Protect your financial rights by formally challenging predatory practices with a Response to Unlawful Debt Collection Dispute Notice. This essential legal document asserts your protections under consumer law, demanding verification and stopping harassment from non-compliant agencies. Effectively contest invalid claims and maintain your credit integrity. To help you get started, below are some ready to use template.

Image cover: Professional Dispute Response Guide: Managing Unlawful Debt Collection Templates

Letter Samples List

- Debt Validation Response Letter

- Acknowledgment of Dispute and Cease Communication Letter

- Request for Additional Fraud Documentation Letter

- Notice of Account Closure and Bureau Deletion Letter

- Rebuttal of Unlawful Collection Allegations Letter

- Verification of Debt Accuracy and Compliance Letter

- Identity Theft Investigation Resolution Letter

- Notice of Incomplete Dispute Information Letter

- Confirmation of Account Status and Balance Letter

- Original Creditor Documentation Forwarding Letter

- Notification of Debt Recall by Original Creditor Letter

- Fair Debt Collection Practices Act Compliance Explanation Letter

- Time-Barred Debt Acknowledgment Letter

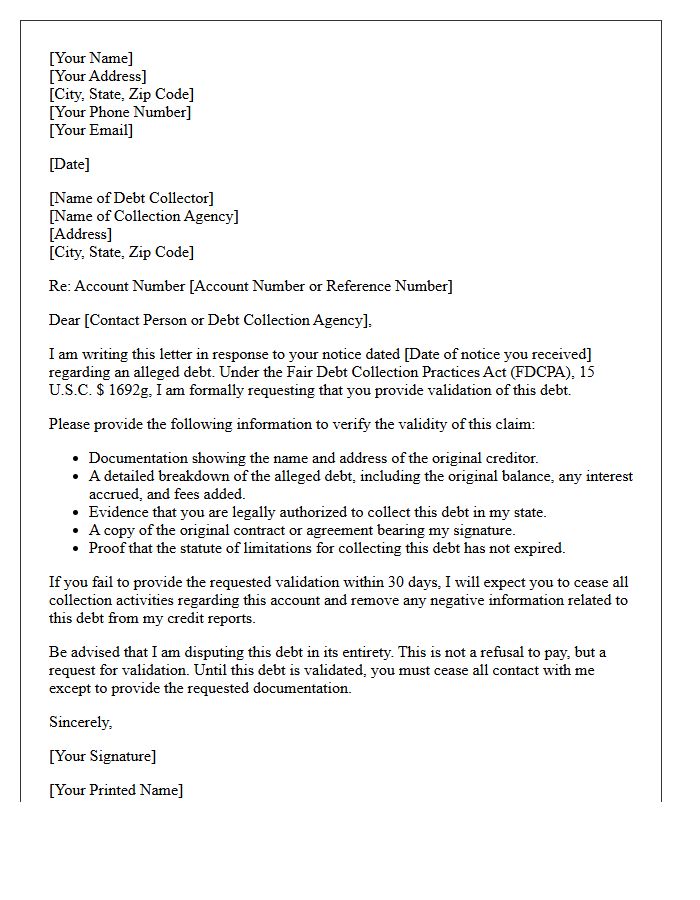

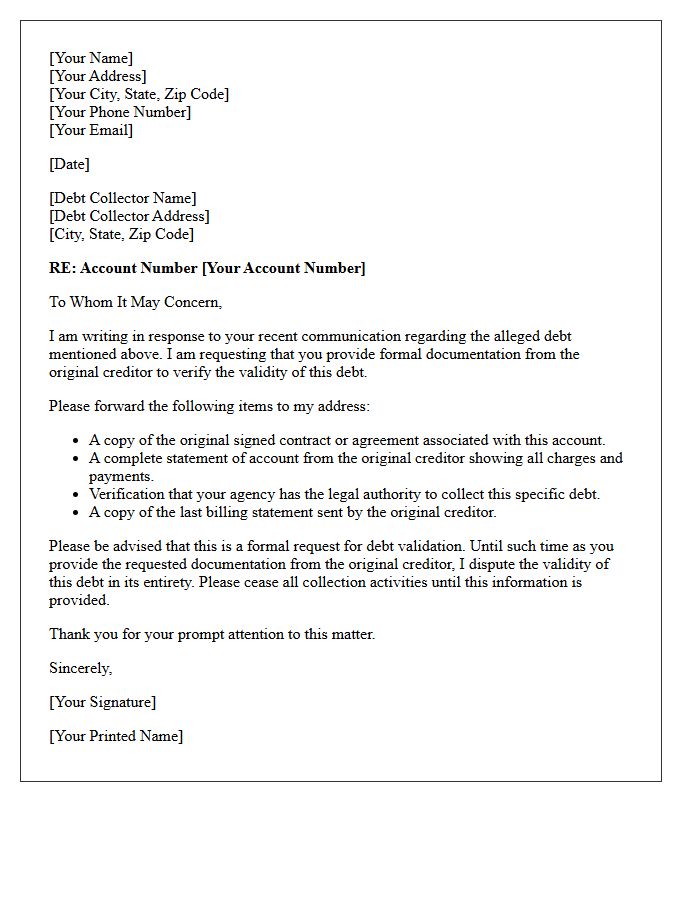

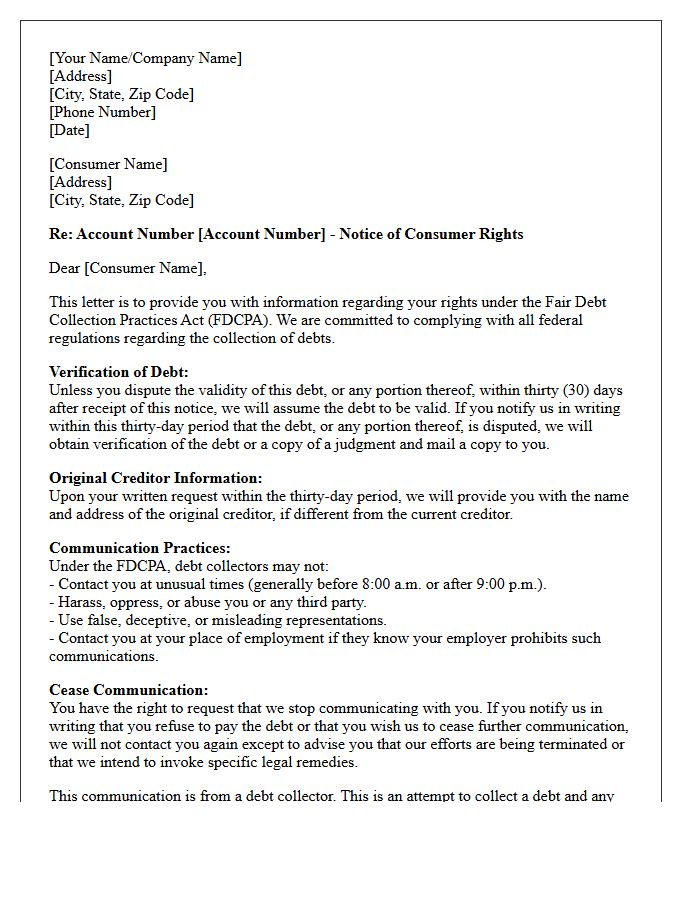

Debt Validation Response Letter

A Debt Validation Response Letter is a critical legal tool used to challenge a collection agency's claim. Under the Fair Debt Collection Practices Act (FDCPA), once you receive an initial notice, you have thirty days to request written verification of the debt. This formal inquiry forces the collector to prove they have the legal authority to collect and that the balance is accurate. If the agency fails to provide sufficient evidence, they must cease collection activities, potentially protecting your credit score from unsubstantiated negative marks and ensuring your consumer rights remain intact.

