Receiving a First Notice of Account Arrears is a formal reminder that a payment deadline has been missed. This initial communication serves as a professional nudge to resolve outstanding balances before late fees or credit impacts occur. Maintaining clear records helps preserve positive business relationships and ensures steady cash flow. To simplify your debt collection process, below are some ready to use template.

Image cover: Professional Templates for Your First Notice of Account Arrears

Letter Samples List

- Collection Agency Letterhead

- Date of the Letter

- Recipient Name and Address

- Formal Salutation

- Notice of Account Arrears

- Original Creditor Information

- Total Debt Balance Due

- Deadline for Account Payment

- Approved Payment Methods

- Instructions for Debt Dispute

- Mandatory Consumer Rights Disclosure

- Agency Contact Information

- Professional Letter Sign-Off

Collection Agency Letterhead

A Collection Agency Letterhead is a formal document used to demand payment for overdue debts. It must legally include the agency's name, contact details, and a clear validation notice informing consumers of their rights. Under the Fair Debt Collection Practices Act (FDCPA), the letterhead must not use deceptive imagery or simulate official court documents. Ensuring the legitimacy of the letterhead helps debtors verify the agency and prevents fraud. Accurate identification and professional formatting are essential for regulatory compliance and effective debt recovery communication.

Date of the Letter

The Date of the Letter is a critical administrative element that establishes a legal and chronological record. It should be placed at the top, typically left-aligned or justified, following the sender's contact information. This specific timestamp ensures traceability for future reference, meeting minutes, or contractual obligations. In professional correspondence, always use the full format, such as Month Day, Year, to avoid international confusion. Accurate dating is essential for formal documentation, providing a clear timeline for responses, deadlines, and the historical verification of all business or personal communication.

Recipient Name and Address

Ensuring an accurate Recipient Name and Address is vital for successful mail delivery. A complete physical address includes the street number, apartment or suite details, city, state, and postal code. Always verify the legal name of the individual or business to prevent processing delays or returns. Proper formatting according to postal standards minimizes errors and ensures your package reaches the intended destination efficiently. Double-checking contact details is the most effective way to avoid lost shipments and maintain professional communication standards in both personal and commercial logistics.

Formal Salutation

A formal salutation sets the professional tone for written correspondence. It is essential to use the recipient's correct title and last name to demonstrate respect and competence. If the contact person is unknown, "Dear Hiring Manager" or "To Whom It May Concern" are traditional options, though researching a specific name is preferred. Avoid overly casual greetings like "Hey" in business settings. Proper punctuation, typically a colon in American English, follows the greeting to maintain professional etiquette and ensure a positive first impression.

