A Payday Loan Debt Validation Notice is a legal tool used to dispute unauthorized or inaccurate loan claims. Sending this letter requires debt collectors to provide documented proof that you legally owe the specific amount. This process protects your consumer rights and helps stop aggressive collection tactics. To help you exercise these rights effectively, below are some ready to use templates.

Image cover: Stop Payday Loan Collectors: Debt Validation Letter Templates and Guide

Letter Samples List

- Initial Payday Loan Debt Validation Notice Letter

- Payday Loan Debt Verification Request Letter

- Disputed Payday Loan Debt Validation Letter

- Second Request Payday Loan Debt Validation Letter

- Payday Loan Debt Collection Cease and Desist Letter

- Fraudulent Payday Loan Debt Dispute Letter

- Proof of Payday Loan Debt Validation Letter

- Payday Loan Debt Settlement Offer Letter

- Payday Loan Debt Acknowledgment Letter

- Final Payday Loan Debt Collection Warning Letter

- Payday Loan Identity Theft Debt Validation Letter

- Time-Barred Payday Loan Debt Dispute Letter

- Payday Loan Debt Payment Arrangement Letter

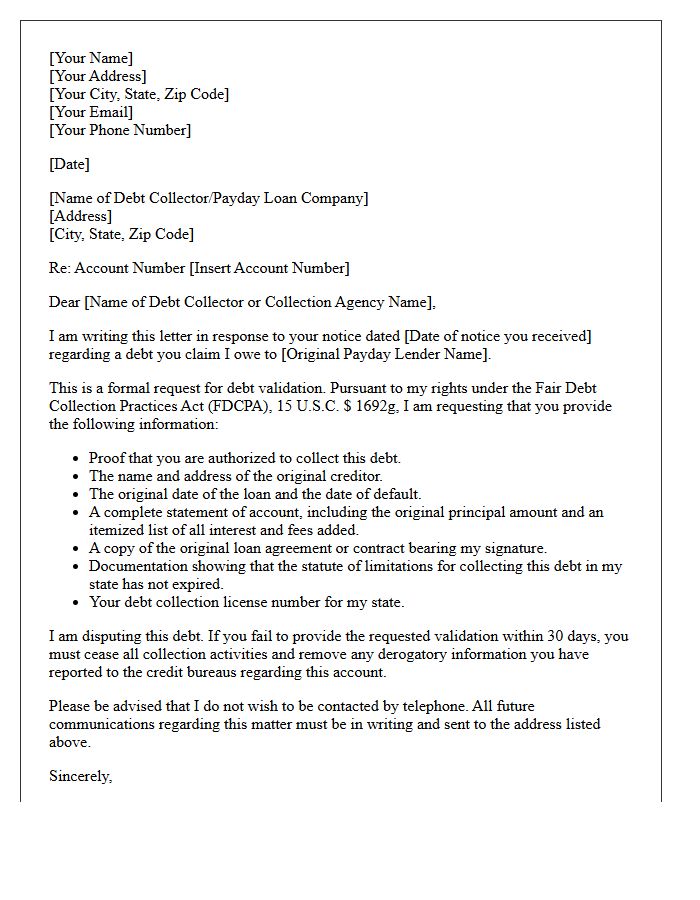

Initial Payday Loan Debt Validation Notice Letter

The Initial Payday Loan Debt Validation Notice is a critical legal document that triggers your right to verify an alleged debt. Under the Fair Debt Collection Practices Act (FDCPA), collectors must provide specific details about the balance and creditor within five days of contact. You have a thirty-day window to submit a written dispute, which legally forces the agency to halt collections until they provide proof of the debt's validity. Reviewing this notice carefully prevents unauthorized withdrawals and protects you from paying fraudulent or expired payday loan claims.

