Receiving a frivolous dispute allegation notice from credit bureaus can be frustrating and stall your credit repair progress. This article explains how to effectively challenge these claims by providing solid evidence and asserting your legal rights under the FCRA. Regain control of your financial standing and clear inaccuracies quickly. Below are some ready to use templates.

Image cover: Defending Your Credit: Strategic Response Templates for Frivolous Dispute Allegations

Letter Samples List

- Frivolous Dispute Response Letter

- Letter of Frivolous Dispute Determination

- Debt Collection Frivolous Dispute Notice Letter

- Response Letter to Frivolous Debt Allegation

- Letter Regarding Frivolous Dispute of Debt

- Frivolous Claim Dismissal Letter

- Notice of Frivolous Dispute Letter

- Letter Rejecting Frivolous Debt Dispute

- Irrelevant and Frivolous Dispute Response Letter

- Letter of Determination on Frivolous Allegation

- Frivolous Debt Allegation Rejection Letter

- Consumer Dispute Frivolous Determination Letter

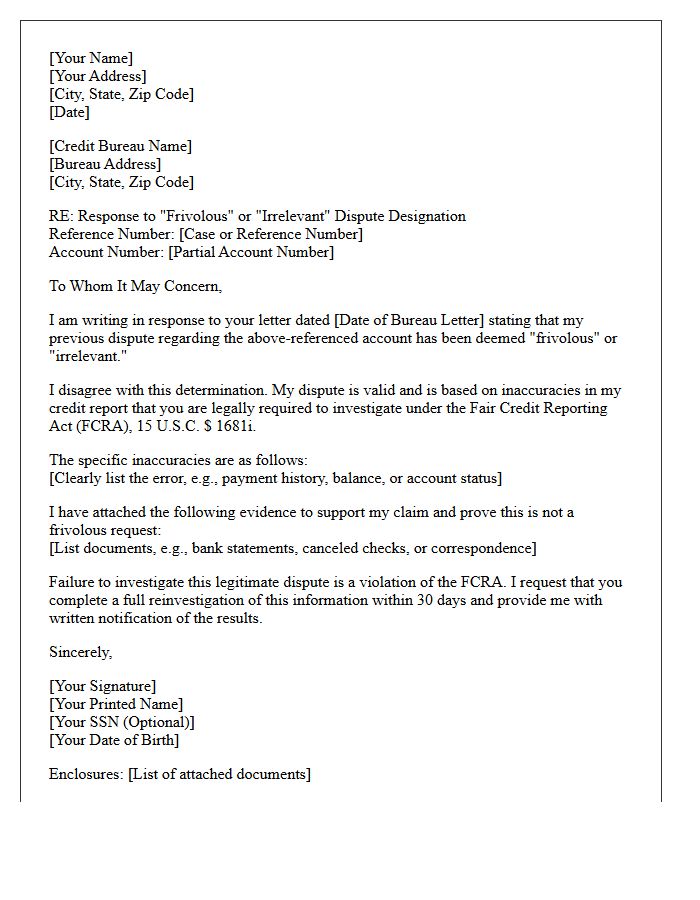

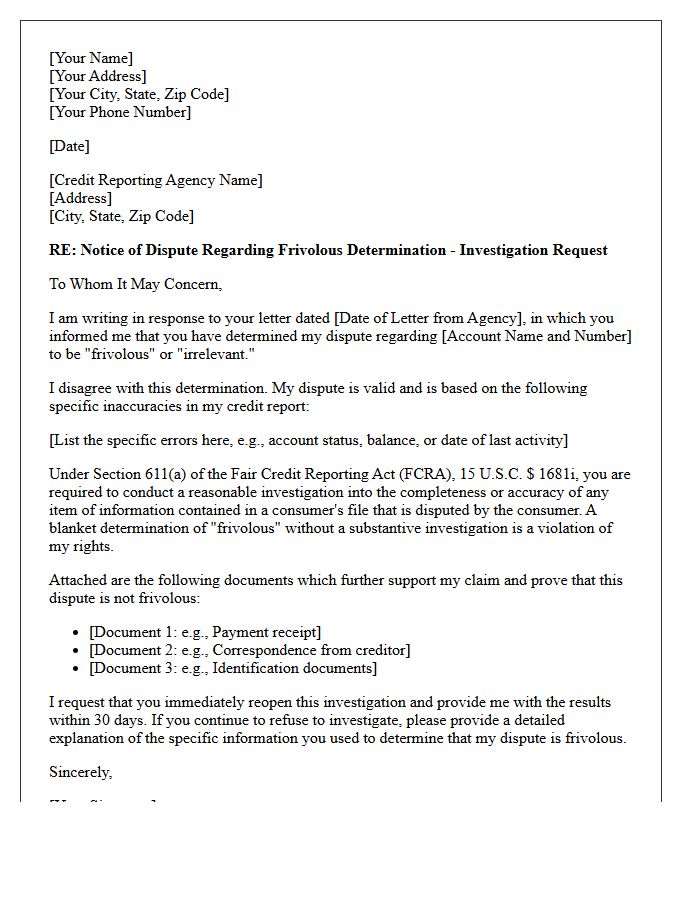

Frivolous Dispute Response Letter

