Receiving a Notice of Rejected Identity Theft Dispute can be frustrating when trying to clear your credit report. This response indicates that creditors or credit bureaus require additional evidence to prove the fraudulent activity. Understanding why your claim was denied is the first step toward a successful appeal. To help you respond effectively, below are some ready to use templates.

Image cover: Rejection of Identity Theft Dispute: Response Strategies and Official Templates

Letter Samples List

- Notice of Rejected Identity Theft Dispute Response Letter

- Debt Collection Identity Theft Claim Denial Letter

- Insufficient Evidence Identity Theft Dispute Rejection Letter

- Incomplete Identity Theft Affidavit Rejection Letter

- Unverified Fraud Dispute Response and Rejection Letter

- Invalid Identity Theft Claim Notice Letter

- Absence of Police Report Identity Theft Rejection Letter

- Rejected Identity Theft Investigation Response Letter

- Account Collection Identity Theft Dispute Denial Letter

- Fraud Dispute Rejection and Collection Resumption Letter

- Unsubstantiated Identity Theft Dispute Response Letter

- Notice of Declined Identity Theft Resolution Letter

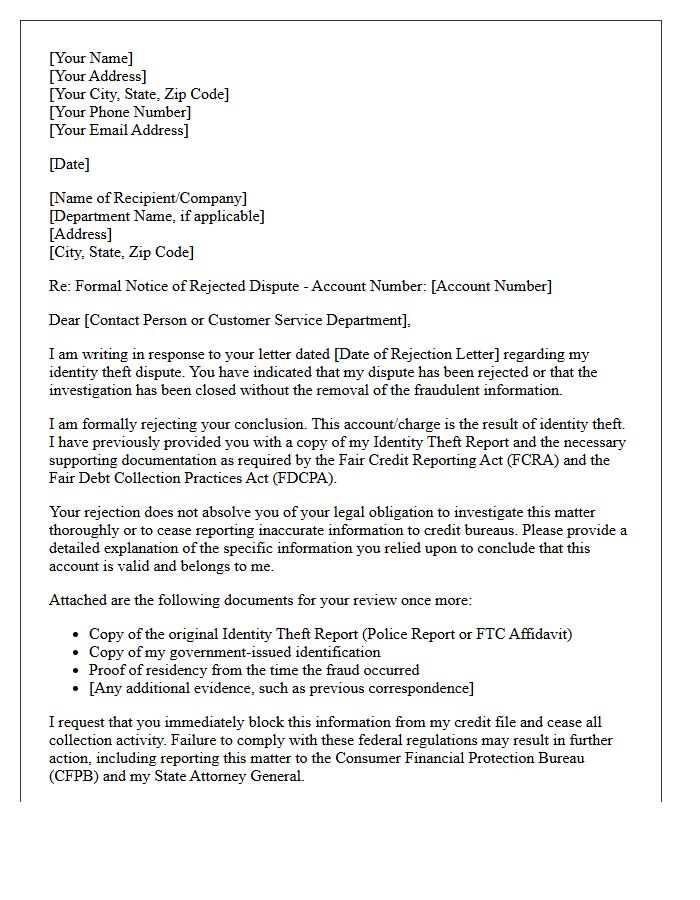

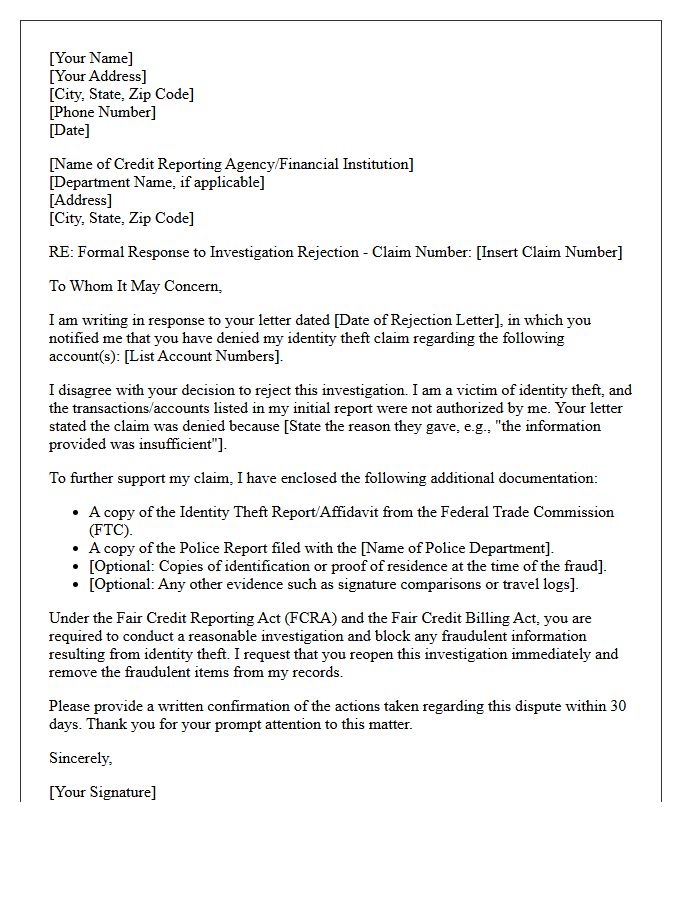

