Protect your consumer rights by sending a Disputed Debt Validation Response Notice to collection agencies. This formal letter demands evidence of the debt's accuracy and the collector's legal authority to pursue payment. Challenging unverified claims helps prevent credit score damage and ensures fair treatment under financial regulations. To assist your process, below are some ready to use templates.

Image cover: How to Effectively Dispute and Validate Debt: Professional Response Templates and Expert Guidance

Letter Samples List

- Initial Disputed Debt Validation Response Letter

- Complete Itemized Debt Verification Letter

- Original Creditor Disclosure Response Letter

- Insufficient Dispute Information Request Letter

- Identity Theft Fraudulent Debt Resolution Letter

- Previously Validated Debt Reiteration Letter

- Detailed Transaction History Validation Letter

- Time-Barred Disputed Debt Acknowledgment Letter

- Partial Account Balance Verification Letter

- Resolved Paid Account Dispute Letter

- Unsubstantiated Debt Dispute Final Notice Letter

- Enclosed Consumer Validation Documents Letter

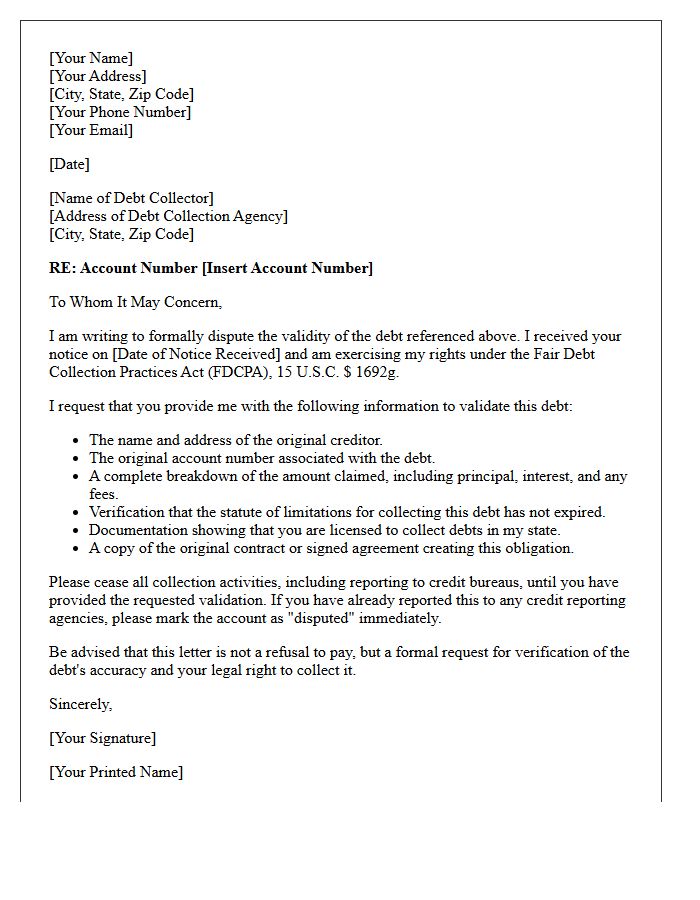

Initial Disputed Debt Validation Response Letter

An Initial Disputed Debt Validation Response Letter is a critical legal tool used to challenge unverified claims under the Fair Debt Collection Practices Act (FDCPA). Sending this document within thirty days of the first contact forces collectors to provide proof of the debt's validity and their legal right to collect. This process ensures accuracy, prevents identity theft errors, and halts collection activities until documentation is produced. Using formal written communication creates a vital paper trail for your financial protection and potential legal defense against predatory practices.

