Protect your consumer rights by sending a formal Response to Insufficient Debt Validation Notice if a collection agency provides incomplete verification. Under the FDCPA, collectors must provide specific proof of the debt's validity before continuing collection efforts. Ensure your financial records remain accurate and demand full documentation to challenge unsubstantiated claims. To help you draft your letter, below are some ready to use template.

Image cover: Defending Your Rights: Strategic Responses to Insufficient Debt Validation Notices

Letter Samples List

- Notice of Insufficient Debt Validation Letter

- Second Request for Complete Debt Validation Letter

- Demand for Adequate Debt Verification Letter

- Dispute of Inadequate Debt Validation Letter

- Follow-Up Debt Validation Request Letter

- Rejection of Insufficient Verification Letter

- Final Demand for Proper Debt Validation Letter

- Cease and Desist Pending Proper Validation Letter

- Request for Comprehensive Debt Validation Letter

- Notice of Non-Compliant Debt Validation Letter

- Demand for Original Creditor Documentation Letter

- Unverified Debt Dispute and Collection Suspension Letter

- Incomplete Debt Verification Response Letter

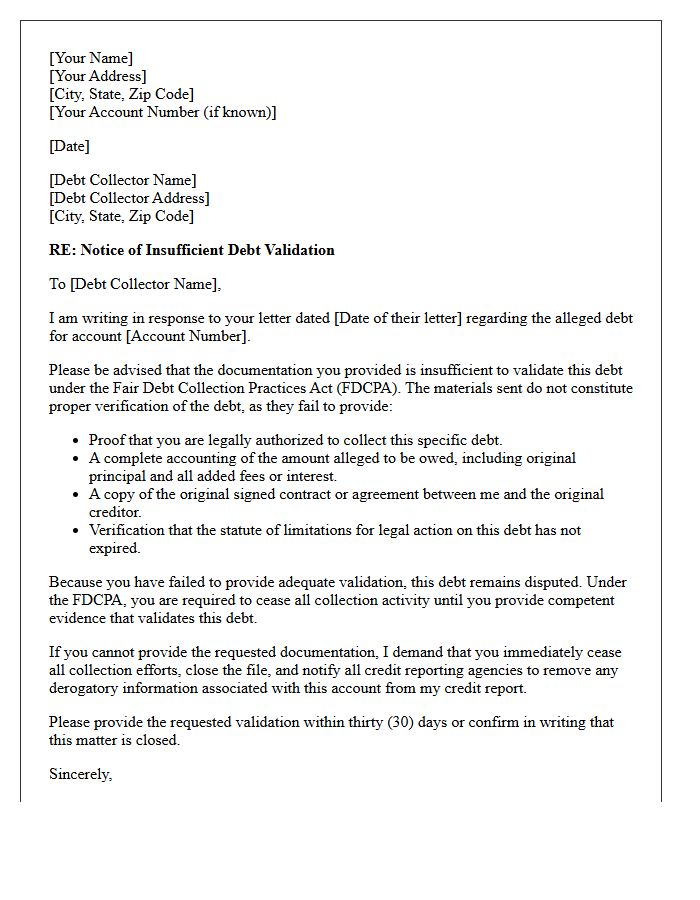

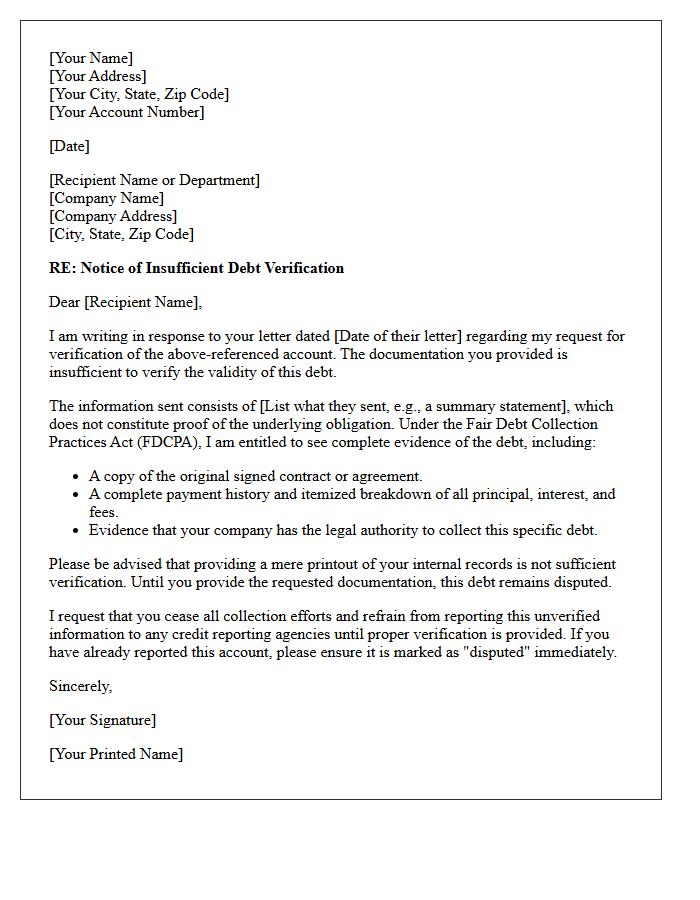

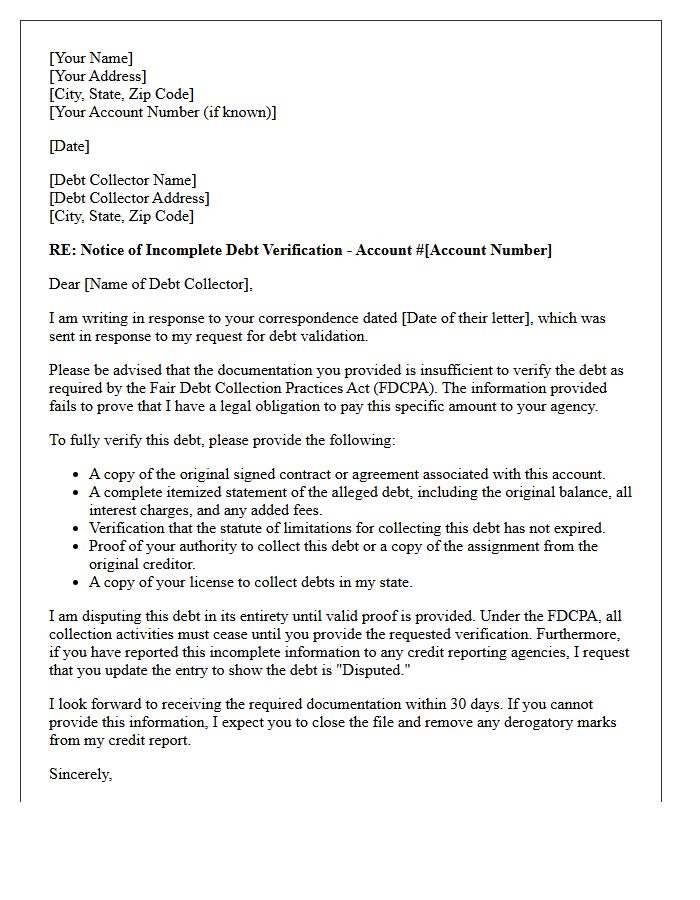

Notice of Insufficient Debt Validation Letter

A Notice of Insufficient Debt Validation Letter is a formal response sent when a collection agency fails to provide adequate proof of a debt's validity. Legally, collectors must provide more than just an invoice; they must verify the original creditor and the exact amount owed. Sending this notice is essential for protecting your consumer rights under the FDCPA. It effectively halts collection activities and prevents unauthorized reporting to credit bureaus until the collector provides verified documentation. If the agency cannot produce evidence, they must cease contact and remove the disputed entry from your credit report.