A Frivolous Dispute Response Letter is a formal notification sent by credit bureaus or businesses when they deem a consumer's challenge lack sufficient evidence or legal merit. Receiving this notice means the recipient must provide supporting documentation, such as police reports or identification, to validate their claim. It is crucial to respond with specific facts rather than generic templates to prove the dispute is legitimate. Failure to provide new information often results in the bureau refusing to reinvestigate the disputed item, keeping negative marks on your credit report.

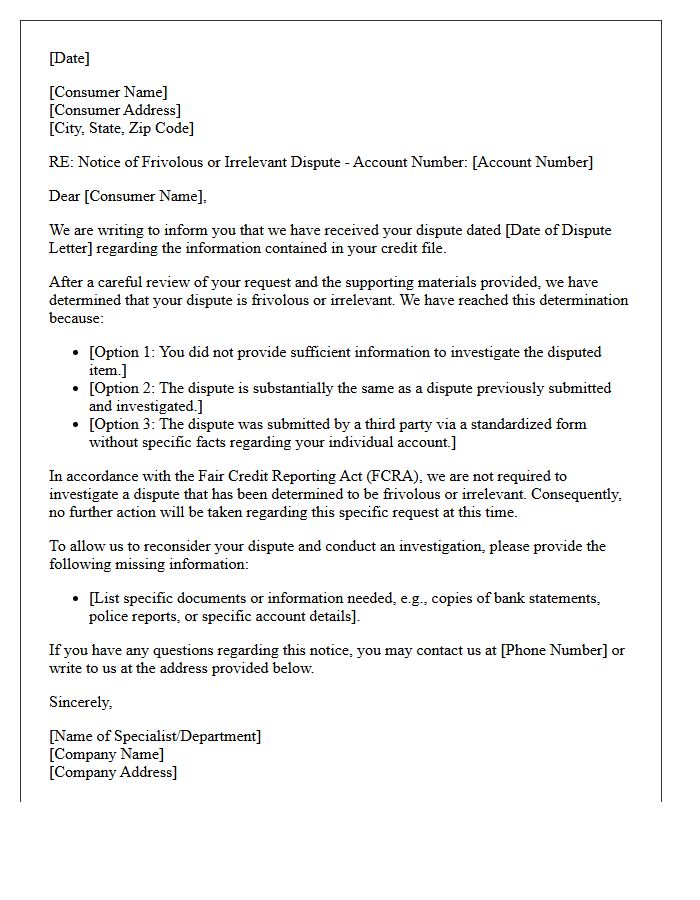

Letter of Frivolous Dispute Determination

A Letter of Frivolous Dispute Determination is a formal notice from a credit bureau stating they will not investigate your claim. This occurs if the bureau believes your request lacks sufficient evidence or is submitted by a credit repair organization using a generic template. To resolve this, you must provide specific documentation and clear proof to validate your dispute. Understanding this notification is crucial because it halts the correction process, requiring you to resubmit a more detailed, individualized challenge to protect your consumer credit rights under the FCRA.