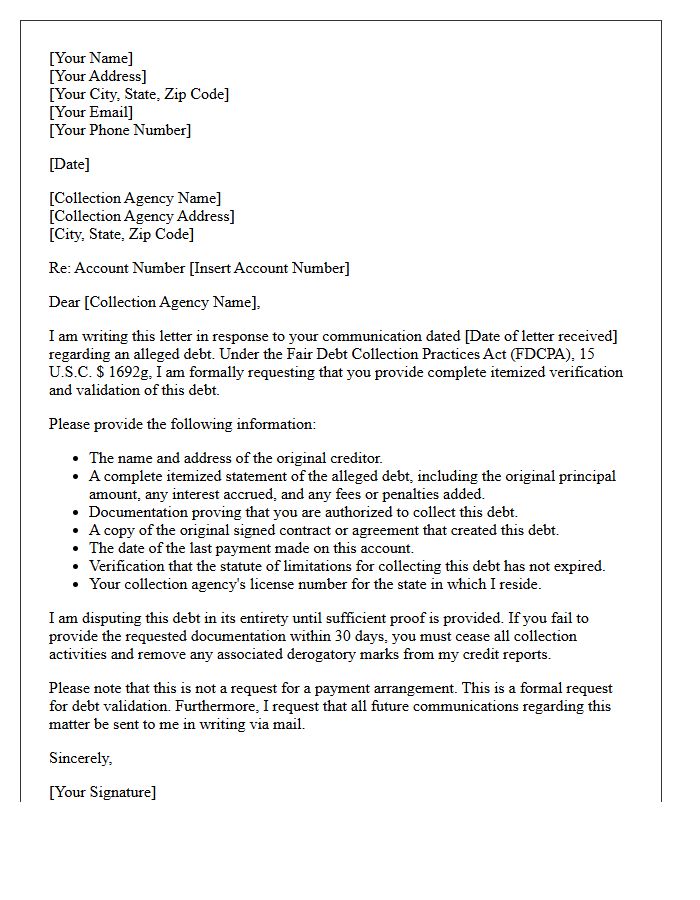

Complete Itemized Debt Verification Letter

A Complete Itemized Debt Verification Letter is a formal legal request sent to collectors to validate a debt's accuracy. Under the Fair Debt Collection Practices Act, you have the right to demand original creditor information, full payment histories, and proof of legal authority to collect. This document forces transparency, ensuring you are not paying for expired or fraudulent claims. Sending this letter within thirty days of initial contact protects your consumer rights and can potentially halt unfair collection activities while the agency gathers necessary supporting documentation.