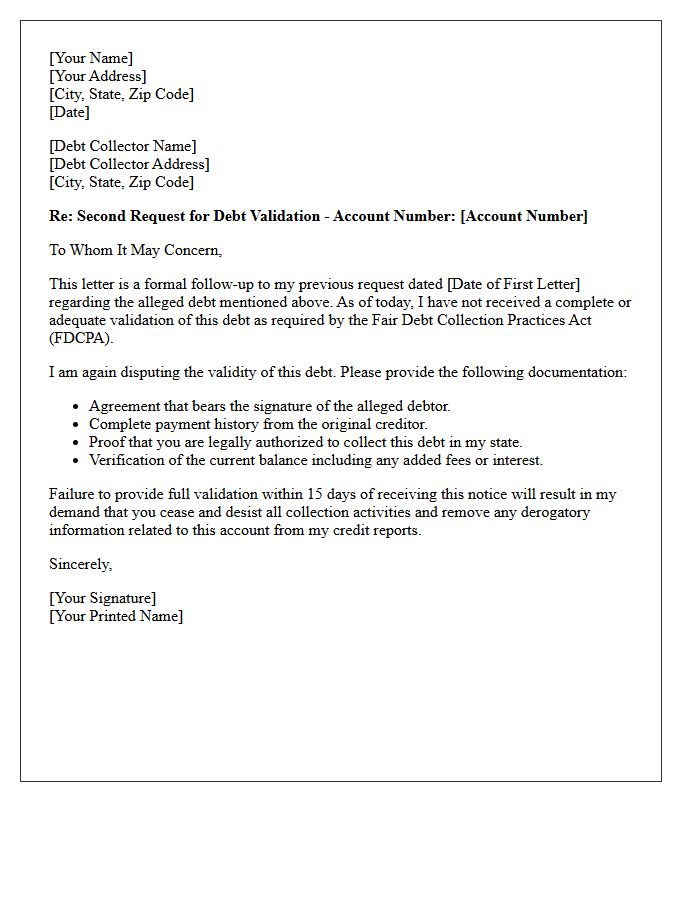

Second Request for Complete Debt Validation Letter

A Second Request for Complete Debt Validation is a critical follow-up letter sent when a collection agency fails to provide adequate proof of a debt. This document reinforces your legal rights under the Fair Debt Collection Practices Act (FDCPA). It informs the collector that their previous response was insufficient and demands full verification, including original contracts and payment history. Sending this via certified mail creates a paper trail, which is essential for disputing inaccurate entries on your credit report or defending against potential legal action from creditors.