Notice of Rejected Identity Theft Dispute Response Letter

Receiving a Notice of Rejected Identity Theft Dispute means a credit bureau or creditor has denied your claim after reviewing your identity theft report. This letter typically indicates that the documentation provided was insufficient or that the business believes the account is valid. It is crucial to act quickly by requesting the specific evidence used for the denial. You should provide additional proof, such as a police report or an FTC Identity Theft Affidavit, to strengthen your case and resubmit the dispute to protect your credit score.

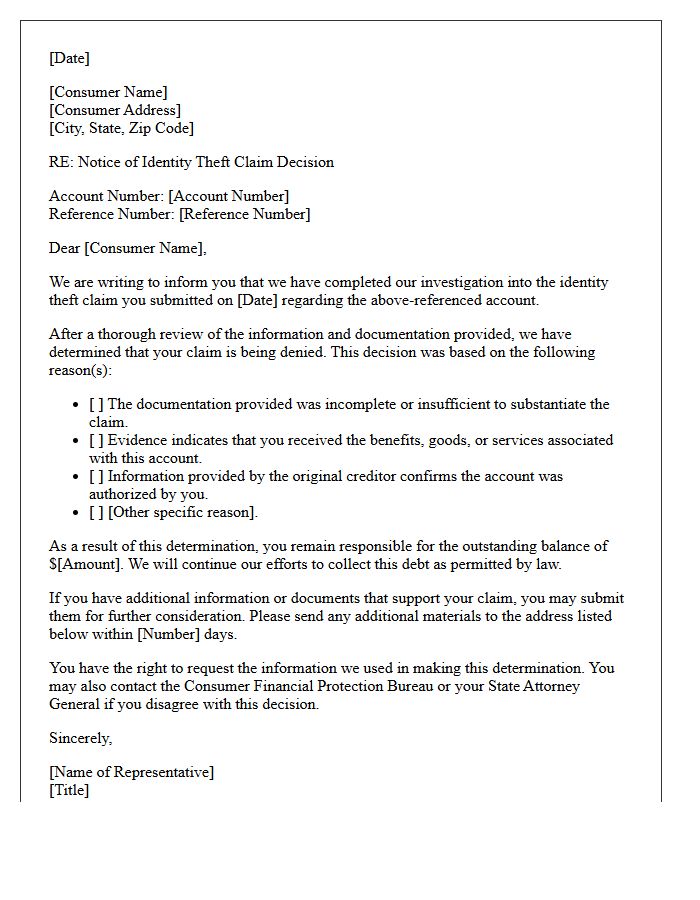

Debt Collection Identity Theft Claim Denial Letter

Receiving a Debt Collection Identity Theft Claim Denial Letter means the collector rejected your dispute due to insufficient evidence or inconsistencies. This formal notice typically states that they believe the debt is validly yours despite your fraud report. To protect your credit, you must immediately provide a sworn police report and a completed FTC Identity Theft Report. Reviewing the specific reason for denial is crucial to filing a reinvestigation request or a formal complaint with the CFPB to clear your financial record and stop further collection actions.