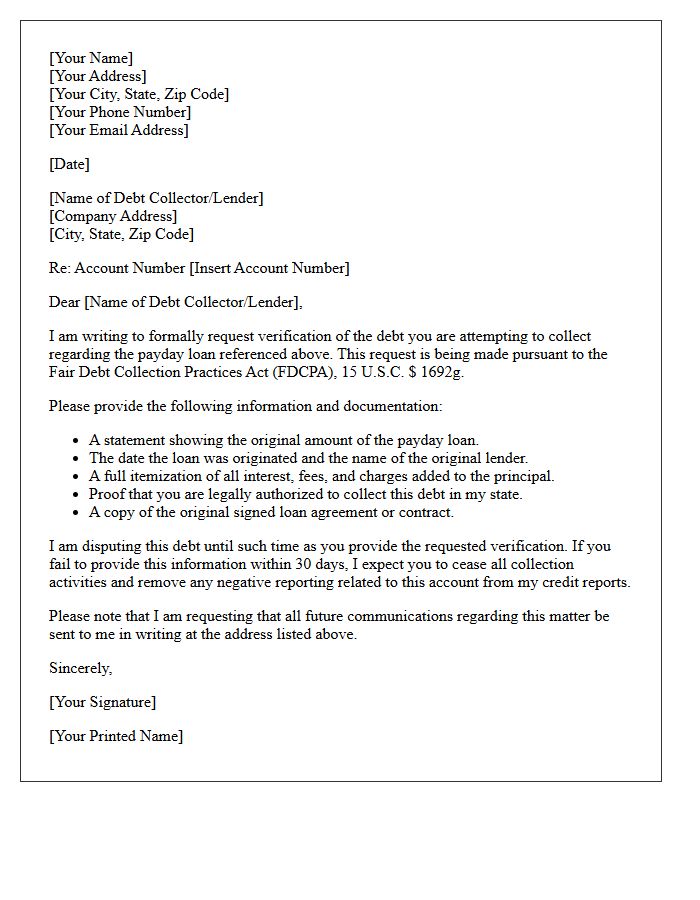

Payday Loan Debt Verification Request Letter

A Payday Loan Debt Verification Request Letter is a formal legal tool used to dispute or confirm the validity of a payday loan. Under the Fair Debt Collection Practices Act (FDCPA), sending this notice forces collectors to provide written evidence of the original contract, total balance, and their legal right to collect. This process protects consumers from predatory lending practices, identity theft, or statute-barred debts. To be effective, you must mail the request within 30 days of the first contact to pause collection activities until full verification is provided.