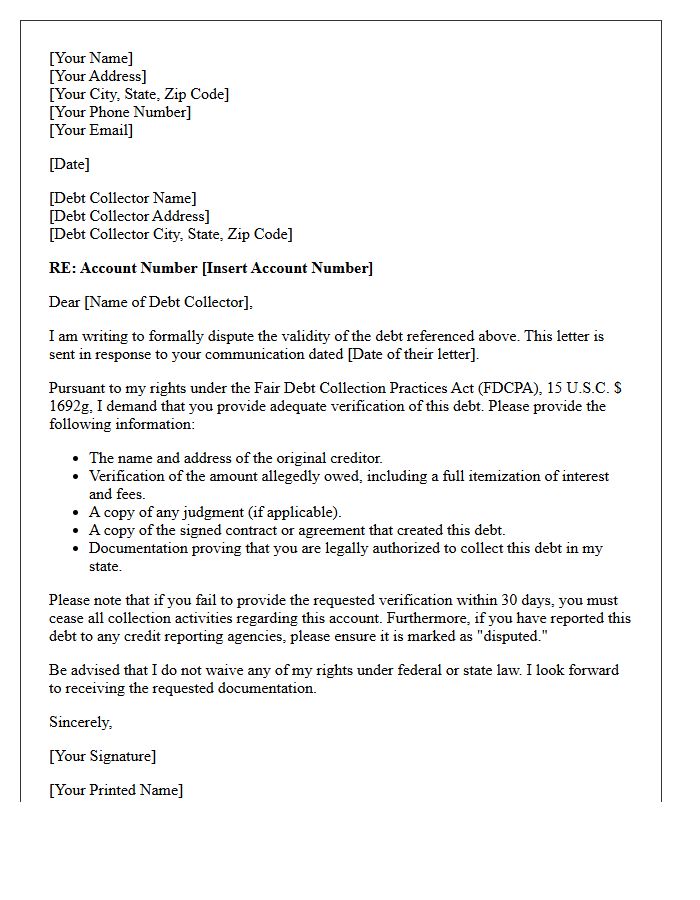

Demand for Adequate Debt Verification Letter

A Demand for Adequate Debt Verification Letter is a formal legal tool used to dispute inaccurate collections. Under the Fair Debt Collection Practices Act (FDCPA), consumers have the right to request proof that a debt is valid and legally owned by the collector. Sending this written notice within 30 days of initial contact forces the agency to cease collection activities until they provide verification. This process protects you from identity theft, outdated balances, and predatory lending practices by ensuring every claim is substantiated with credible evidence and original contract documentation.

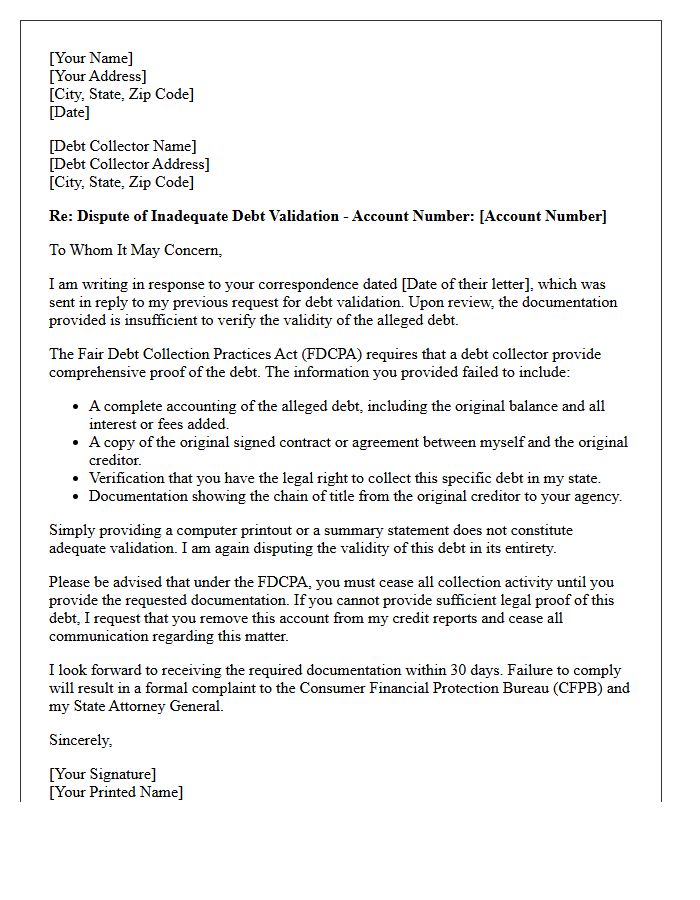

Dispute of Inadequate Debt Validation Letter

A dispute of inadequate debt validation occurs when a collection agency fails to provide verified proof of a debt's legitimacy. Under the Fair Debt Collection Practices Act (FDCPA), consumers have the right to demand original account statements and evidence of the collector's legal authority to collect. If a response is incomplete or vague, the debt remains legally unverified. Disputing these deficiencies is essential to protect your credit score and prevent unlawful collection activities. Always send your follow-up rebuttal letter via certified mail to maintain a clear paper trail of the non-compliance.