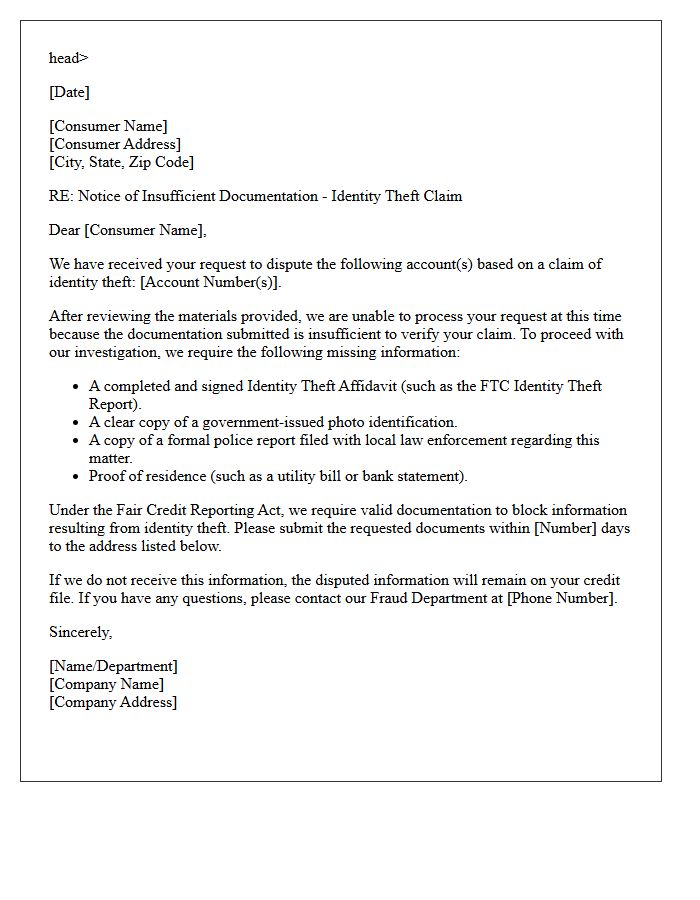

Insufficient Evidence Identity Theft Dispute Rejection Letter

Receiving an Insufficient Evidence rejection letter means the credit bureau or creditor determined your identity theft claim lacks enough documentation to prove fraud. To successfully dispute this, you must provide a FTC Identity Theft Report or a formal police report as concrete proof. Simply stating a transaction is unauthorized is often inadequate. You should resubmit your request with clear identification, specific account details, and any supporting affidavits. Strengthening your evidence trail is the most effective way to overturn a denial and restore your credit accuracy.