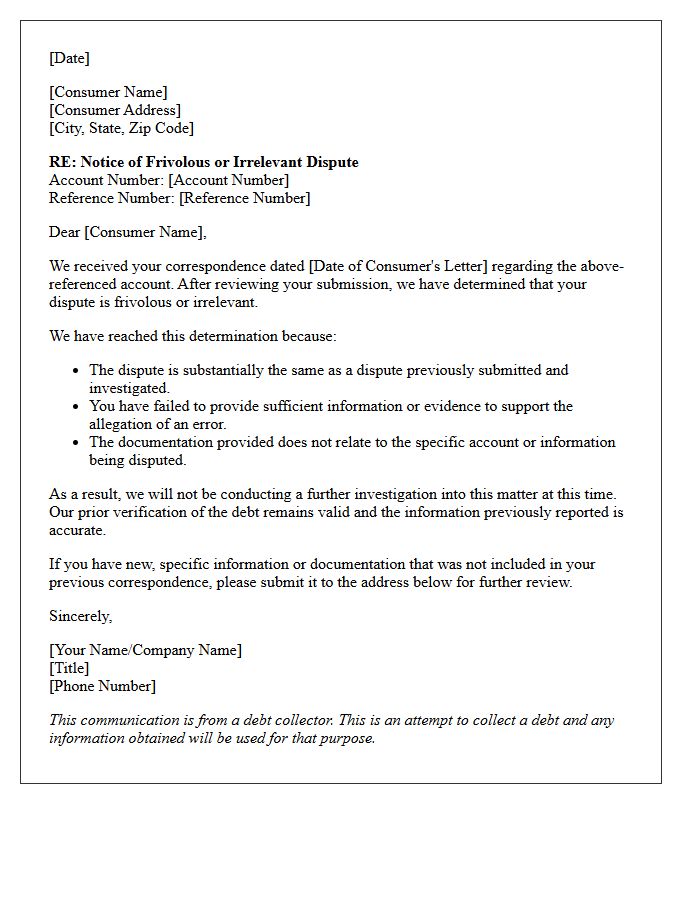

Debt Collection Frivolous Dispute Notice Letter

A Debt Collection Frivolous Dispute Notice Letter is a formal response sent by a collection agency when they believe a consumer's dispute lacks substantive evidence or new information. Under the Fair Debt Collection Practices Act (FDCPA), collectors can deem a challenge frivolous if it is repetitive or lacks supporting documentation. Receiving this notice means the agency will stop investigating unless you provide valid proof or specific details regarding the error. It is crucial to respond with clear evidence, such as payment receipts or identity theft reports, to protect your credit score.