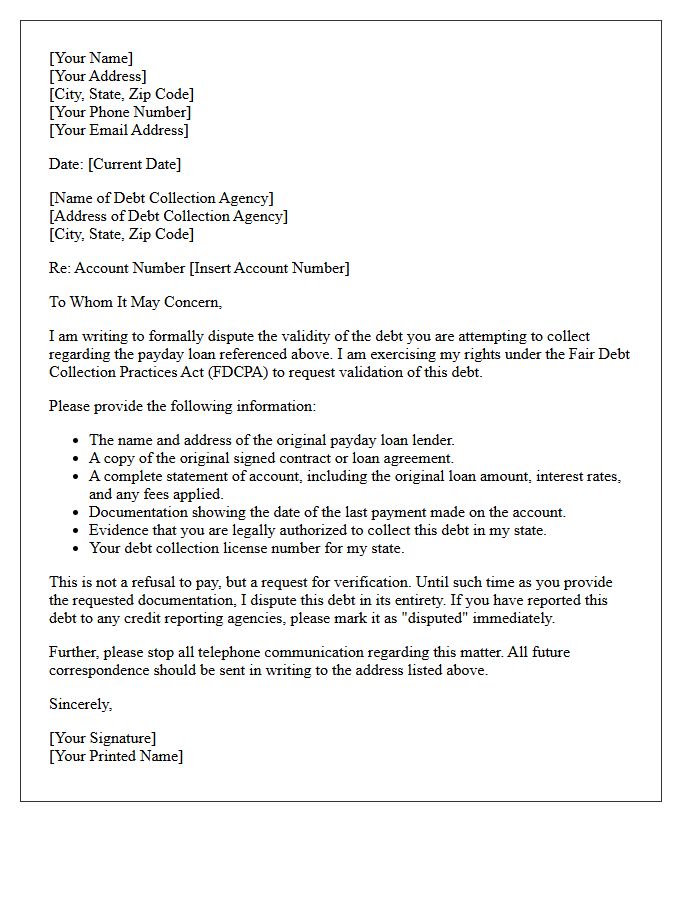

Disputed Payday Loan Debt Validation Letter

A Disputed Payday Loan Debt Validation Letter is a formal legal request requiring a creditor to provide verified proof that a debt is legitimate, accurate, and legally owed by you. Under the Fair Debt Collection Practices Act (FDCPA), sending this notice within thirty days of initial contact halts collection activities until documentation is provided. This essential tool protects consumers from predatory lending practices, unauthorized withdrawals, and fraudulent claims by ensuring the collector has the legal right to pursue the balance. Always keep copies for your records to maintain strong consumer protection evidence.

Second Request Payday Loan Debt Validation Letter

A Second Request Payday Loan Debt Validation Letter is a critical follow-up used when a collection agency fails to respond to your initial inquiry. Legally, under the FDCPA, collectors must provide verified proof of the debt's origin and amount. Sending this formal notice creates a paper trail that can stop aggressive collection tactics. If the agency continues reporting or calling without providing documentation, their actions may become legally unenforceable. This second demand reinforces your consumer rights and protects your credit score from inaccurate or fraudulent payday loan claims.

Payday Loan Debt Collection Cease and Desist Letter

A Payday Loan Cease and Desist Letter is a formal legal notice used to stop harassment from aggressive debt collectors. By exercising your rights under the Fair Debt Collection Practices Act (FDCPA), you can legally demand that a collector stop all direct communication with you. Sending this document via certified mail creates a paper trail, ensuring the agency must cease contact or face potential legal penalties. This tool is essential for regaining privacy and stopping unauthorized communication at your workplace or home while you seek financial resolution.

Fraudulent Payday Loan Debt Dispute Letter

A Fraudulent Payday Loan Debt Dispute Letter is a formal legal notification sent to credit bureaus and collection agencies to contest unauthorized accounts. To be effective, you must clearly state that the debt is the result of identity theft and demand immediate removal from your credit report. Attach supporting documentation, such as an identity theft affidavit or police report, to strengthen your claim. Sending this letter via certified mail ensures a paper trail, forcing lenders to investigate and verify the debt's validity according to the Fair Credit Reporting Act.

Proof of Payday Loan Debt Validation Letter

A Proof of Payday Loan Debt Validation Letter is a formal legal request sent to collectors to verify a debt's legitimacy. Under the Fair Debt Collection Practices Act, consumers have the right to demand written evidence that the collector owns the account and the amount is accurate. Sending this document stops collection activities until the agency provides original loan agreements and payment history. It is a critical tool for identifying fraudulent claims or expired statutes of limitations, protecting your financial rights and preventing unlawful wage garnishments or harassment.