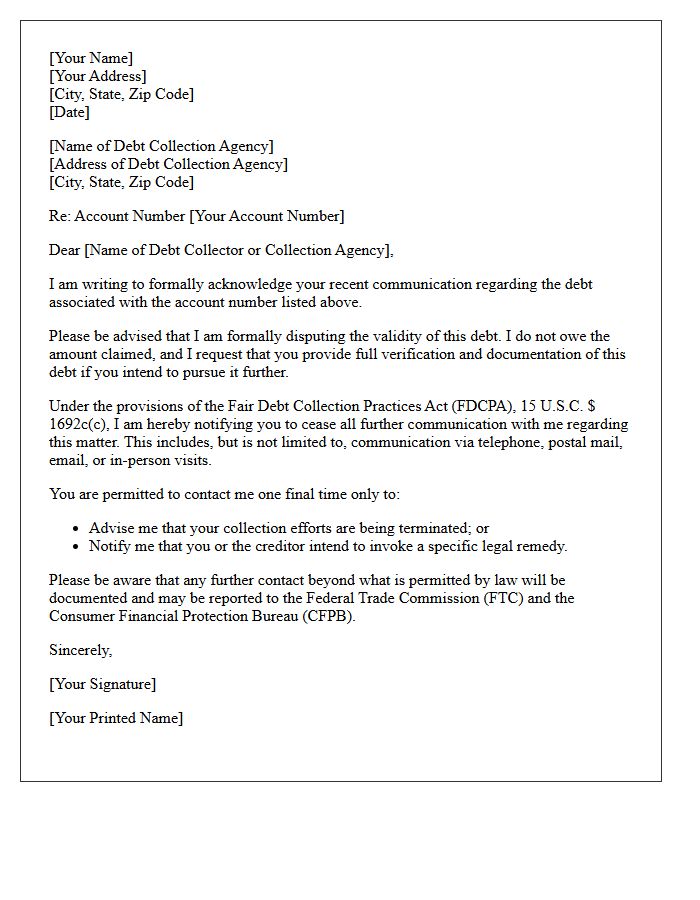

Acknowledgment of Dispute and Cease Communication Letter

An Acknowledgment of Dispute and Cease Communication Letter is a formal legal notice sent to debt collectors. Under the Fair Debt Collection Practices Act (FDCPA), this document serves two vital functions: it officially disputes the validity of a debt and legally mandates that the agency stop all further contact. Once received, the collector may only contact you to confirm they are ceasing communication or to notify you of specific legal actions. Using this letter protects your rights against harassment while ensuring the dispute is documented for your financial records.