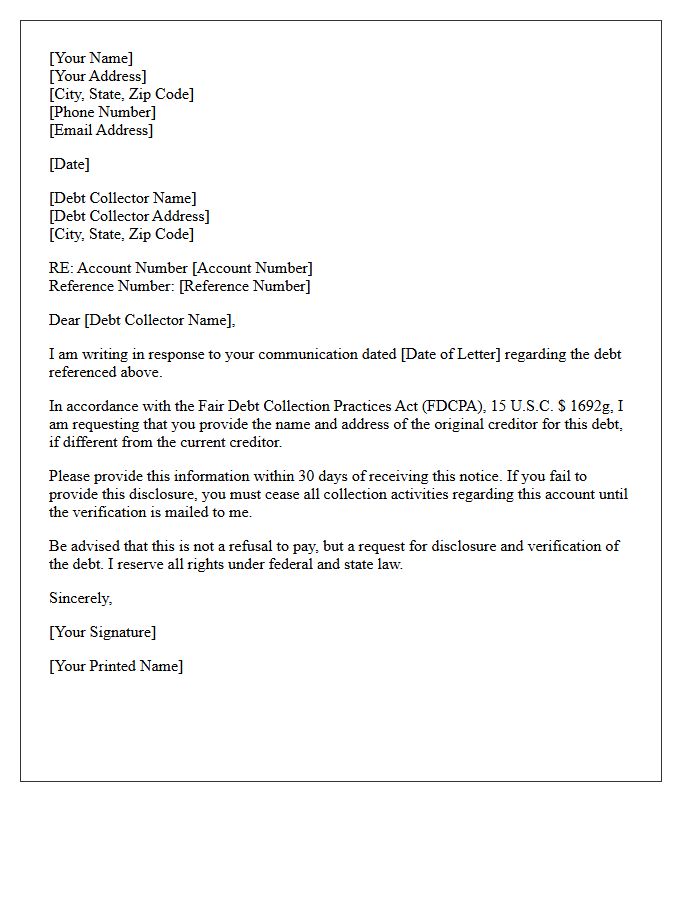

Original Creditor Disclosure Response Letter

An Original Creditor Disclosure Response Letter is a formal document sent by a lender following a debt validation request. It serves to verify the debt's legitimacy by providing the name and address of the original creditor, the current balance, and account history. Legally required under the Fair Debt Collection Practices Act (FDCPA), this response ensures consumer transparency and prevents identity theft or incorrect billing. Reviewing this document carefully allows you to confirm your financial obligations before making payments or disputing errors with credit bureaus to protect your credit score.

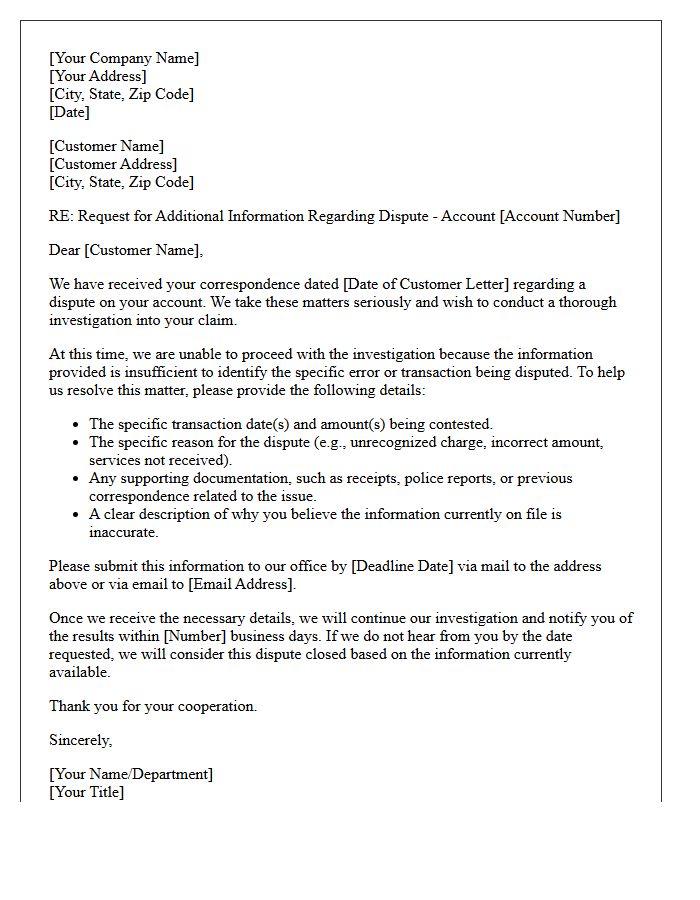

Insufficient Dispute Information Request Letter

An Insufficient Dispute Information Request Letter is a formal notice sent by creditors or credit bureaus when a consumer's dispute lacks supporting evidence. To ensure a successful investigation, you must provide specific details, such as account numbers and documentation of the error. Failing to respond with clear, factual data may lead the agency to dismiss your claim as frivolous. Providing comprehensive information is the most effective way to protect your consumer rights and ensure your credit report reflects accurate financial history under the Fair Credit Reporting Act.