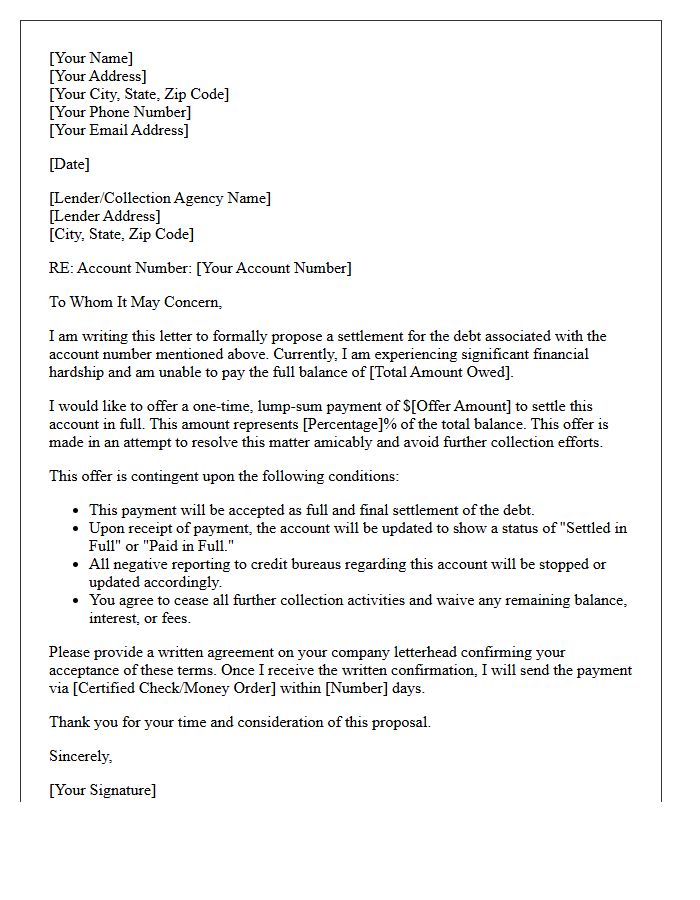

Payday Loan Debt Settlement Offer Letter

A Payday Loan Debt Settlement Offer Letter is a formal proposal sent to lenders to resolve outstanding high-interest debt for a reduced lump sum. To be effective, the letter must clearly state your hardship, account details, and the specific amount you can afford to pay. Successfully negotiating a settlement can stop aggressive collection calls and prevent legal action. Always request a written agreement confirming that the payment satisfies the total balance in full before sending funds. This process helps borrowers regain financial stability by eliminating predatory interest cycles and resolving debt permanently.

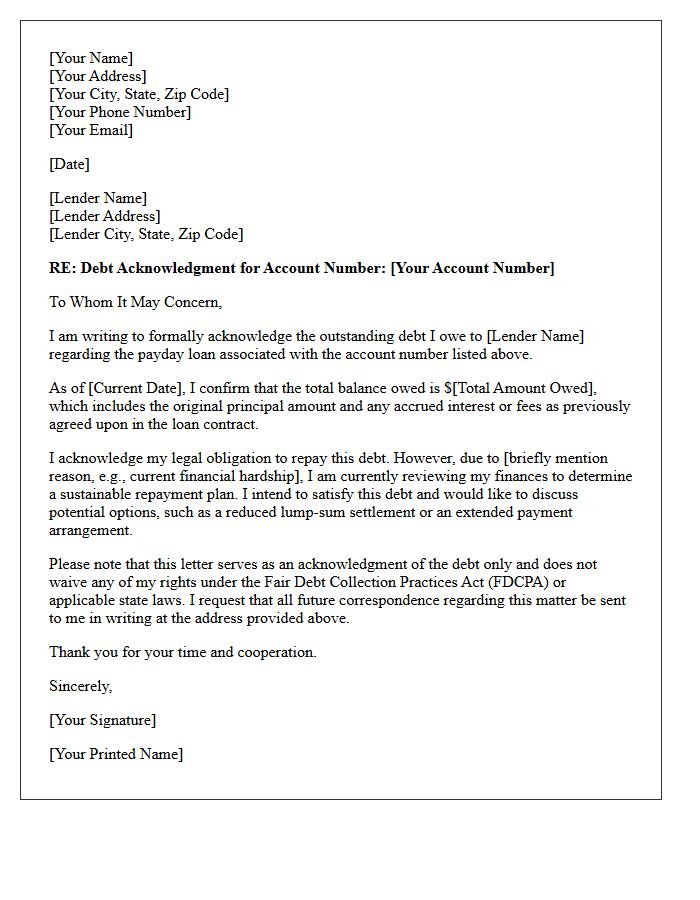

Payday Loan Debt Acknowledgment Letter

A Payday Loan Debt Acknowledgment Letter is a formal document where a borrower confirms the validity of an outstanding balance. Signing this letter restarts the statute of limitations, legally extending the timeframe a lender has to sue for collection. It typically outlines the total amount owed, interest rates, and a proposed repayment plan. Before signing, ensure the debt details are accurate to avoid unintentionally reviving time-barred obligations. This written admission serves as critical evidence in legal proceedings, making it vital to verify all terms before providing a signature.