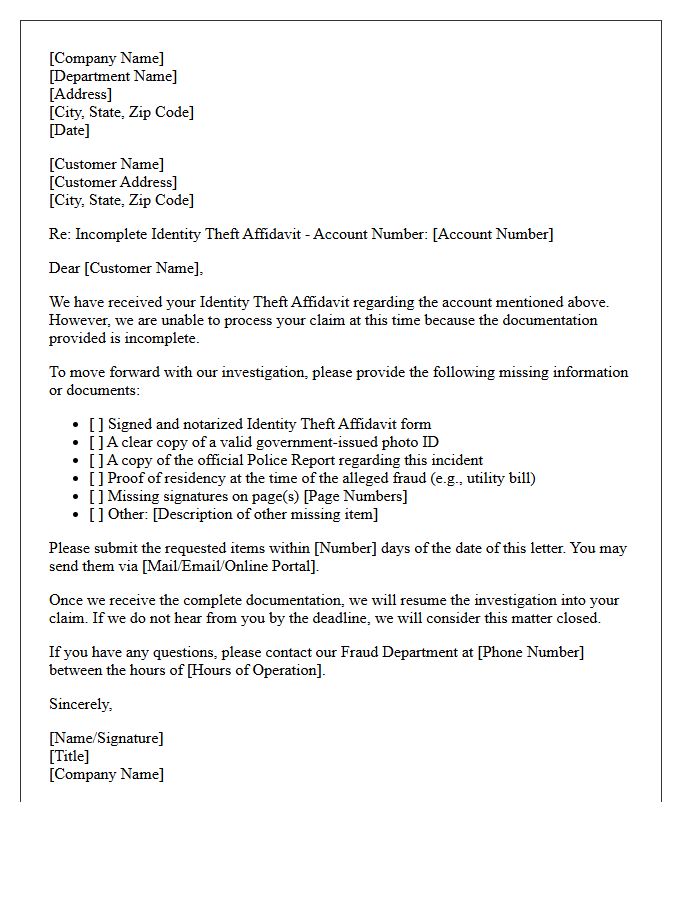

Incomplete Identity Theft Affidavit Rejection Letter

Receiving an Incomplete Identity Theft Affidavit Rejection Letter means the FTC or financial institution could not process your claim due to missing information. This formal notice typically indicates a lack of supporting documentation, such as a police report, valid government ID, or specific transaction details. To resolve this, you must promptly provide the required evidence to restore your legal protections. Failing to address these deficiencies can delay the removal of fraudulent charges from your credit report and hinder the restoration of your financial security and identity rights.

Unverified Fraud Dispute Response and Rejection Letter

An Unverified Fraud Dispute Response and Rejection Letter is a formal notification issued by a financial institution to deny a claim. It occurs when investigations conclude that the reported activity was authorized or lacks sufficient evidence of criminal intent. To avoid liability, consumers must provide specific documentation, such as police reports or proof of compromised credentials. Understanding the rejection reason is critical for filing an appeal. Clear communication ensures both parties adhere to legal protections under Regulation E while preventing potential first-party fraud or errors in the dispute process.

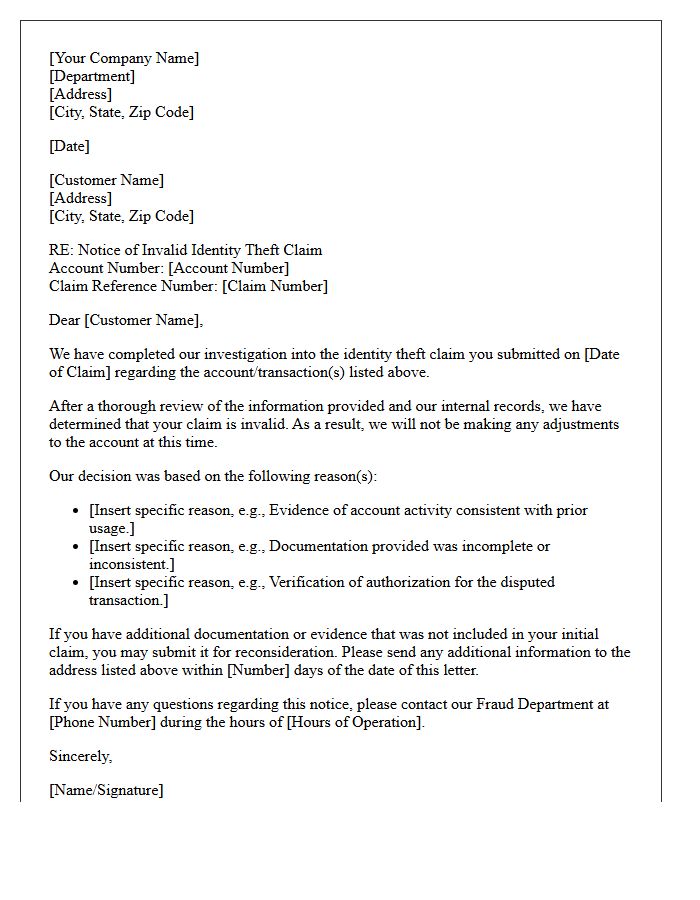

Invalid Identity Theft Claim Notice Letter

An Invalid Identity Theft Claim Notice is a formal letter from a creditor or credit bureau stating that your fraud report lacks sufficient evidence. It signifies that your dispute was denied because the provided documentation, such as an identity theft report or police affidavit, failed to meet legal requirements. To resolve this, you must quickly provide additional proof of the crime to restore your protections under the Fair Credit Reporting Act. Failure to respond may result in the fraudulent debt remaining on your credit report and impacting your financial standing.