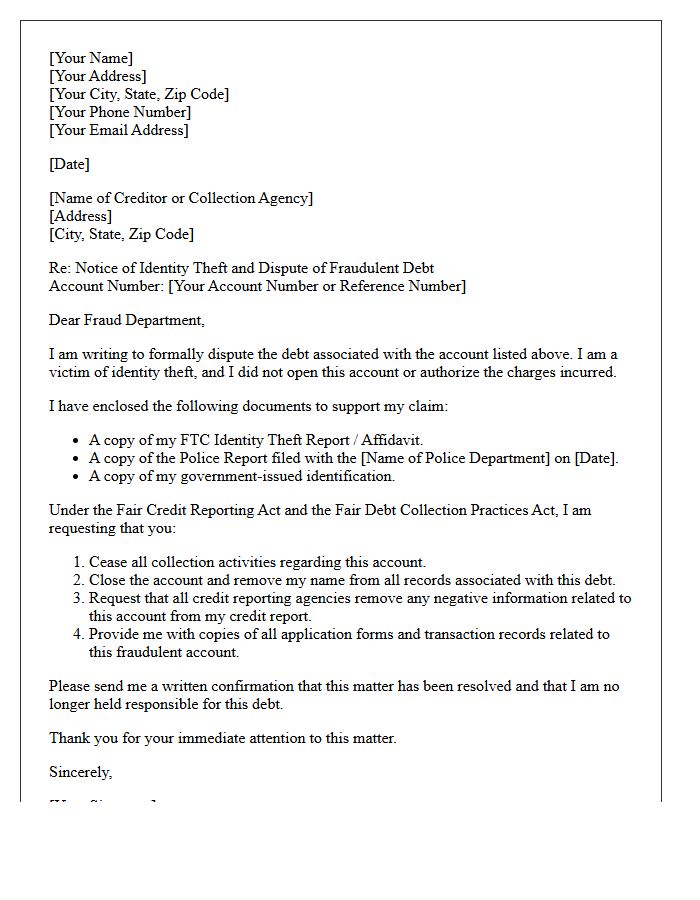

Identity Theft Fraudulent Debt Resolution Letter

An Identity Theft Fraudulent Debt Resolution Letter is a formal document used to dispute unauthorized debts resulting from stolen personal information. It is crucial to send this written notice to creditors and credit bureaus to initiate an investigation under the Fair Credit Reporting Act. Timely action ensures you are not held liable for fraudulent charges. For maximum legal protection, include a copy of your Identity Theft Report from the FTC and use certified mail to prove delivery, effectively clearing your financial record of criminal activity.