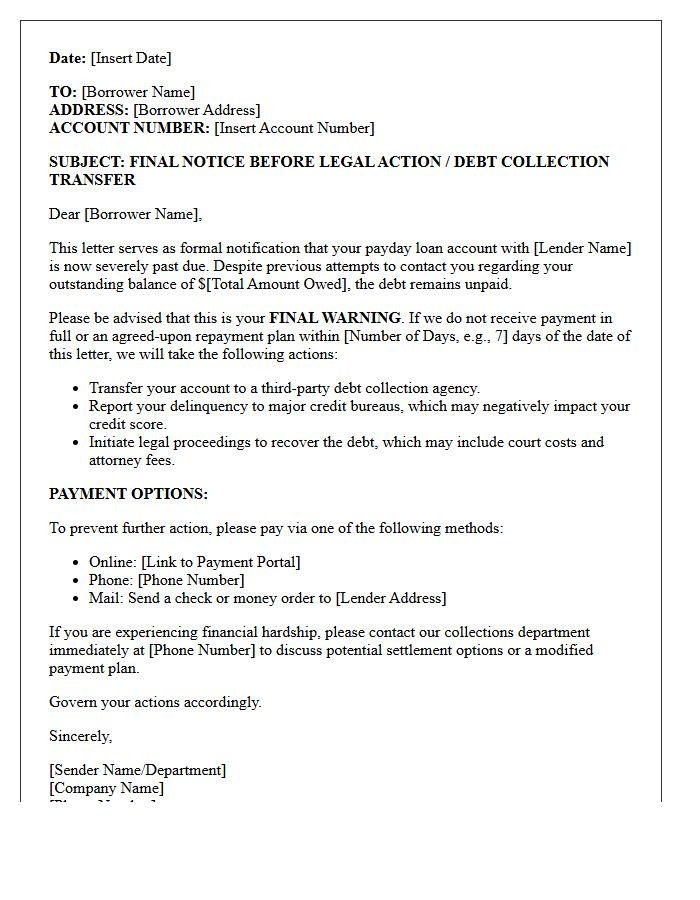

Final Payday Loan Debt Collection Warning Letter

A Final Payday Loan Debt Collection Warning Letter is a formal notification indicating that your account is moving toward legal action or professional debt recovery. This document serves as a final opportunity to settle the balance before the creditor initiates a lawsuit, reports the default to credit bureaus, or sells the debt to a third party. To protect your rights, you must verify the debt's validity in writing immediately. Responding promptly can help you negotiate a settlement or payment plan to avoid long-term damage to your credit score and potential wage garnishment.