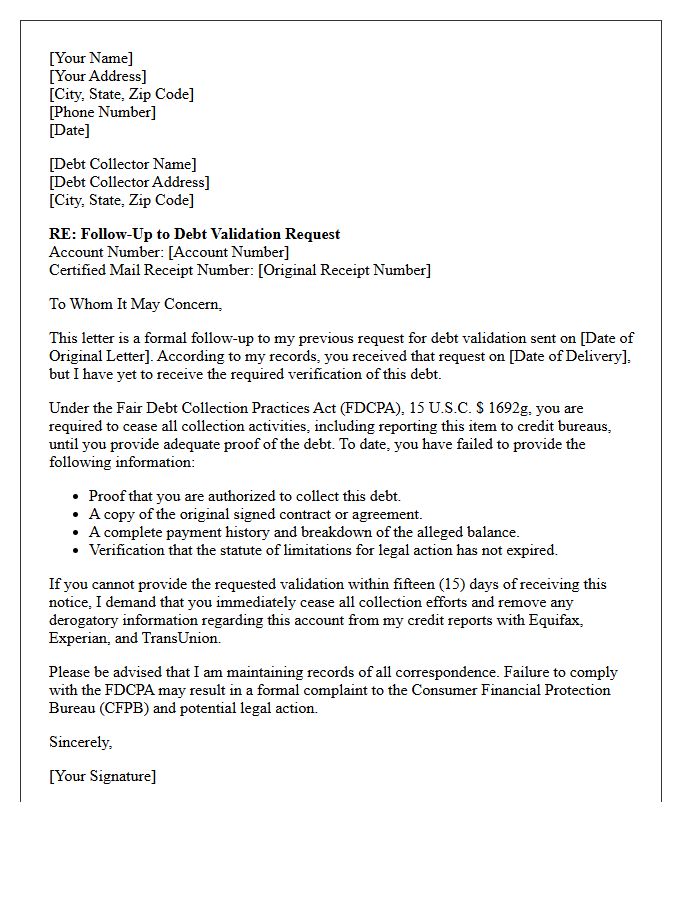

Follow-Up Debt Validation Request Letter

A Follow-Up Debt Validation Request Letter is a critical legal tool used when a collection agency ignores your initial inquiry. Under the Fair Debt Collection Practices Act (FDCPA), you have the right to demand verified proof of a debt's validity. If the collector continues reporting or attempting to collect without providing documentation, this follow-up serves as formal notice of their non-compliance. Sending this via certified mail creates a paper trail, potentially making the debt uncollectible or providing grounds to dispute and remove inaccurate entries from your credit report.

Rejection of Insufficient Verification Letter

A Rejection of Insufficient Verification Letter is a formal notice issued when submitted documentation fails to meet specific compliance or authentication standards. This document informs the recipient that their provided evidence-such as proof of identity, income, or residency-is incomplete, illegible, or unverified. To resolve this, you must promptly provide the requested supplementary evidence to satisfy legal or procedural requirements. Failing to address these deficiencies can lead to application denials or service delays, making it crucial to ensure all supporting records are accurate and fully authenticated before resubmitting.