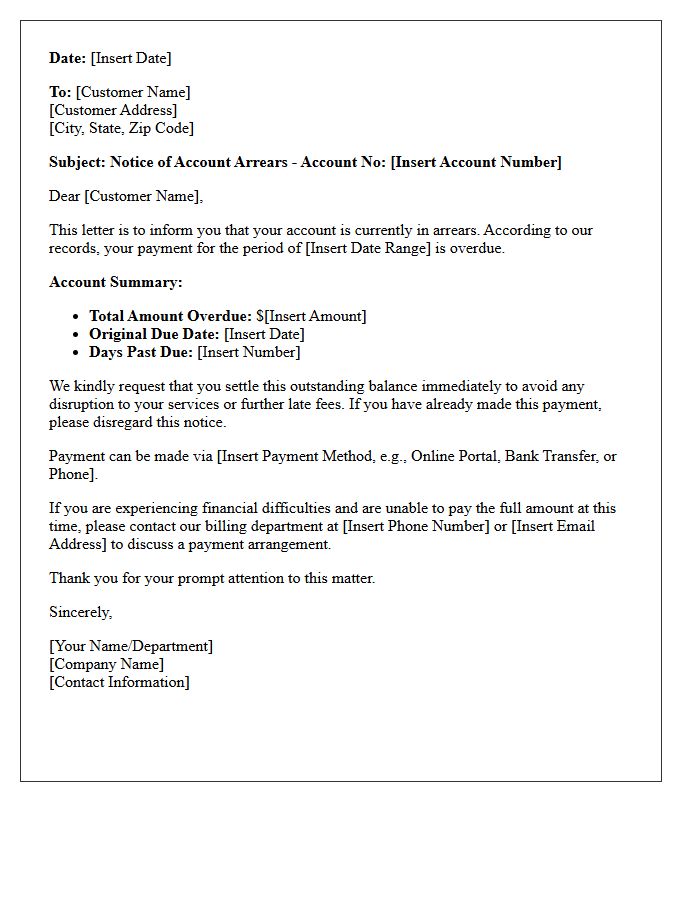

Notice of Account Arrears

A Notice of Account Arrears is a formal communication indicating that your payments are overdue. It serves as a legal warning that you have missed scheduled deadlines, which can negatively impact your credit score and lead to service disruptions. To avoid further financial penalties or collection actions, it is essential to address the outstanding balance immediately. Contacting the creditor to arrange a repayment plan can often prevent legal escalation and help restore your account to good standing. Prompt action is the best way to maintain financial stability and creditworthiness.

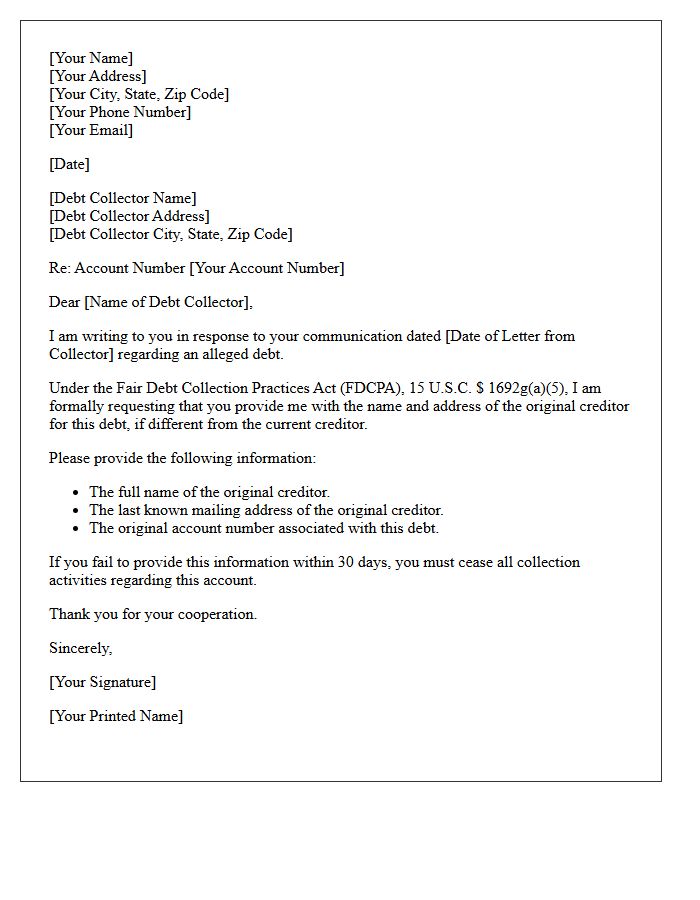

Original Creditor Information

When managing debt, identifying the Original Creditor Information is essential for verifying legal obligations. The original creditor is the institution that first extended the credit, such as a bank or retailer. Under the Fair Debt Collection Practices Act, you have the right to request this entity's name and address in writing. Accurate records help prevent identity theft and ensure you are not paying fraudulent claims. Always cross-reference your credit report to confirm that the balance and history align with the initial lender's records before making payments to third-party collectors.