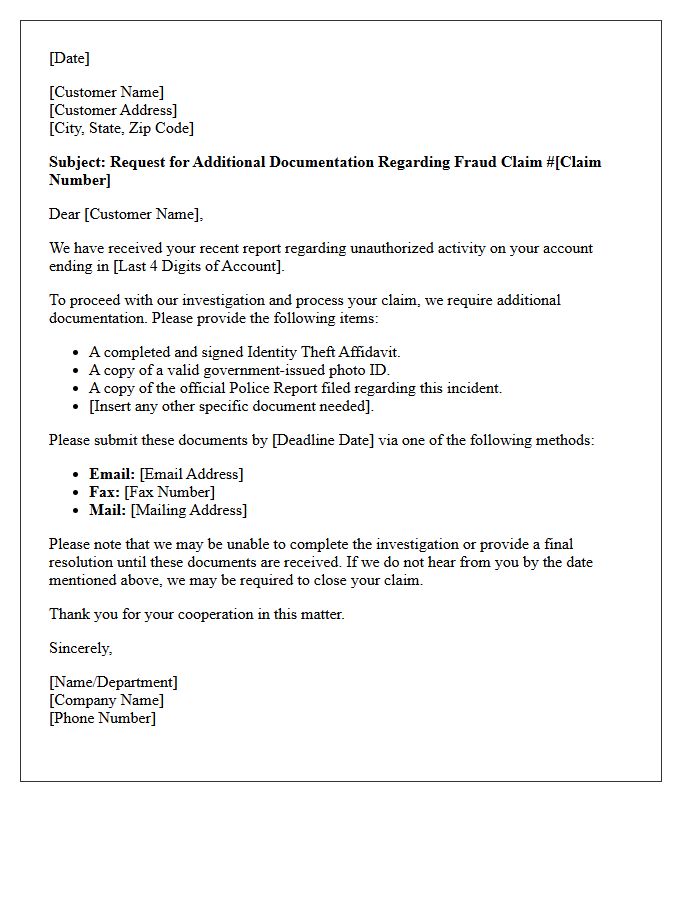

Request for Additional Fraud Documentation Letter

A Request for Additional Fraud Documentation Letter is a formal notice issued by financial institutions when suspicious activity occurs. It requires you to provide verifiable evidence, such as identity documents or transaction receipts, to prove your legitimacy. Failure to respond promptly can result in account suspension or denied claims. Ensuring identity verification is the primary goal of this process, protecting both the consumer and the bank from unauthorized access. Always submit requested files through secure, official channels to maintain security and resolve the investigation efficiently.

Notice of Account Closure and Bureau Deletion Letter

A Notice of Account Closure and Bureau Deletion Letter is a formal request sent to creditors or collection agencies. It demands the permanent removal of negative marks or closed accounts from your credit report. This process is essential for improving your credit score by ensuring that inaccurate, outdated, or settled debts are no longer reported. Sending this letter via certified mail creates a legal paper trail, forcing credit bureaus to verify or delete the information within thirty days to maintain compliance with consumer protection laws.

Rebuttal of Unlawful Collection Allegations Letter

A Rebuttal of Unlawful Collection Allegations Letter is a formal legal response used to challenge unauthorized debt recovery efforts. It serves as a vital tool to dispute inaccurate claims or procedural errors made by creditors. By demanding debt validation, the consumer forces the collector to provide proof of the legal right to collect. This document protects your consumer rights under the Fair Debt Collection Practices Act, effectively stopping harassment and preventing negative credit reporting while ensuring all financial disputes are handled with transparency and legal compliance.

Verification of Debt Accuracy and Compliance Letter

A Debt Validation Letter is a critical legal tool used to ensure collection agencies provide proof of a debt's accuracy and legal standing. Under the Fair Debt Collection Practices Act, consumers have the right to challenge claims within thirty days of initial contact. This process requires the collector to verify the original creditor, the exact amount owed, and their legal authority to collect. Sending this formal notice forces compliance with federal regulations and prevents the reporting of fraudulent or expired debts to credit bureaus, protecting your financial reputation from errors.

Identity Theft Investigation Resolution Letter

An Identity Theft Investigation Resolution Letter is a formal document issued by a business or credit bureau confirming the final outcome of a fraud inquiry. It serves as legal proof that disputed transactions or accounts were deemed fraudulent and subsequently removed. This letter is essential for restoring your credit score and protecting your financial reputation. Always retain a copy of this resolution to prevent future collection actions on cleared debts and to provide evidence to law enforcement or other creditors that the matter has been officially resolved.

