Receiving a Notice of Debt Validation Investigation Results is a critical step in resolving financial disputes. This document confirms whether a debt collector has verified the accuracy and legality of a reported balance. Understanding these findings helps you protect your consumer rights and decide on further legal or credit actions. To help you respond effectively, below are some ready to use template.

Image cover: Debt Validation Results: Professional Templates and Notice Guide

Letter Samples List

- Notice Of Debt Validation Investigation Results Letter

- Verified Debt Validation Investigation Conclusion Letter

- Notice Of Invalidated Debt Following Investigation Letter

- Fraud Claim Investigation Results And Debt Validation Letter

- Identity Theft Investigation And Debt Invalidation Letter

- Creditor Verification And Debt Validation Results Letter

- Insufficient Documentation And Debt Validation Dismissal Letter

- Notice Of Partial Debt Validation Investigation Results Letter

- Final Investigation Results And Debt Validation Notice Letter

- Dispute Resolution And Debt Validation Investigation Letter

- Account Verification And Debt Validation Findings Letter

- Debt Validation Investigation Results And Account Closure Letter

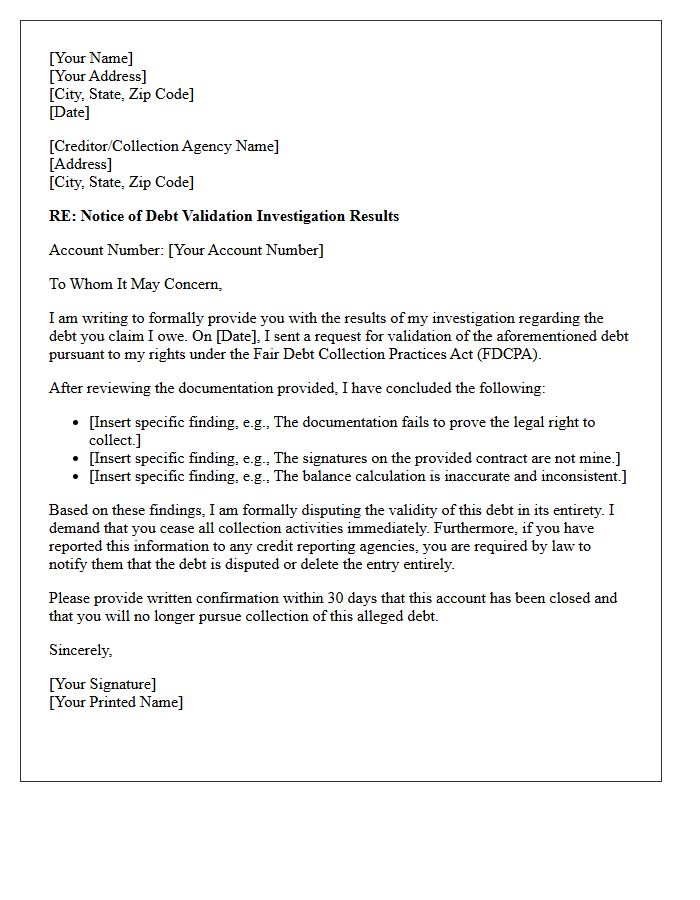

Notice Of Debt Validation Investigation Results Letter

A Notice of Debt Validation Investigation Results Letter confirms whether a disputed debt is legally verifiable. After a consumer challenges a claim, the collection agency must provide documented evidence of the balance, original creditor, and legal right to collect. If the agency fails to validate the debt, they must cease all collection activities and remove the entry from your credit report. Always review these results carefully to ensure accuracy and protect your financial rights under the Fair Debt Collection Practices Act (FDCPA).