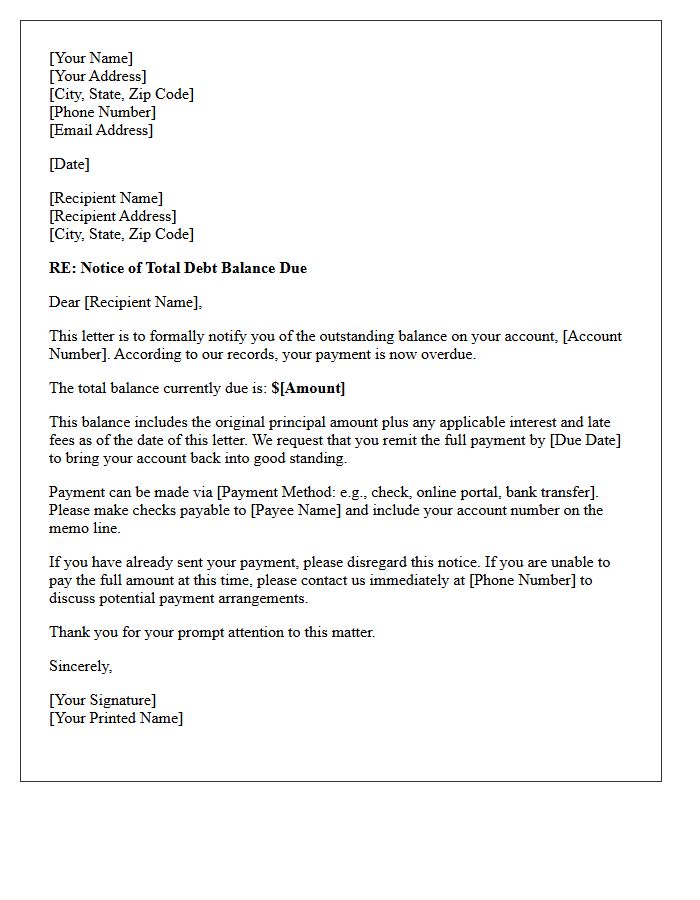

Total Debt Balance Due

The Total Debt Balance Due represents the comprehensive sum of all outstanding liabilities owed to creditors at a specific time. This figure includes the principal amount, accumulated interest, and any applicable fees. Monitoring this balance is critical for maintaining a healthy credit score and ensuring effective financial planning. It is the highlighted metric used by lenders to assess your debt-to-income ratio and overall creditworthiness. Tracking this total allows individuals to prioritize high-interest obligations and develop a structured strategy for achieving long-term financial stability and becoming debt-free.

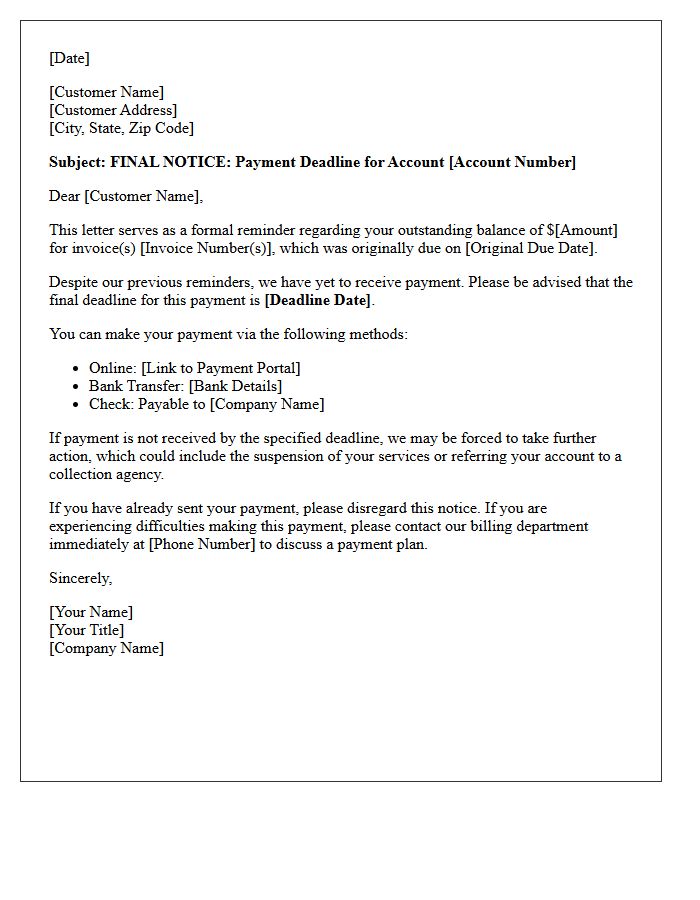

Deadline for Account Payment

Meeting your account payment deadline is essential to maintain financial health and service continuity. Always prioritize the due date to avoid late fees, penalty interest, or negative impacts on your credit score. Many providers offer a grace period, but consistently missing timelines can result in account suspension. To ensure security, schedule automated transfers or reminders at least two days early to account for processing times. Timely settlement protects your reputation and ensures uninterrupted access to essential services.