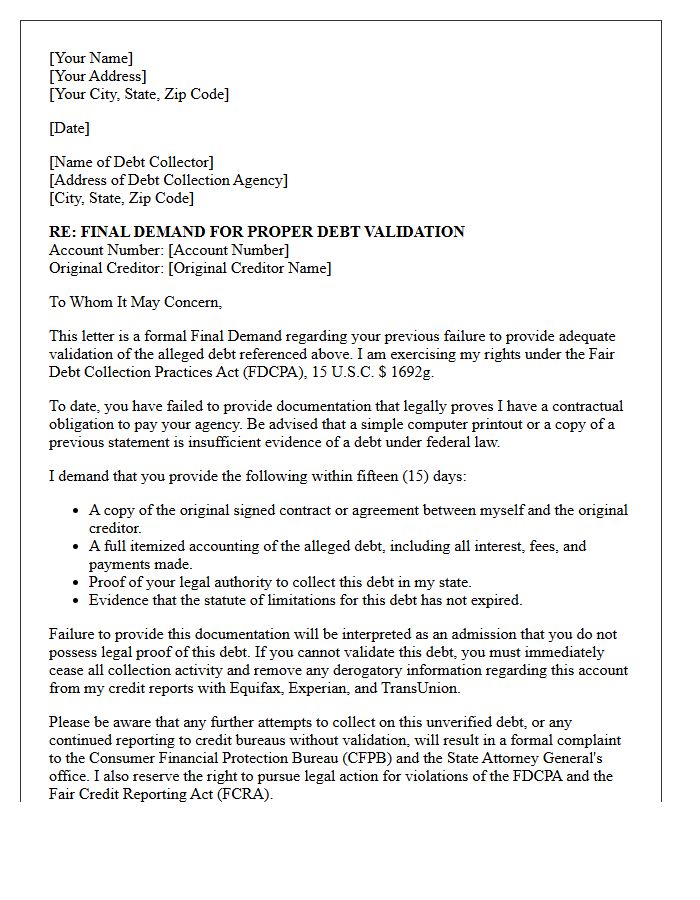

Final Demand for Proper Debt Validation Letter

A Final Demand for Proper Debt Validation Letter is a critical legal tool used to dispute unverified claims under the Fair Debt Collection Practices Act. This formal notice requires collectors to provide certified proof of the debt's validity, including the original contract and complete payment history. Sending this letter stops collection activities until documentation is provided, protecting your credit score from inaccurate reporting. It serves as essential evidence if you need to contest the matter in court, ensuring your rights are upheld against aggressive or fraudulent agencies seeking unauthorized payments.

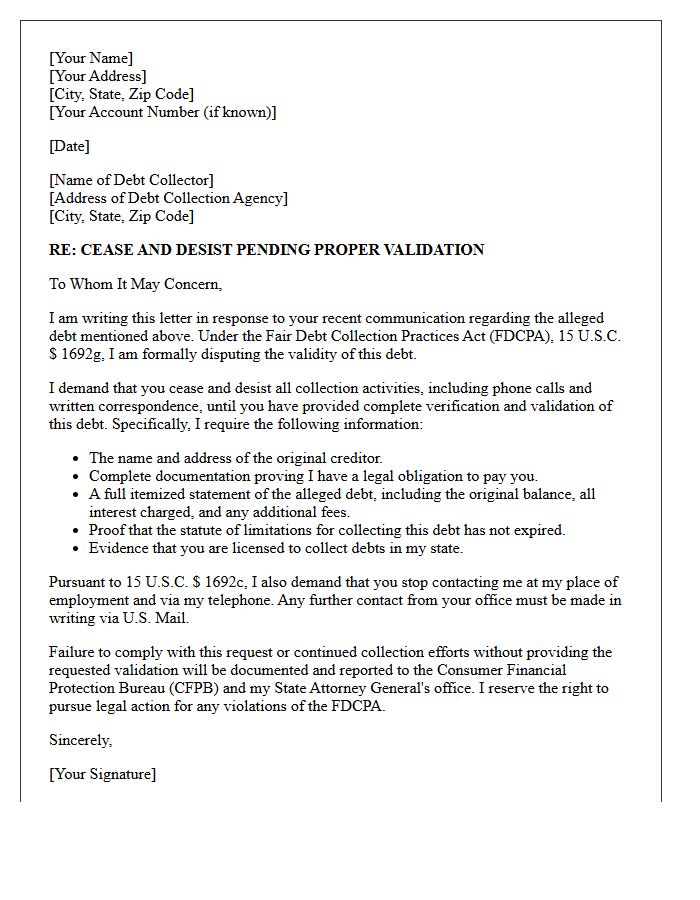

Cease and Desist Pending Proper Validation Letter

A cease and desist pending proper validation letter is a formal legal notice used to halt debt collection efforts. Under the Fair Debt Collection Practices Act (FDCPA), you have the right to request debt verification if you dispute an amount. Once a collector receives this request, they must stop all communication until they provide documented proof of the debt's validity. Sending this letter protects your rights, prevents potential harassment, and ensures you are not paying for unverified or fraudulent claims while creating a crucial paper trail for legal protection.