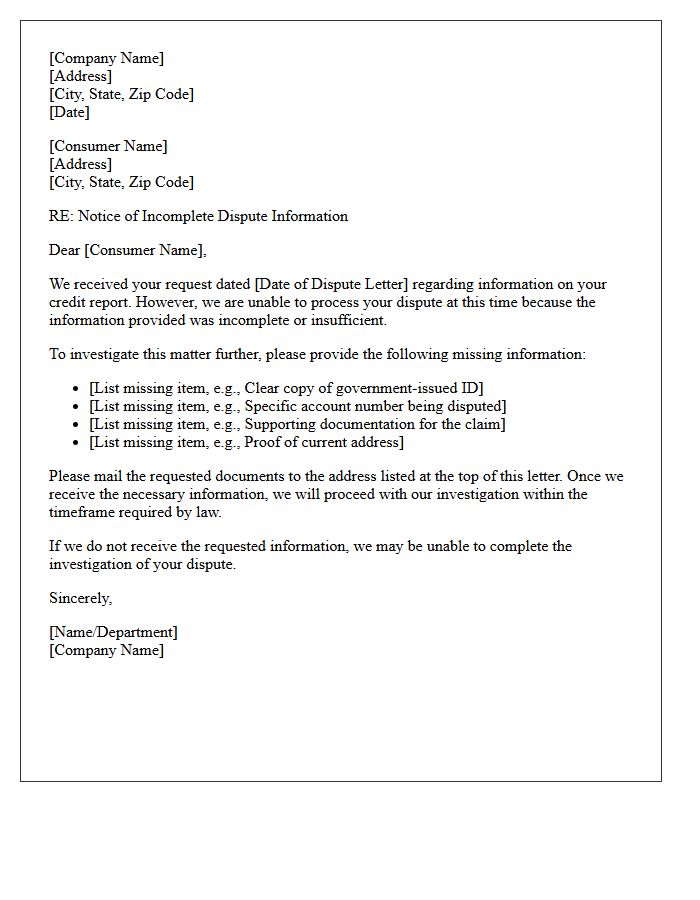

Notice of Incomplete Dispute Information Letter

A Notice of Incomplete Dispute Information Letter is a formal response from a credit bureau indicating that your credit dispute lacks sufficient evidence or clarity. Receiving this means the bureau will not investigate your claim until you provide supplemental documentation, such as account statements or identity verification. To avoid delays, ensure your initial request is specific and includes clear proof of inaccuracies. Promptly addressing these deficiencies is essential to protecting your consumer rights and ensuring an accurate credit report.

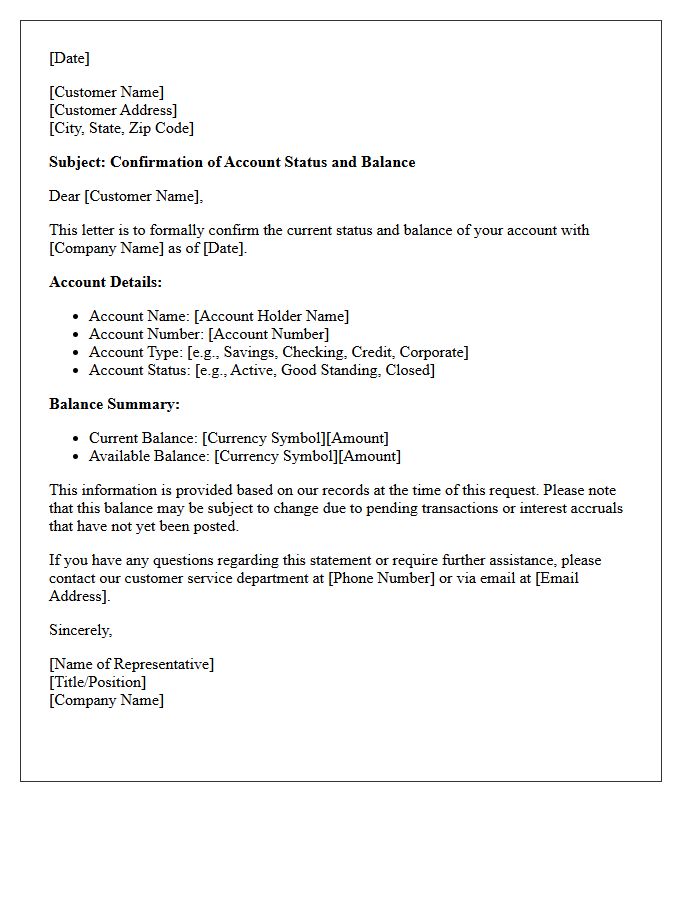

Confirmation of Account Status and Balance Letter

A Confirmation of Account Status and Balance Letter serves as official verification issued by a financial institution. It confirms essential details, including the current account standing, opening date, and real-time balance. This document is vital for audit compliance, mortgage applications, or visa processing to prove financial solvency. By providing third-party validation of liquid assets, it ensures transparency between account holders and requesting entities. Always ensure the letter features an official bank stamp and authorized signature to maintain its legal authenticity and professional credibility.