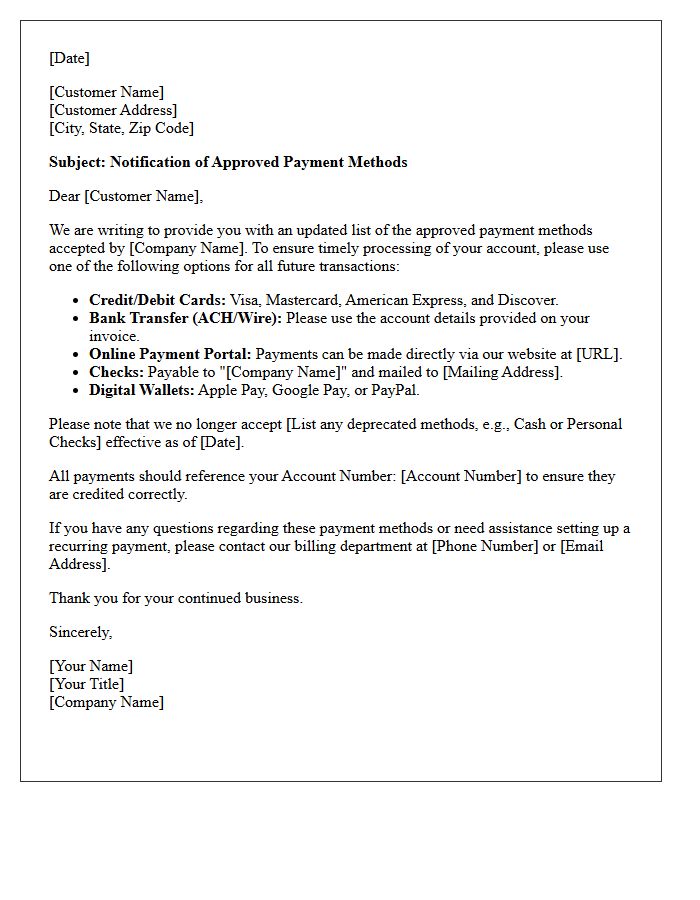

Approved Payment Methods

When completing a transaction, using Approved Payment Methods ensures both security and speed. Most platforms accept major credit cards, debit cards, and digital wallets like PayPal. For mobile users, Apple Pay and Google Pay offer seamless integration. Always verify if local options or bank transfers are supported before checkout. Using authorized channels protects your financial data from fraud while providing a valid proof of purchase for refunds or disputes. Confirming accepted methods beforehand prevents payment failures and ensures a smooth, secure checkout experience every time.