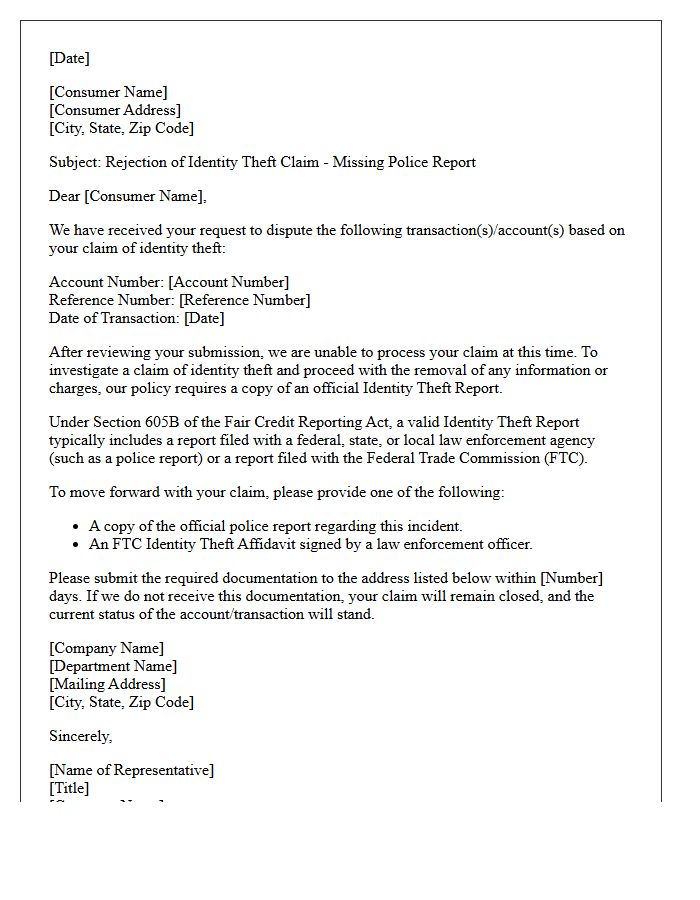

Absence of Police Report Identity Theft Rejection Letter

Receiving an identity theft rejection letter due to the absence of a police report is a common obstacle. Creditors often deny fraud claims if you fail to provide official law enforcement documentation. To resolve this, you must file a FTC Identity Theft Report or a local police report to validate your case. Submitting this official proof forces creditors to investigate under federal law. Without this supporting evidence, protecting your credit score and disputing fraudulent charges becomes significantly more difficult, as institutions may view your claim as unsubstantiated.

Rejected Identity Theft Investigation Response Letter

Receiving a Rejected Identity Theft Investigation Response Letter means a credit bureau or creditor has denied your claim after reviewing the submitted evidence. This typically occurs due to insufficient documentation or inconsistent police reports. To challenge this, you must quickly provide additional proof, such as utility bills or identity affidavits, to verify the fraudulent activity. Understanding the specific reason for denial is crucial for a successful appeal. Acting promptly helps restore your credit accuracy and ensures your legal rights under the Fair Credit Reporting Act are fully protected.