Original Creditor Documentation Forwarding Letter

An Original Creditor Documentation Forwarding Letter is a formal notice sent by a debt buyer to a consumer. Its primary purpose is to provide validated evidence of a debt's origin, typically including the initial contract or billing statements. This document serves as legal proof that the current collector has the right to pursue payment. Receiving this letter is crucial during the debt verification process, as it ensures the consumer is paying the correct entity and that the outstanding balance is accurately documented according to federal consumer protection laws.

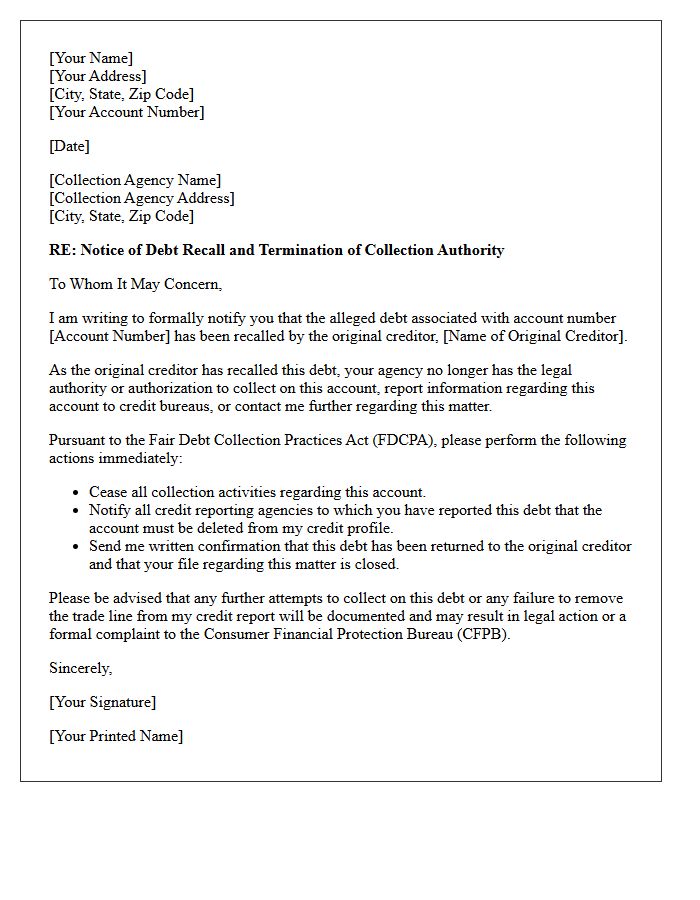

Notification of Debt Recall by Original Creditor Letter

A Notification of Debt Recall informs you that the original creditor has legally reclaimed your account from a third-party collection agency. This action typically voids the collector's authority to demand payment. It is crucial to verify this recall in writing to prevent double payment and ensure your credit report is updated accurately. Once a debt is recalled, you should direct all future correspondence and payments exclusively to the original creditor. Always retain this notice as legal proof that the agency no longer owns or manages your outstanding balance.

Fair Debt Collection Practices Act Compliance Explanation Letter

A Fair Debt Collection Practices Act (FDCPA) compliance explanation letter is a formal document sent by creditors or agencies to confirm they are following federal consumer protection laws. This letter ensures that collection efforts remain ethical, transparent, and free from harassment or deceptive tactics. It serves as legal documentation that the collector respects debtor rights, such as providing debt validation and honoring cease-and-desist requests. Understanding this letter helps consumers verify the legitimacy of a debt while protecting themselves against abusive practices during the recovery process.