Response Letter to Frivolous Debt Allegation

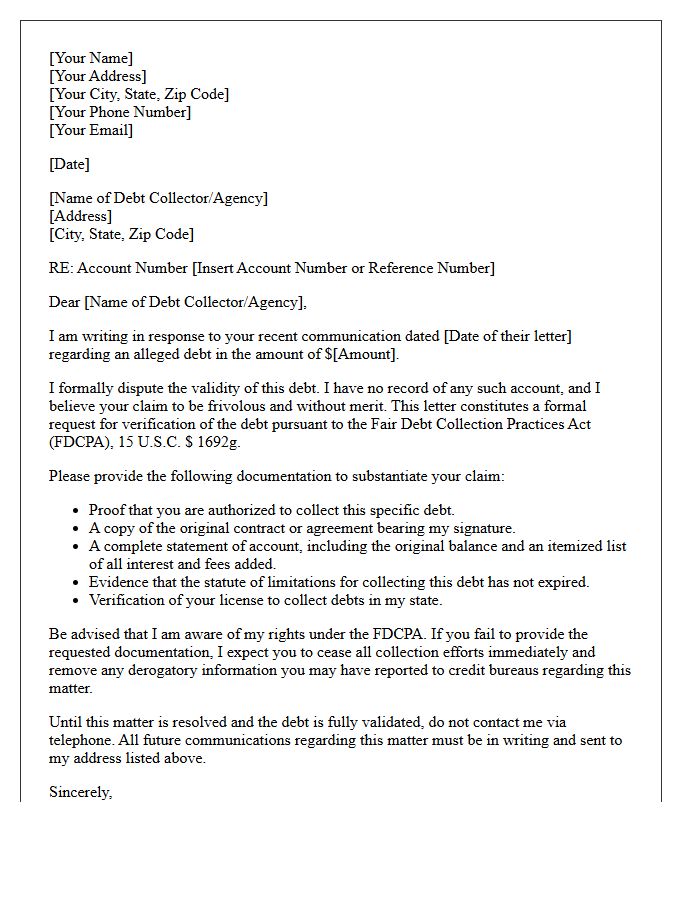

When sending a Response Letter to Frivolous Debt Allegation, you must formally dispute the claim in writing. Under the Fair Debt Collection Practices Act, you have the right to demand verification of the alleged debt. Clearly state that you refuse to pay without documented proof of the original contract and accurate balance history. Sending this via certified mail creates a legal paper trail, protecting your credit score and stopping unauthorized harassment. Never acknowledge ownership of the debt or make partial payments, as this can restart the statute of limitations on expired claims.

Letter Regarding Frivolous Dispute of Debt

Receiving a Letter Regarding Frivolous Dispute of Debt indicates that a credit bureau or creditor has dismissed your challenge because it lacks supporting evidence or appears generated by a template. To resolve this, you must provide specific documentation, such as payment receipts or identity theft reports, to prove the inaccuracy. Simply repeating a claim without new facts will result in a rejected dispute. Ensure your response includes concrete details to restart the verification process and protect your consumer rights under the Fair Credit Reporting Act.

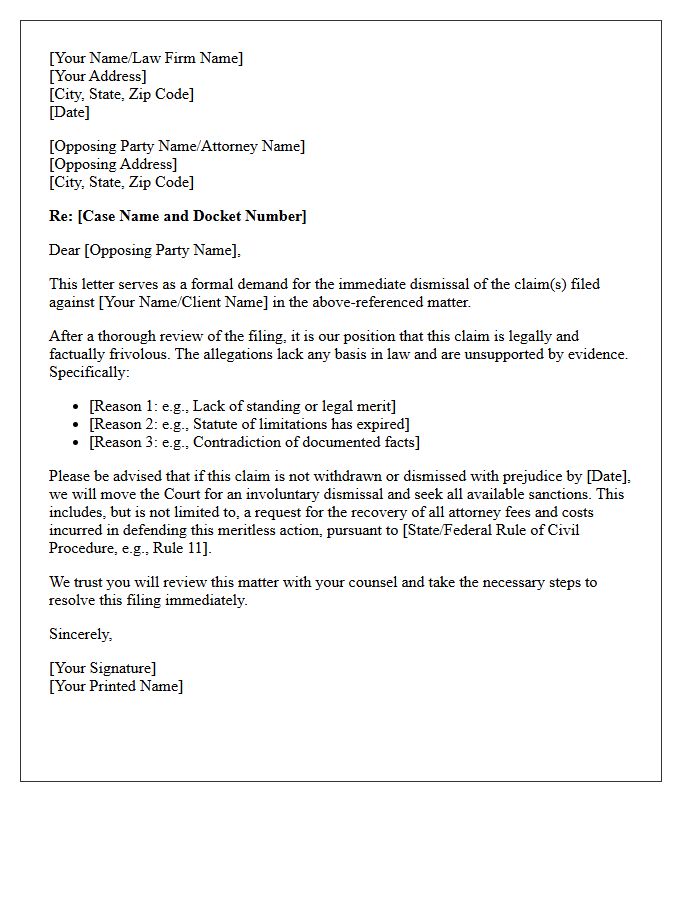

Frivolous Claim Dismissal Letter

A Frivolous Claim Dismissal Letter is a formal legal response used to reject a lawsuit or demand that lacks any legal basis or factual merit. This document serves as a procedural defense, warning the opposing party that their action is considered groundless or intended to harass. It typically demands the immediate withdrawal of the claim to avoid court-ordered sanctions or recovery of legal fees. Sending this letter is a critical step in mitigating litigation costs and protecting your reputation against bad-faith legal assertions.