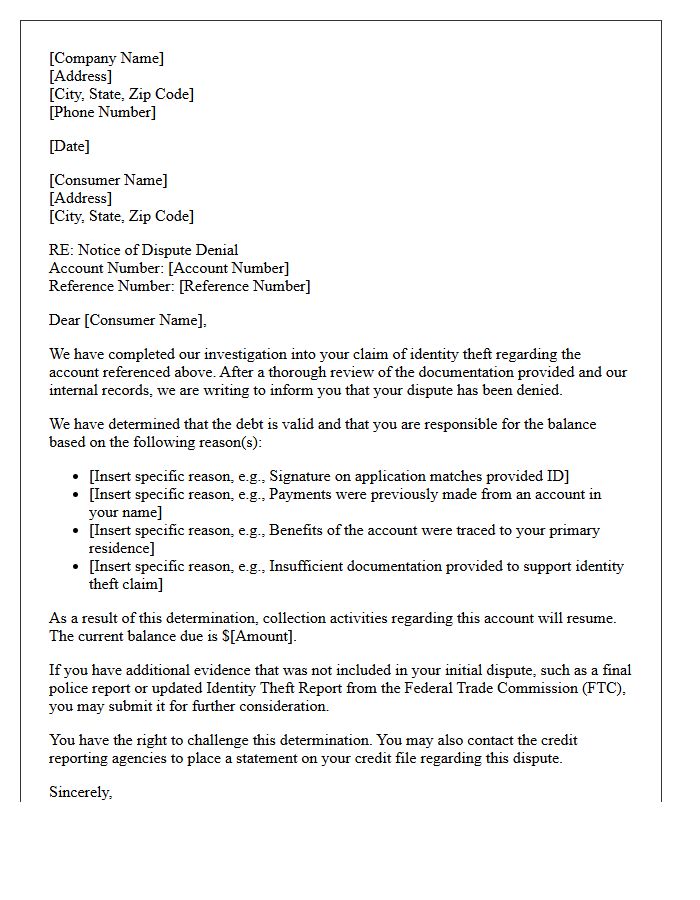

Account Collection Identity Theft Dispute Denial Letter

Receiving an Account Collection Identity Theft Dispute Denial Letter means a creditor or bureau rejected your claim of fraudulent activity. This occurs if provided evidence was insufficient or the account appears verified. To resolve this, you must immediately request the specific documents used for verification and file a formal police report or FTC Identity Theft Report if not already done. Consistently challenging the denial with additional proof is essential to clear your credit report and stop collection efforts on accounts you did not open.