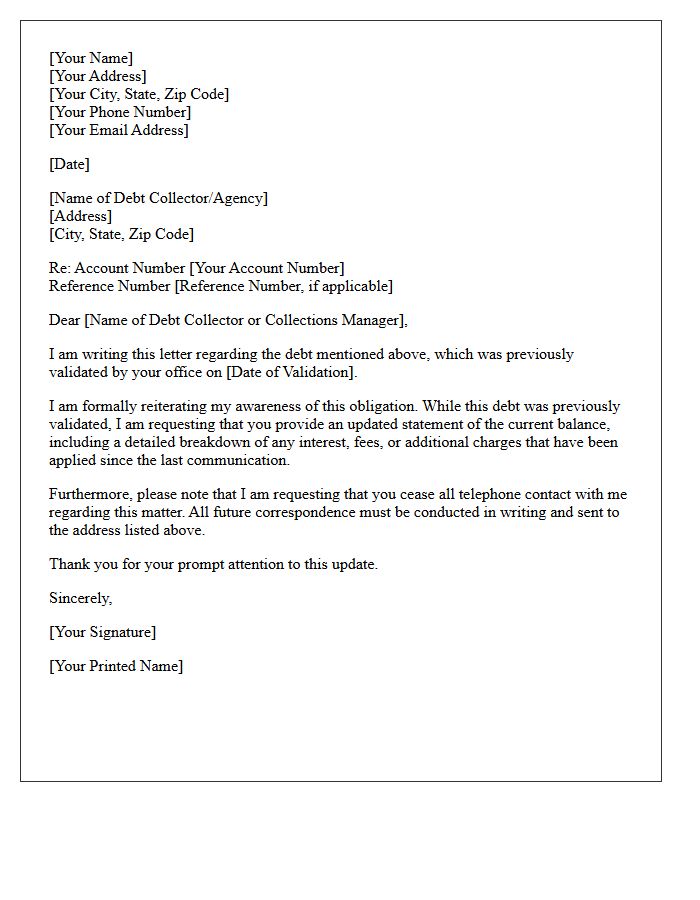

Previously Validated Debt Reiteration Letter

A Previously Validated Debt Reiteration Letter is a formal response sent by a creditor or collector when a consumer disputes a debt that has already been verified. Its primary purpose is to reaffirm the debt's legitimacy by referencing prior validation documents. This letter serves as legal notice that the collector will continue recovery efforts, as they have already met Fair Debt Collection Practices Act (FDCPA) requirements. Understanding this document is crucial for consumers to recognize that further disputes require new evidence rather than repeating initial verification requests.

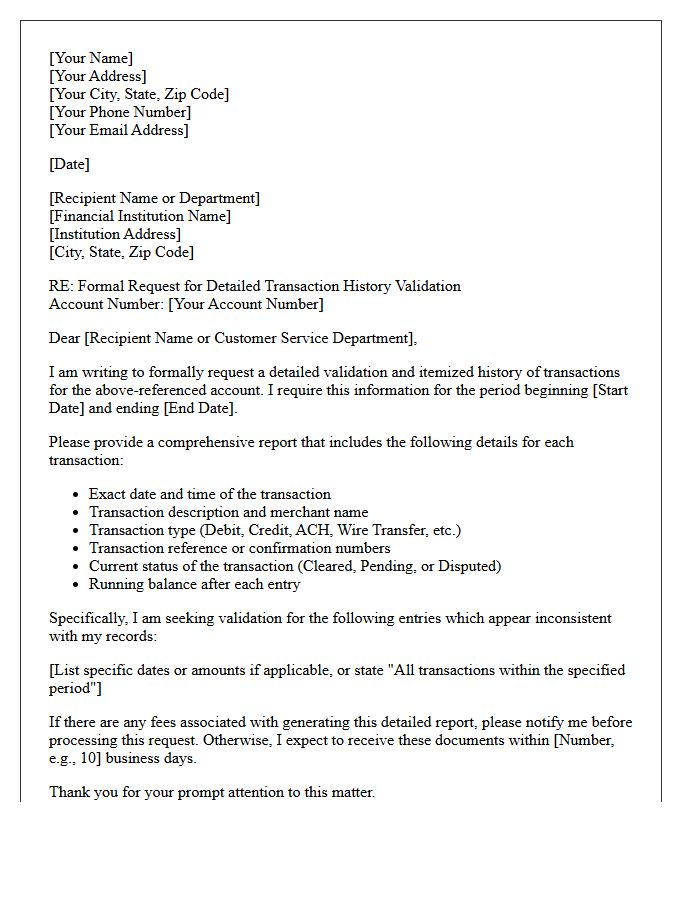

Detailed Transaction History Validation Letter

A Detailed Transaction History Validation Letter is a formal request sent to creditors to verify the accuracy of a debt. It requires the collector to provide an itemized breakdown of all charges, payments, and interest accrued since the original balance. This document is essential for identifying billing errors or unauthorized fees before making payments. Under the Fair Debt Collection Practices Act, consumers have the legal right to dispute discrepancies. Using this letter ensures transparency and protects your financial rights by forcing the agency to prove the validity of the total amount claimed.