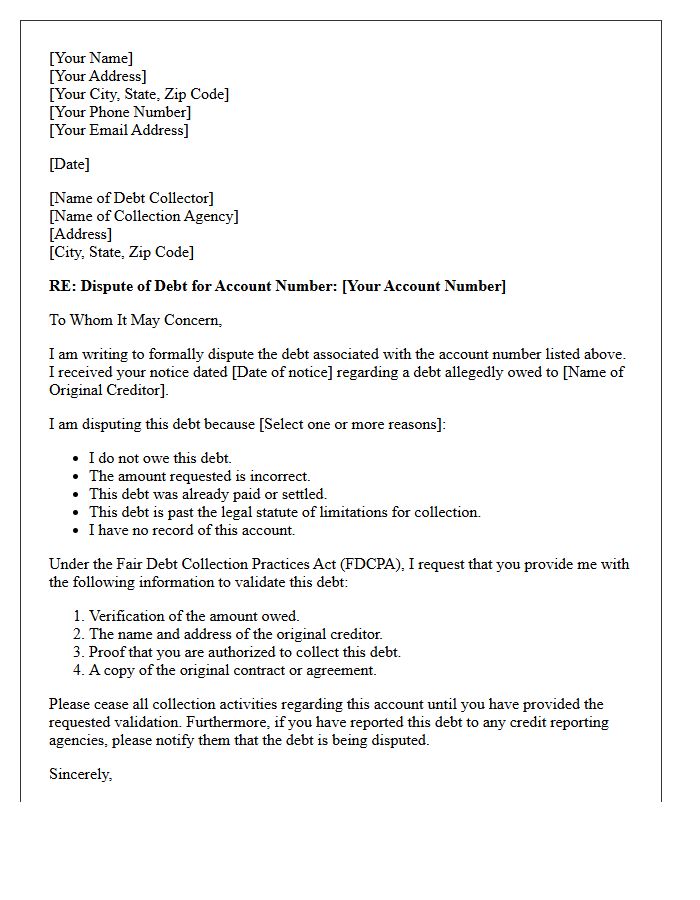

Instructions for Debt Dispute

When initiating a debt dispute, you must act quickly to protect your consumer rights. Send a formal validation letter to the collection agency within thirty days of their initial contact. Clearly state that you are disputing the accuracy of the balance or the ownership of the account. Demand written proof of the original contract and payment history. To ensure a legal paper trail, always send your correspondence via certified mail with a return receipt requested. This process legally compels collectors to cease communication until they provide official verification of the debt.

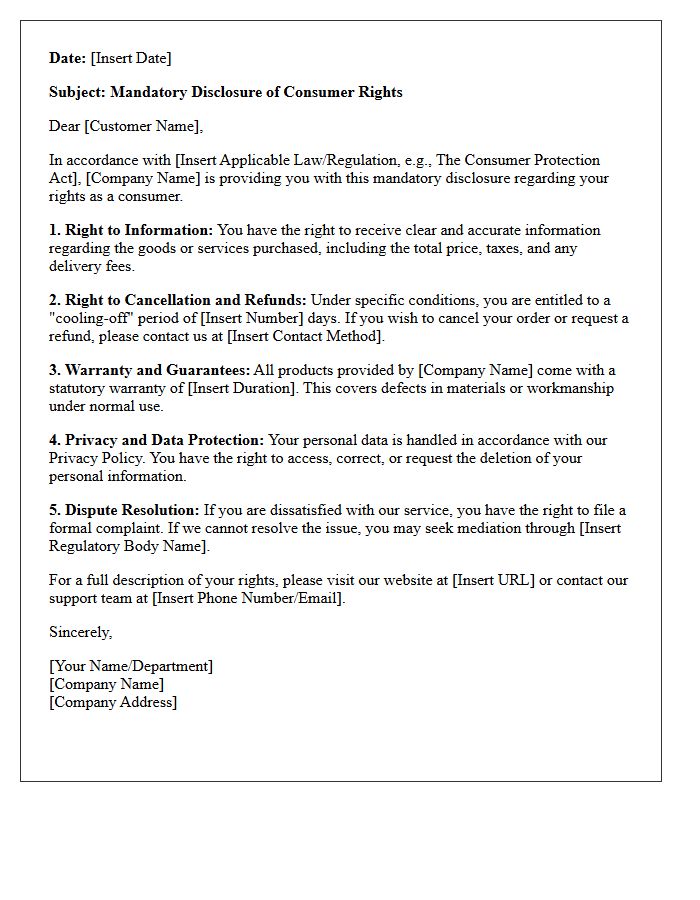

Mandatory Consumer Rights Disclosure

A Mandatory Consumer Rights Disclosure is a legally required notification that businesses must provide to inform customers of their statutory protections. These disclosures ensure transparency regarding refund policies, warranties, and data privacy rights under regulations like the Australian Consumer Law or the CCPA. Failing to present these terms clearly can lead to legal penalties and contract invalidation. It is essential for consumers to review these documents to understand their legal recourse and for businesses to remain compliant with consumer protection standards during every transaction.