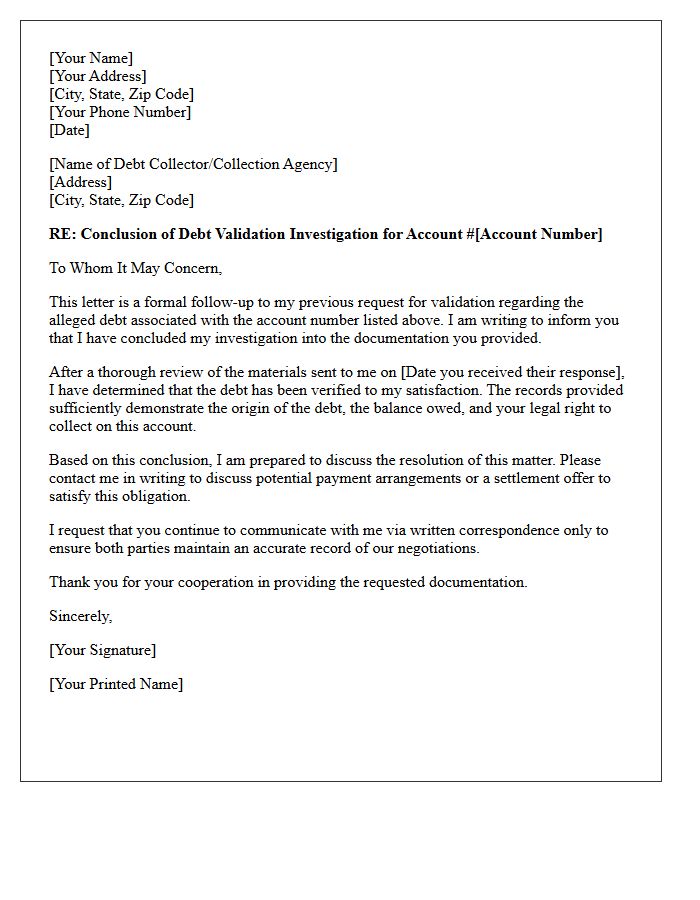

Verified Debt Validation Investigation Conclusion Letter

A Verified Debt Validation Investigation Conclusion Letter is a formal document from a collection agency confirming that a debt is legitimate. It serves as legal proof that the collector has verified the account details, original creditor information, and the total amount owed. Receiving this letter means the collector has fulfilled their legal obligation under the Fair Debt Collection Practices Act (FDCPA). You should carefully review the attached documentation to ensure all figures are accurate before deciding to pay, dispute further, or negotiate a settlement to protect your credit score.

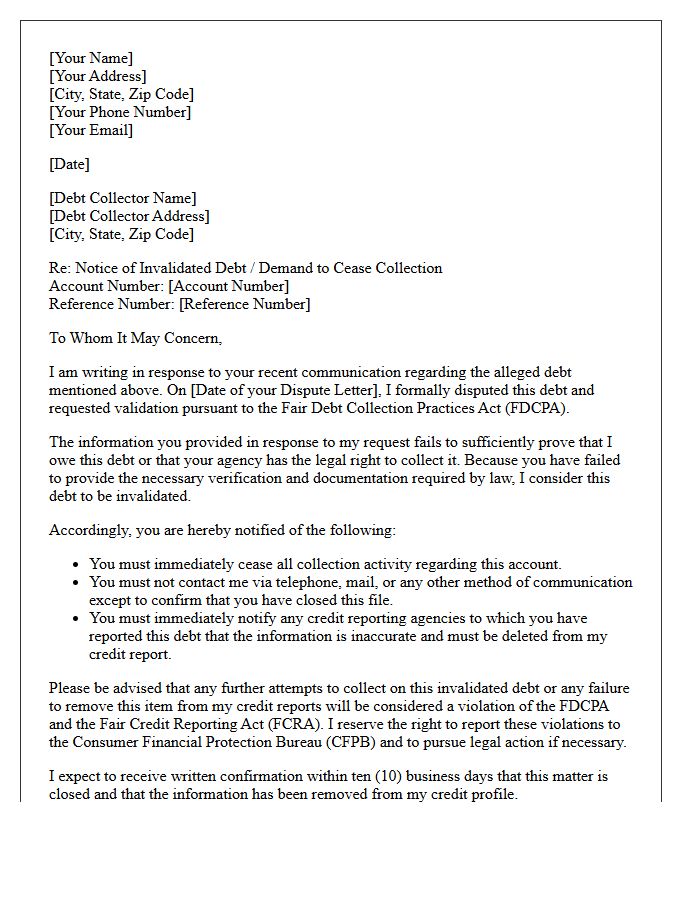

Notice Of Invalidated Debt Following Investigation Letter

A Notice Of Invalidated Debt Following Investigation is a critical legal document confirming that a debt collector failed to verify a disputed account. Under the Fair Debt Collection Practices Act (FDCPA), if a collector cannot provide proof of ownership or accurate records, they must cease collection efforts. Receiving this letter means you are no longer legally obligated to pay the specific entity, and they must remove any negative remarks from your credit report. Retain this document permanently as evidence to protect your financial rights and prevent future collection attempts on the same debt.

Fraud Claim Investigation Results And Debt Validation Letter

A fraud claim investigation determines if unauthorized activity occurred on your account. If the bank denies your claim, you must act quickly to protect your rights. Requesting a debt validation letter is a critical next step, as it legally requires creditors to provide documented proof that you owe the specific amount. Under the Fair Debt Collection Practices Act (FDCPA), this process ensures accuracy and prevents collectors from pursuing fraudulent charges. Always review investigation results carefully and use validation requests to challenge unverified debts and maintain your financial integrity.

Identity Theft Investigation And Debt Invalidation Letter

An Identity Theft Investigation is the essential legal process of verifying fraudulent activity to clear your name. Victims must submit a formal Debt Invalidation Letter to creditors and bureaus to dispute unauthorized charges. This document asserts your rights under the Fair Credit Reporting Act, demanding that collectors prove the debt's legitimacy. Providing a police report and a signed affidavit ensures the investigation leads to the removal of fraudulent accounts from your credit profile, protecting your financial future from long-term damage caused by criminal impersonation.