Request for Comprehensive Debt Validation Letter

A Debt Validation Letter is a critical legal tool under the Fair Debt Collection Practices Act (FDCPA). When a collector contacts you, sending this formal request forces them to provide verifiable proof that the debt is legitimate, accurate, and legally theirs to collect. You must submit this written demand within 30 days of initial contact to dispute the claim effectively. This process protects your consumer rights, prevents unauthorized collections on your credit report, and ensures you do not pay for expired or fraudulent obligations.

Notice of Non-Compliant Debt Validation Letter

Receiving a Notice of Non-Compliant Debt Validation Letter indicates that a collection agency failed to provide legally required verification under the Fair Debt Collection Practices Act (FDCPA). This notice serves as a formal dispute, informing the collector that their previous response was insufficient or incomplete. It is a critical step in protecting your consumer rights, as it demands the cessation of collection activities until proper documentation, such as the original contract or itemized statements, is provided. Maintaining a paper trail of this non-compliance is essential for potential legal defense or credit repair.

Demand for Original Creditor Documentation Letter

A Demand for Original Creditor Documentation Letter is a formal legal request used to verify the legitimacy of a debt. Consumers send this to collection agencies to require proof of the legal right to collect, specifically seeking the original contract or account statements. This process ensures the debt is accurate and belongs to you before any payment is made. Under the Fair Debt Collection Practices Act (FDCPA), providing these documents is essential for debt validation, potentially stopping collection efforts if the agency cannot prove ownership of the debt.

Unverified Debt Dispute and Collection Suspension Letter

An Unverified Debt Dispute and Collection Suspension Letter is a formal legal tool used to stop aggressive collection activities. Under the Fair Debt Collection Practices Act (FDCPA), once you submit this written request, the collector must cease all contact until they provide proof of the debt's validity. This process ensures you are not paying for fraudulent claims or expired obligations. Sending this letter via certified mail protects your consumer rights, prevents harassment, and forces transparency regarding the original creditor and the exact amount owed before any further payment is made.

Incomplete Debt Verification Response Letter

An Incomplete Debt Verification Response Letter is a formal notice sent to creditors or collection agencies when they fail to provide legally required documentation under the Fair Debt Collection Practices Act (FDCPA). This letter informs the collector that their previous response lacked essential details, such as the original contract or a complete payment history. By sending this, you protect your consumer rights and demand full validation before acknowledging any obligation. Failure to provide complete proof may require the agency to cease collection efforts and remove the disputed entry from your credit report.

What is a Response to Insufficient Debt Validation Notice?

This is a formal letter sent to a debt collector when their previous validation attempt failed to provide specific proof of the debt's validity, such as the original contract or a complete payment history.

When should I send a response for insufficient debt validation?

You should send this response immediately after receiving a debt validation packet that lacks essential documentation, typically within 30 days of their last correspondence to maintain your consumer rights under the FDCPA.

What specific documentation should I request in an insufficient validation response?

You should demand the original signed agreement, a full breakdown of all principal and interest charges, proof of the collector's legal authority to collect in your state, and evidence that the statute of limitations has not expired.

Does an insufficient validation notice stop collection activities?

Yes, under the Fair Debt Collection Practices Act (FDCPA), if you dispute the debt based on insufficient evidence, the collector must cease all collection efforts until they provide the legally required documentation.

What happens if a debt collector ignores my notice of insufficient validation?

If a collector continues to report the debt to credit bureaus or pursues collection without providing adequate proof, they may be in violation of federal law, giving you grounds to file a complaint with the CFPB or pursue legal action.

Comments