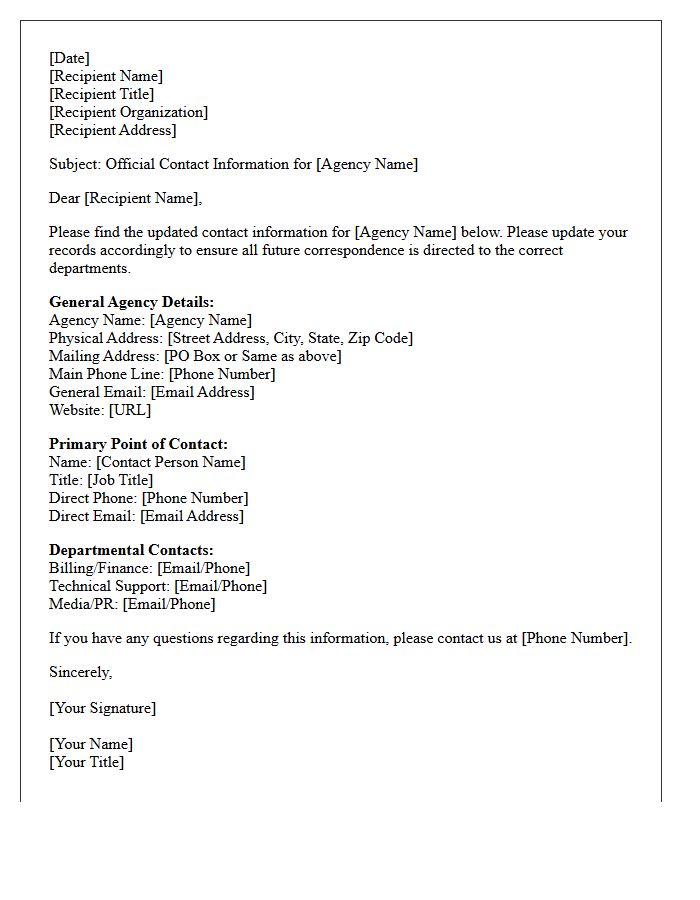

Agency Contact Information

Maintaining accurate Agency Contact Information is vital for seamless communication and service delivery. This data typically includes physical addresses, verified email addresses, and direct phone lines. Ensuring these details are current allows stakeholders to resolve inquiries quickly and reduces administrative delays. Always confirm the official website to prevent reaching fraudulent entities. Accessibility to a designated point of contact streamlines collaboration, enhances transparency, and fosters trust between the agency and the public.

Professional Letter Sign-Off

Choosing the right professional letter sign-off is essential for maintaining credibility and tone. Your closing serves as the final impression, bridging your message to your signature. Common formal options include "Sincerely" or "Best regards," which suit most business contexts. Ensure the sign-off matches the level of formality established in your salutation. For digital correspondence, "Best" or "Thank you" remains effective. Always follow the closing with a comma, then your name and contact details to ensure a polished conclusion to your professional communication.

What is a First Notice of Account Arrears?

A First Notice of Account Arrears is a formal communication sent by a creditor to notify a customer that a scheduled payment has been missed. This document serves as an initial reminder to settle the outstanding balance and bring the account back into good standing.

How long after a missed payment is a first arrears notice sent?

Most creditors issue a first notice of arrears between 7 and 14 days after the payment due date. The exact timing depends on the terms of the credit agreement and the internal billing cycle of the service provider or lender.

Will receiving a first notice of account arrears affect my credit score?

A first notice itself is a warning and may not immediately impact your credit score if the balance is paid within the grace period. However, if the payment remains overdue for more than 30 days, the creditor may report the delinquency to credit bureaus, which can lower your credit rating.

What should I do if I receive a first notice of arrears but have already paid?

If you have already made the payment, allow 3 to 5 business days for processing. If the notice was sent after you paid, you should contact the creditor's billing department with your transaction receipt or reference number to ensure your account record is updated correctly.

What are the consequences of ignoring a first notice of account arrears?

Ignoring a first notice can lead to late payment fees, the accumulation of interest, and a transition to more serious collection actions. Continued non-payment may result in service disconnection, a formal "Notice of Default," and potential legal action or debt collection agency involvement.

Comments