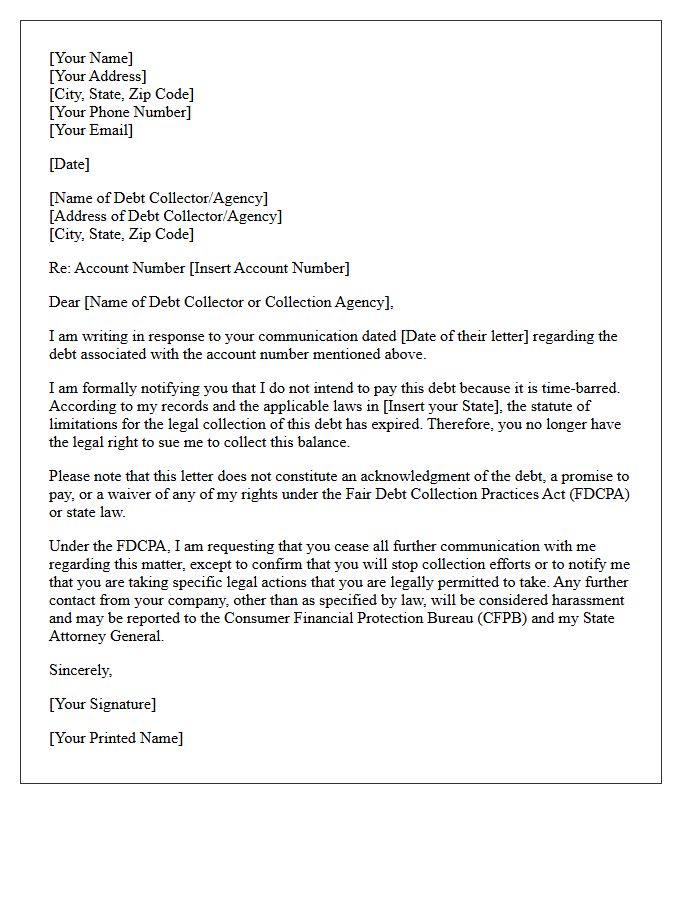

Time-Barred Debt Acknowledgment Letter

A Time-Barred Debt Acknowledgment Letter is a critical document used by creditors to restart the statute of limitations on old financial obligations. If you sign or respond to this letter by admitting the debt belongs to you, or by making a partial payment, you may legally revive a debt that was otherwise uncollectible in court. Always verify the legal expiration of a debt before responding, as acknowledging it can waive your consumer protections and allow collectors to sue for the full balance again.

How should a debt collector legally respond to an Unlawful Debt Collection Dispute Notice?

Upon receiving a dispute notice, a debt collector must cease all collection activities immediately until they provide written verification of the debt. The response should include the amount owed, the name of the original creditor, and a statement verifying that the debt is valid and legally enforceable under the Fair Debt Collection Practices Act (FDCPA).

What information must be included in a debt validation letter following a dispute?

A legally compliant response to a dispute notice must include a copy of the original judgment or a document from the original creditor confirming the debt balance. It should also detail the chain of title for the debt and provide a breakdown of any interest, fees, or additional charges applied since the last payment.

What are the consequences if a debt collector ignores a dispute notice?

If a debt collector continues collection efforts without responding to a valid dispute notice, they are in violation of federal law. This can result in legal liability for statutory damages, attorney fees, and the potential dismissal of the debt claim in court due to non-compliance with the FDCPA.

How long does a debt collector have to respond to a dispute notice?

While federal law does not mandate a specific number of days to respond, the collector cannot resume any pursuit of the debt-including reporting it to credit bureaus-until they have mailed the verification to the consumer. Most reputable agencies aim to respond within 30 days to maintain their right to collect.

Can a debt collector proceed with a lawsuit after receiving a dispute notice?

A debt collector cannot initiate or proceed with a lawsuit once a timely dispute notice has been received until they have provided the consumer with the required verification of the debt. Filing a lawsuit before validating the debt after a formal dispute may be considered an unfair or deceptive collection practice.

Comments