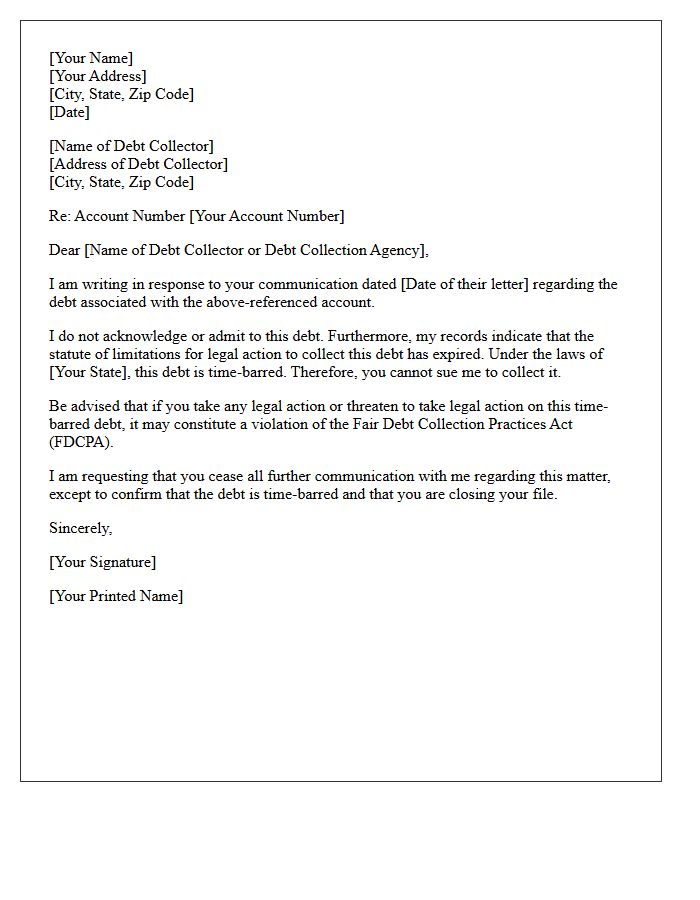

Time-Barred Disputed Debt Acknowledgment Letter

A Time-Barred Disputed Debt Acknowledgment Letter is a critical legal document used when a creditor attempts to collect an expired debt. Once the statute of limitations passes, you are no longer legally required to pay. However, any written acknowledgment or partial payment can inadvertently restart the clock on the debt's expiration. This letter formally disputes the claim and asserts your legal protection, preventing collectors from suing you for old balances. Understanding your rights ensures you do not accidentally revive a dead financial obligation through improper communication.