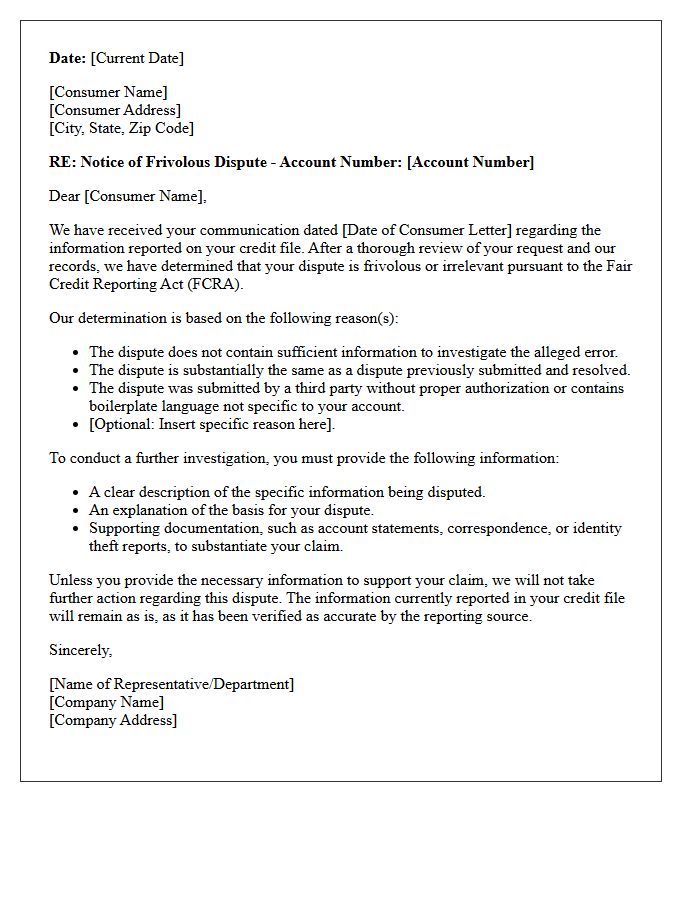

Notice of Frivolous Dispute Letter

A Notice of Frivolous Dispute Letter is a formal notification sent by a credit bureau when they determine a consumer's challenge lacks sufficient evidence or merit. Receiving this notice means the bureau will cease investigation of the disputed item. To resolve this, you must provide new documentation or specific facts that validate your claim. Avoid using generic automated templates or repetitive filings without updates, as these often trigger this status. Providing clear, supporting proof is essential to re-opening the investigation and ensuring your credit report remains accurate and fair.

Letter Rejecting Frivolous Debt Dispute

When a credit bureau receives a Letter Rejecting Frivolous Debt Dispute, it means they have determined the consumer's challenge lacks merit or sufficient evidence. Under the FCRA, bureaus can dismiss claims that are repetitive or unsubstantiated. To overcome this, you must provide specific documentation, such as account statements or identity theft reports, to prove the inaccuracy. Simply using boilerplate templates often leads to a frivolous designation. Ensuring your dispute is fact-based and includes new, relevant information is essential to force a reinvestigation and protect your credit score integrity.

Irrelevant and Frivolous Dispute Response Letter

An Irrelevant and Frivolous Dispute Response Letter is a formal notice issued by credit bureaus when they deem a consumer's challenge lack merit or sufficient evidence. To prevent your claim from being dismissed, you must provide specific documentation and clear reasoning for each discrepancy. Avoid using generic templates or "pro-per" legal jargon, as these often trigger automated rejections. To successfully overturn this status, resubmit your request with new supporting facts to prove the inaccuracy is genuine, ensuring your credit report remains accurate and fair.

Letter of Determination on Frivolous Allegation

A Letter of Determination on Frivolous Allegation is a formal notice issued by an oversight body, such as the Office of the Inspector General, regarding a complaint. This document signifies that a reported claim lacks a legal basis or factual merit. Receiving this determination means the investigation is officially closed because the evidence provided was insufficient or intentionally misleading. Understanding this status is crucial for administrative accountability, as it protects individuals from baseless accusations while ensuring that investigative resources are focused on legitimate violations of policy or law.

Frivolous Debt Allegation Rejection Letter

A Frivolous Debt Allegation Rejection Letter is a formal legal tool used to dispute invalid or unverified claims from collectors. This document asserts your rights under the Fair Debt Collection Practices Act by demanding strict proof of the alleged liability. It effectively challenges unsubstantiated demands and prevents predatory agencies from damaging your credit score without evidence. Sending this notice via certified mail creates a vital paper trail, forcing collectors to provide validation or cease all communication regarding the questionable debt immediately.