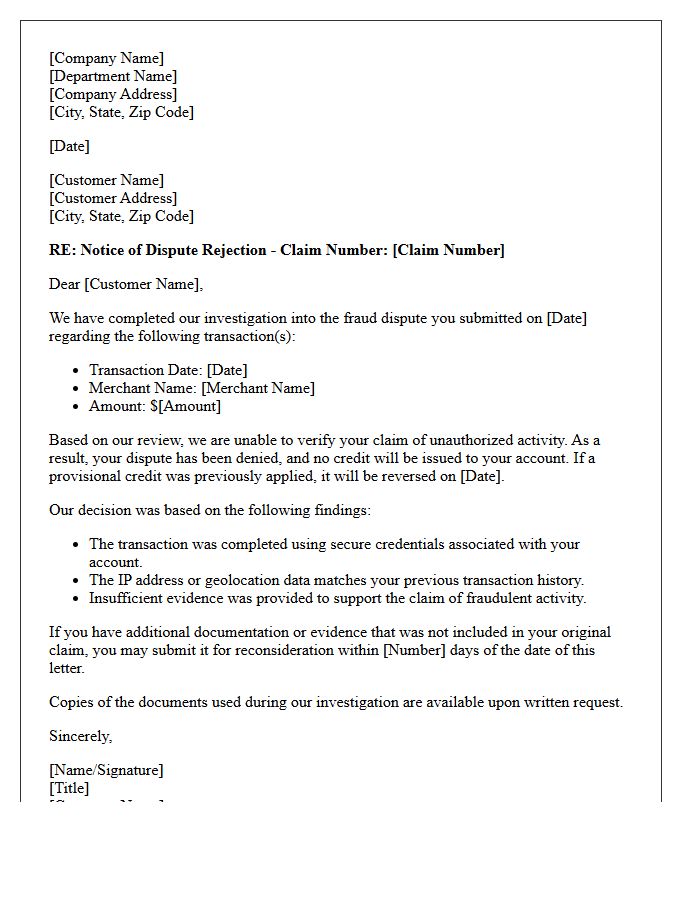

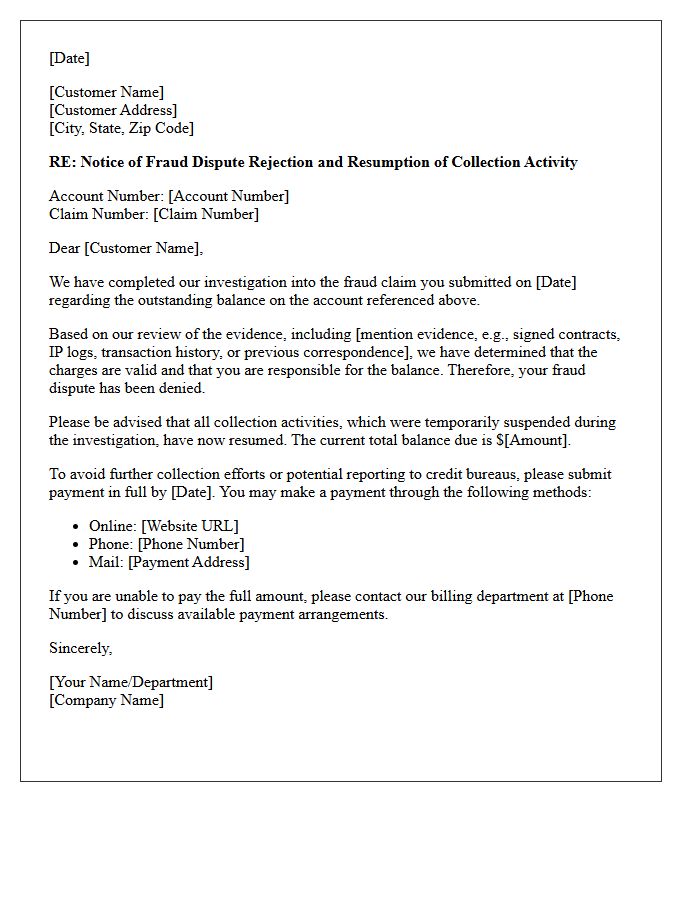

Fraud Dispute Rejection and Collection Resumption Letter

A Fraud Dispute Rejection letter notifies you that your claim was denied after a formal investigation. This typically happens due to insufficient evidence or validation of the transaction. Consequently, collection resumption occurs, meaning the creditor will restart efforts to recover the outstanding balance. It is crucial to review the stated reasons for denial immediately. You may have a limited window to provide additional documentation or appeal the decision to prevent further negative impacts on your credit score and avoid potential legal escalation from the recovery department.

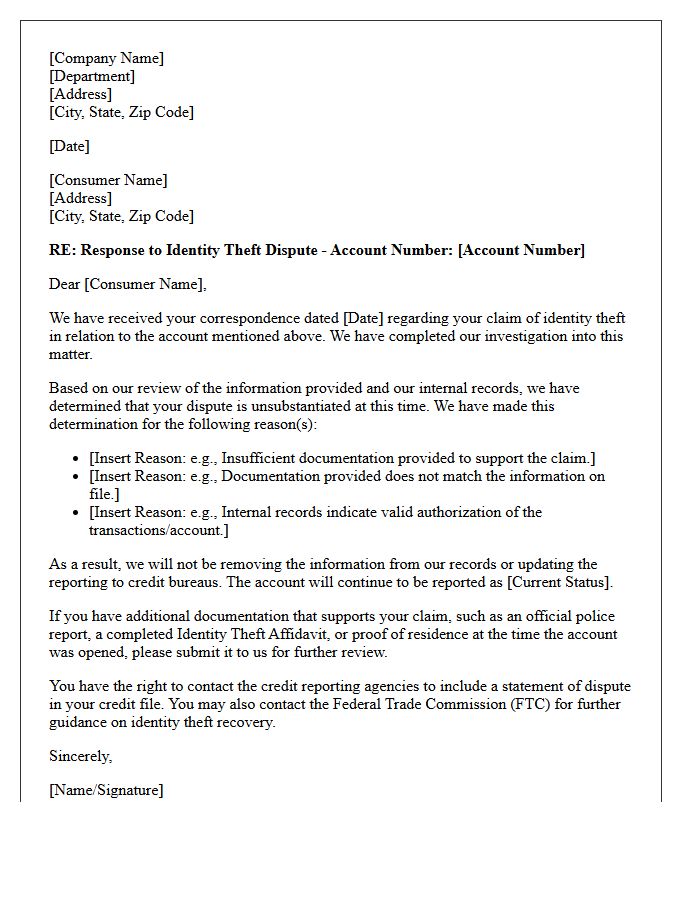

Unsubstantiated Identity Theft Dispute Response Letter

Receiving an unsubstantiated identity theft dispute response letter from a credit bureau means your claim was rejected due to insufficient evidence. To overturn this decision, you must provide a formal identity theft report or a completed FTC affidavit. Simply stating fraud occurred is rarely enough; bureaus require validated documentation to legally remove fraudulent accounts. Carefully review the specific reasons for denial mentioned in the notice, then resubmit your dispute with official police reports and clear proof of your true identity to ensure your consumer rights are protected.