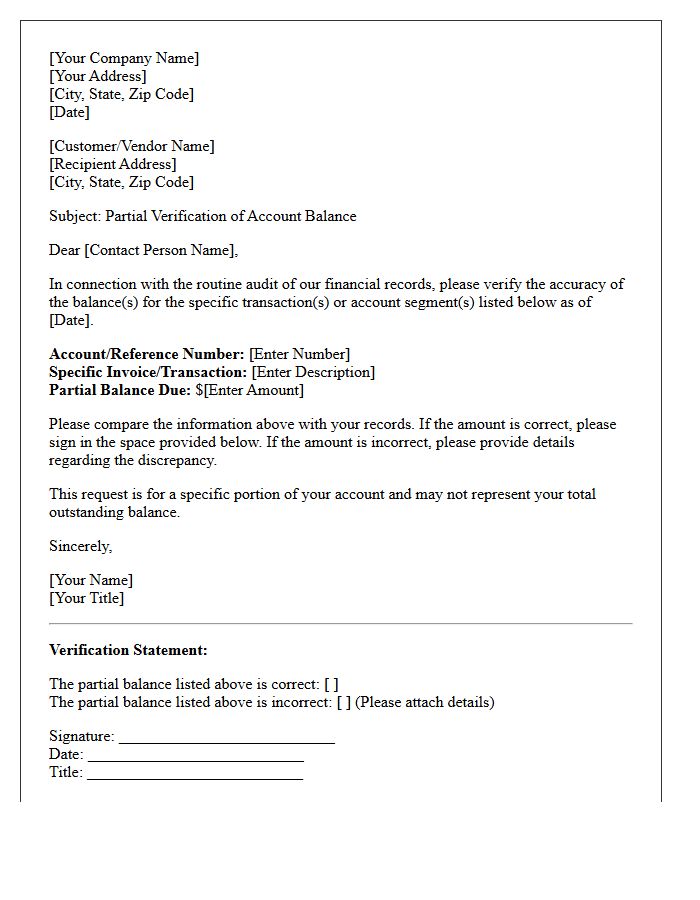

Partial Account Balance Verification Letter

A Partial Account Balance Verification Letter is a formal document used to confirm specific portions of a financial statement rather than the entire total. This process is essential for auditing purposes and ensuring transaction accuracy. It serves as written evidence that a specific asset or debt exists as recorded on a given date. Businesses use these letters to maintain transparency and resolve discrepancies with creditors or financial institutions. By verifying individual balances, stakeholders can validate financial integrity and ensure compliance with standard accounting practices.

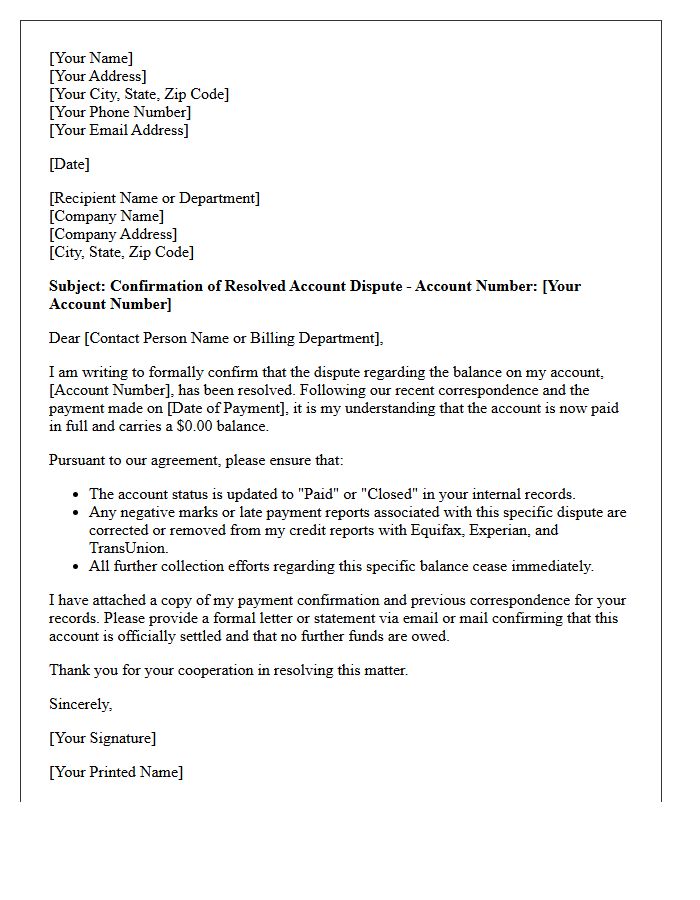

Resolved Paid Account Dispute Letter

A Resolved Paid Account Dispute Letter serves as formal proof that a previously contested debt is settled. It is crucial to verify payment and ensure the creditor updates your credit report to reflect a zero balance. This document protects your financial reputation by preventing future collection attempts on the same debt. Always include your account details, the settlement date, and a clear request for a status update with all major credit bureaus. Maintaining this written record is essential for long-term credit score protection and resolving any recurring reporting errors.