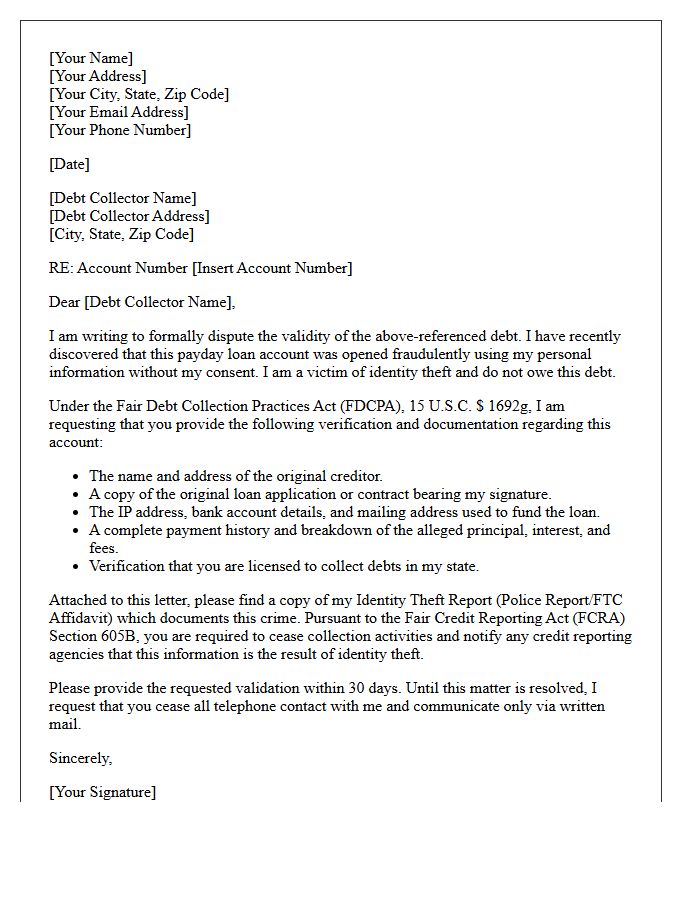

Payday Loan Identity Theft Debt Validation Letter

A Payday Loan Identity Theft Debt Validation Letter is a critical legal tool used to dispute fraudulent claims. If a lender pursues you for a loan you never authorized, this document forces them to provide verifiable evidence of the debt's legitimacy. Under the Fair Debt Collection Practices Act, you must send this notice within thirty days of initial contact. It requires the collector to supply original contracts and IP logs, effectively stopping collection activity on identity theft accounts while protecting your credit score from unauthorized negative entries.

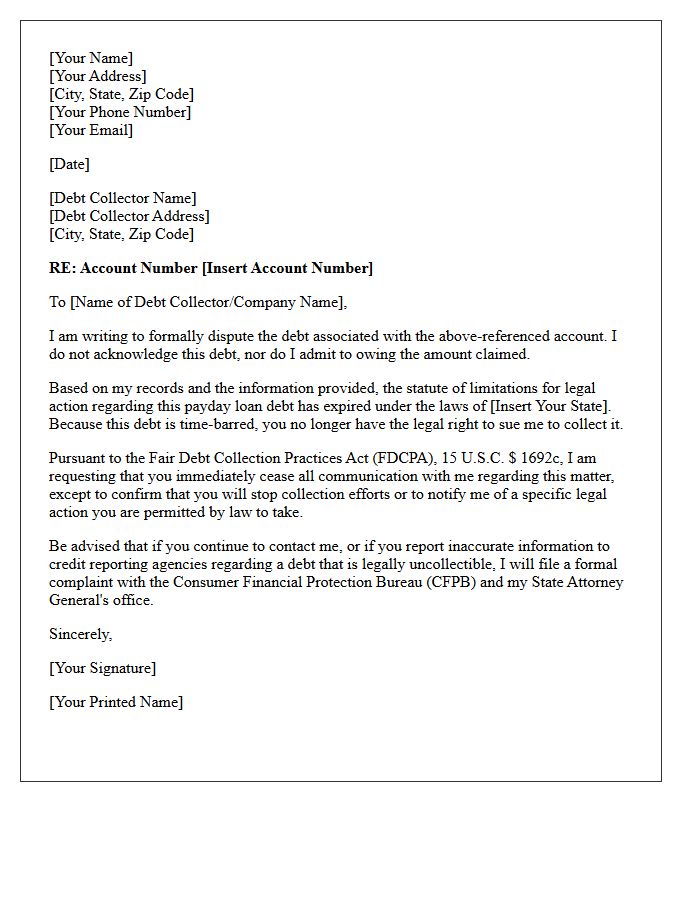

Time-Barred Payday Loan Debt Dispute Letter

A Time-Barred Payday Loan Debt Dispute Letter is a formal notice sent to collectors when a debt exceeds the legal statute of limitations. This document asserts your rights under the Fair Debt Collection Practices Act, effectively stopping collection efforts for old accounts that are no longer legally enforceable in court. By submitting this written dispute, you prevent collectors from pursuing expired debts and protect your financial standing. Always send the letter via certified mail to maintain a paper trail and avoid inadvertently restarting the limitation period through partial payments.