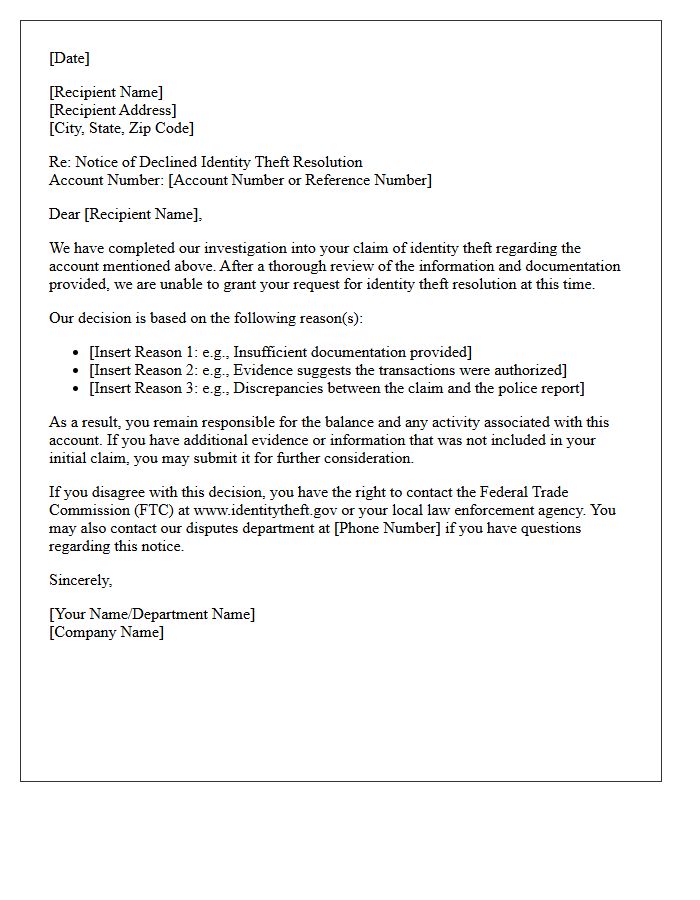

Notice of Declined Identity Theft Resolution Letter

A Notice of Declined Identity Theft Resolution Letter informs a claimant that their fraud claim has been rejected by a financial institution. This formal document typically states that the investigation found insufficient evidence to prove unauthorized activity. It is crucial to review the provided reasoning immediately, as you have the right to request the specific documents used in the decision. To contest the denial, you must submit additional documentation, such as a formal police report or an updated identity theft affidavit, to provide further proof of the incident.

What is a Notice of Rejected Identity Theft Dispute?

A Notice of Rejected Identity Theft Dispute is a formal communication from a credit reporting agency or creditor stating that they have reviewed your claim of identity theft but determined that the disputed information will not be removed from your record.

Why was my identity theft dispute rejected?

Disputes are commonly rejected if the documentation provided-such as an Identity Theft Report or police report-is incomplete, if the information is deemed "frivolous," or if the creditor provides proof that the account or transaction genuinely belongs to you.

What should I do if my identity theft dispute is denied?

If your dispute is denied, you should request the specific evidence used to make the decision, provide additional supporting documentation (such as utility bills or affidavits), and resubmit the dispute or file a complaint with the Consumer Financial Protection Bureau (CFPB).

Does a rejected dispute mean the debt is my responsibility?

A rejection means the credit bureau or creditor currently considers the debt valid; however, it does not legally finalize your liability. You maintain the right to appeal the decision, seek legal counsel, or provide further evidence to prove the debt resulted from fraudulent activity.

How can I improve my documentation for a resubmitted identity theft dispute?

To strengthen a resubmission, include a formal FTC Identity Theft Report, a specific police report number, copies of government-issued identification, and any correspondence from the merchant acknowledging potential fraud or unauthorized account opening.

Comments