Creditor Verification And Debt Validation Results Letter

A Debt Validation Results Letter is a critical document sent by a collection agency to prove their legal right to collect. This verification process ensures the debt is accurate, timely, and belongs to you. Under the Fair Debt Collection Practices Act, collectors must provide the original creditor's name and the total balance owed. Reviewing these results allows you to dispute errors or identity theft. If a collector fails to provide sufficient evidence, they must cease all collection activities, protecting your consumer rights and credit score integrity.

Insufficient Documentation And Debt Validation Dismissal Letter

An Insufficient Documentation and Debt Validation Dismissal Letter is a formal legal tool used to challenge unverified claims. Under the Fair Debt Collection Practices Act (FDCPA), collectors must provide competent evidence of the original contract and balance accuracy. If a creditor fails to produce these records, this letter demands an immediate case dismissal and removal from credit reports. Sending this notice protects your rights by forcing the collector to prove the debt's legitimacy or cease all collection activities due to a lack of legal standing.

Notice Of Partial Debt Validation Investigation Results Letter

A Notice of Partial Debt Validation Investigation Results Letter confirms that a debt collector verified only a portion of a disputed balance. Under the Fair Debt Collection Practices Act, this document specifies which parts of the debt are deemed valid and which were corrected or removed. It is crucial to review the itemized breakdown to ensure accuracy. If you still disagree with the remaining balance, you must submit a written dispute within thirty days to protect your consumer rights and prevent inaccurate reporting on your credit file.

Final Investigation Results And Debt Validation Notice Letter

A Debt Validation Notice is a critical legal document sent by collectors to verify a debt's legitimacy. Upon receiving it, you have thirty days to submit a Debt Validation Letter to dispute errors or request proof of ownership. The Final Investigation Results conclude this process, confirming if the debt is verified, corrected, or must be deleted. Understanding these documents ensures consumer protection under the FDCPA, preventing unlawful collection efforts and protecting your credit report from inaccurate negative marks. Always keep copies of all correspondence for your financial records.

Dispute Resolution And Debt Validation Investigation Letter

A Debt Validation Investigation Letter is a critical legal tool used to dispute unverified claims under the Fair Debt Collection Practices Act. By sending this formal written request, you compel collection agencies to provide documented proof of the debt's accuracy and their legal right to collect it. If the collector fails to verify the account within thirty days, they must cease all collection activities. Utilizing this dispute resolution method protects your consumer rights, prevents fraudulent reporting, and ensures your credit profile remains accurate against unsubstantiated or expired financial claims.

Account Verification And Debt Validation Findings Letter

An Account Verification and Debt Validation Findings Letter is a formal response from a creditor or collection agency confirming the legitimacy of a debt. This document validates the balance, original creditor details, and payment history after a consumer challenge. Receiving this letter means the agency has provided evidence to support their claim, shifting the burden back to the debtor to either pay or provide further proof of inaccuracy. It is a critical component of debt collection compliance under the Fair Debt Collection Practices Act to ensure consumer protection and financial transparency.

Debt Validation Investigation Results And Account Closure Letter

A Debt Validation Investigation is a legal process where a consumer demands proof that a debt is valid and accurate. If the collection agency fails to provide verified evidence or discovers errors, they must cease collection activities. Receiving an Account Closure Letter serves as formal confirmation that the investigation concluded in your favor. This document is vital for your financial records, as it ensures the erroneous debt is permanently removed from your credit report, preventing future collection attempts and protecting your overall credit score from further damage.

What is a Notice of Debt Validation Investigation Results?

A Notice of Debt Validation Investigation Results is a formal document sent by a debt collector or credit bureau informing a consumer of the outcome of an inquiry into a disputed debt. It confirms whether the debt has been verified as accurate, corrected, or deleted from the records based on provided evidence.

How long does a debt collector have to provide investigation results?

Under the Fair Debt Collection Practices Act (FDCPA), once a consumer submits a written dispute within the initial 30-day validation period, the collector must cease collection efforts until they provide verification. Generally, credit bureaus have 30 to 45 days to complete an investigation and notify the consumer of the results.

What does it mean if my debt was "verified" during the investigation?

If a debt is "verified," it means the collector has provided sufficient documentation-such as a copy of the original contract or a final billing statement-to prove that the consumer owes the debt and that the amount is correct. Following verification, the collector is legally permitted to resume collection activities.

What should I do if the investigation results are inaccurate?

If the investigation results are still incorrect, you can submit a secondary dispute with additional evidence, file a complaint with the Consumer Financial Protection Bureau (CFPB), or contact the original creditor. You also have the right to add a 100-word statement to your credit report explaining the discrepancy.

Can a debt be re-reported after it is deleted following an investigation?

Yes, a debt can be re-reported, but only if the data furnisher certifies that the information is 100% accurate and complete. If a credit bureau re-inserts a previously deleted item, they are legally required to notify the consumer in writing within five business days.

Comments