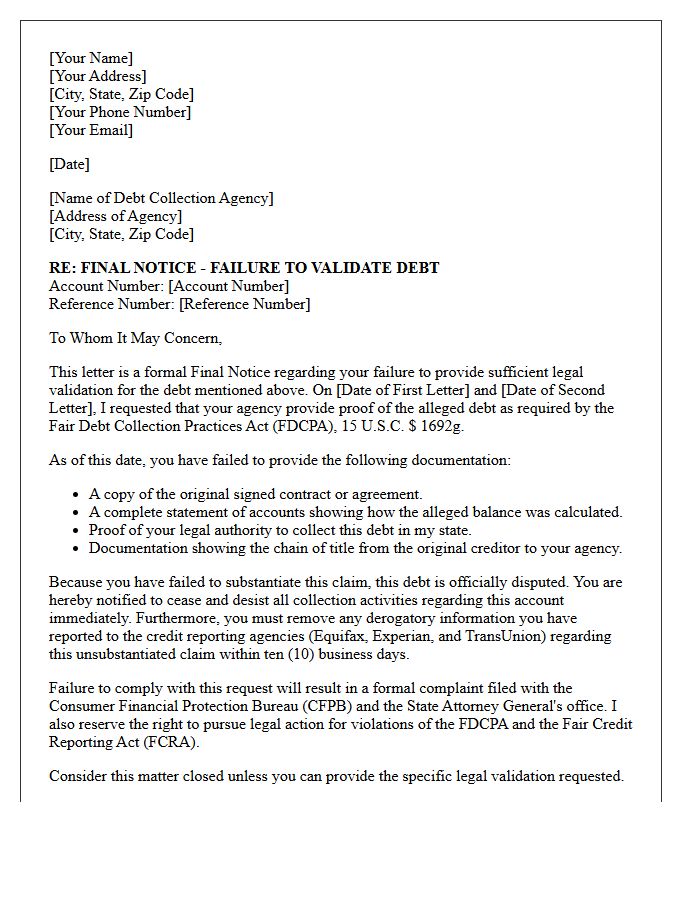

Unsubstantiated Debt Dispute Final Notice Letter

An Unsubstantiated Debt Dispute Final Notice Letter represents a critical formal communication from a creditor or collection agency. It signifies that the consumer has failed to provide verifiable evidence or legal documentation to support their claim that the debt is invalid. This notice often serves as a final warning before the creditor initiates aggressive legal action or reports the delinquency to credit bureaus. Receiving this document means the dispute process is concluding, and immediate professional advice is recommended to avoid judgment liens or wage garnishment.

Enclosed Consumer Validation Documents Letter

An Enclosed Consumer Validation Documents Letter is a critical tool for debt verification. Under the Fair Debt Collection Practices Act, this formal response ensures creditors provide legal proof of an alleged debt. It typically includes original contracts or payment histories to confirm the amount and ownership. Reviewing these documents is essential for disputing inaccuracies and protecting your credit score. If a collector fails to provide this validation, they must cease collection activities, making this letter your primary defense against unverified claims and potential identity theft.

What is a Disputed Debt Validation Response Notice?

A Disputed Debt Validation Response Notice is a formal written communication sent by a consumer to a debt collector to challenge the validity of a debt. Under the Fair Debt Collection Practices Act (FDCPA), this notice requires the collector to provide proof that the debt is accurate, legally owed, and that they have the right to collect it.

When should I send a debt validation response notice?

You should send this notice within 30 days of receiving the initial "G-Notice" or first collection letter from a debt collector. While you can dispute a debt at any time, sending the notice within this 30-day window legally compels the collector to cease collection activities until the debt is verified.

What information should be included in a debt validation letter?

A comprehensive response notice should include a clear statement that you are disputing the debt, a request for the original creditor's name and address, an itemized breakdown of the total amount owed, and a demand for documentation proving the collector is authorized to collect the specific account.

Does a debt validation notice stop a debt collector from calling?

Yes. Once a collector receives a timely written dispute, the FDCPA mandates that they stop all collection efforts, including phone calls and letters, until they provide the consumer with the requested validation documents. If they continue to contact you before providing proof, they may be in violation of federal law.

What happens if a debt collector fails to validate the debt?

If a debt collector cannot provide adequate documentation to verify the debt, they are legally prohibited from continuing collection efforts or reporting the debt to credit bureaus. In such cases, you may use the lack of validation as grounds to request the removal of the account from your credit report.

Comments