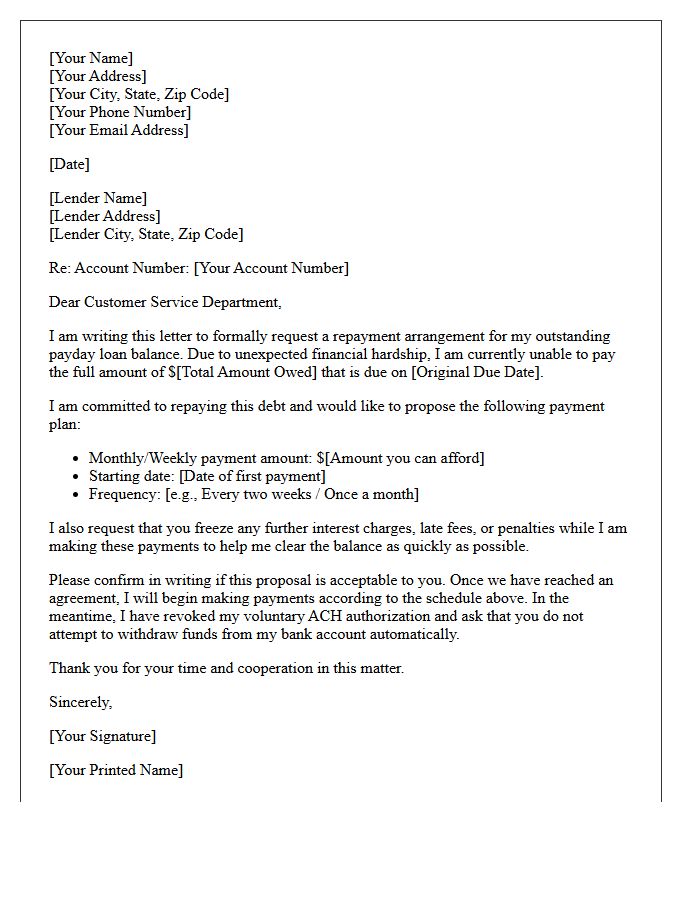

Payday Loan Debt Payment Arrangement Letter

A Payday Loan Debt Payment Arrangement Letter is a formal proposal sent to lenders to negotiate affordable repayment terms. This document is essential when you cannot meet original deadlines due to financial hardship. It should clearly outline your current financial situation, a realistic installment plan, and a request to freeze high interest rates or penalty fees. Providing this written offer creates a verifiable paper trail, helping you regain financial control while preventing aggressive collection tactics and protecting your long-term credit health during the settlement process.

What is a payday loan debt validation notice letter?

A payday loan debt validation notice letter is a formal document sent by a debt collector to a consumer within five days of initial contact, providing essential details about the alleged payday loan debt as required by the Fair Debt Collection Practices Act (FDCPA).

What information must be included in a payday loan debt validation notice?

The notice must include the total amount of debt owed, the name of the original payday lender, and a statement informing the consumer they have 30 days to dispute the debt's validity before it is assumed to be valid by the collector.

How long do I have to respond to a debt validation notice for a payday loan?

Consumers have exactly 30 days from the date they receive the validation notice to send a written dispute or request verification of the debt to protect their legal rights under federal law.

Can a debt collector continue calling me after I request payday loan validation?

No, if you submit a written request for validation within the 30-day window, the debt collector must cease all collection activities and communication until they provide the legally required proof of the debt.

What happens if a collector fails to send a payday loan validation notice?

If a debt collector fails to send a validation notice within five days of their first communication, they are in violation of the FDCPA, which may entitle the consumer to statutory damages and the potential dismissal of the collection claim.

Comments