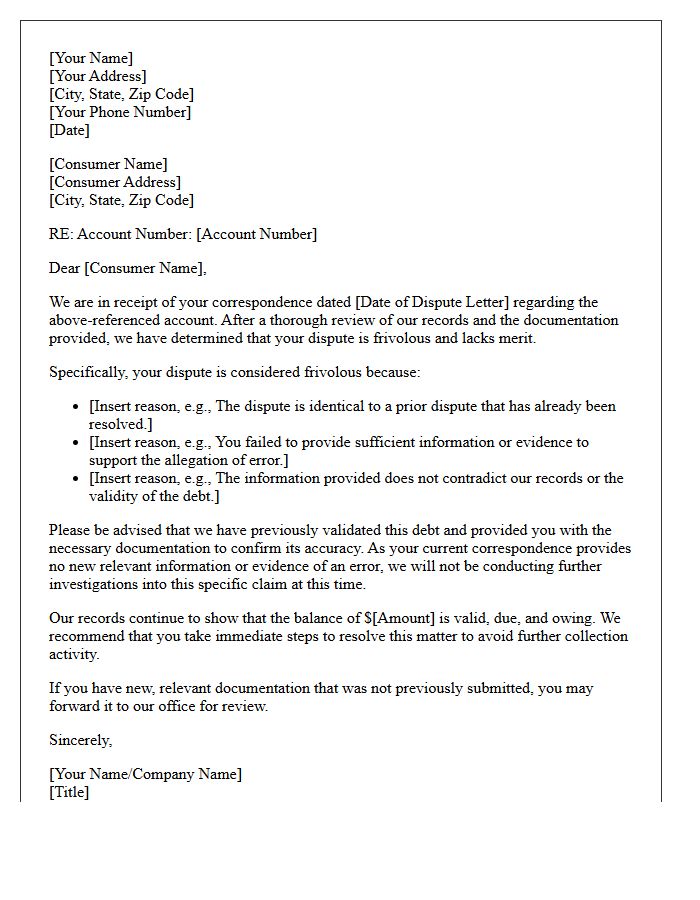

Consumer Dispute Frivolous Determination Letter

A consumer dispute frivolous determination letter is a formal notice from a credit bureau stating they will not investigate your claim. This occurs if your request lacks sufficient evidence or appears to be generated by a credit repair scam. To bypass a frivolous determination, you must provide specific facts, documentation, and clear reasons why an item is inaccurate. Simply resubmitting the same claim without new information will trigger this rejection. Always include proof to ensure the bureau fulfills its legal obligation to perform a reinvestigation under the Fair Credit Reporting Act.

What is a Frivolous Dispute Allegation Notice?

A Frivolous Dispute Allegation Notice is a formal letter sent by a credit bureau or creditor claiming that your dispute lacks sufficient evidence, is repetitive, or was submitted by a third party without proper authorization. It is a mechanism used to halt an investigation under the Fair Credit Reporting Act (FCRA).

How should I respond to a claim that my dispute is frivolous?

You should respond by providing additional supporting documentation, such as account statements, police reports, or identity theft affidavits, that proves the inaccuracy of the item. Clearly state that your dispute is valid under the FCRA and demand that the bureau complete a reinvestigation within the remaining statutory timeframe.

What happens if I don't respond to a frivolous dispute notice?

If you fail to respond with more information or a rebuttal, the credit bureau is legally permitted to terminate the investigation and leave the disputed information on your credit report. Ignoring the notice essentially allows the bureau to dismiss your claim without verifying the data with the original creditor.

Does a frivolous allegation mean my dispute is permanently denied?

No, a frivolous allegation is not a final denial. It is a procedural delay. By refining your dispute, providing "new" information or specific details that were missing from the initial request, you can force the credit bureau to reopen the case and provide a substantive response.

Can a credit bureau legally ignore my dispute if they label it frivolous?

Under Section 611 of the FCRA, a credit bureau can decline to investigate if they determine a dispute is frivolous; however, they must notify you within five business days and provide the specific reasons for their determination. If they fail to provide a valid reason, they may be in violation of federal law.

Comments