signed. This document requests that the drawer provide a valid replacement check or an alternative form of payment immediately.

How do I respond to a notice for a missing signature on a check?

To respond, you should contact the recipient immediately to acknowledge the error. You must issue a new, signed check or provide a secure payment method such as a wire transfer or certified funds. Most jurisdictions require you to rectify the payment within a specific timeframe (usually 10 to 30 days) to avoid legal penalties.

Are there bank fees associated with a check dishonored for a missing signature?

Yes, both the drawer (the person who wrote the check) and the payee (the person receiving it) may be charged "returned item" or "non-sufficient funds" (NSF) fees by their respective banks. In a notice of dishonor, the payee often requests that the drawer reimburse them for these specific bank charges.

Is a check without a signature considered a legal payment?

No, a check is not a valid negotiable instrument under the Uniform Commercial Code (UCC) unless it bears the authorized signature of the drawer. A check without a signature is legally incomplete and cannot be processed by financial institutions until the signature requirement is satisfied.

Can I be sued for a check dishonored due to a missing signature?

Yes, if you fail to provide a replacement payment after receiving a formal notice of dishonor, the payee can file a civil lawsuit to recover the original amount plus damages. While a missing signature is often a clerical error, failure to correct it may be treated similarly to a "bad check" or "bounced check" in a court of law.

Comments